Solutions to Problems

P4-1 Depreciation (LG 2; Basic)

Depreciation Schedule

Year Cost (1) Percentages

from Table 4.2 (2) Depreciation

(3) = [(1) (2)]

Asset A

Research Equipment

1 $17,000 33% $5,610

3 $45,000 19% $8,550

P4-2. Depreciation (LG 2; Basic)

Depreciation Schedule – Cork stopper machine

Year (1) Cost (2) Table 4.2

Percentages Depreciation

(3) = (1) (2)

1 $10,000 33% $3,300

P4-3. MACRS depreciation expense, taxes, and cash flow (LG 2 and LG 3; Challenge)

a. Depreciation expense $80,000 0.20 $16,000 (MACRS depreciation percentages can be

P4-4 Depreciation and cash flow (LG 2 and LG 3; Intermediate)

a. Operating cash flow (OCF) = [Earnings before interest and taxes Tax rate)]

Depreciation

Alternatively, using a tax rate of 40%, which does not reflect the changes enacted in the Tax

Cuts and Jobs Act, the OCF would be $79,680.

b. Depreciation expense is an accounting entry to smooth the cost of an asset over time; there is

P4-5 Classifying cash inflows and outflows (LG 3; Basic)

Notes:

(i) Any reduction in an asset is a cash inflow because that cash has been released for another

purpose. Hence, the $300 decline in cash below is an inflow.

payable

n

Long-term

dividends

1,000 I

Repurchase

900 O

assets

stock

P4-6. Finding operating and free cash flows (LG 2; Intermediate)

a. Net operating profit after taxes (NOPAT)

Earnings before interest and taxes (EBIT) [1 Tax rate (T)] $2,700 (1 0.21) $2,133.

b. OCF NOPAT Depreciation $2,133 $1,600 $3,733

c. FCF OCF Net fixed asset investment (NFAI) Net current asset investment (NCAI)

NFAI = ∆Net fixed assets Depreciation = ($14,800 $15,000) $1,600 = $1,400

(Or again, if the tax rate is 40%, FCF becomes $420.)

d. Keith Corporation has positive cash flows from operating activities. Operating cash flow (OCF)

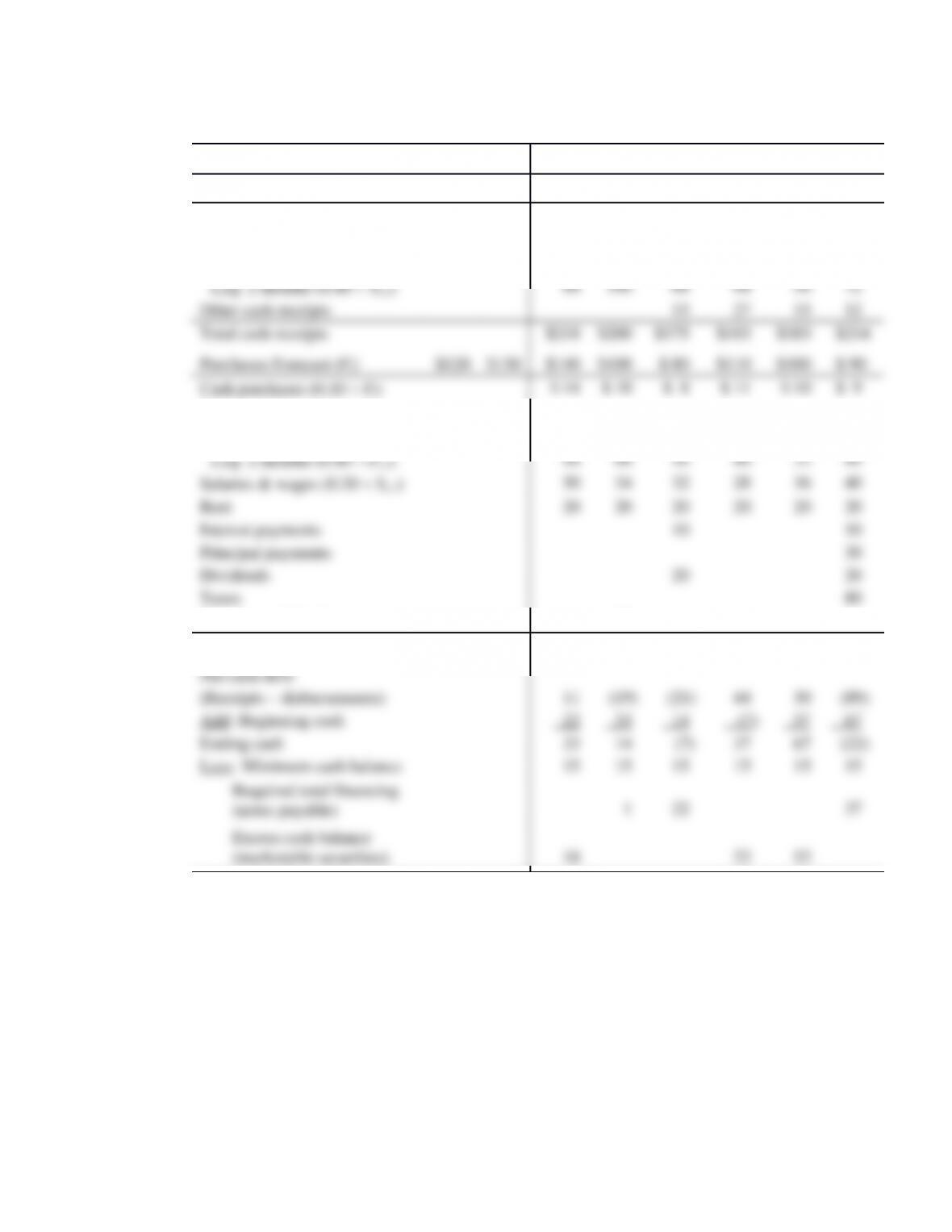

P4-7. Statement of cash flows (LG 3; Intermediate)

a. The change in stockholders equity of $157 on the balance sheet is entirely traceable to a $157

increase in retained earnings. No other equity accounts changed in 2019. From Tables 4.4, 4.5

and 4.6, the increase in retained earnings may be broken down as follows:

On the cash-flow statement, the entry for net profits after taxes appears as a positive $237 (cash

inflow) under “cash flow from operations.” The entry common/preferred dividends paid

Note: In the first-run printing of this book, the change in retained earnings was $100, not $157.

b. Other values are possible. For, example, the company could sell new stock for cash payment.

P4-8 Cash receipts (LG 4; Basic)

April May June July August

Sales (St) $65,000 $60,000 $70,000 $100,000 $100,00

0

Cash sales (0.50 St)$32,500 $30,000 $35,000 $50,000 $50,000

Collections:

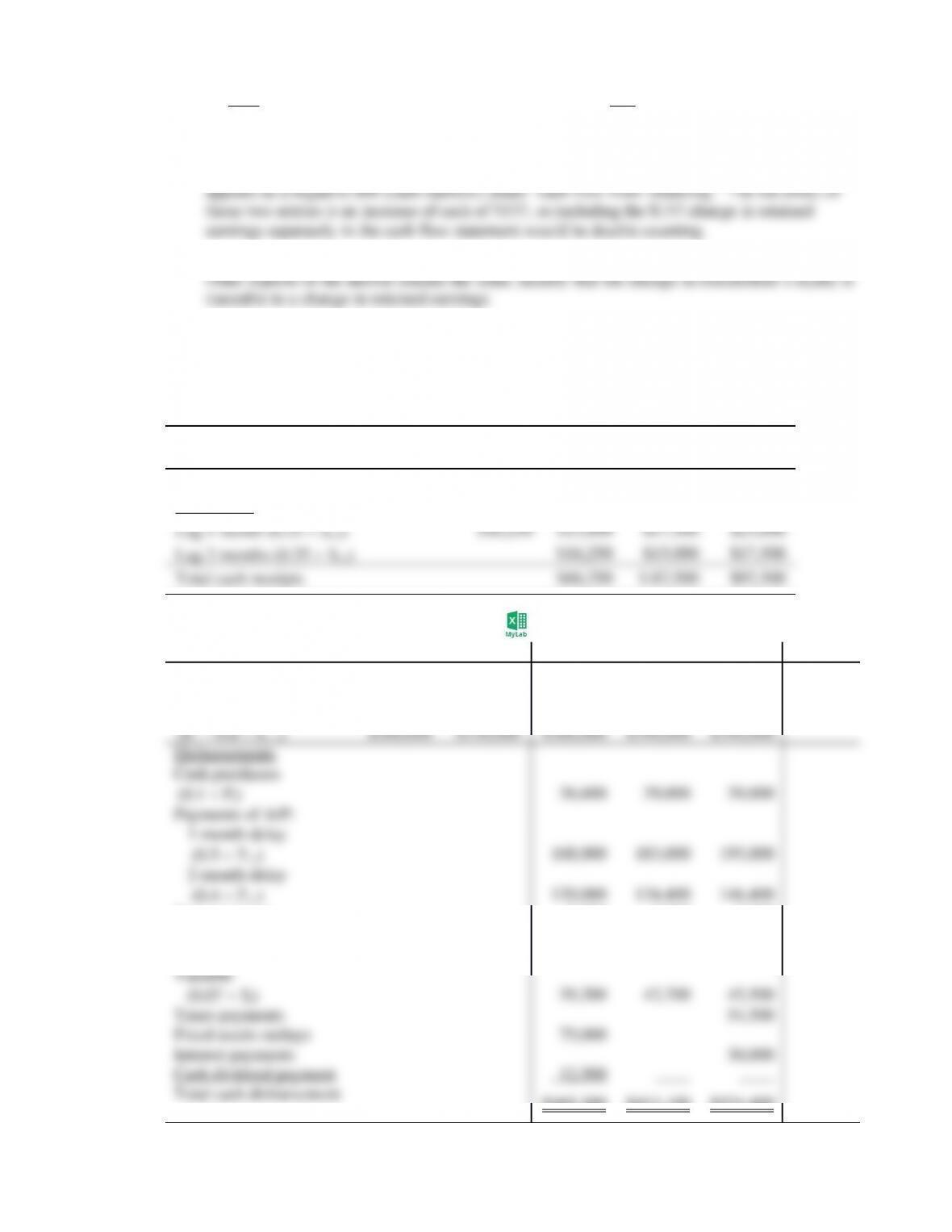

P4-9. Cash disbursement schedule (LG4; Basic)

February March April May June July

Sales (St) $500,000 $500,000 $560,000 $610,000 $650,000 $650,00

0

Purchases

Rent payments 8,000 8,000 8,000

Wages & salary

Fixed 6,000 6,000 6,000

P4-10. Cash budget (LG 4; Basic)

March April May June July

Sales $50,000 $60,000 $70,000 $80,000 $100,000

Cash sales (0.2 St)) $10,000 $12,000 $14,000 $16,000 $20,000

Lag 1 month (0.6 St-1)36,000 42,000 48,000

Rent 3,000 3,000 3,000

March April May June July

Total cash receipts $62,000 $72,000 $84,000

Total cash disbursements 59,000 93,000 97,000

Net cash flow $ 3,000 ($21,000) ($13,000)

P4-11. Personal finance: Preparation of cash budget (LG 4; Basic)

a. Sam and Suzy Sizeman—Personal Budget

October – December 2020

October November December

Income

Take-home pay $4,900 $4,900 $4,900

Expenses Percent

Housing 30.0% $1,470 $1,470 $1,470

Personal care 2.0% 98 98 98

Entertainment 6.0% 294 294 1,500

Note: Amounts are rounded.

b. December is a deficit month.

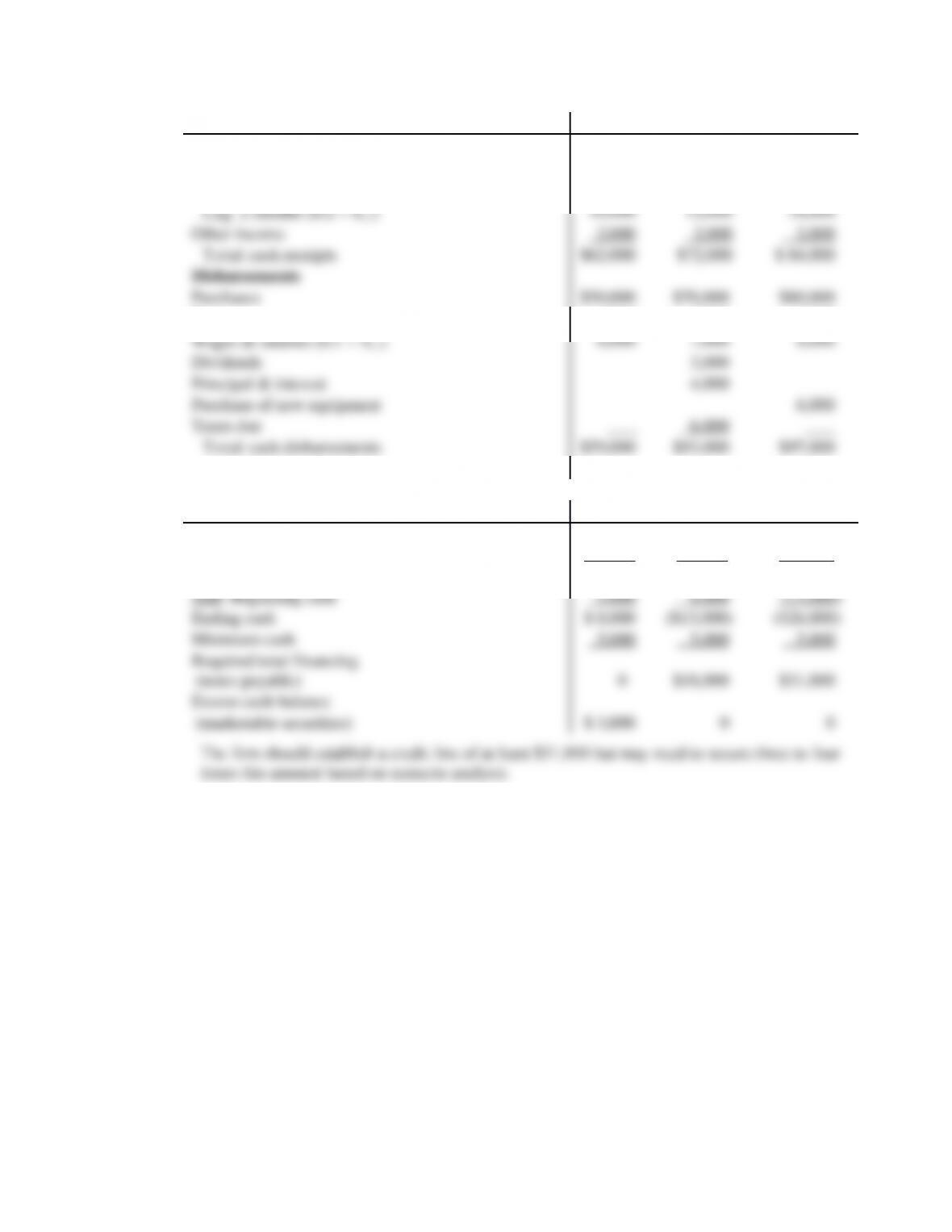

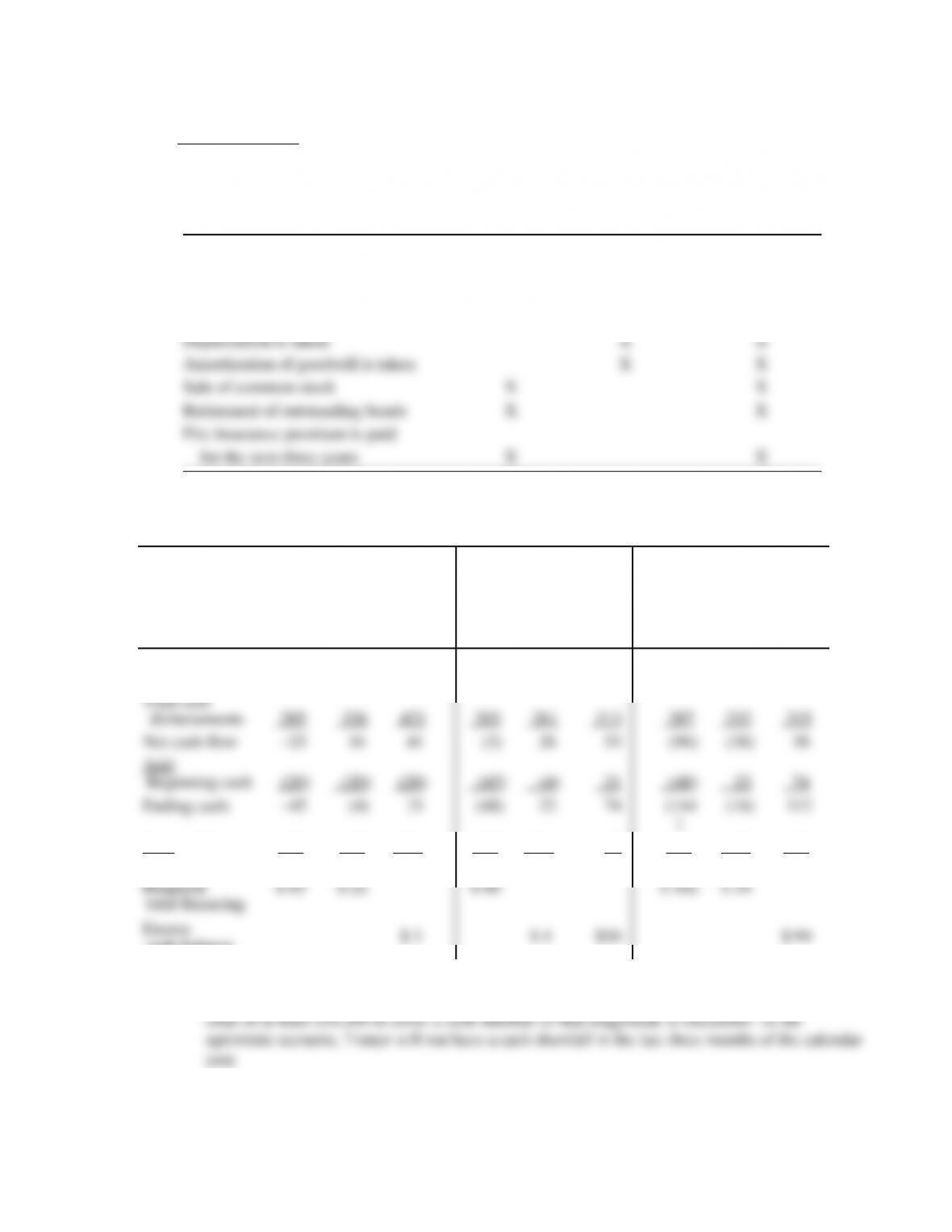

P4-12. Cash budgeting: Advanced (LG 4; Challenge)

a. and b. Xenocore, Inc.($000)

Sept. Oct. Nov. Dec. Jan. Feb. Mar. Apr.

Forecast of Sales St)$210 $250 $170 $160 $140 $180 $200 $250

Cash sales (0.20 St)$ 34 $ 32 $ 28 $ 36 $ 40 $ 50

Collections

Lag 1 month (0.40 St-1)100 68 64 56 72 80

Payments

Lag 1 month (0.50 Pt-1) 75 70 50 40 55 50

Purchases of fixed assets 25

Total cash disbursements $207 $219 $196 $139 $153 $303

b. The line of credit should be at least $37,000 to cover the maximum borrowing needs (for

April).

P4-13. Cash flow concepts (LG 4; Basic)

Note to instructor: There are a variety of possible answers to this problem, depending on student

assumptions. The question is designed to provoke discussion of differences among cash flows,

income, and assets.

Transaction Cash

Budget Pro Forma

Income Statement Pro Forma

Balance Sheet

Cash sale X X X

Credit sale X X X

Accounts receivable are collected X X

Asset with a five-year life is purchased X X

P4-14 Cash budget: Scenario analysis (LG 4; Intermediate)

a. Trotter Enterprises, Inc.—Multiple Cash Budgets ($000)

OCTOBER NOVEMBER DECEMBER

Pessi-

mistic Most

Likely Opti-

mistic Pessi

–

mistic

Mos

t

Likel

y

Opti-

mistic Pessi

–

misti

c

Most

Likel

y

Opti-

mistic

Total

cash receipts $260 $342 $462 $200 $287 $366 $191 $294 $353

Less minimum

cash balance 18 18 18 18 18 18 18 18 18

cash balance

b. Under the pessimistic scenario, Trotter will need a credit line of at least $162,000 to cover a

cash shortfall of that amount in December. In the most likely scenario, Trotter will need a credit

P4-15 Multiple cash budgets: Scenario analysis (LG 5; Intermediate)

a. and b. Brownstein, Inc. Multiple Cash Budgets ($000)

1st

Month

2nd

Month

3rd Month

Pessi-

mistic

Most

Likely

Opti-

mistic

Pessi-

misti

c

Most

Likel

y

Opti-

misti

c

Pessi

–

misti

c

Most

Likel

y

Opti-

mistic

Sales $ 80 $100 $120 $ 80 $100 $120 $80 $100 $120

Asset sale 8 8 8

Add:

Beginning cash 0 0 0 (14) 5 24 (23) 15 53

c. Considering the extreme values reflected in the pessimistic and optimistic outcomes allows

Brownstein to plan borrowing or short-term investments carefully. For example, the firm knows

P4-16 Pro forma income statement (LG 5; Intermediate)

a. Pro Forma Income Statement—Metroline Manufacturing, Inc.

Year Ending December 31, 2020 (Percent-of-Sales Method)

Sales $1,500,000

Less: Cost of goods sold (0.65 sales) 975,000

Gross profits $ 525,000

Less: Operating expenses (0.086 sales) 129,000

Note: Operating expense percentage was found by dividing 2019

operating expenses ($) by sales ($), and rounding to third

decimal place.

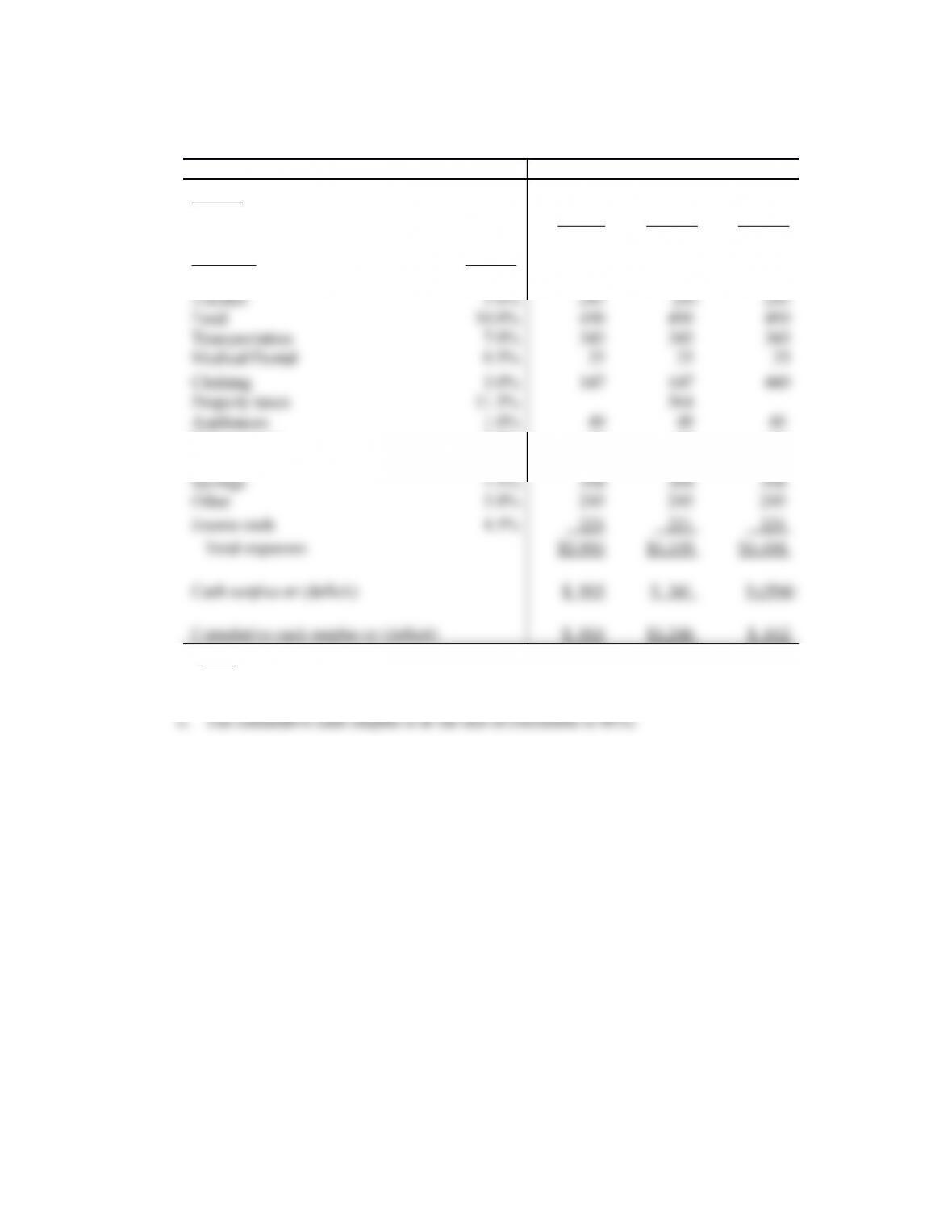

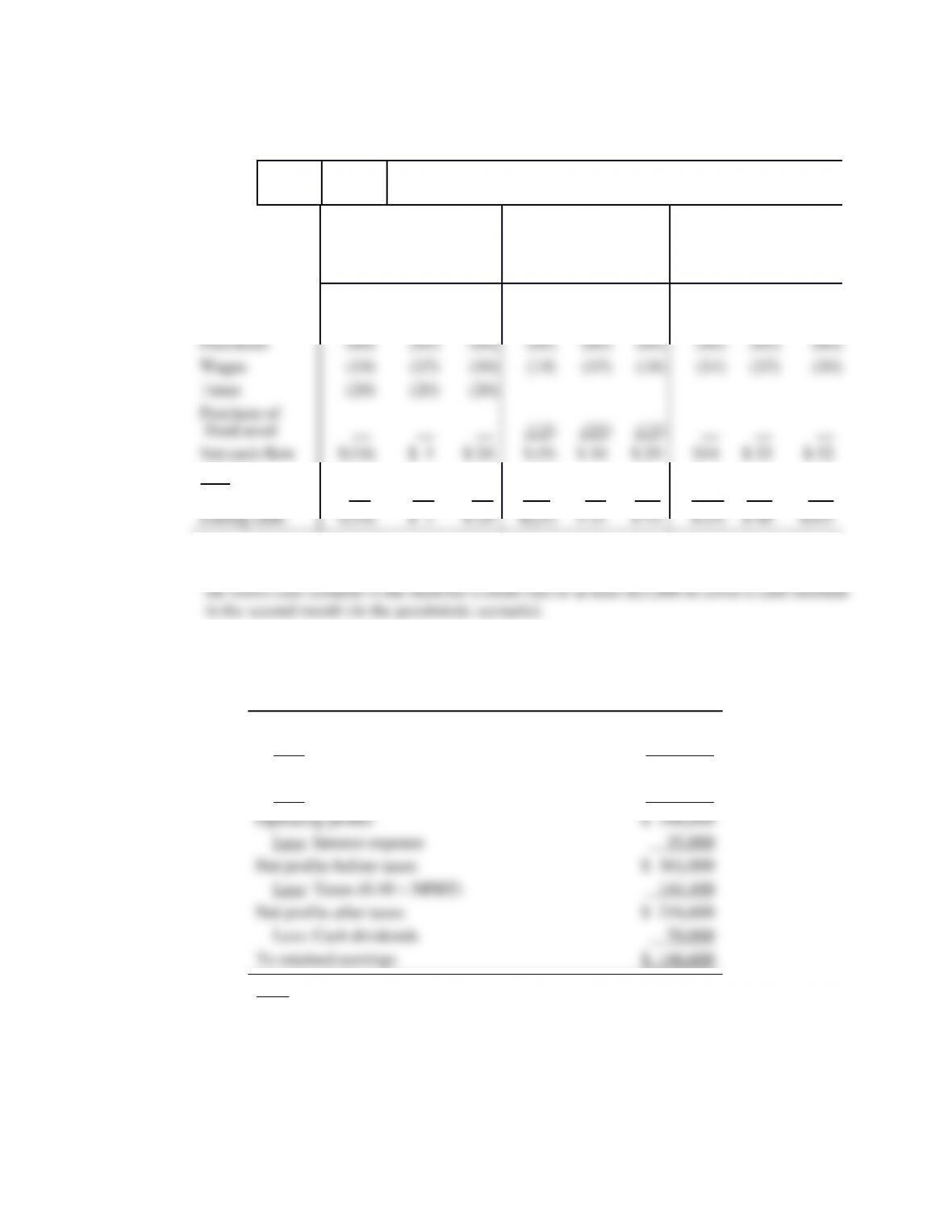

c. Pro Forma Income Statement – Metroline Manufacturing, Inc

Year Ending December 31, 2020 (Fixed and Variable Data)

Sales

$1,500,000

Less: Cost of goods sold – fixed

210,000

Cost of goods sold – variable (0.5 sales)

750,000

Gross profits

$ 540,000

Less: Fixed expense

36,000

Variable expense (0.06 sales)

90,000

Operating profits

$ 414,000

Less: Interest expense

35,000

Net profits before taxes (NPBT)

$ 379,000

Less: Taxes (0.40 NPBT)

151,600

Net profits after taxes

$ 227,400

Less: Cash dividends

70,000

To retained earnings

$ 157,400

Note: Variable cost and expense percentages were found by dividing 2019

c. When sales are projected to rise, and the firm has fixed costs, pro forma income statements

based on percentages of sales will overstate costs and understate profits. Both conditions are