P13-25 Integrative: Optimal capital structures (LG 3, 4, 6; Challenge)

a. 0% debt ratio – baseline: Probability (p)

p1 = 0.20 p2 = 0.60 P3 =0.20

Sales $200,000 $300,000 $400,000

Less: Variable

80,000 120,000 160,000

Earnings before

taxes $ 20,000 $ 80,000 $140,000

Less: Taxes (40%

8,000 32,000 56,000

EPS (After-tax

earnings 25,000

shares)

$ 0.48 $ 1.92 $ 3.36

Note: Total capital with 100% equity = $250,000 (25,000 shares

$10 book value)

Summary statistics – EPS (0% debt):

Standard deviation:

Because all outcomes and probabilities are known, standard deviation (EPS) is given

by:

Coefficient of variation (EPS) = Standard deviation (EPS) Expected EPS

***

20% debt ratio: Amount of debt 20% $250,000 $50,000

Probability (p)

p1 = 0.20 p2 = 0.60 P3 =0.20

EBIT $20,000 $80,000 $140,000

Less: Taxes (40% of before-tax

earnings) 6,000 30,000 54,000

Summary statistics – EPS (20% debt):

Expected (EPS) = $2.25

Number of shares $150,000 equity $10 book value 15,000 shares

Probability (p)

p1 = 0.20 p2 = 0.60 p3 =0.20

EBIT $20,000 $80,000 $140,000

Less: Interest (12% of debt) 12,000 12,000 12,000

Summary statistics – EPS (40% debt):

Coefficient of variation (EPS) = $1.5179 $2.72 = 0.5580

***

60% debt ratio:

Number of shares $100,000 equity $10 book value 10,000 shares

Probability (p)

p1 = 0.20 p2 = 0.60 p3 =0.20

EBIT $20,000 $80,000 $140,000

Less: Interest (14% of debt) 21,000 21,000 21,000

Summary statistics – EPS (60% debt):

Expected (EPS) = $6.54

Standard deviation, σEPS = $2.2768

***

Share

Debt

Ratio Expected

(EPS)

EPS) CV(EPS)

Common

Shares Total

Debt ($) Price

*

=

Expect

ed

EPS

Requir

ed

Return

0% $1.92 0.9107 0.4743 25,000 0 $1.92÷0.16 $12.00

*Share price: E(EPS)

required return for CV for E(EPS), from table in problem.

b. (1) Optimal capital structure to maximize EPS: 60% debt, 40% equity

equity

c.

P13-26 Integrative: Optimal capital structure

(LG 3, 4, 5, 6; Challenge)

a. % Debt Total Assets $ Debt $ Equity No. of Shares @ $25

0 $40,000,000 $ 0 $40,000,000 1,600,000

10 40,000,000 4,000,000 36,000,000 1,440,000

b. % Debt $ Total Debt Before Tax Cost of

Debt, rd

$ Interest Expense

0 $ 0 0.0% $ 0

10 4,000,000 7.5 300,000

20 8,000,000 8.0 640,000

c. %

De

bt

$ Interest

Expense EBT Taxes

@40% Net

Income # of

Shares EPS

0 $ 0 $8,000,000 $3,200,000 $4,800,000 1,600,000 $3.00

10 300,000 7,700,000 3,080,000 4,620,000 1,440,000 3.21

40 1,760,000 6,240,000 2,496,000 3,744,000 960,000 3.90

Note: In the final column of the table above, EPS values with a 21% tax rate EPS are (from

d. and e.

% Debt EPS rSP0

0 $3.00 10.0% $30.00

10 3.21 10.3 31.17

20 3.45 10.9 31.65

The optimal capital structure is 30% debt and 70% equity. This mix will maximize the price per

share of the firm’s common stock and, thus, maximize shareholders’ wealth.

.Note: When the tax rate falls to 21%, stock prices for various debt levels change, but the

P13-27 Integrative: Optimal capital structure (LG 3, 4, 5, 6; Challenge)

a. Probability

0.30 0.40 0.30

Sales $600,000 $900,000 $1,200,000

Less: Variable costs (40%) 240,000 360,000 480,000

b.

Debt

Ratio

Amount

of Debt Amount

of Equity Shares of

Common Stock*

0% $ 0 $1,000,000 40,000

15% 150,000 850,000 34,000

* Dollar amount of equity

$25 per share

Number of shares of common stock.

c. Debt

Ratio Amount

of Debt Before-Tax

Cost of Debt Annual

Interest

0% $ 0 0.0% $ 0

15% 150,000 8.0 12,000

30% 300,000 10.0 30,000

d. EPS [(EBIT interest) (1 T)] number of common shares outstanding:

Debt

Ratio Calculation EPS

0% ($60,000 $0) (0.6) 40,000 shares $0.90

($240,000 $0) (0.6) 40,000 shares 3.60

($420,000 $0) (0.6) 40,000 shares 6.30

45% ($60,000 $58,500) (0.6) 22,000 shares $0.04

($240,000 $58,500) (0.6) 22,000 shares 4.95

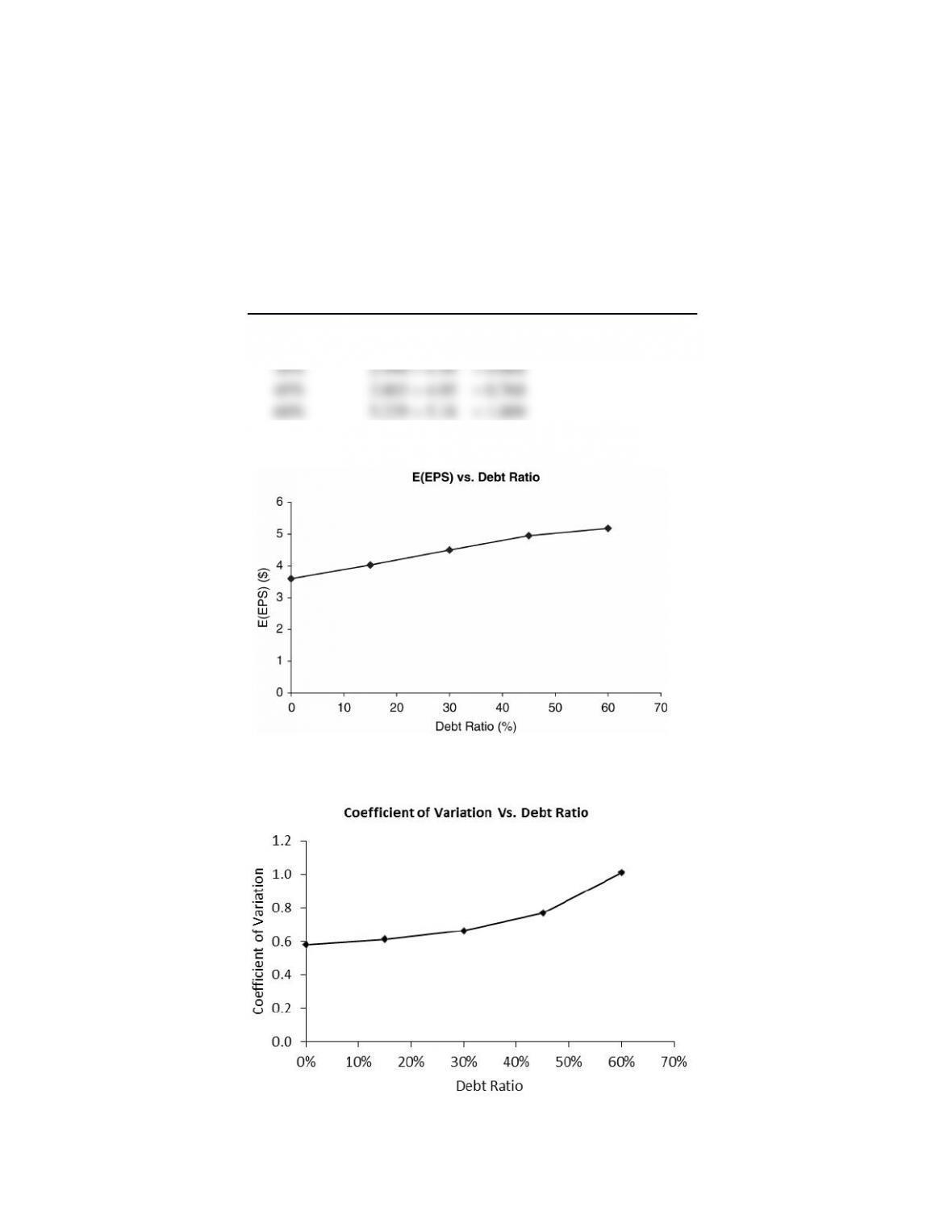

e. (1) Expected (EPS) 0.30(EPS1) 0.40(EPS2) 0.30(EPS3):

Debt Ratio Calculation E(EPS)

0% 0.30 (0.90) 0.40

(3.60) 0.30 (6.30)

0.19 1.80 2.51 $4.50

45% 0.30 (0.04) 0.40

(2) Standard deviation of EPS,

EPS:

Debt Ratio Calculation

0% = 2.091

60% = 5.229

(3)

Debt

Ratio

EPS E(EPS) Coefficient of Variation

0% 2.091 3.60 0.581

15% 2.463 4.03 0.611

f. (1)

(2)

The return, as measured by the E(EPS), as shown in part d, continually increases as the debt

ratio increases, although at some point the rate of increase of the EPS begins to decline (the

increases but at a more rapid rate.

g.

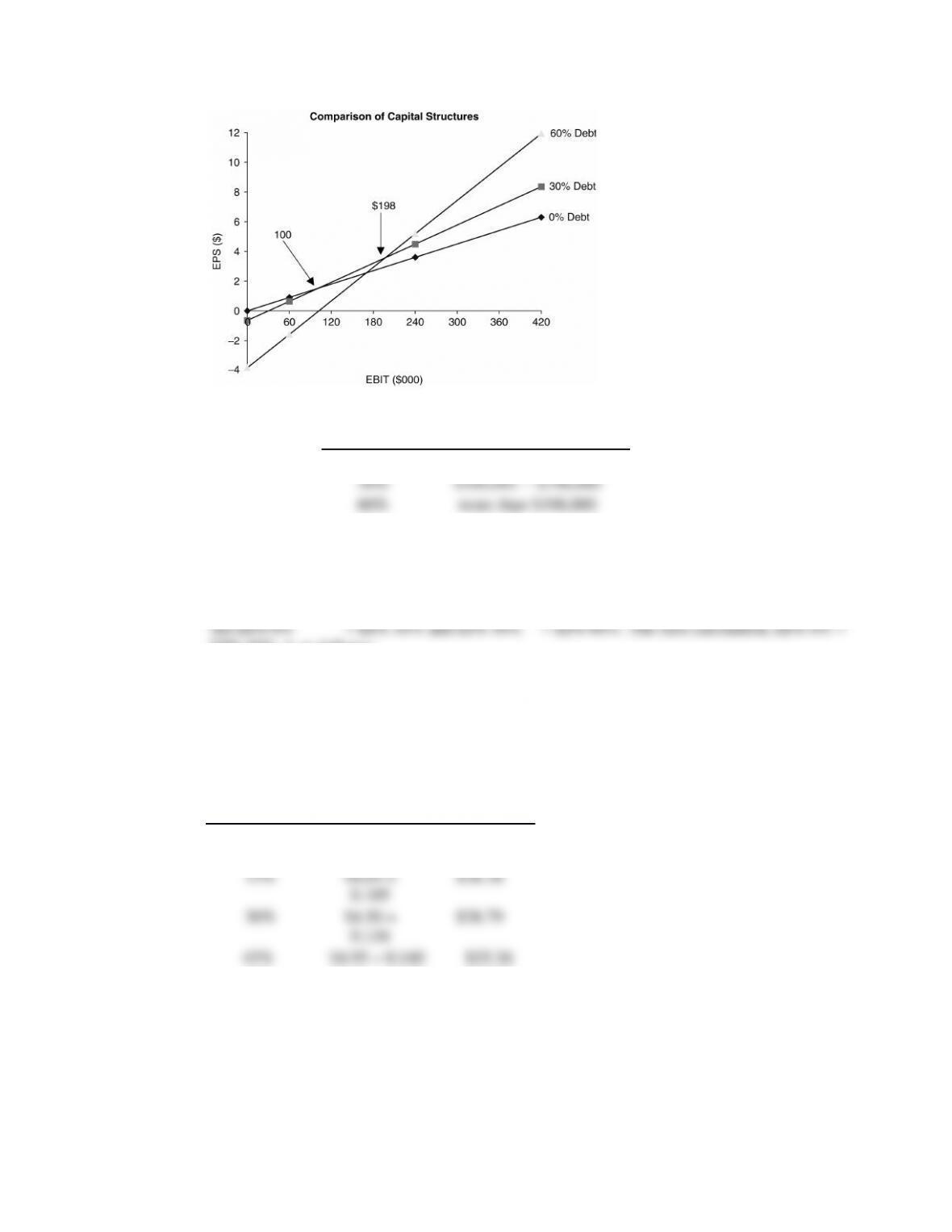

The EBIT ranges over which each capital structure is preferred are as follows:

Debt Ratio EBIT Range

0% $0 $100,000

To calculate the intersection points on the graphic representation of the EBIT-EPS approach to

capital structure, the EBIT level which equates EPS for each capital structure must be found,

using the formula in Footnote 18 of the text:

EPS 30%, is as follows:

The major problem with this approach is failure to focus on shareholder-wealth maximization.

h. Debt Ratio EPS rsShare Price

0% $3.60

0.100 $36.00

60% $5.18 0.200 $25.90

i. A 60% debt structure maximizes EPS, but a 30% debt structure maximizes share prices. A

capital structure with 30% debt is recommended because it maximizes shareholder wealth.