Solutions to Problems

P6-1 Interest-rate fundamentals: The real rate of return (LG1; Basic)

Real rate of return (r*) nominal interest rate (r) – expected inflation (i) = 1.5% 0.5% 1.0%

More precisely:

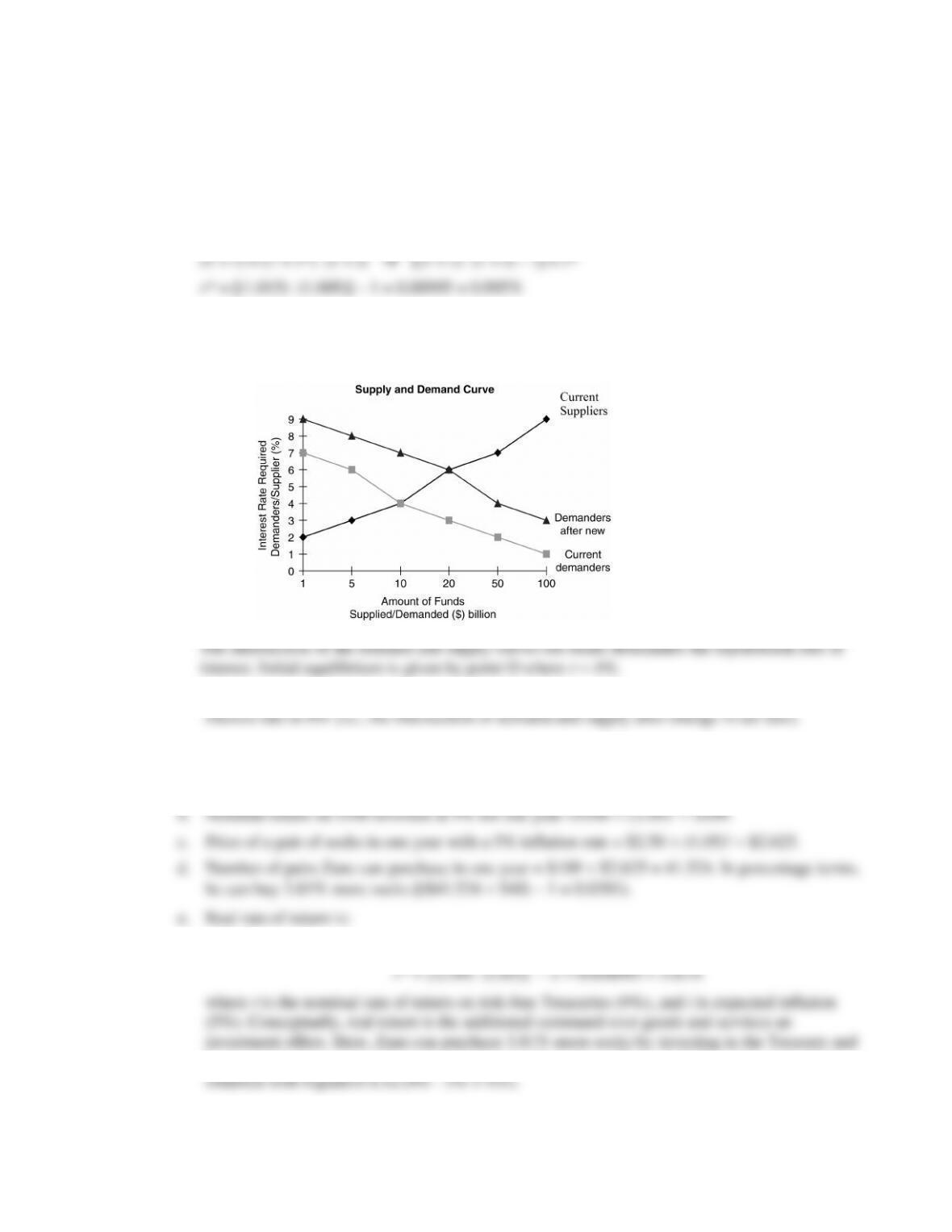

P6-2 Equilibrium rate of interest (LG 1; Intermediate)

a,b and c.

d. The change in tax law shifts the demand curve up and to the right, raising the equilibrium

P6-3 Personal finance: Real and nominal rates of interest (LG 1; Intermediate)

a. $100 budget $2.5 per pair of socks = 40 pair of socks.

(1 + r) = (1 + r*) (1 + i) → [(1 + r) (1 + i) – 1] = r*

buying socks in one year (as opposed to buying them now). Notice 3.81% is close to real rate

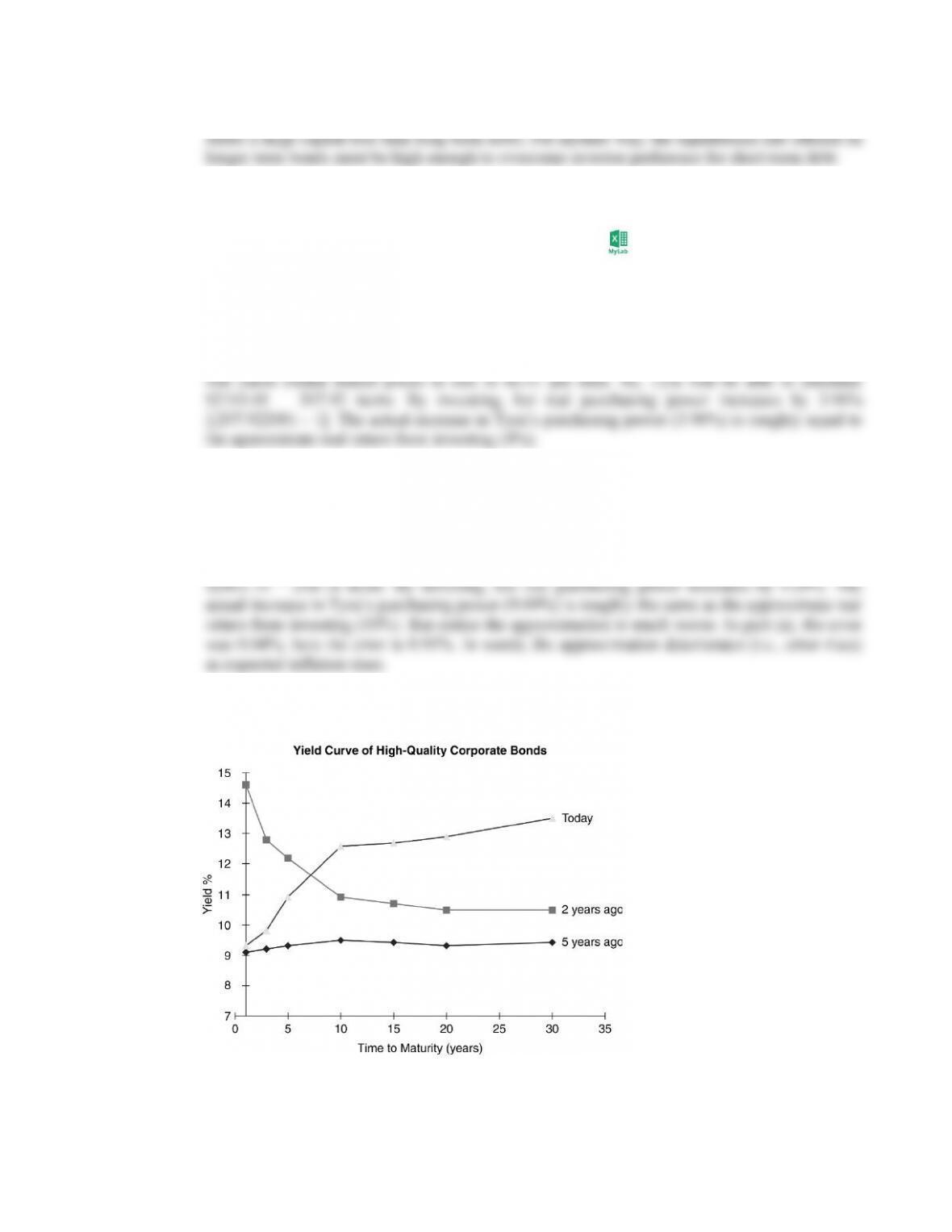

P6-4 Yield curve (LG 1; Intermediate)

a.

b. The yield curve is slightly downward sloping, which under the expectations theory of the term

rates typically fall during a recession (as demand for funds weakens).

P6-5 Nominal interest rates and yield curves (LG 1; Challenge)

a. For individual security j, nominal rate of return rj equals real rate of interest (r*) plus expected

inflation rate (i) plus risk premium on security j (RPj) or rj = r*+ i + RPj. Treasuries are risk free

(RP = 0), and expected inflation will remain 2% per year, so the real return on each Treasury is:

b. If nominal rates of interest at every maturity fall 1.5%, but expected inflation remains at 2%,

c.

The yield curve for Treasuries is upward sloping, which under the expectations theory of the

d. Followers of the liquidity-preference theory attribute the upward-sloping shape of the curve to a

strong preference by investors for short-term debt (because it is more liquid and less likely to

e. Believers in market segmentation would argue the upward slope is attributable to greater

demand (and/or weaker supply) for long-term debt.

P6-6 Nominal and real rates and yield curves (LG 1; Challenge)

a. The approximate real rate of interest is the nominal rate minus expected inflation:

r* ≈ r – i ≈ 5% – 1% ≈ 4%

If Tyra spends $200 at Dollar Barrel today where everything costs $1, she can purchase 200

items. If, however, she invests the $200, at year end she will have $210. In one year, inflation

b. The approximate real rate of interest is the nominal rate minus expected inflation:

r* ≈ r – i ≈ 20% – 10% ≈ 10%

If Tyra spends $200 at Dollar Barrel today where everything costs $1, she can purchase 200

items. If, however, she invests the $200, at year end she will have $240. In one year, inflation

will cause Dollar Barrel prices to rise to $1.10 per item. So, Tyra will be able to purchase

P6-7 Term structure of interest rates (LG 1; Intermediate)

a.

b. and c.

Five years ago, the yield curve was slightly upward sloping, suggesting (under the expectations

theory) investors expected future short-term interest rates to be only slightly higher than current

d. Consider two 10-year investment options five years ago: (i) a 10-year bond offering 9.5% or (ii)

a 5-year bond offering 9.3% and another 5-year bond in 5 years. Under the expectations theory

P6-8 Term structure (LG 1; Basic)

Consider two 2-year investment options: (i) a 2-year bond offering 5.5% or (ii) a 1-year bond

offering 5% and another 1-year bond in 1 year. Under the expectations theory of the term structure,

the options should offer the same return. Denoting expected return on a 1-year bond in one year

P6-9 Risk premiums (LG 1; Intermediate)

a. The coupon rate (3.3%) on the Anheuser-Busch (AB) bond exceeds yield to maturity (2.82%,

also the current market interest rate on bonds of equivalent risk), so the AB bond sells at a

b. The bonds mature at the same time, so any difference in yield to maturity (YTM) likely reflects

differences in perceived risk. The SH bond has the higher YTM, so it probably has the higher

risk and lower rating.

As noted, the bonds mature at the same time, so comparing their current yields reveals nothing

about the shape of the yield curve; the difference in yields is likely traceable to a difference in

P6-10 Bond interest payments before and after taxes (LG 2; Intermediate)

b. Total interest expense $70.00 per bond 2,500 bonds $175,000

the difference between before-tax and after-tax interest expense is now smaller.

P6-11 Bond prices and yields (LG 4; Basic)

a. 0.97708 $1,000 $977.08

appreciation from now to maturity on May 15, 2027.

P6-12 Personal finance: Valuation fundamentals (LG 4; Basic)

a. In years 1 – 4, $6,000 is paid on property taxes and maintenance, but $10,000 is saved on rent.

The value of any asset is the present value of its cash flows. At a 4% discount rate, the present

P6-13 Valuation of assets (LG 4; Basic)

Asse

tEnd of Year Cash Flows Discount Rate Present Value

1 $

3,000

A2 $

3,000 0.08 $7,731.29

D1–5 $

1,500 0.04 $13.395.41

5 4,000

6 1,000

P6-14 Personal finance: Asset valuation and risk (LG 4; Intermediate)

a. The value of an asset is the present value of its cash flows. So:

Discount Rates

n CFnLow Risk (r =4%) Avg. Risk (r = 7%) High Risk (r =14%)

=

b. To be sure of a good deal, Laura must take care to not understate risk. A conservative approach

c. Higher risk means discounting cash flows at a higher rate, which reduces present value (asset

value), holding cash flows and their timing constant.

P6-15 Basic bond valuation (LG 5; Intermediate)

a. The answer may be obtained in Excel using the PV function with r 10%, n 16, C (PMT)

$120, and M (FV) $1,000. Solving for PV $1,156.47.

b. Complex Systems bonds sell at a premium, meaning required return has fallen since issuance.

c. The answer may be found in Excel using the PV function with r 12%, n 16, C (PMT)

required rate of return.