Solutions to Problems

P3-1 Financial-statement account identification (LG 1; Basic)

a., b.

Column 1 for (a) Column 2 for (b)

Account Name Statement Type of Account

Accounts payable BS CL

Accounts receivable BS CA

Accruals BS CL

Column 1 for (a) Column 2 for (b)

Account Name Statement Type of Account

Accumulated depreciation BS FA*

Administrative expense IS E

Buildings BS FA

*Not a fixed asset, but a charge against a fixed asset (and better known as a contra-asset).

P3-2 Income-statement preparation (LG 1; Intermediate)

a. Cathy Chen, CPA – Income Statement

Year Ending December 31, 2019

Sales revenue $360,000

Less: Operating expenses

Salaries $180,000

Employment taxes and

34,600

b. In her first year of business, Ms. Chen covered operating expenses and earned a net profit of

$38,500 (net profit margin of $38.500/$360,000 or 10.7%). Assuming the salary she paid herself

P3-3 Personal Finance Problem: Income-statement preparation (LG 1; Intermediate)

a. 2019 Personal Income and Expense Statement—Adam and Arin Adams

Income

Adam’s salary $45,000

Arin’s salary 30,000

Interest received 500

Dividends received 150

Total Income $75,650

Total Expenses $46,309

2019 Cash Surplus (Deficit) $29,341

b. Income exceeds expenses, so the Adams have a cash surplus.

c. The cash surplus can be used for a variety of purposes. In the short term, the Adams could

replace their car, buy better furniture, or reduce their mortgage debt. Alternatively, they could

P3-4 Calculation of EPS and retained earnings (LG 1; Intermediate)

a. Earnings per share:

Net profit before taxes $436,000

Less: Taxes at 21% 91,560

b. Addition to retained earnings:

170,000 shares $0.80 = $136,000 common stock dividends

Earnings available to common shareholders $280,440

This problem originally asked students to use a tax rate of 40% rather than the 21% enacted under

new tax law. With a 40% tax rate in place, we would have the following:

Earnings per share:

EPS = $197,600 ÷ 170,000 = $1.16

P3-5 Balance-sheet preparation (LG 1; Basic)

Mellark’s Baked Goods

Balance Sheet

December 31, 2019

Assets

Current assets

Cash $215,000

Marketable securities 75,000

Land and buildings $325,000

Machinery and equipment 560,000

Net fixed assets $ 815,000

Total assets $1,930,000

Liabilities and stockholders’ equity

Current liabilities

Total liabilities $1,170,000

Stockholders’ equity

Preferred stock $100,000

P3-6 Effect of net income on a firm’s balance sheet (LG 1; Basic)

Account Beginning Value Change

Ending Value

a

.

Marketable securities $35,000 +$1,365,000 $1,400,000

Retained earnings $1,575,000 +$1,365,000 $2,940,000

d

.

No net change in any accounts

P3-7 Initial sale price of common stock (LG 1; Basic)

Total proceeds from original sale of common stock

= Par value of common stock + Paid-in capital in excess of par on common stock

P3-8 Statement of retained earnings (LG 1; Basic)

a. Common stock dividends = Net profits after taxes – Preferred dividends – ∆ Retained earnings

= $377,000 – $47,000 – ($1,048,000 – $928,000) = $210,000

b. Earnings available for common stockholders = Net profits after taxes – Preferred stock

dividends = $377,000 – $47,000 = $330,000

c. Cash dividend per share of common stock = Total cash dividends / common shares outstanding

= $210,000 (from part a) / 140,000 = $1.50

P3-9 Changes in stockholders’ equity (LG 1; Intermediate)

a. 2019 Net income = ∆ Retained earnings − Dividends paid = $500,000 − $200,000 = $700,000

b. New shares issued = Outstanding shares in 2015 – Outstanding shares in 2014 = 1,000,000

c. Total proceeds from new issue

= Par value of newly issued stock + Paid-in capital in excess of par on newly issued stock

d. Original issue price

P3-10 Ratio comparisons (LG 2, LG 3, LG 4, and LG 5; Basic)

a. The companies operate in dissimilar industries, with wide-ranging differences in the nature of

and degree of government regulation. So ratio comparisons will be apples to oranges.

b. The electric utility and fast-food restaurant operate with lower liquidity ratios than the other

firms, implying the two firms probably need less liquidity. Utilities tend to be relatively large,

c. Firms can operate with high levels of debt if cash flows are large, steady, and

predictable. Demand for power does vary by season, but it fairly predictable ways. Moreover,

d. Although the software industry offers potentially high profits and returns, it also carries

significant risk. As noted, rapidly changing technology, intense competition, and consumer

P3-11. Liquidity management (LG 3; Challenging)

a. Both Bauman’s liquidity ratios are falling over time as shown below.

Ratio 2016 2017 2018 2019

Current ratio 1.88 1.74 1.79 1.55

b. Both ratios fall over the four-year period, indicating deterioration in Bauman’s liquidity

position. Because peer data are not given, it is not clear if this deterioration is industry-wide or

c. Bauman’s inventory turnover ratio is only about 60% of the industry average, suggesting the

firm does a relatively poor job managing inventory. Put another way, Bauman carries more

P3-12. Personal finance: Liquidity ratio (LG 3; Basic)

a. Liquidity ratio = Total liquid assets / Total current debts

b. Josh’s liquidity ratio exceeds 1.8, so he has more liquidity than his benchmark friends.

P3-13 Inventory management (LG 3; Intermediate)

Inventory-turnover ratio = Cost of goods sold / Inventories. So:

Firm 2016 2015 2014

Foot Locker 3.8 3.8 3.6

The first thing to notice is the three companies have similar turnover ratios— that is, all three turn

selling a different mix of products, specifically one with higher margins but lower sales volume, the

P3-14. Accounts-receivable management (LG 3; Basic)

a. A good ratio for evaluating a firm’s collection system is average collection period

(= Accounts receivable Average sales per day).

Blair Supply normally extends 30-day credit to customers, so an average collection period over

b. Seasonality could explain the high average collection period. End-of-year accounts receivable

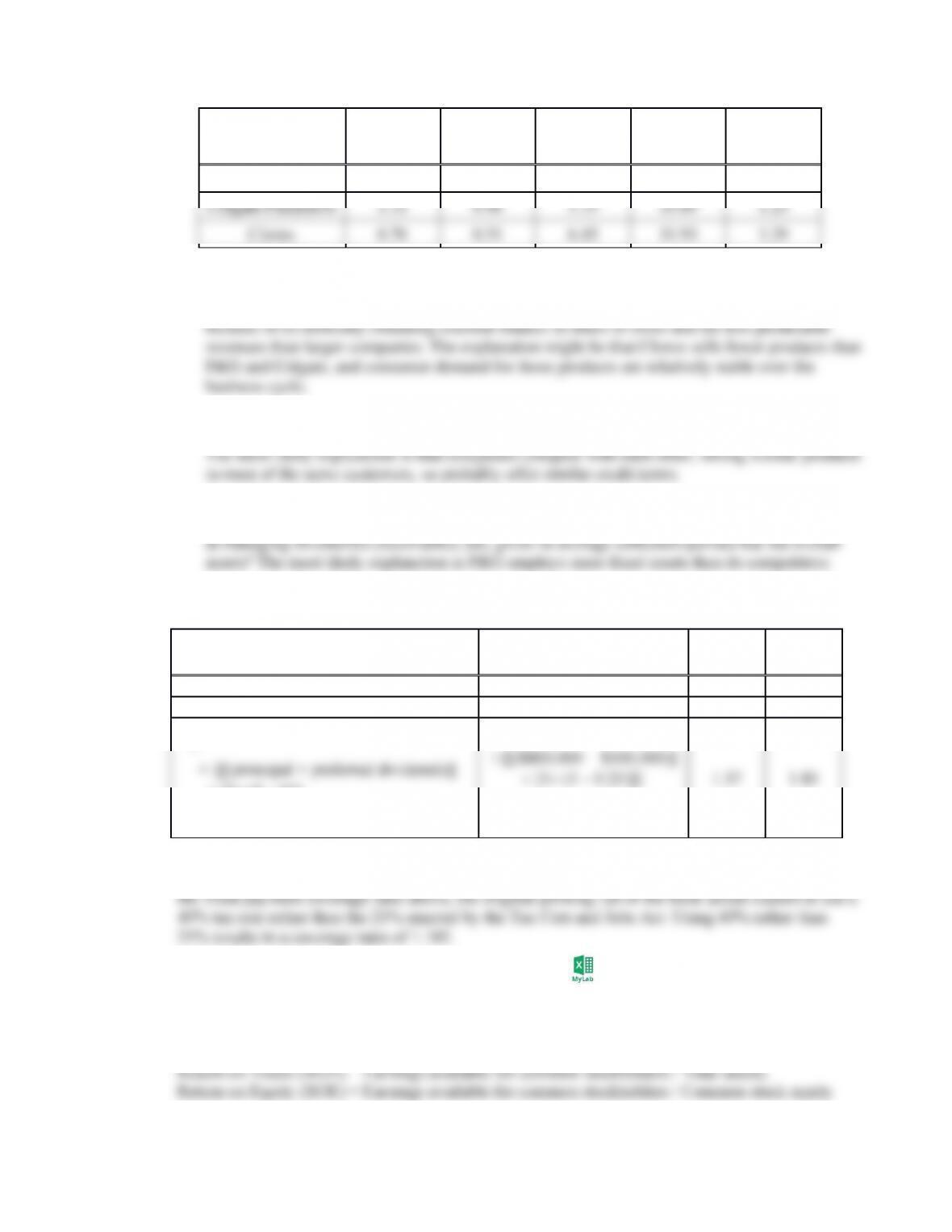

P3-15. Interpreting liquidity and activity ratios (LG 3; Intermediate)

a. Current ratio = Current assets / Current liabilities;

Quick ratio = [Current assets – Inventory] / Current liabilities;

So,

Firm

Current

Ratio

Quick

Ratio

Inventory

Turnover

Average

Collection

Period

Total

Asset

Turnover

Proctor & Gamble 0.89 0.72 6.89 26.46 0.56

b. Colgate-Palmolive boasts the highest current and quick ratios, so they have the most liquidity.

Clorox’s relatively low liquidity ratios are surprising because it is considerably smaller than

P&G and Colgate. Usually smaller companies have greater liquidity on their balance sheets

c. All three firms collect on sales in about 30 days, with the differences in average collection

periods between the shortest (P&G) and longest (Colgate) collection periods only seven days.

d. Procter & Gamble turned inventory over a bit faster than the other firms but assets much

slower. This is surprising because both ratios measure asset efficiency—how could P&G excel

P3-16 Debt analysis (LG 4; Basic)

Ratio Calculation Creek Industr

y

Debt = 0.73 0.51

Times-interest-earned = 3.00 7.30

Fixed-payment coverage

[1 (1 – t)]}

Creek Enterprises finances a much larger percentage of assets with debt and has less ability to

service additional debt than the average firm in the industry, so the loan should be rejected. Note in

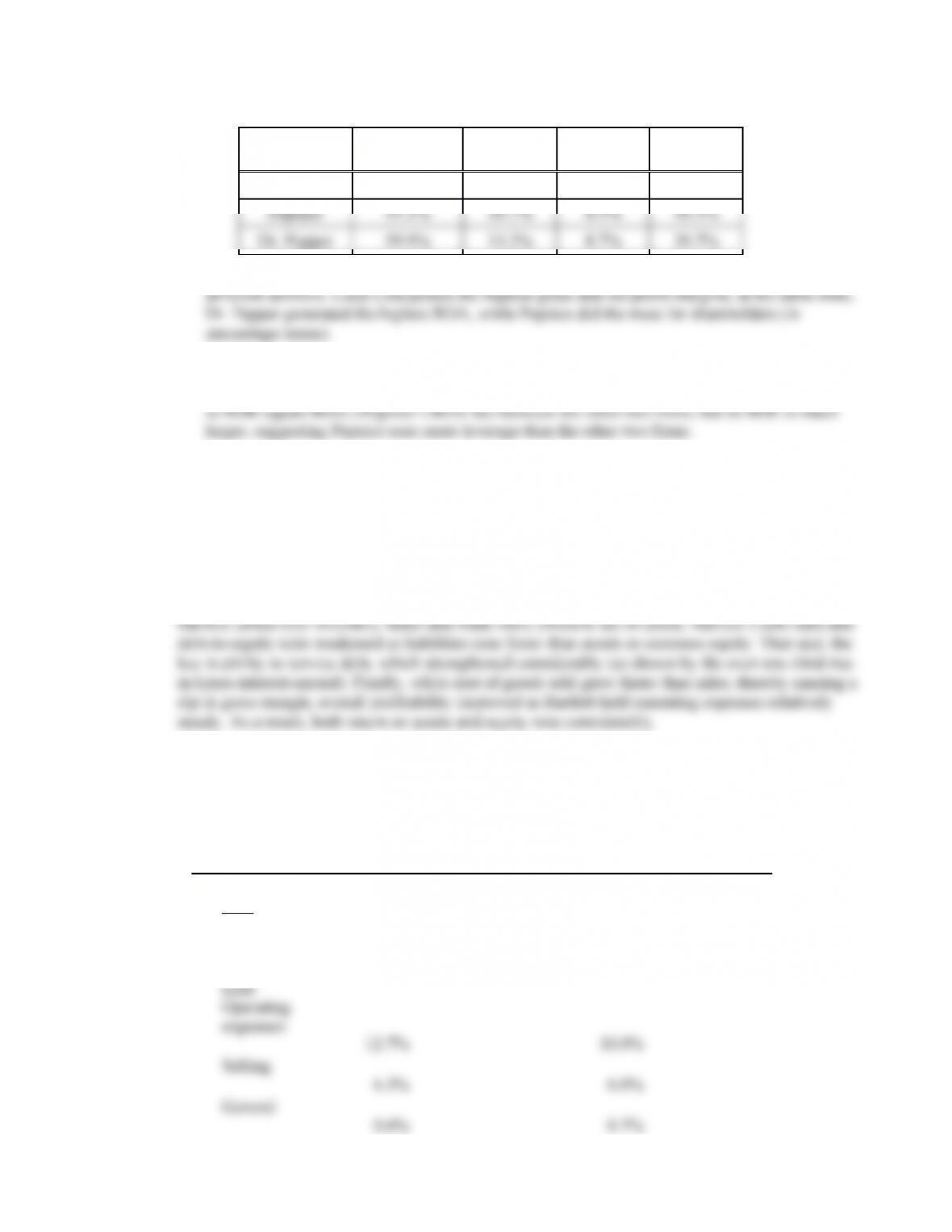

P3-17 Profitability analysis (LG 4 and LG 5; Intermediate)

Gross profit margin = [Sales – Cost of goods sold] / Sales;

Net profit margin = Earnings available for common stockholders / Sales;

So,

Firm

Gross Profit

Margin

Net Profit

Margin ROA ROE

Coca-Cola 60.7% 15.6% 7.5% 28.3%

It is difficult to say which company is most profitable because the four measures provide

b. ROE exceeds ROA because—while both ratios have the same numerator (earnings)—ROE has

a smaller denominator for all firms with some debt. (If a firm has no debt, assets equal equity,

P3-18 Ratio analysis (LG 2, LG 3, and LG 4; Challenging)

From 2018 to 2019, Bartlett’s liquidity position weakened in that the current ratio deteriorated and

average collection period lengthened. One bright spot is that inventories, which can be relatively

illiquid, became a smaller percentage of current assets. Activity ratios unequivocally improved as

P3-19. Common-size statement analysis (LG 5)

Creek Enterprises

Common-Size Income Statement

Years Ending December 31, 2018 and 2019

2018 2019

Sales revenue 100.0% 100.0%

Less: Cost

of goods

sold

Gross profits

Lease

expense

Depreciati

on

3.6% 23.2% 3.3% 20 .0%

before taxes

Less:

Taxes

2.0% 1 .4%

after taxes

In dollar terms, sales declined from $35 to $30 million. Meanwhile, as a percentage of sales, cost of

goods sold increased, probably reflecting a loss of productive efficiency. Operating expenses (as a

percentage of sales) fell— a favorable development unless the decline contributed to drop in sales (say