Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

P5-31 Value of a single amount versus mixed stream (LG 4; Challenge)

If Gina takes $24,000 and leaves it in account earning 7% for five years, she will have $33,661.24

(PV = $24,000, n = 5, and r = 0.07) for her home. The future value of the mixed stream is:

Time Compounding Years Cash Flow Interest Rate Future Value

0 5 $ 2,000 7% $ 2,805.10

1 4 $ 4,000 $ 5,243.18

Gina should take the mixed-stream the stream of payments because its future value will be

P5-32 Value of mixed streams (LG 4; Basic)

Project A: Interpret the negative cash flow as a payment made rather than one received; discount it

as you would a positive value. Cash flows are received/paid at year end, so the $2,000

an interest rate of 12%, present value = $26,034.58.

Project C: Treat this mixed stream as two ordinary annuities—the first paying $10,000 for 5 years

with an interest rate of 12% and present value of $36,047.76 and the second paying

$8,000 for 5 years with an interest rate of 12%, and present value of $28,838.21. The

P5-33 Present value: Mixed streams (LG 4; Intermediate)

a. The present value of stream A with cash flows of CF0 $50,000 (i.e., a $50,000 payment is

made immediately), CF1 $40,000 (i.e., a $40,000 payment is received at the end of year one),

b. Both streams pay $50,000, but stream A has a large negative cash outflow right away whereas

stream B’s large negative cash outflow occurs 4 years later. Because money today is more

P5-34 Value of a mixed stream (LG 1 and LG 4; Intermediate)

a.

b.

a. Harte should still accept the offer of a 10-year mixed stream because its present value of that

mixed stream exceeds the $100,000 immediate payment.

P5-35 Value of a mixed stream (LG 1 and LG 4; Intermediate)

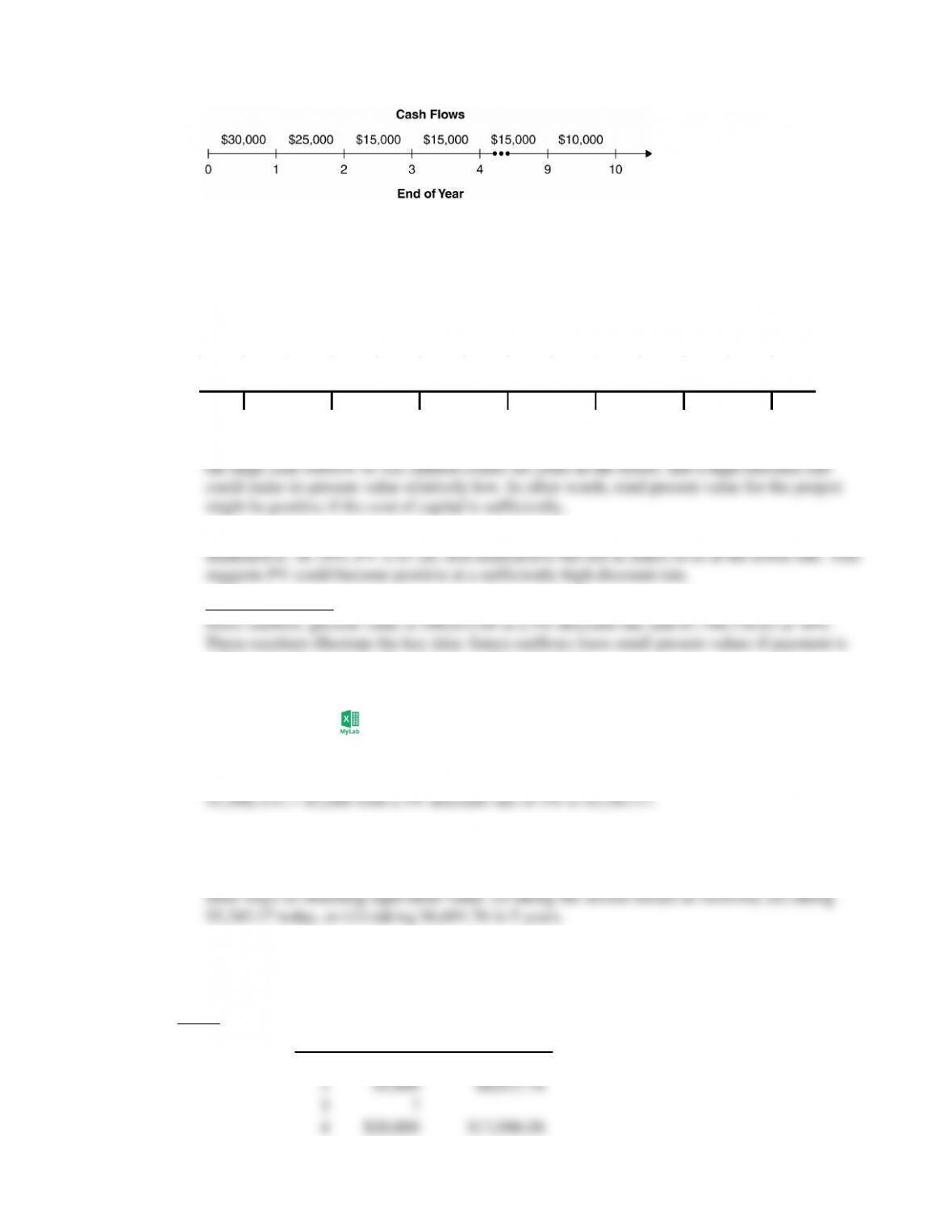

a.

Year

5

$4 million

6

-$22 million

2

$4 million

3

$4 million

4

$4 million

0

-$10 million

1

$4 million

b. Total undiscounted cash flow is $10 million. At first glance, this project seems unattractive, but

c. Project present value with a 5% discount rate is 9.10 million, which means the project is

Note to Instructors: The text contains a typo; year 1 outflow was to be $1 million. With this

sufficiently distant or the discount rate sufficiently high.

P5-36 Relationship between future value and present value-mixed stream

(LG 4; Intermediate)

a. The present value of end-of-year cash flows CF1 $800, CF2 $900, CF3 $1,000, CF4

b. FV = $5,243.17 (1 + 0.05)5 = $6,691.76.

c. Future value is $6,691.77, apart for rounding error the same as in part (b). The point here is the

d. The appropriate price for the mixed stream is its present value ($5,243.17).

P5-37 Relationship between future value and present value (LG 4; Intermediate)

Step 1: Calculate present value of known cash flows:

Year CFtPV @ 4%

1 $10,000 $9,615.38

5 $3,000 $ 2,465.78

Step 2: Subtract present values for years 1, 2, 4, and 5 from present value of entire stream:

Step 3: Calculate value in 3 years of Step 2 value today: The future value of $888.99,

P5-38 Changing compounding frequency (LG 5; Intermediate)

Future value with different compounding frequencies:

(1) Annual Semiannual

n 5, r 12%, PV $5,000 n 5 2 10, r 12% 2 6%,

Quarterly

(2) Annual Semiannual

Quarterly

n 6 4 24 periods, r 16% 4 4%, PV $5,000. Solve for FV $12,816.52

(3) Annua l Semiannual

Quarterly

Effective interest rate: reff (1 r/m)m – 1

(1) Annual Semiannual Quarterly

reff (1 0.12/1)1 – 1 reff (1 12/2)2 – 1 reff (1 12/4)4 –

1

(2) Annual Semiannual Quarterly

reff (1 0.16/1)1 – 1 reff (1 0.16/2)2 – 1 reff (1 0.16/4)4

– 1

(3) Annual Semiannual Quarterly

reff (1 0.20/1)1 – 1 reff (1 0.20/2)2 – 1 reff (1 0.20/4)4

– 1

P5-39 Compounding frequency, time value, and effective annual rates

(LG 5; Intermediate)

a. Different compounding frequencies:

A: n 10, r 3%, PV $2,500 B: n 18, r 2%,

PV $50,000

Solve for FV10 $1,628.89 Solve for FV6

$51,226.08

b. Effective interest rate: reff (1 r%/m)m – 1

1

reff (1 0.03)2 1 reff (1 0.02)6 1

– 1

reff (1 0.05)1 1 reff (1 0.04)4 1

= reff 0.17 17%

c. Effective interest rates rise relative to stated rates as compounding frequency rises.

P5-40 Continuous compounding (LG 5; Intermediate)

FVcont. PVer

n (where e 2.718282, r = annual interest rate, and n = number of years)

P5-41 Personal finance: Compounding frequency and time value (LG 5; Challenge)

a. (1) Annually: n 10; r 8%, PV $2,000. FV $4,317.85.

reff (1 0.08)1 1 reff (1 0.08)2 1

0.0833 8.33%

c. Continuous compounding yields $133.23 more than annual compounding over 10 years.

d. The more frequent the compounding, the larger the future value. Part (a) demonstrates this idea

with larger future values as compounding increases from annual to continuous. Because future

P5-42 Personal finance: Annuities and compounding (LG 3 and LG 5; Intermediate)

a. For the ordinary annuity with annual compounding: n 10, r 8%, PMT $300, and solve for

compounding: n 10 4 40; r 8 4 2%; PMT $75, and solve for FV $4,530.15.

b. The sooner a deposit is made, the sooner the funds can earn interest. Thus, the sooner the

deposit and more frequent the compounding, the larger the future sum.

P5-43 Deposits to accumulate growing future sum (LG 6; Basic)

Using the framework for future value of an annuity:

Case Terms Given

Information Payment

A 12%, 3 years n 3, r 12, FV $5,000 $1,481.74

P5-44 Personal finance: Creating a retirement fund (LG 6; Intermediate)

a. Given n 42, r 8%, and FV $220,000, solve for PMT $723.10.

P5-45 Personal finance: Accumulating a growing future sum (LG 6: Intermediate)

Step 1: Determining cost of home in 20 years: Given n 20, r 6%, and PV $185,000, solve for

Step 2: Determining how much to save annually to afford home: Given n 20, r 10%, and FV

P5-46 Personal finance: Inflation, time value, and annual deposits (LG 2, LG 3, and LG 6; Challenge)

a. n 25, r 5%, PV = $200,000. Solve for FV25 $677,270.99.

P5-47 Loan payment (LG 6; Basic)

A: Given n 3, r 8%, and PV $12,000, solve for PMT $4,656.40.

P5-48 Personal finance: Loan-amortization schedule (LG 6; Intermediate)

a. Treat the problem like an ordinary annuity with n= 3, r = 4%, PV = $45,000, and solve for

b. End of

Year Loan

Payment Beginning-of-

Year Principal Payments

Interest Principal

1 $16,215.68 $45,000.00 $1,800.00 $14,415.68

c. The interest portion falls each period because some principal is being repaid (so the same

interest rate is applied to smaller principal).

P5-49 Loan-interest deductions (LG 6; Challenge)

a. Use the ordinary annuity framework with n 3, r 13%, PV (loan amount) $10,000, and

solve for PMT. Annual end-of-year loan payments = $4,235.22.

b. and c.

End of

Year Loan

Payment Beginning-of-

Year Principal Payments

Interest Principal

1 $4,235.22 $10,000.00 $1,300.00 $2,935.22

P5-50 Personal finance: Monthly loan payments (LG 6; Challenge)

a. Use the ordinary annuity framework with n 12 3 = 36, r 6% 12 = 0.005,

b. Use the ordinary annuity framework with n 36, r 4% 12 = 0.003333,