Chapter 11

Capital Budgeting Cash Flows

NOTE TO INSTRUCTORS: Shortly after the first press run for the 15th edition, Congress passed the Tax Cuts

and Jobs Act of 2017, which included changes in the corporate tax rate relevant to this chapter. In subsequent

printing runs, the text was updated to reflect the new tax law, but these updates may not appear in every

student’s copy of the text. Accordingly, solutions to problems P11-8, P11-11, P11-14, P11-17, P11-18, P11-20,

and P11-24 include answers based on the new as well as the old corporate income tax rate.

Instructor Resources

Chapter Overview

This chapter expands upon capital-budgeting techniques presented in the previous chapter. Shareholder

wealth maximization relies upon selection of projects with positive net present values. The most important

and difficult aspect of the capital-budgeting process is developing good estimates of the relevant cash flows.

Chapter 11 focuses on the basics of determining relevant after-tax cash flows of a project, from the initial

cash outlay to annual cash stream of costs and benefits and terminal cash flow. It also describes the special

concerns facing capital budgeting for multinational companies. The text highlights the importance of capital

budgeting to the post-graduate professional and personal lives students.

Suggested Answers to Opener-in-Review

The chapter opener talked about the $12 billion acquisition by Molson Coors of the MillerCoors joint

venture. According to Molson, the acquisition provided 15 years’ worth of tax savings in the amount of

The discount rate is the “r” that makes the following equation hold:

Present value = + + + … +

Answers to Review Questions

11-1 The decision to invest (or to refrain from investing) should be based on whether the added benefits

justify the added costs. Thus, capital budgeting projects should be evaluated using incremental

11-2 The three components of cash flow for any project are (1) initial investment, (2) operating cash

flows, and (3) terminal cash flows. Expansion decisions are merely replacement decisions in which

all cash flows from the old asset are zero.

11-3 Sunk costs are costs that have already been incurred and cannot be recovered. They should be

ignored in project analysis because whether the firm invests or not, the sunk costs will not be

recovered. Opportunity costs are cash flows that could be realized from the next best alternative use

11-4 To minimize long-term currency risk, companies can finance a foreign investment in local capital

markets so that the project’s revenues and costs are in the local currency rather than dollars.

Techniques such as currency futures, forwards, and options market instruments protect against

11-5 a. The cost of the new asset is the purchase price. (Outflow)

b. Installation costs are any added costs necessary to get an asset into operation. (Outflow)

the change in current liabilities. (May be an inflow or an outflow)

11-6 The book value of an asset is its strict accounting value.

Book value installed cost of asset – accumulated depreciation

Gains and losses in the sale of an asset may have tax consequences, and hence, these are key forms

of taxable income. More specifically, taxable income may arise from (1) capital gain: portion of

11-7 The asset may be sold at a price (1) above book value, (2) equal to book value, or (3) below book

value. In the second case, no taxes would be required. In the third case, a tax credit would occur.

11-8 The depreciable value of an asset is the cost of the asset plus any installation costs.

11-9 Depreciation is relevant because it reduces the firm’s tax liability even though it is not really a cash

outlay. In project cash flow calculations, subtract depreciation like any other expense, then

11-10 To calculate incremental operating cash inflow for both the existing situation and proposed project,

(incremental after-tax cash flows), is the relevant measure for evaluating the proposed project.

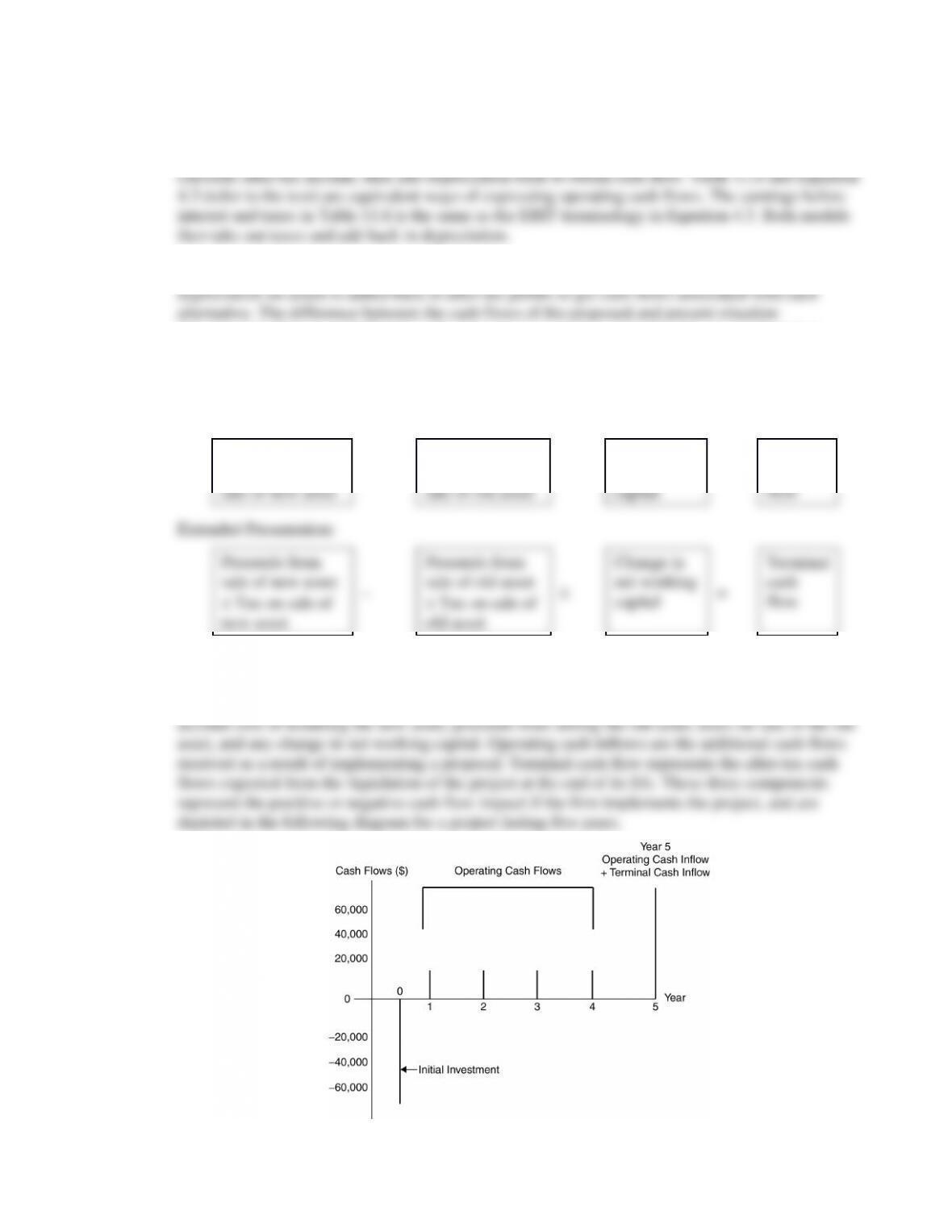

11-11 The terminal cash flow is the cash flow resulting from termination and liquidation of a project at the

end of its economic life. The form of calculating terminal cash flows is shown below:

Terminal Cash Flow Calculation:

After-tax

proceeds from

proceeds from

Change in

net working

cash

11-12 The relevant cash flows necessary for a conventional capital-budgeting project are the incremental

after-tax cash flows attributable to the proposed project: the initial investment, net operating cash

inflows, and terminal cash flow. The initial investment is the initial outlay required, taking into

Suggested Answer to Focus on Ethics Box: “Fumbling Sunk Costs”

Recommitting to a losing project for emotional or reputational reasons can destroy shareholder wealth.

What safeguards could a firm use to remove such bias from recommitment decisions?

The most important safeguard is to recognize the problem. If, for example, the project under consideration

for renewal is the “CEO’s Baby,” she is not likely to approach the decision objectively. In such cases, it

Suggested Answer to Global Focus Box:

“Changes May Influence Future Investments in China”

Although China has been actively campaigning for foreign investment, how do you think having

a communist government affects its foreign investment?

Having a communist government has a negative effect on foreign direct investment (FDI). As in all

investments abroad, FDI in China entails high travel and communications expenses. The differences of

political system and culture that exist between the country of the investor and the host country will also

Answers to Warm-Up Exercises

E11-1 Categorizing a firm’s expenditures

Answer: In this case, the tuition reimbursement should be categorized as a capital expenditure because

the outlay of funds is expected to produce benefits over a period of time greater than 1 year.

E11-2 Classification of project costs and cash flows

Answer: $3.5 billion already spent—sunk cost (irrelevant)

E11-3 Initial investment

Answer: Initial investment

= Price of new asset + Installation cost – After-tax proceeds of sale of old asset

E11-4 Book value and recaptured depreciation

Answer: Book value $175,000 $124, 250 $50,750

E11-5 Initial investment

Answer: Initial investment

Note: Change in net working capital is treated as an outflow (cost), hence the positive number.