Market

Expected Return

Weighted Value

Return Probability Weighted Value

r

i

P

ri

r

i

x P

ri

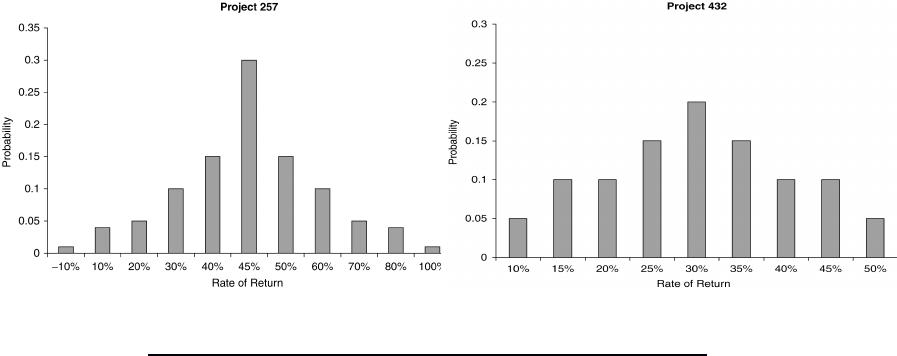

-0.10 0.010 -0.001000

0.10 0.040 0.004000

0.20 0.050 0.010000

0.30 0.100 0.030000

0.40 0.150 0.060000

0.45 0.300 0.135000

0.50 0.150 0.075000

0.60 0.100 0.060000

0.70 0.050 0.035000

0.80 0.040 0.032000

1.00 0.010 0.010000

Sum = 1.000

Sum = Average Return (r

r) = 0.450000

= 45.0%

(3) Standard deviation: , where:

ri is the return for outcome i, is the average return across all outcomes, and Pri is the

probability of outcome i.

Column → (1) (2) (3) (4) (5) (6)

Return

(r

i

)

Average

Return (r

r)

= (1) ─ (2) = (3)

2

Probability

(P

ri

)

= (4) x (5)

-0.10 0.45 -0.550 0.3025 0.010 0.003025

0.10 0.45 -0.350 0.1225 0.040 0.004900

0.20 0.45 -0.250 0.0625 0.050 0.003125

0.30 0.45 -0.150 0.0225 0.100 0.002250

0.40 0.45 -0.050 0.0025 0.150 0.000375

0.45 0.45 0.000 0.0000 0.300 0.000000

0.50 0.45 0.050 0.0025 0.150 0.000375

0.60 0.45 0.150 0.0225 0.100 0.002250

0.70 0.45 0.250 0.0625 0.050 0.003125

0.80 0.45 0.350 0.1225 0.040 0.004900

1.00 0.45 0.550 0.3025 0.010 0.003025

Sum = 0.027350

0.16538

= 16.54%

√ (Sum) = Standard Deviation (σ) =

(4) Coefficient of variation (CV) is given by σ , where σ is the standard deviation of returns on

the asset and is the average return. So:

Project 432

Return Probability Weighted Value

r

i

P

ri

r

i

x P

ri

0.10 0.050 0.0050

0.15 0.100 0.0150

0.20 0.100 0.0200

0.25 0.150 0.0375

0.30 0.200 0.0600

0.35 0.150 0.0525

0.40 0.100 0.0400

0.45 0.100 0.0450

0.50 0.050 0.0250

Sum = 1.000

Sum = Average Return (r

r) = 0.300000

= 30.0%

(3) Standard deviation: , where:

ri is the return for outcome i, is the average return across all outcomes, and Pri is the

probability of outcome i.

Column → (1) (2) (3) (4) (5) (6)

Return

(r

i

)

Average

Return (r

r)

= (1) ─ (2) = (3)

2

Probability

(P

ri

)

= (4) x (5)

0.10 0.30 -0.200 0.0400 0.050 0.002000

0.15 0.30 -0.150 0.0225 0.100 0.002250

0.20 0.30 -0.100 0.0100 0.100 0.001000

0.25 0.30 -0.050 0.0025 0.150 0.000375

0.30 0.30 0.000 0.0000 0.200 0.000000

0.35 0.30 0.050 0.0025 0.150 0.000375

0.40 0.30 0.100 0.0100 0.100 0.001000

0.45 0.30 0.150 0.0225 0.100 0.002250

0.50 0.30 0.200 0.0400 0.050 0.002000

Sum = 0.011250

0.106066

= 10.61%

√ (Sum) = Standard Deviation (σ) =

(4) Coefficient of variation (CV) is given by σ , where σ is the standard deviation of returns on

the asset and is the average return. So: CV = 0.106066 0.300 = 0.3536.

Asset F

Column → (1) (2) (3) (4) (5) (6)

Return

(r

i

)

Average

Return (r

r)

= (1) ─ (2) = (3)

2

Probability

(P

ri

)

= (4) x (5)

0.40 0.04 0.360 0.1296 0.100 0.012960

0.10 0.04 0.060 0.0036 0.200 0.000720

0.00 0.04 -0.040 0.0016 0.400 0.000640

-0.05 0.04 -0.090 0.0081 0.200 0.001620

-0.10 0.04 -0.140 0.0196 0.100 0.001960

Sum = 0.017900

0.133791

= 13.38%

√ (Sum) = Standard Deviation (σ) =

Asset G

Column → (1) (2) (3) (4) (5) (6)

Return

(r

i

)

Average

Return (r

r)

= (1) ─ (2) = (3)

2

Probability

(P

ri

)

= (4) x (5)

0.35 0.11 0.240 0.0576 0.400 0.023040

0.10 0.11 -0.010 0.0001 0.300 0.000030

-0.20 0.11 -0.310 0.0961 0.300 0.028830

Sum = 0.051900

0.227816

= 22.78%

√ (Sum) = Standard Deviation (σ) =

Asset H

Column → (1) (2) (3) (4) (5) (6)

Return

(r

i

)

Average

Return (r

r)

= (1) ─ (2) = (3)

2

Probability

(P

ri

)

= (4) x (5)

0.40 0.10 0.300 0.0900 0.100 0.009000

0.20 0.10 0.100 0.0100 0.200 0.002000

0.10 0.10 0.000 0.0000 0.400 0.000000

0.00 0.10 -0.100 0.0100 0.200 0.002000

-0.20 0.10 -0.300 0.0900 0.100 0.009000

Sum = 0.022000

0.148324

= 14.83%

√ (Sum) = Standard Deviation (σ) =

Based on standard deviation, Asset G appears to have the greatest risk.

c. Coefficient of variation (CV) is given by σ , where so σ is the standard deviation of returns on

the asset and is the average return. So:

Asset F: CV = 0.1338 0.04 = 3.345 Asset H: CV = 0.1483

0.10 = 1.483

Asset G: CV = 0.2278 2.071

As measured by the coefficient of variation, Asset F has the largest relative risk.

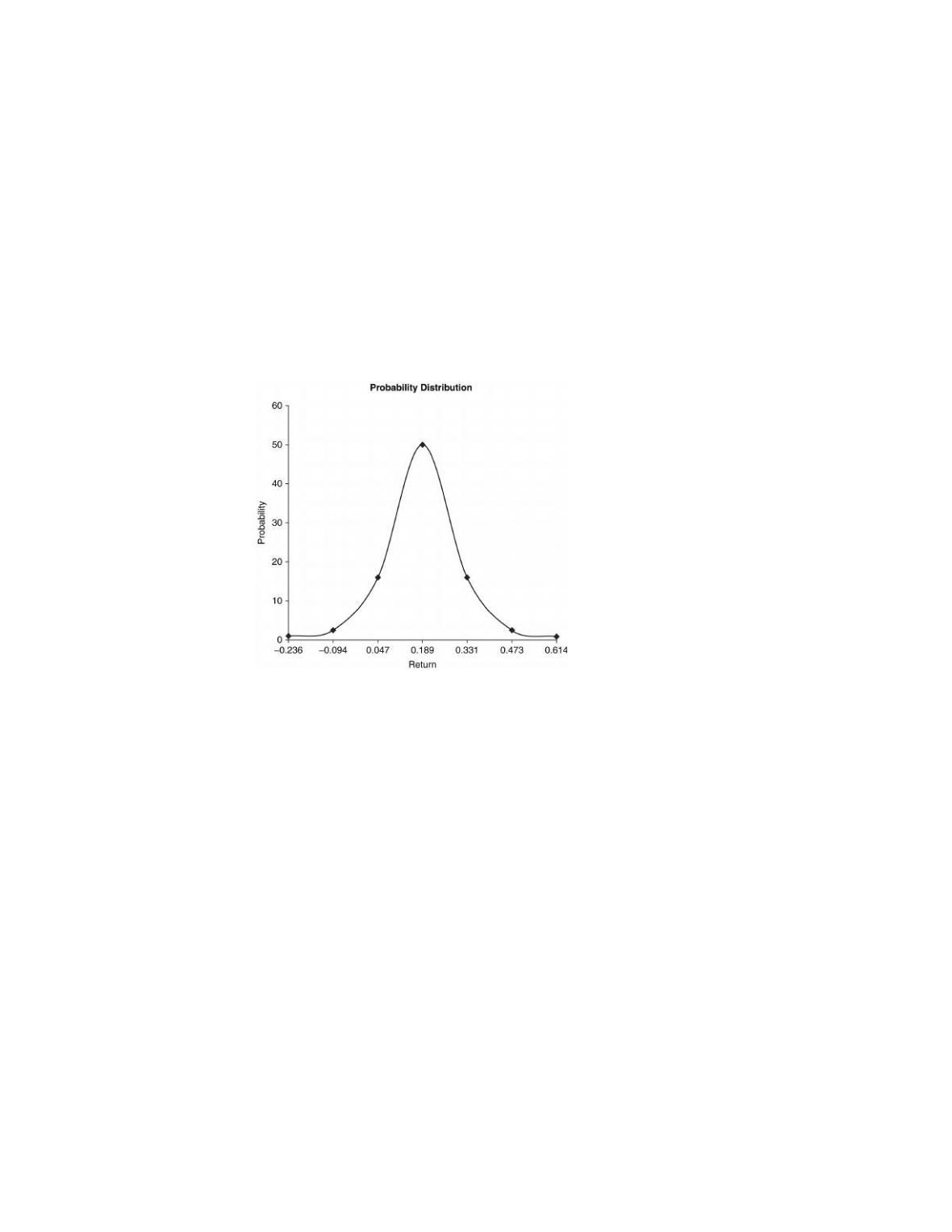

P8-12 Normal probability distribution (LG 2; Challenge)

a. Coefficient of variation: CV = σ , where so σ is the standard deviation of returns on the asset

and is the expected return. So, given the CV (0.75) and the expected return (0.189), solve for

standard deviation: 0.75

0.189 →

0.750.189 0.14175