Case: “Evaluating Cherone Equipment’s Risky Plans for Increasing Its

Production Capacity”

Case studies are available on www.pearson.com/mylab/finance.

a. 1. Plan X

Cash flows: CF0 (project cost) −$2,700,000, CF1 $470,000, CF2 $610,000,

Plan Y

Cash flows: CF0 (project cost) −$2,100,000, CF1 $380,000, CF2 $700,000

2. To use the IRR command in Excel, start by arranging the cash outflows and inflows in adjacent

cells (starting with the outflow— project costs— as a negative number). Proper syntax is:

b. Plan X

Cash flows: CF0 (project cost) −$2,700,000, CF1 $470,000, CF2 $610,000, CF3 $950,000,

CF4 $970,000, and CF5 $1,500,000.

Ranking

Plan NPV IRR RADRs

X 2 2 1

c. Both NPV and IRR produced the same relative rankings before adjusting for risk. Making risk

adjustments with RADRs, however, caused project rankings to reverse. The final choice

would be Plan X because it produces the highest NPV using the risk-adjusted method.

d. Plan X

Value of real options 0.25 $100,000 $25,000

e. With the additional value from the real options, the ordering of projects is reversed. Project Y

is now favored over Project X using the RADR NPV.

f. Capital rationing could change the selection of the plan. Plan Y requires only $2,100,000

Spreadsheet Exercise

Answers to Chapter 12’s Dyno Corporation problem are available on www.pearson.com/mylab/finance.

Group Exercise

Group exercises are available on www.pearson.com/mylab/finance .

The group exercise for this chapter will focus on integrating risk into capital budgeting; specifically,

investment projects from the previous two chapters will now be modified to include risk. Cash flows

estimated previously will no longer be certain. Each estimated dollar flow is now assigned three possible

levels for three possible states of the worlds (pessimistic, most likely, and optimistic). Original estimates

serve as the most likely value. Analysis of these estimates begins with a calculation of the ranges for each

outcome. A simplified RADR is then calculated using the previously determined discount rate. The risk-

adjusted NPV is then calculated.

Using information from Chapters 10, 11, and 12, the groups are asked to defend their choice of investment

projects. As pointed out in the assignment, groups should use this assignment to defend their choices in the

form of documents suitable for presentation to their board of directors. This conclusion should summarize

all the work done across the chapters, and students should take pride in the quantity and quality of their

efforts. It works well to have each student group present their project and decision to the remainder of the

class, who can be viewed as a “board of directors.”

Integrative Case 5: “Lasting Impressions Company”

The Lasting Impressions Company is a commercial printer faced with a replacement decision in which two

mutually exclusive projects have been proposed. The data for each press have been designed to produce

conflicting rankings using the NPV and IRR decision rules. The case tests student understanding of the

techniques as well as the qualitative aspects of risk and return decision-making.

a. 1. Calculation of initial investment for Lasting Impressions Company:

Press A Press B

Installed cost

of new press

Cost of new

press $830,000 $640,000

sale of old

press*

Total (298,400) (298,400)

proceeds—

sale of old

press

Increase in current liabilities (35,000)

Increase in net working capital $ 90,400

2. Depreciation

Year Cost Rate Depreciation

Press A

1 $870,000 0.20 $174,000

2 870,000 0.32 278,400

3 870,000 0.19 165,300

Existing Press

1 $400,000 0.12 (Yr. 4) $48,000

2 400,000 0.12 (Yr. 5) 48,000

3 400,000 0.05 (Yr. 6) 20,000

Operating Cash Inflows

Year

Earnings

before

Depreciat

ion

and

Taxes Depre-

ciation

Earnings

before

Taxes

Earnings

after

Taxes Cash

Flow

Old

Cash

Flow

Incremen

tal

Cash

Flow

Existing

Press

1 $120,0

00 $48,000 $72,000 $43,200 $91,200

2 120,00

048,000 72,000 43,200 91,200

Press A

1 $250,0

00 $174,00

0$76,000 $45,600 $219,60

0$91,200 $128,400

2 270,00

0278,400 8,400 5,040 273,360 91,200 182,160

3 300,00

0165,300 134,700 80,820 246,120 80,000 166,120

Press B

1 $210,0

00 $132,00

0$78,000 $46,800 $178,80

0$91,200 $87,60

0

6 0 33,000 33,000 19,800 13,200 0 13,200

3. Terminal cash flow

Press A Press B

After-tax proceeds—sale of new press

Proceeds on sale of new press $400,000 $330,000

Tax on sale of new press* (142,600

) (118,800)

** Sale price $150,000

Less: Book value (Yr. 6) 0

Cash Flows

Year Press A Press B

Initial investment ($662,000) ($361,600)

1 $128,400 $ 87,600

* Year 5 Press A Press B

Operating cash flow $191,760 $ 85,680

b.

c. Relevant cash flow

Cumulative Cash Flows

Year Press A Press

B

1 $128,400 $87,600

2 310,560 206,880

1. Press A: 4 years [(662,000 644,440) 191,760]

Payback 4 (17,560 191,760)

2. Press A

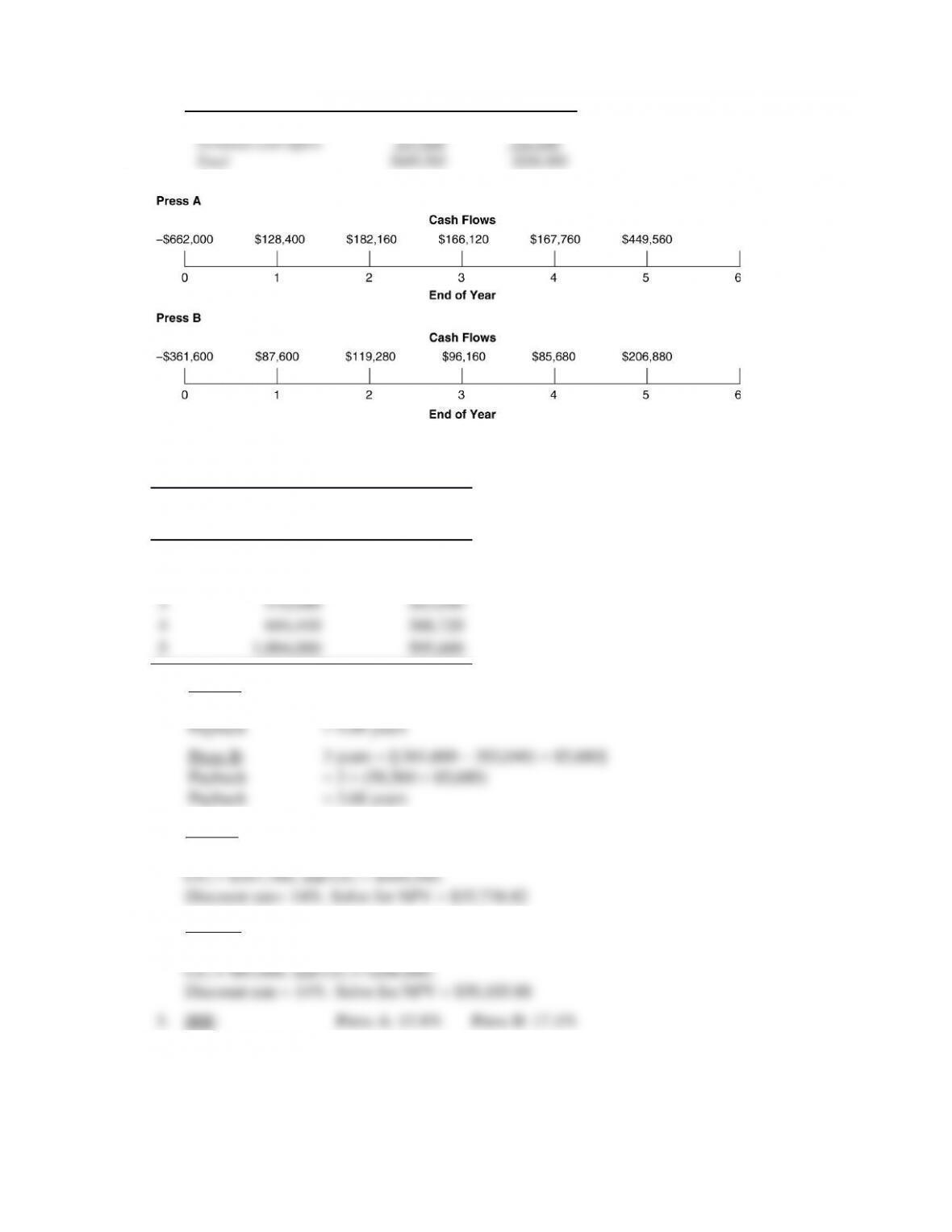

Cash flows: CF0 (project cost) −$662,000, CF1 $128,400, CF2 $182,160, CF3 $166,120,

Press B

Cash flows: CF0 (project cost) −$361,600, CF1 $87,600, CF2 $119,280, CF3 $96,160,

d.

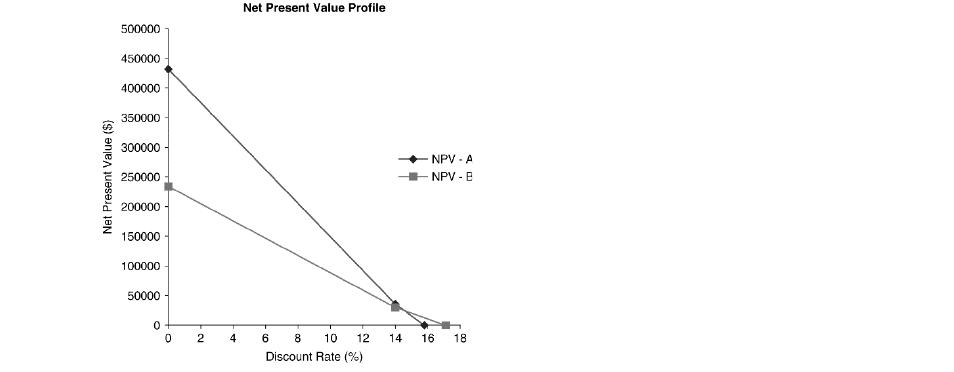

Data for NPV Profile

Discount Rate NPV

Press A Press B

0% $432,000 $234,000

When the cost of capital is below approximately 15% (where the NPV profiles for the two presses

higher NPV and top ranking (even though it has the lower IRR).

e. a. If the firm has unlimited funds, Press A is preferred.

b. But if the firm is subject to capital rationing, Press B would be preferred if the capital constraint