P6-16 Bond valuation: Annual interest (LG 5; Basic)

Bond Years to

Maturity

(n)

Required

Return (r) Coupon (C) Par Value (M) Bond

Value

A 20 12% 0.11

$1,000

$110

$1,000 $925.31

$70

P6-17 Bond value and changing required returns (LG 5; Intermediate)

a. Required

Return (r) Years to

Maturity

(n) Coupon (C) Par Value (M) Bond

Value

11% 12 0.11 $1,000

$110

$1,000 $1,000.00

b.

c. When the coupon rate exceeds required return, market value exceeds par value (i.e., the bond

value equals par.

d. The required return on the bond could differ from the coupon rate because of changes in the: (i)

risk-free rate (perhaps because of changes in macroeconomic conditions), or (ii) risk of the

issuing firm.

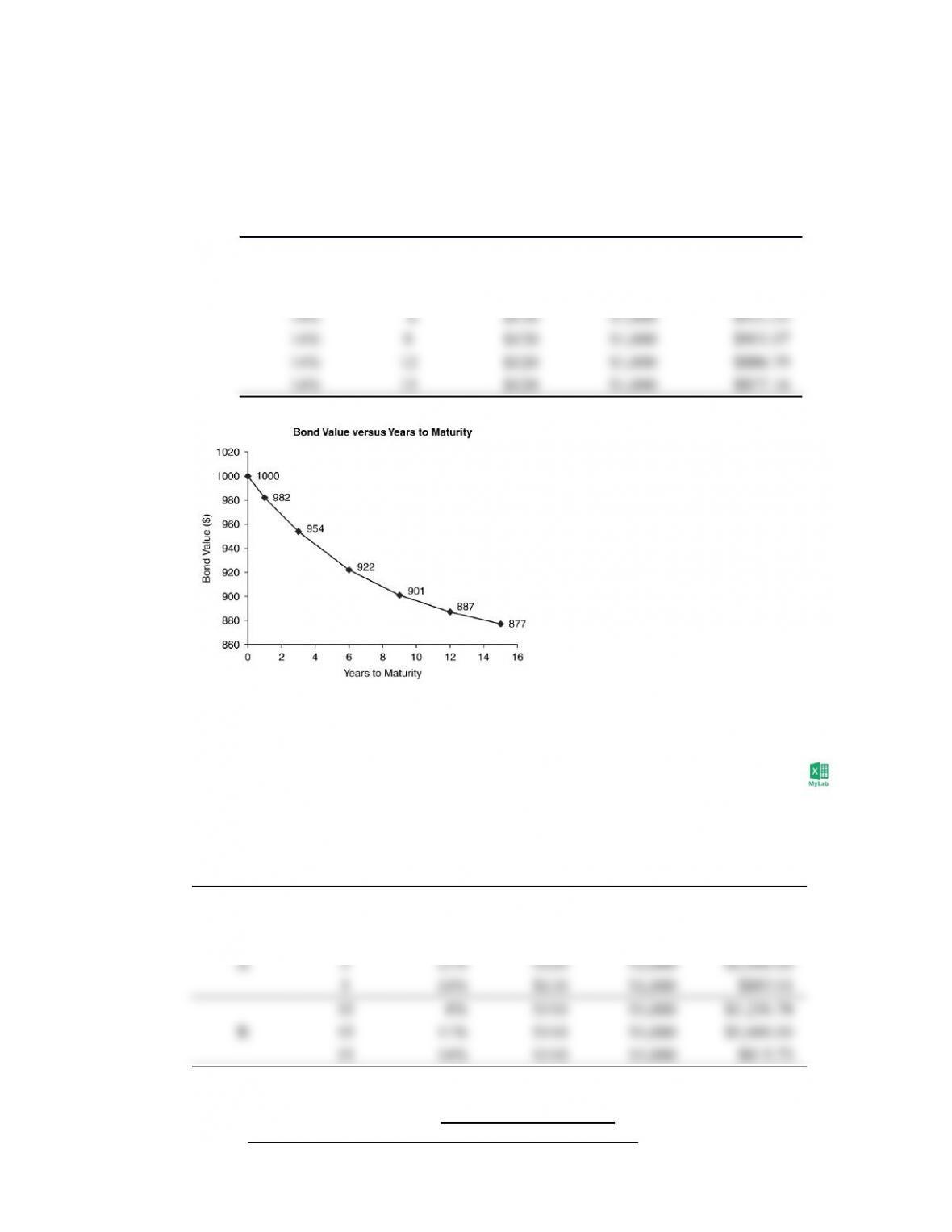

P6-18 Bond value and time: Constant required returns (LG 5; Intermediate)

a. Using the PV function in Excel with the syntax:

=pv(required return, years to maturity, coupon, par value)

Required

Return (r) Years to

Maturity (n) Coupon (C) ParValue

(M) Bond

Value

14% 1 0.12 $1,000

$120

$1,000 $982.46

14% 3 $120 $1,000 $953.57

b.

c. As can be seen in part (b), other things equal, when required return differs from the coupon rate

and remains constant to maturity, bond value will approach par value as time to maturity

declines.

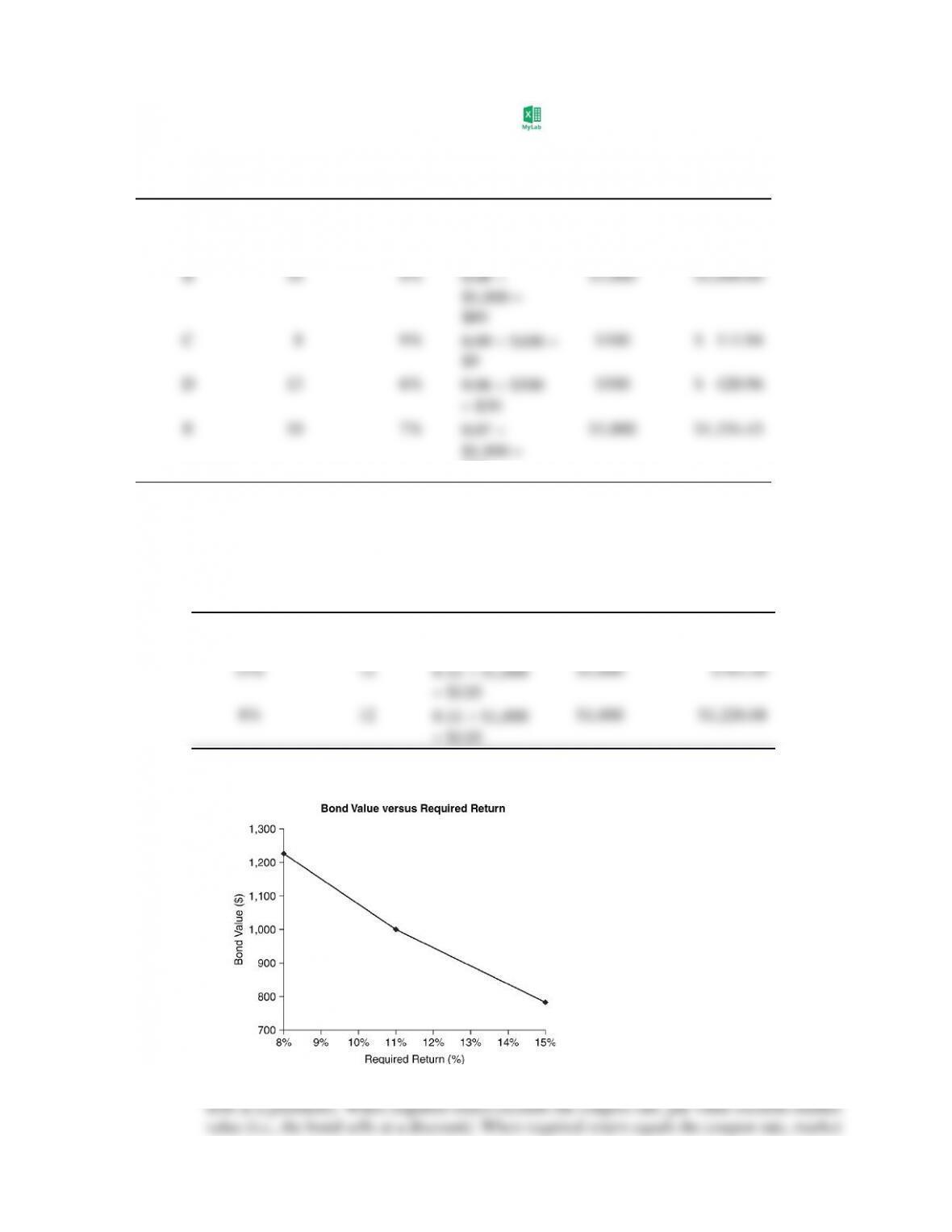

P6-19 Personal finance: Bond value and time—Changing required returns (LG 5; Challenge)

a. and b.

Bond Years to

Maturity

(n)

Required

Return (r) Coupon (C) Par

Value (M) Bond

Value

5 8% 0.11

$1,000

$110

$1,000

$1,119.78

c.

Value

Required Return Bond A Bond B

8% $1,119.78 $1,256.75

The longer the time to maturity, the more responsive bond price is to changes in required

return.

d. Lynn could minimize interest-rate risk by choosing Bond A with the shorter maturity. The price

P6-20 Yield to maturity (LG 6; Basic)

Bond A will sell at a discount to par; Bond B will sell at par value; Bond C will sell at a premium to

par; Bond D will sell at a discount to par, Bond E will sell at a premium to par.

P6-21 Yield to maturity (LG 6; Intermediate)

a. Yield to maturity (YTM) may be found in Excel using the RATE function with the following

syntax:

b. Note in part (a), the bond sells at a discount ($867.59) from par ($1,000), and YTM (7.5%)

exceeds the coupon rate (6%). Required return has risen since the bond was issued. For this

P6-22 Yield to maturity (LG 6; Intermediate)

a. In Excel, the RATE function will generate a bond’s yield to maturity (YTM). For example, for

where periods (n) is number of periods to maturity, payment (C) is coupon payment, present

b. If YTM exceeds coupon rate, the bond sells at a discount, and if the coupon rate exceeds YTM,

the bond sells at a premium. When YTM equals the coupon rate, the bond sells at par value.

P6-23 Personal finance: Bond valuation and yield to maturity (LG 2, LG 5, and LG 6; Challenge)

a. Value of the Crabbe Waste bond may be found in Excel using the PV function and n 5,

Value of the Malfoy bond may be found in Excel using the PV function and n 5,

b. The number of Crabbe Waste bonds $20,000 $952.42 21, and the number of Malfoy

bonds $20,000 $1052.60 19.

c. Annual interest income on Crabbe Waste bonds 21 bonds$63.24 per year $1,328.04, and

d. By purchasing the Crabbe Waste bonds, Mark will receive $1,328.04 in interest at the end of

years

where r is the required rate of return, n is years interest will be earned, and CF is total interest

reinvested interest may be found using the FV function in Excel with the following syntax:

e. The opportunity to reinvest coupon payments at 10% is attractive because both bonds offer

yield to maturities of only 7.5%. Although both bonds offer the same YTM, Malfoy has the

6-24 Bond valuation—Semiannual interest (LG 6; Intermediate)

To adjust the bond-valuation framework for semiannual interest, let n be the number of semiannual

P6-25 Bond valuation—Semiannual interest (LG 6; Challenge)

P6-26 Bond valuation—quarterly interest (LG 6; Challenge)

To adjust the bond-valuation framework for quarterly interest, let n be the number of quarterly

periods

P6-27 Ethics problem (LG 1; Intermediate)

This is a good question for class discussion. On the one hand, bundling ratings with other services

could reduce welfare by: (i) giving ratings agencies some market power and (ii) tempting agencies

to “tweak” ratings based on issuer willingness to buy other services. The counterargument

Case: “Evaluating Annie’s Proposed Investment in

Atilier Industries Bonds”

Case studies are available on www.pearson.com/mylab/finance.

a. Annie should convert the bonds. The value of the stock if the bond is converted is 50 shares$30 per

b. Current value of bond under different required returns:

c.

Under all three required returns for both annual and semiannual interest payments, the relationship

between required return (relative to coupon rate) and bond price (relative to par value) is the same. When

d. If expected inflation increases by 1%, required return will increase from 8% to 9%, and bond price will

e. If the ratings downgrade raises expected return from 8% to 8.75%, bond price will fall to $924.81 (i.e.,

f. In three years, the bond will be worth $1,110.61 (i.e., with n 22, r 7%, C $80, and M $1,000,

g. In ten years, the bond will be worth $1,091.08 (i.e., with n 15, r 7%, C $80, and M $1,000,

price $1,091.08)—the present value of remaining interest and principal payments. If Annie

h. Yield to maturity, given n 25, r 7%, C $80, and a bond price (V0) $983.80, is 8.154%.

i. Annie should probably not invest in the Atilier bond because:

The potential for a rating downgrade means significant risk of capital loss from a rise in the default

premium.

Spreadsheet Exercise

Answers to Chapter 6’s CSM Corporation spreadsheet problem are available on

www.pearson.com/mylab/finance.

Group Exercise

Group exercises are available on www.pearson.com/mylab/finance .

This chapter’s exercise focuses on debt. Each group will conduct Internet research to identify debt recently

issued by its shadow firm—specifically the issue’s rating and interest rate. Then, armed with this

information, each group will compare that interest rate with the rate on Treasuries with similar maturities to

infer the risk premium on the shadow firm’s debt. An important lesson from this exercise is the lack of