Solutions to Problems

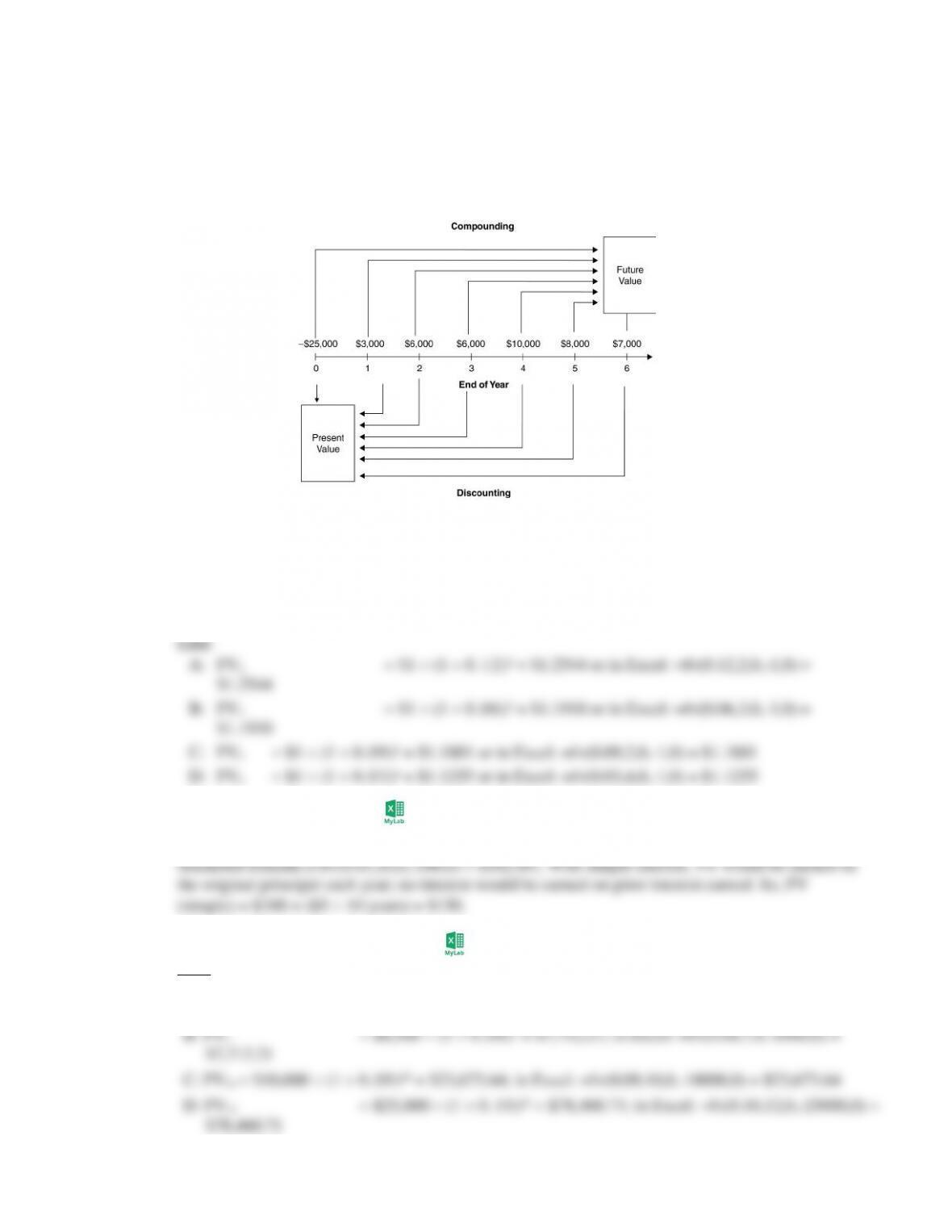

P5-1 Using a time line (LG 1; Basic)

a, b, and c

d. Financial managers rely more on present value than future value because their decisions are

typically made before a project starts (i.e., at time zero).

P5-2 Future value calculation (LG 2; Basic)

To find future value in each case, plug $1 for PV as well as the given interest rates (r) and

compounding periods (n) into FVn PV (1 r)n.

P5-3 Future value (LG 1; Basic)

With compound interest: FVn PV (1 r)n = $100 (1 0.05)10 =$162.89, or in Excel the

P5-4 Future values (LG 2; Intermediate)

Case

A: FV20 $200 (1 0.05)20 = $530.66; in Excel: =fv(0.05,20,0,-200,0) =

$530.66

E: FV5 $37,000 (1 0.11)5 = $62,347.15. In Excel: =fv(0.11,5,0,-37000,0) =

P5-5 Personal finance problem: Compounding (LG 2; Intermediate)

a. (1) FV3 = $1,500 (1 + 0.03)3 = $1,837.56. In Excel: =fv(0.03,3,0,-1500,0) = $1,837.56

b. (1) Interest earned, years 1 through 3 = FV3 PV0 = $1,837.56 $1,500 = $337.56

c. The amount of interest earned in the second three-year period ($413.53) exceeds the amount

earned in the first ($337.56), and interest earned in the third three-year period ($506.59)

P5-6 Personal finance: Time value (LG 2; Challenge)

a. To find car price in five years with 2% inflation, use future-value equation with PV = $14,000,

b. The car will cost $1,576.01 more with a 4% inflation rate than an inflation rate of 2% – an

c. Again, use the future-value equation for both steps. Specifically, for the first two years:

P5-7 Personal finance: Time value (LG 2; Challenge)

To find the future value of $10,000 today, invested at 9% annual interest for 40 years:

difference is the magic of compounding (i.e., earning interest on interest).

P5-8 Personal finance: Time value (LG 2; Challenge)

The problem asks students to use a financial calculator or Excel spreadsheet to obtain

approximations. Exact answers are offered below. Using the future-value framework (5 years,

$15,000 = FV5), solve for r with the various starting present values.

a. FVn = PV (1 + r)n

b. FVn = PV (1 + r)n

c. FVn = PV (1 + r)n

P5-9 Personal finance: Single-payment loan repayment (LG 2; Intermediate)

To find the amount that must be repaid, use the future-value framework with $200 as the present

value, 8.5% the interest rate, and various values for n.

a. In one year: FVn = PV (1 + r)n = $200 (1 + 0.085) = $217.00

P5-10 Present value calculation (LG 2; Basic)

In all cases, solve for present value using the present-value equation: PV = FVn (1 + r)n

Case

A PV = $1 (1 + 0.02)4 $0.9238 or in Excel: =pv(0.02,4,0,-1,0) = $0.9238

P5-11 Present values (LG 2; Basic)

Case

A: PV = $7,000 (1 + 0.12)4 $4,448.63; in Excel: =pv(0.12,4,0,-7000,0) = $4,448.63

P5-12 Present value concept (LG 2; Intermediate)

a. PV = FVn (1 + r)n = $6,000 (1 + 0.12)6 $3,039.79

P5-13 Personal finance: Time Value (LG 2; Basic)

b. Jim should pay no more than $408.15 for $500 in three years if his discount rate is 7%.

P5-14 Time value: Present value of a lump sum (LG 2; Intermediate)

The state will sell bonds at a price equal to present value of cash flows. The bond can be converted

P5-15 Personal finance: Time value and discount rates LG 2; Intermediate

a. (1) PV = FVn (1 + r)n = $1,000,000 (1 + 0.06)10 $558,394.78

c. As the discount rate increases, present value decreases because of the higher opportunity cost

associated with the higher rate. Moreover, the longer the time until the lottery payment is

P5-16 Personal finance: Time value comparisons of single amounts (LG 2; Intermediate)

a. (A) PV = FVn (1 + r)n = $28,500 (1 + 0.09)3 $22,007.22

b. The benchmark for an acceptable alternative is $23,000, what you would have to pay today to

benefits exceeding marginal cost) and should, therefore, be undertaken.

c. Although alternatives (B) and (C) are both attractive, (C) is the most attractive if only one can

P5-17 Personal finance: Cash flow investment decision (LG 2; Intermediate)

The general approach is to determine the present value of each investment and then compare that

present value to the purchase price. All investments with present values exceeding price should be

purchased. As always, the formula for present value is PV = FVn (1 + r)n.

If limited to one investment, Tom should purchase option A because marginal benefits exceed price

P5-18 Calculating deposit needed (LG 2; Challenge)

Step 1: Determine future value of initial deposit at the end of the 7 years.

Step 3: Calculate the present value of second deposit at the end of year 3 (i.e., actual amount

deposited at that time):

for 4 years. To solve for the missing payment:

value of the missing payment.

P5-19 Future value of an annuity (LG 3; Intermediate)

a. The future value of an ordinary annuity is given by:

where CF1 is the equal end-of-period payments, r the interest rate, and n the number of periods.

Case

A FV10 = $2,500 {[(1 + 0.08)10 $36,216.41

Future value of an ordinary annuity may also be found with a financial calculator or

The future value of an annuity due is given by:

where CF0 is the equal beginning-of-period payments, r the interest rate, and n the number of

periods.

Case

A FV10 = $2,500 {[(1 + 0.08)10 (1 + 0.08)

Again, future value of an annuity due may be found with a financial calculator or spreadsheet

b. The annuity due has a greater future value in each case. By making deposits at the beginning

rather than the end of the year, each cash flow enjoys one additional year of compounding.

P5-20 Present value of an annuity (LG 3; Intermediate)

a. Using the formula for present value of an ordinary annuity:

where CF1 is the equal end-of-period payments, n the number of periods, and r the interest rate

per period.

Case

A PV3 = ($12,000 [1 (1 + 0.07)-3 $31,491.79

Present value of an ordinary annuity may also be in Excel using the bracketed formula [=PV(r,

The present value of an annuity due is given by:

where CF0 is the equal beginning-of-period payments, r the interest rate, and n the number of

periods.

Case

A PV3 = ($12,000 [1 (1 + 0.07)-3 (1 + 0.07)

$33,696.22

$850,596.89

0.10)$93,821.97

Present value of an annuity due may be in Excel with the bracketed formula

b. The annuity due has the greater present value in each case. By making deposits at the beginning

rather than the end of the year, each cash flow is discounted one less year.

P5-21 Personal finance: Time value—annuities (LG 3; Challenge)

a. The future value of the ordinary annuity is $32,951.99 when the interest rate is 6% and

b. When the interest rate is 6%, the ordinary annuity has a higher future value, but when the

when the interest rate is 6% and $15,545.75 when the interest rate is 10%.

d. At 6% the ordinary annuity has a higher present value, but at 10% the annuity due has the

higher present value.

e. Ignoring the time value of money, the ordinary annuity pays out more cash ($25,000 vs.

that cash faster.

P5-22 Personal finance: Retirement planning (LG 3; Challenge)

a. The correct framework is the future value of an ordinary annuity. Specifically, FV with end-of-

b. If contributions begin 10 years later (i.e., are made for thirty years), but all other information

c. The opportunity cost of delaying deposits for 10 years is the difference in future values in parts

deposits and (ii) 10 years of lost compound interest.

d. The correct framework is the future value of an annuity due. Specifically, future value of an

annuity due—given annual end-of-year contributions of $2,000, an interest rate of 10% and 40

P5-23 Personal finance: Value of a retirement annuity (LG 3; Intermediate)

The correct framework is present value of an ordinary annuity, with $12,000 payments for 25 years

P5-24 Personal finance: Funding your retirement (LG 2, 3; Challenge)

a. At age 65, Emily will be one year away from making the first of 25, $50,000 annual

withdrawals (i.e., she will take out $50,000 each birthday from age 66 to age 90). Imagine

years, plug FV20 = $421,087.23, r = 11%, and n = 20 into Equation 5.2 in the text (i.e. PV =

b. The approach is the same as in part (a) except the present value of the 25-year, $50,000 annuity

on Emily’s 65th birthday is calculated with a discount rate of 8% rather than 11%. Now,

c. In part (b) Emily needs to invest $66,201.71 today to reach her retirement-income goals. If she

deposits $75,000 instead, the difference ($8,798.29) will compound at 11% for 20 years then at

Correct answers may be obtained another way. Consider part (b). Suppose Emily deposits

$75,000 today at 11% to reach a value of $604,673.36 in 20 years [FV = $75,000 (1.11)20].

P5-25 Personal finance: Value of an annuity vs. a single amount (LG 2 and LG 3; Intermediate)

a. n 25, r 5%, PMT $40,000; solve for PV $563,757.78. Take the annuity because its

present value exceeds the lump sum by $63,757.58.

exceeds the present value of the annuity by $33,856.67.

c. View this problem as a $500,000 investment offering a 25-year annuity of $40,000, and

P5-26 Perpetuities (LG 3; Basic)

Case Equation Present Value

A $20,000 0.08 $250,000

P5-27 Perpetuities (LG 3; Intermediate)

a. The present value of the perpetuity is $100 0.07 = $1,428.57. To see this is the correct

b. This problem is identical to part (a) except here you also get $100 immediately. If the

c. This situation is the same as part (a) except here you must wait 2 additional years

before the $100 payments begin. The perpetuity in part (a) is worth $1,428.57; to obtain

P5-28 Perpetuities (LG 3; Intermediate)

a. Present value is $75 1.10 = $68.18.

b. In 100 years, the payment will be $75 1.0499 = $3,642.18. The present value of this

c. Using Equation 5.8 in the text, the present value of a perpetuity initially paying $75 but

d. Payments further in the future have a lower present value, with present value going to

P5-29 Personal finance: Creating an Endowment (LG 4; Intermediate)

a. Cost next year = $600 (1.02) = $612.

b. The present value of an annuity paying $612 initially but growing at 2% per year with a

P5-30 Value of a mixed stream (LG 4; Challenge)

a.

Stream Year Compoundi

ng Years Cash flow Interest Rate Future

Value

1 2 $ 900 $ 1,128.96

1 4 $30,000 $ 47,205.58

2 3 25,000 35,123.20

1 3 $ 1,200 $1,685.91

C 2 2 1,200 1,505.28

b. If payments are made at the beginning of each period, the present value of each end-of-period

cash flow should be multiplied by (1 r) to obtain present values for beginning-of-period cash