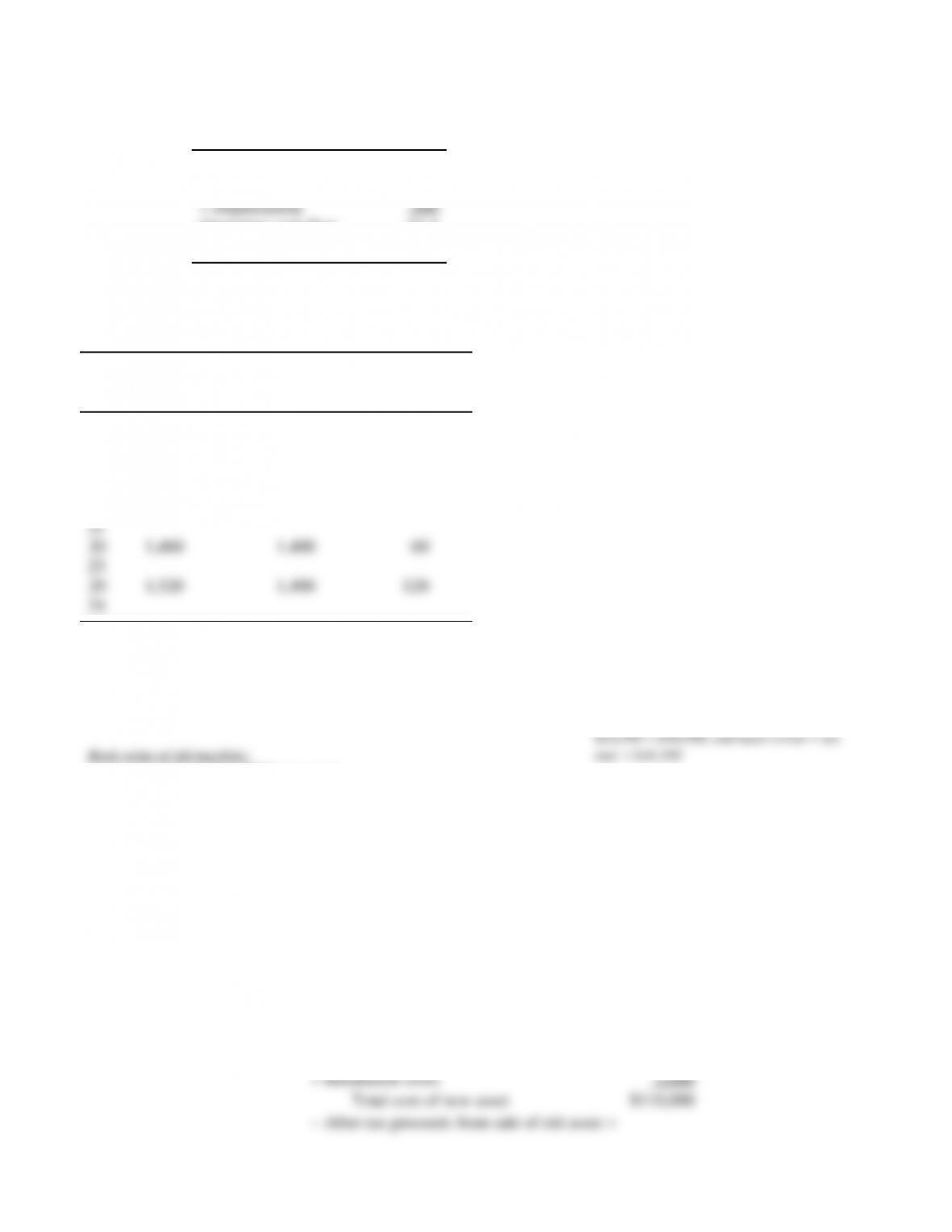

P11-19 Incremental operating cash flows (LG 5; Intermediate)

a.

Year Revenu

e

Expenses

(excluding

depreciation

and interest)

Profits before

Depreciation

and Taxes Depre-

ciation

Net

Profits

before

Taxes Taxes

Net

Profits

after Tax

Operatin

g

Cash

Inflows

New

Lathe

1 $40,00

0$30,000 $10,000 $2,00

0$8,000 $3,2

00 $4,80

0$6,80

0

2 41,000 30,000 11,000 3,200 7,800 3,12

04,680 7,880

0$6,00

0

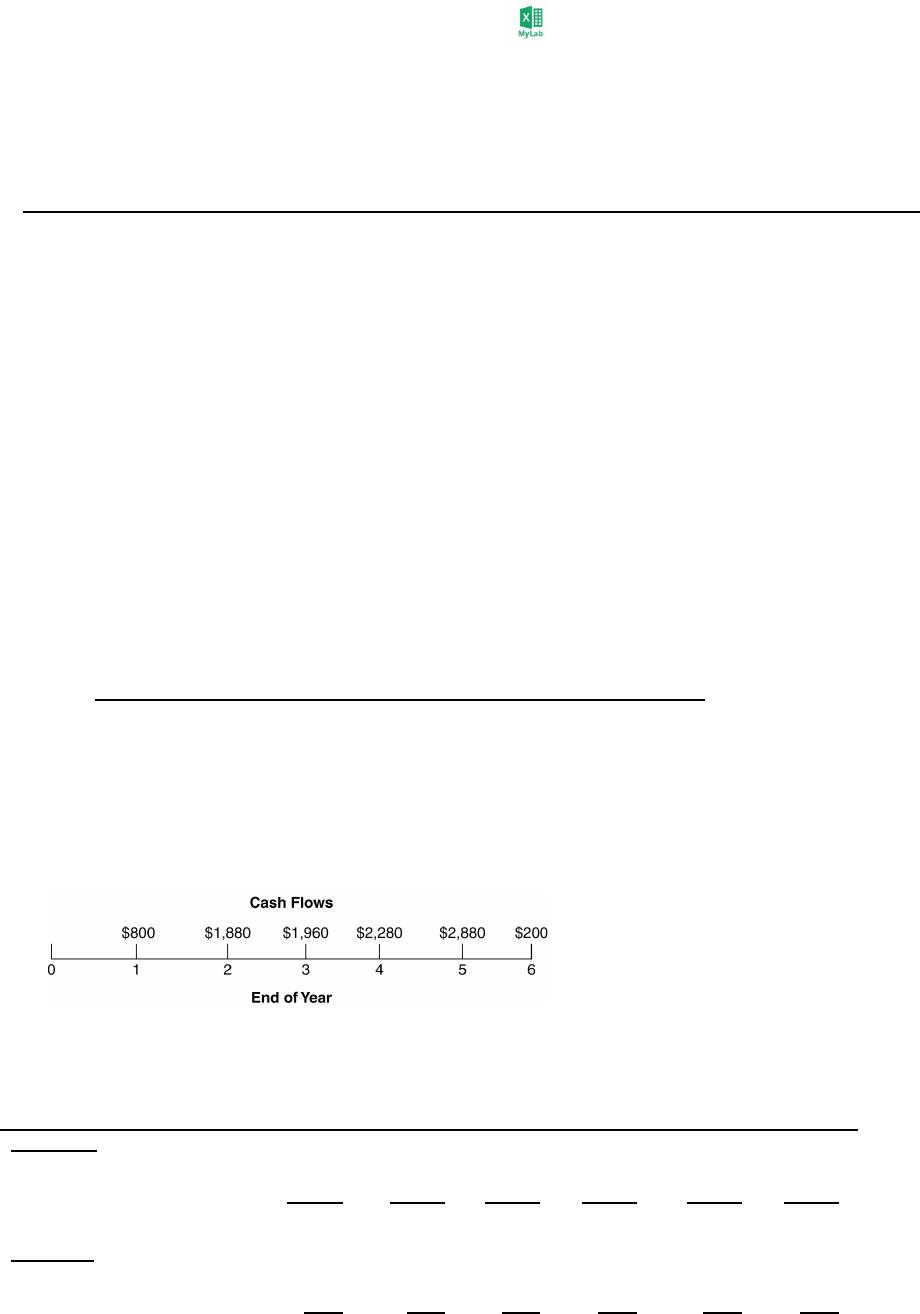

b. Calculation of incremental cash flows

Year New Lathe Old Lathe Incremental Cash

Flows

1 $6,800 $6,000 $800

2 7,880 6,000 1,880

c.

P11-20 Determining incremental operating cash flows (LG 5; Intermediate)

Year

1 2 3 4 5 6

Revenues: (000)

New buses $1,850 $1,850 $1,830 $1,825 $1,815 $1,800

Old buses 1,800 1,800 1,790 1,785 1,775 1,750

Year

1 2 3 4 5 6

Depreciation: (000)

New buses $ 600 $ 960 $ 570 $ 360 $ 360 $ 150

At a 21% tax rate, net incremental cash flows would be:

Year 1 2 3 4 5 6

Revenues 50 50 40 40 40 50

P11-21 Terminal cash flows: Various lives and sale prices (LG 6; Challenge)

a. After-tax proceeds from sale of new asset 3-Year *

5-Year *

7-Year *

Proceeds from sale of proposed asset $10,000 $10,000 $10,000

Terminal cash flow $56,880 $39,600

$36,000

*1. Book value of asset

[1

(0.20

0.32

0.19)]

$180,000

$52,200

Proceeds from sale

$10,000. So, $10,000

$52,200

($42,200) loss

(0.40)

$4,000 tax liability

b. If the usable life is less than the normal recovery period, the asset has not been depreciated

fully and a tax benefit may be taken on the loss; therefore, the terminal cash flow is higher.

c. (1)

(2)

After-tax proceeds from sale of new asset

Proceeds from sale of new asset $ 9,000

+ Tax on sale of proposed asset*0

$135,600

1. Book value of the asset

$180,000

0.05

$9,000; no taxes are due

d. The higher the sale price, the higher the terminal cash flow.

P11-22 Terminal cash flow: Replacement decision (LG 6; Challenge)

After-tax proceeds from sale of new asset

Proceeds from sale of new machine $75,000

Tax on sale of new machinel(14,360)

Terminal cash flow $76,640

1 Book value of new machine at end of year 4:

[1

(0.20

0.32

0.19

0.12)

($230,000)]

$39,100

$75,000

$15,000

(0.40)

$6,000 tax benefit

P11-23 Relevant cash flows for a marketing campaign (LG 3, 4, 5, 6; Challenge)

Marcus Tube – Calculation of Relevant Cash Flow ($000)

Calculation of Net Profits after Taxes and Operating Cash Flow with Marketing Campaign

2019 2020 2021 2022 2023

Sales $20,

500 $21,0

Gross

$

2,100 $

2,15

0

$

2,25

0

$

2,35

0

150 150 150 150 150

Market

ing

campai

gn

Deprec

iation

500 500 500 500 500

Total

operati

ng

expens

es

2,70

Net

profit

after

taxes $

840 $ 870 $

900 $

960 $

1,02

0

Deprec

iation

Without Marketing Campaign

Years 2019–2023

Net profit after taxes $

900

Operating cash flow $1,4

00

Relevant

Cash Flow

($000)

Yea

rWith Marketing

Campaign

Without

Marketing

Campaign

Increment

al Cash

Flow

20

19 $1,34

0$1,400 $(60)

20

20 1,370 1,400 (30)

20

P11-24 Relevant cash flows: No terminal value (LG 3, 4, 5; Challenge)

a.

Book value of old machine:

[1

(0.20

0.32

0.19)]

$50,000

$14,500. So, taxable amount = $55,000

b. and c. (40% tax rate)

b. and c. (21% tax rate)

P11-25 Integrative: Determining relevant cash flows (LG 3, 4, 5, 6; Challenge)

a. Initial investment:

Installed cost of new asset

Cost of new asset $105,000

*Book value of old asset: [1

(0.20

0.32)]

$60,000

b. Calculation of Operating Cash Flows

Year

Profits

before

Depreciation

and Taxes Depreciatio

n

Net Profits

before

Taxes Taxe

s

Net Profits

after Taxes

Operating

Cash

flows

New Grinder

1 $43,00

0$22,000 $21,000 $8,4

00 $12,600 $34,60

0

2 43,000 35,200 7,800 3,12

04,680 39,880

3 43,000 20,900 22,100 8,84

013,260 34,160

Existing Grinder

1 $26,00

0$11,400 $14,600 $5,8

40 $8,760 $20,16

0

2 24,000 7,200 16,800 6,72

010,080 17,280

Calculation of

Incremental

Cash Flows

Year New Grinder Existing

Grinder Incremental Operating Cash

Flow

1 $34,600 $20,160 $14,440

2 39,880 17,280 22,600

c. Terminal cash flow:

After-tax proceeds from sale of new asset

Proceeds from sale of new asset $29,000

*Book value of asset at end of year 5

$5,500. Recaptured depreciation is $29,000

$5,500

$23,500.

Hence, taxes due are $23,500

0.40

$9,400.

d. Year 5 relevant cash flow:

Operating cash flow $20,280

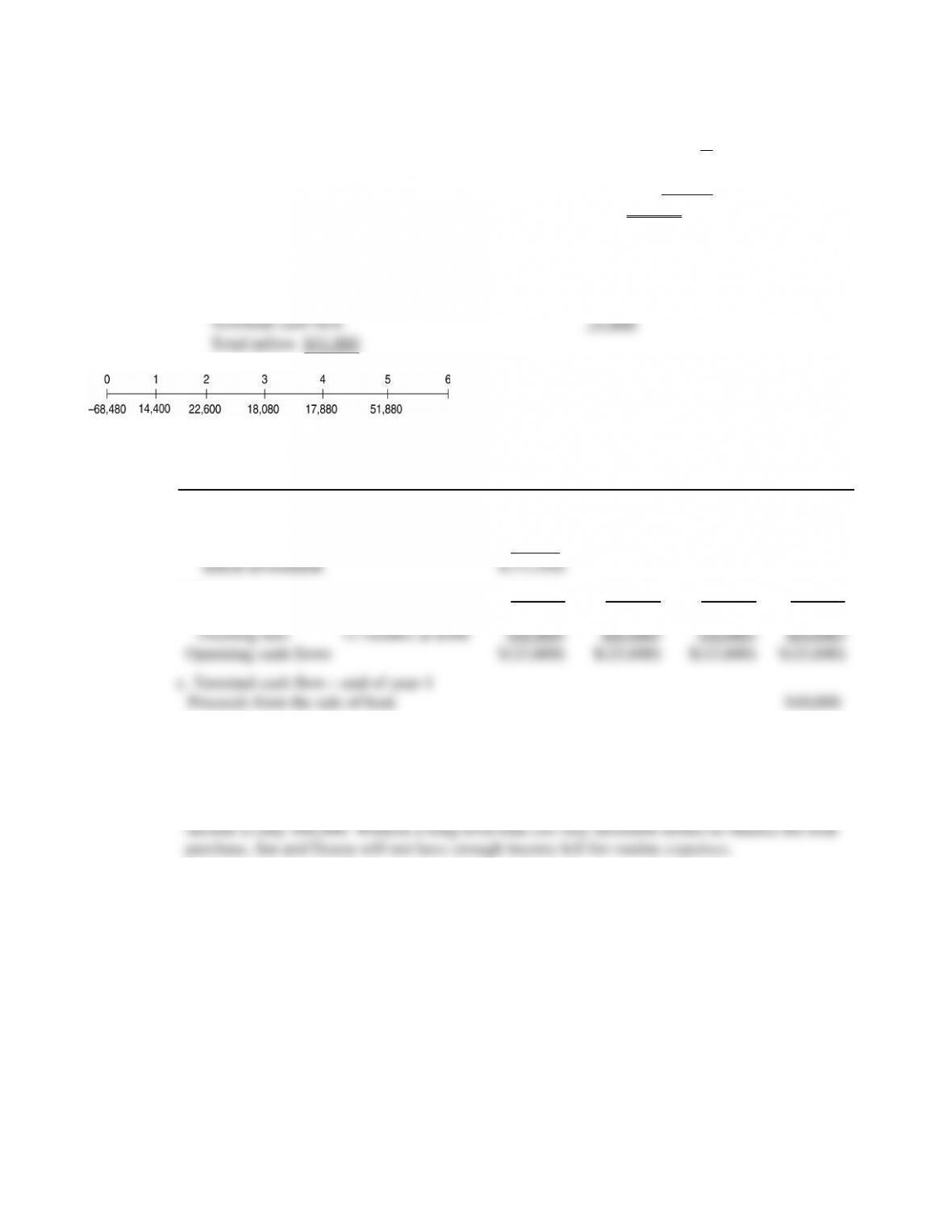

P11-26 Personal finance: Determining relevant cash flows for a new boat (LG 3, 4, 5, 6; Challenge)

Jan and Deana – Cash Flow Budget for Boat Purchase

a.Initial investment

Total cost of new boat

Add: Taxes (6.5%)

$(74,550)

b.Operating cash flows Year 1 Year 2 Year 3 Year 4

Maint. & repair 12 months at $800 $(9,600) $(9,600) $(9,600) $(9,600)

d. and e. Assume for simplicity the interest rate is zero (so the timing of inflows and outflows

within each year is not relevant.

Over the four-year period, the net cash outflow on the boat is $96,950, but annual disposable