-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

-13.0% -8.0% -4.0% 0.0% 2.0% 6.0% 8.0% 10.0% 13.0% 15.0% 16.0%

Deriving Beta

Asset B

Beta = 1.38

Asset A

Beta = 0.793

Asset

Returns

Market

Return

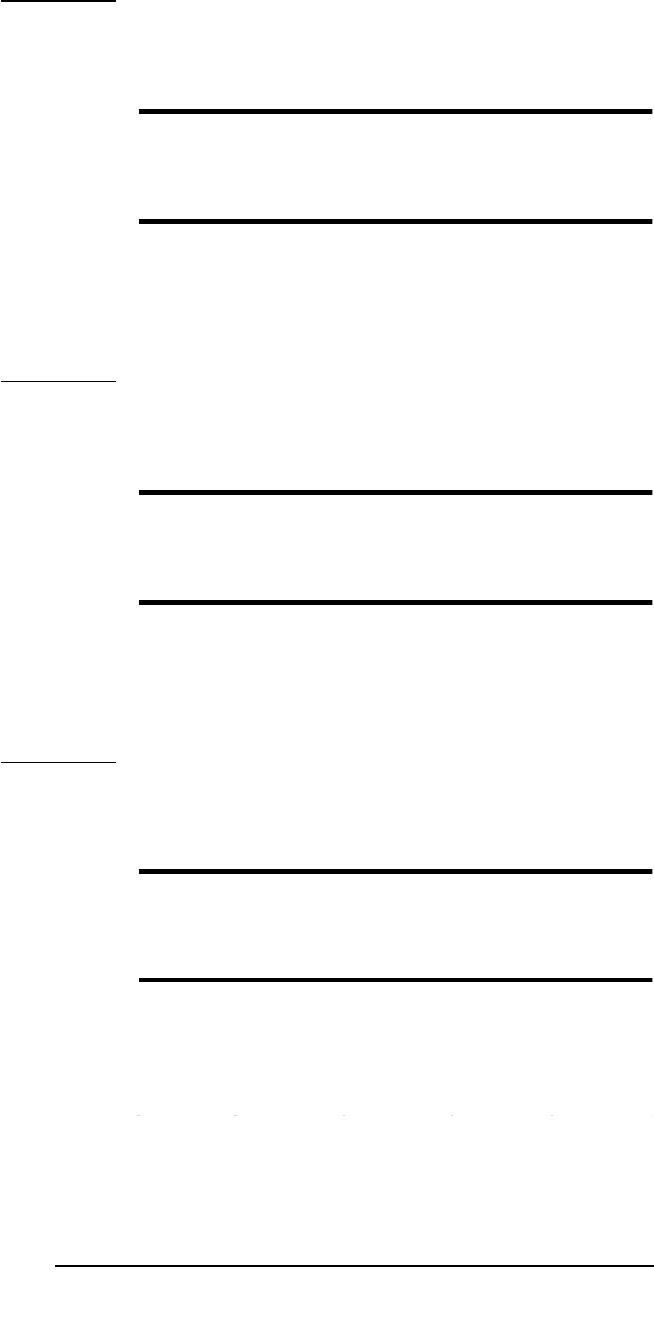

P8-17 Total, non-diversifiable, and diversifiable risk (LG 5; Intermediate)

a. and b.

c. Only nondiversifiable risk is relevant because, as shown above, building a portfolio of at least

20 securities with imperfectly correlated returns substantially reduces diversifiable risk. When

additional securities no longer reduce risk, the remaining standard deviation of David Talbot’s

portfolio is non-diversifiable. That standard deviation of returns of 6.47% (down from 14.50%).

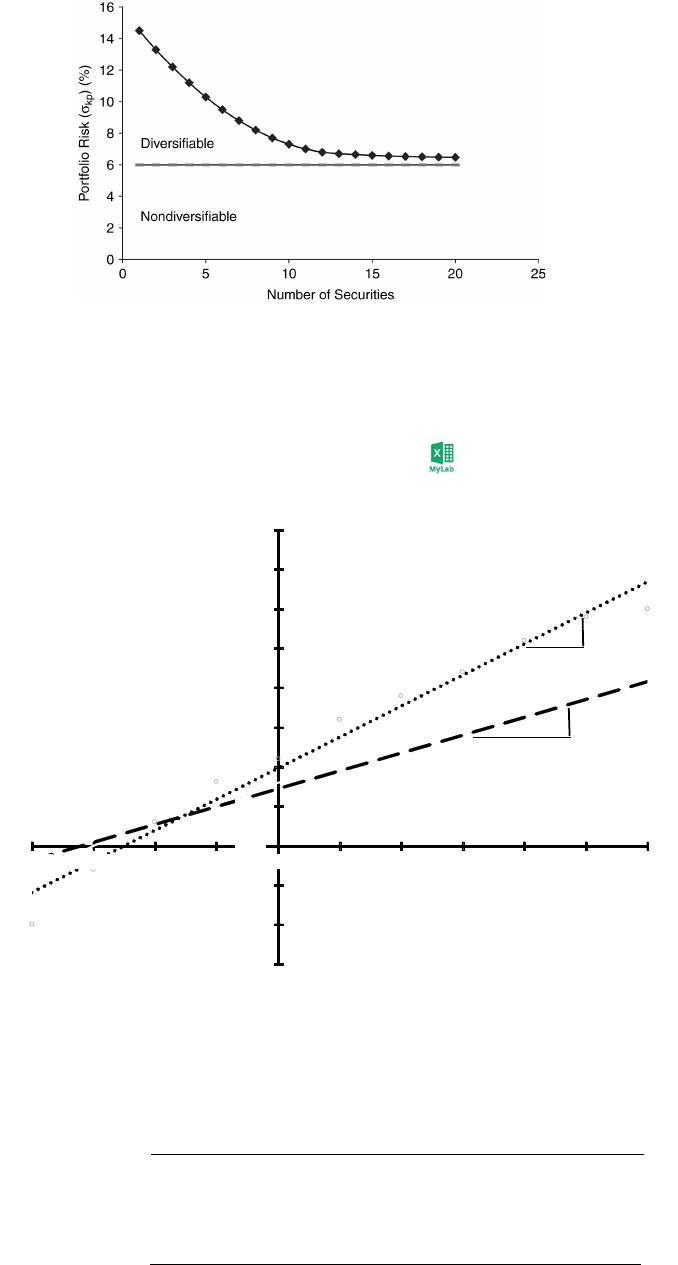

P8-18 Graphic derivation of beta (LG 5; Intermediate)

a.

b. The betas for assets A and B are the slopes of the characteristic lines above. Typically, the

slopes of these lines are estimated with a statistical technique known as linear regression. But,

slope can also be calculated given any two points on a line. Here, we can obtain slopes (i.e.,

betas) with the highest and lowest returns for each asset. Specifically:

Beta = ∆ Asset Return ∆ Market Return

BetaAsset A = Highest Return on Asset A – Lowest Return on Asset A

Highest Market Return – Lowest Market Return

= [0.19 – (–0.04)] [0.16 – (–0.13)] = 0.23 0.29 = 0.793

BetaAsset B = Highest Return on Asset B – Lowest Return on Asset B

Highest Market Return – Lowest Market Return