Solutions to Problems

Note : The MACRS depreciation percentages used in the following problems appear in Chapter 4, Table 4.2.

Percentages are rounded to the nearest integer for ease in calculation. For simplification, five-year-lived

projects with five years of cash inflows are typically used throughout this chapter. Projects with usable lives

equal to the number of years of cash inflows are also included in the end-of-chapter problems. It is

important to recall from Chapter 4 that under the Tax Reform Act of 1986, MACRS depreciation results in

n 1 years of depreciation for an n-year class asset. This means in actual practice projects will typically

have at least one year of cash flow beyond their recovery period.

P11-1 Classification of expenditures (LG 2; Basic)

a. Operating expenditure—market changes require obtaining another report within a year.

b. Capital expenditure—machine will last more than one year.

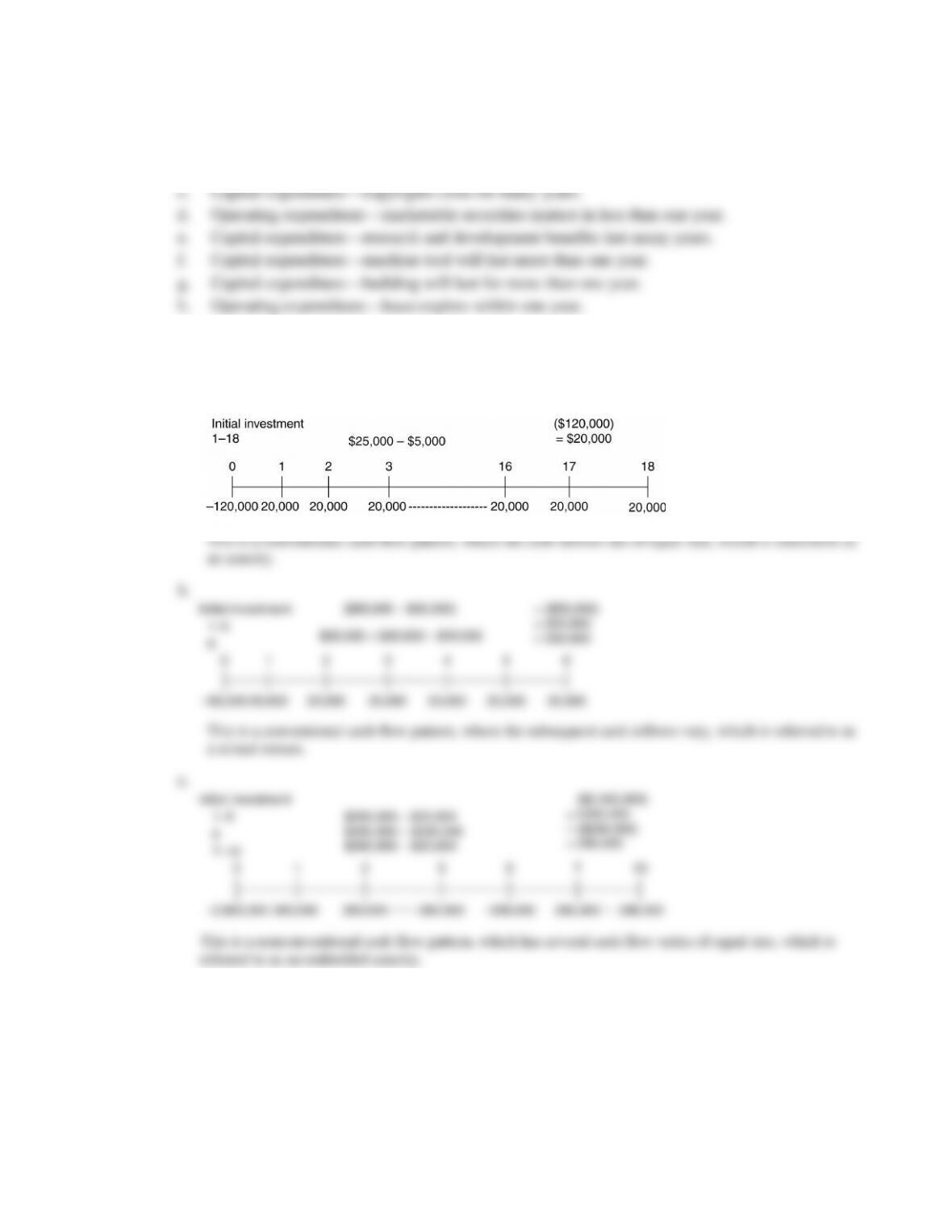

P11-2 Relevant cash flow and timeline depiction (LG 1, 2; Intermediate)

a.

Year Cash Flow

P11-3 Expansion versus replacement cash flows (LG 3; Intermediate)

a.

b. An expansion project is simply a replacement decision in which all cash flows from the old

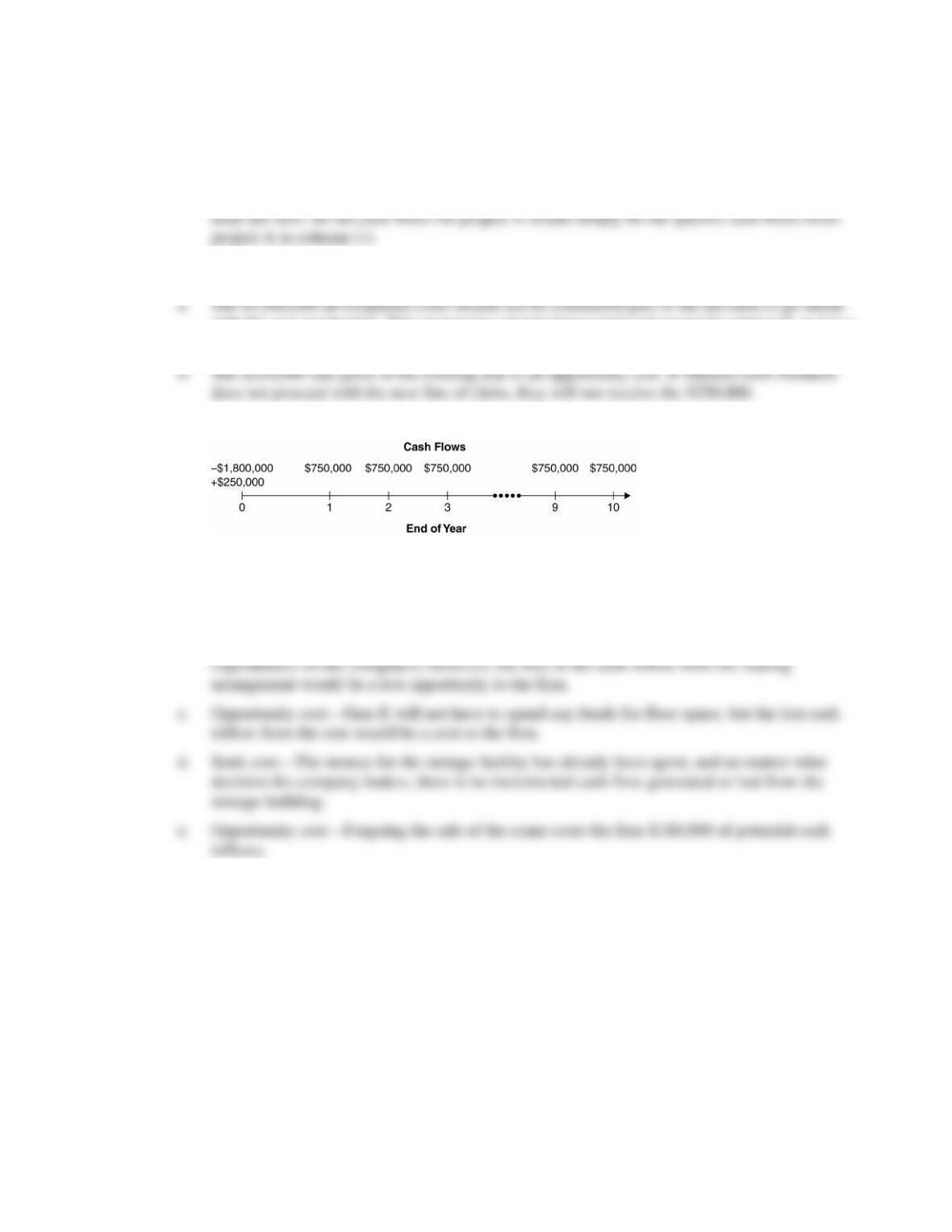

P11-4 Sunk costs and opportunity costs (LG 2; Basic)

with the new production. This money has already been spent and cannot be retrieved, so it is a

sunk cost.

c.

P11-5 Sunk costs and opportunity costs (LG 2; Intermediate)

a. Sunk cost—The funds for the tooling had already been expended and would not change, no

matter whether the new technology would be acquired or not.

b. Opportunity cost—The development of the computer programs can be done without additional

P11-6 Personal finance: Sunk and opportunity cash flows (LG 2; Intermediate)

a. Sunk costs are expenditures made in the past that cannot be altered by a current decision. The

cash outlays done before David and Ann decided to rent out their home would be classified as

b. Sunk costs (cash flows):

Replace water heater

Opportunity costs (cash flows):

Rental income

P11-7 Book value (LG 3; Basic)

Asset Installed

Cost Accumulated

Depreciation Book

Value

A $ 950,000 $ 674,500 $275,500

B 40,000 13,200 26,800

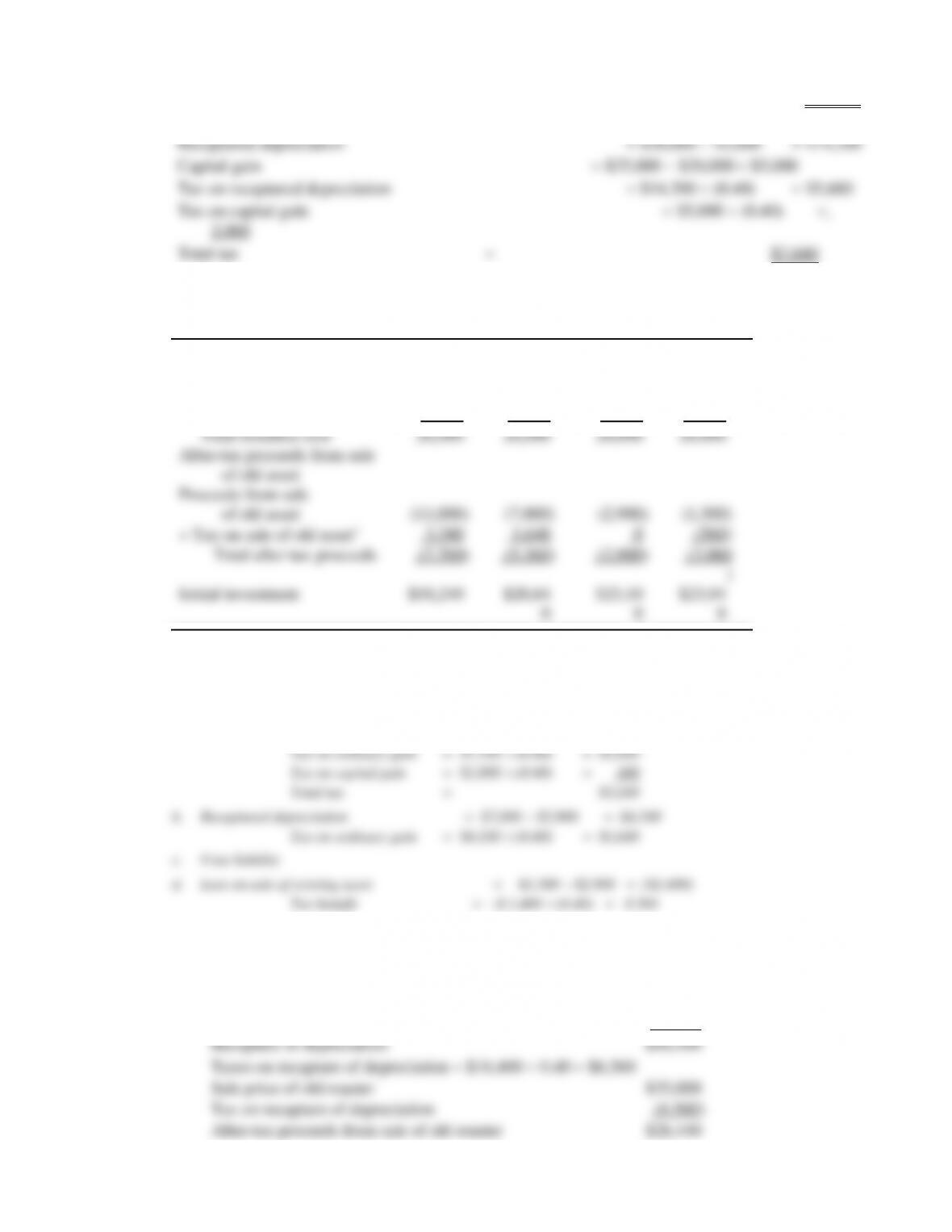

P11-8 Book value and taxes on sale of assets (LG 3, 4; Intermediate)

a. Book value Installed cost of asset $80,000) – Accumulated depreciation

b.

Note: Taxable amount in column (3) has two components: (i) capital gain on the asset sale and

(ii) recovered depreciation. Capital gain equals sale price –original purchase price of

P11-9 Tax calculations (LG 3, 4; Intermediate)

Current book value = Installed cost of asset ($200,000) – Accumulated depreciation

capital gain (if any).

P11-10 Change in net working capital calculation (LG 3; Basic)

a.

Current Assets Current Liabilities

Cash $15,0

00 Accounts payable $90,00

0

Accounts receivable 150,0

00 Accruals 40,00

0

c. Yes, in computing the terminal cash flow, the net working capital increase should be reversed.

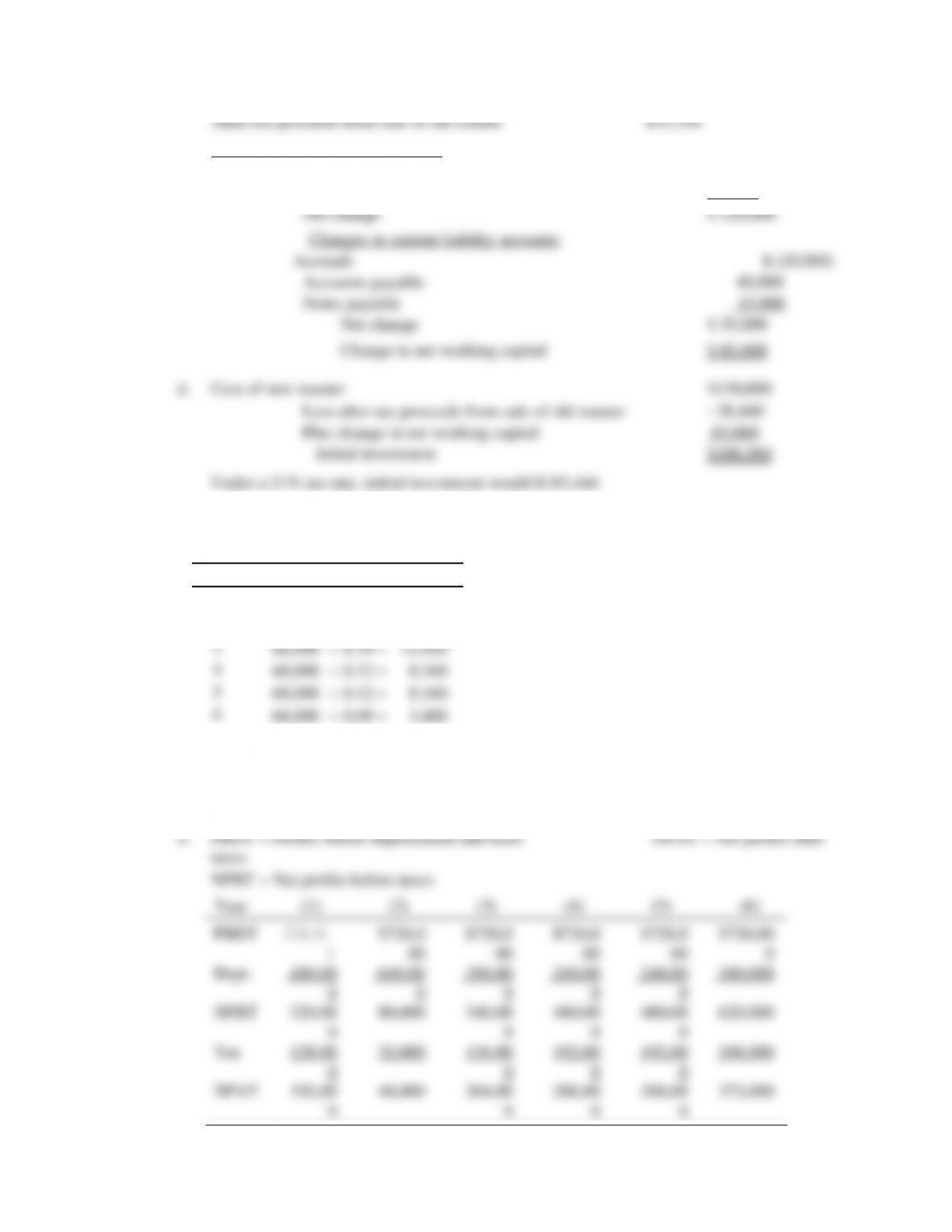

P11-11 Calculating initial investment (LG 3, 4; Intermediate)

a. Book value $325,000 (1 0.20 – 0.32) $325,000 0.48 $156,000

b. Sales price of old equipment $200,000

Book value of old equipment 156,000

c. Cost of new machine $500,000

Less sales price of old machine $(200,000)

Plus tax on recapture of depreciation (40% tax rate) $17,600

If the new computer qualified for 100% bonus depreciation, the firm could deduct the full cost

right away and realize tax savings equal to the cost of the machine times the tax rate, thus

reducing the initial outflow.

P11-12 Initial investment: Basic calculation (LG 3, 4; Intermediate)

Installed cost of new asset

Cost of new asset $35,000

Installation costs 5,000

Initial investment $22,680

Book value of existing machine $20,000 (1 (0.20 0.32 0.19)) $5,800

P11-13 Initial investment at various sale prices (LG 3, 4; Intermediate)

(a) (b) (c) (d)

Installed cost of new asset:

Cost of new asset $24,000 $24,00

0$24,00

0$24,00

0

Installation cost 2,000 2,000 2,000 2,000

Book value of existing machine $10,000 [1 (0.20 0.32 0.19)] $2,900

*Tax Calculations:

a. Recaptured depreciation

$10,000

$2,900

$7,100

Capital gain

$11,000

$10,000

$1,000

P11-14 Calculating initial investment (LG 3, 4; Challenge)

a. Book value ($60,000 0.31) $18,600

b. Sales price of old equipment $35,000

Book value of old equipment 18,600

Under a 21% tax rate, taxes on depreciation recovery = $16,400 0.21 $3,444

c. Changes in current asset accounts

Inventory $ 50,000

Accounts receivable 70,000

P11-15 Depreciation (LG 5; Basic)

Depreciation Schedule

Year Depreciation Expense

1$68,000 0.20 $13,600

2 68,000 0.32 21,760

P11-16 Incremental operating cash inflows (LG 5; Intermediate)

a. Incremental profits before depreciation and tax $1,200,000 $480,000

$720,000 each year.

b. Cash Flow = NPAT depreciation

Cash

flow (1)

$592,000 (2)

$688,000 (3)

$584,000 (4)

$528,000 (5)

$528,000 (6)

$472,000

P11-17 Personal finance: Incremental operating cash inflows (LG 5; Challenge)

Incremental Operating Cash Flows – Replacement of John Deere Riding Mower

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Savings from new and improved mower $500 $ 500 $500 $500 $500 —

Annual maintenance cost 120 120 120 120 120 0

Depreciation* 360 576 342 216 216 90

*MACRS Depreciation Schedule

Year Base MACRS Depreciation

Year 1 $1,800 20.0% $360

Year 2 1,800 32.0% 576

Year 3 1,800 19.0% 342

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Savings (loss) before taxes 20 –196 38 164 164 –90

Taxes (21%) 4.2 –41.16 7.98 34.44 34.44 –18.9

If the mower is eligible for 100% bonus depreciation, then the schedule would change to reflect

a much larger depreciation deduction in the first year and no depreciation deductions at all in

subsequent years.

P11-18 Incremental operating cash flows: Expense reduction (LG 5; Intermediate)

Year (1) (2) (3) (4) (5) (6)

Incremental

expense savings $16,00

0$16,0

00 $16,00

0$16,00

0$16,0

00 $ 0

Incremental profits

before dep. and

0 00

Taxes (40%) 2,560 256 2,752 4,096 4,096 960

Net profits

*Incremental profits before depreciation and taxes will increase the same amount as the decrease in expenses.

**Net profits after taxes plus depreciation expense.

With a 21% tax rate, the lower half of the table would be:

Year (1) (2) (3) (4) (5) (6)

Net profits before taxes 6,400 640 6,880 10,240 10,240