P10-24 All techniques—decision among mutually exclusive investments (LG 2, 3, 4, 5, 6; Challenge)

Project A Project B Project C

Project Cost (year 0) 60,000$ 100,000$ 110,000$

Cash inflows (years 1-5) 20,000$ 31,500$ 32,500$

a. Payback* 3 years 3.2 years 3.4 years

b. NPV* 10,345$ 10,793$ 4,310$

c. IRR* 19.86% 17.33% 14.59%

*Supporting calculations below.

Project B: $100,000 $31,500 3.2 years

Project B: NPV = Present value of cash inflows – Initial outlay.

Present value of cash inflows = PV(0.13,5,-31500) = $110,792.78

c. IRR

Project A: To use the IRR command in Excel, start by putting cash outflows and inflows in

adjacent cells starting with project cost expressed as a negative number. If, for

Project B: To use the IRR command in Excel, put cash outflows and inflows in adjacent cells

starting with project cost expressed as a negative number. If all cash flows are

Project C: To use the IRR command in Excel, put cash outflows and inflows in adjacent cells

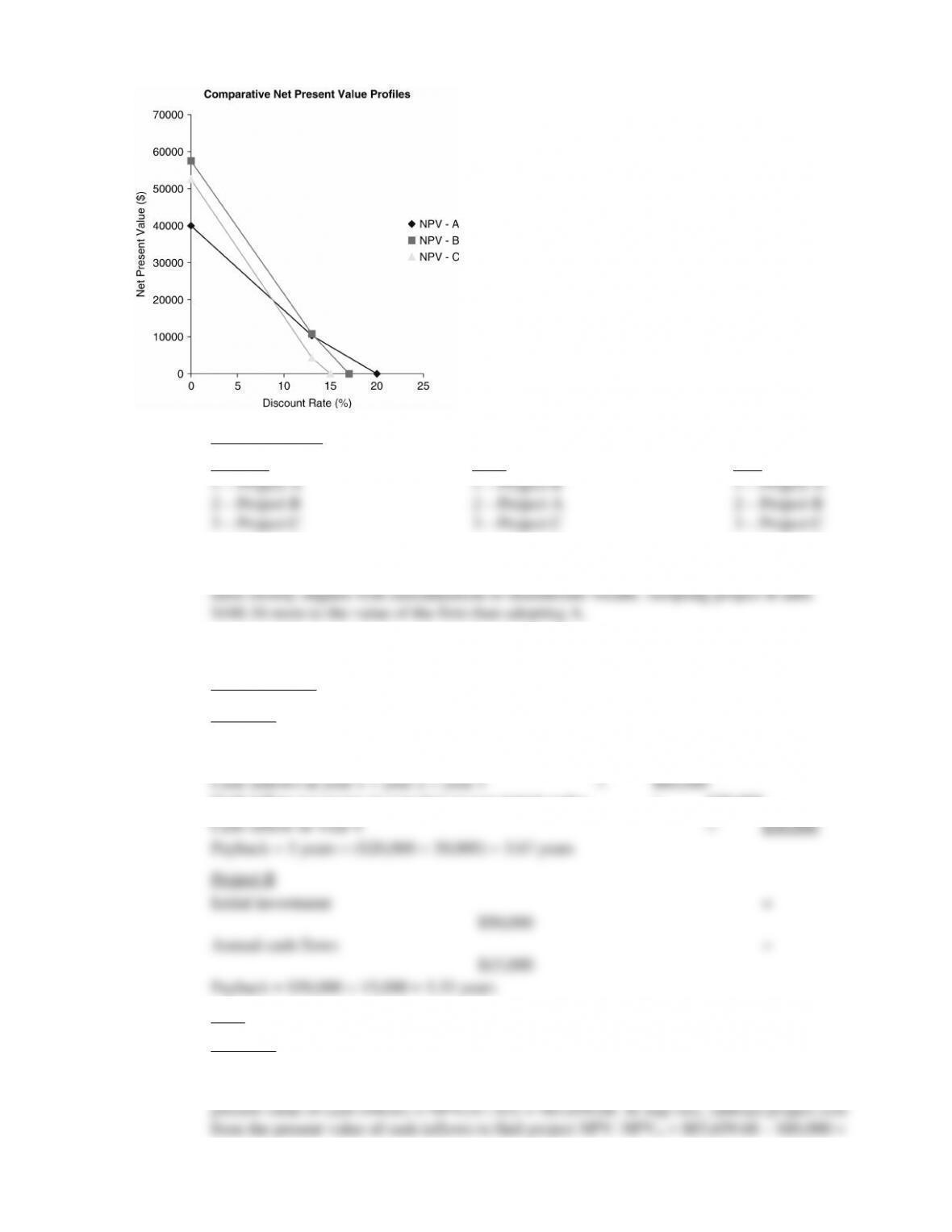

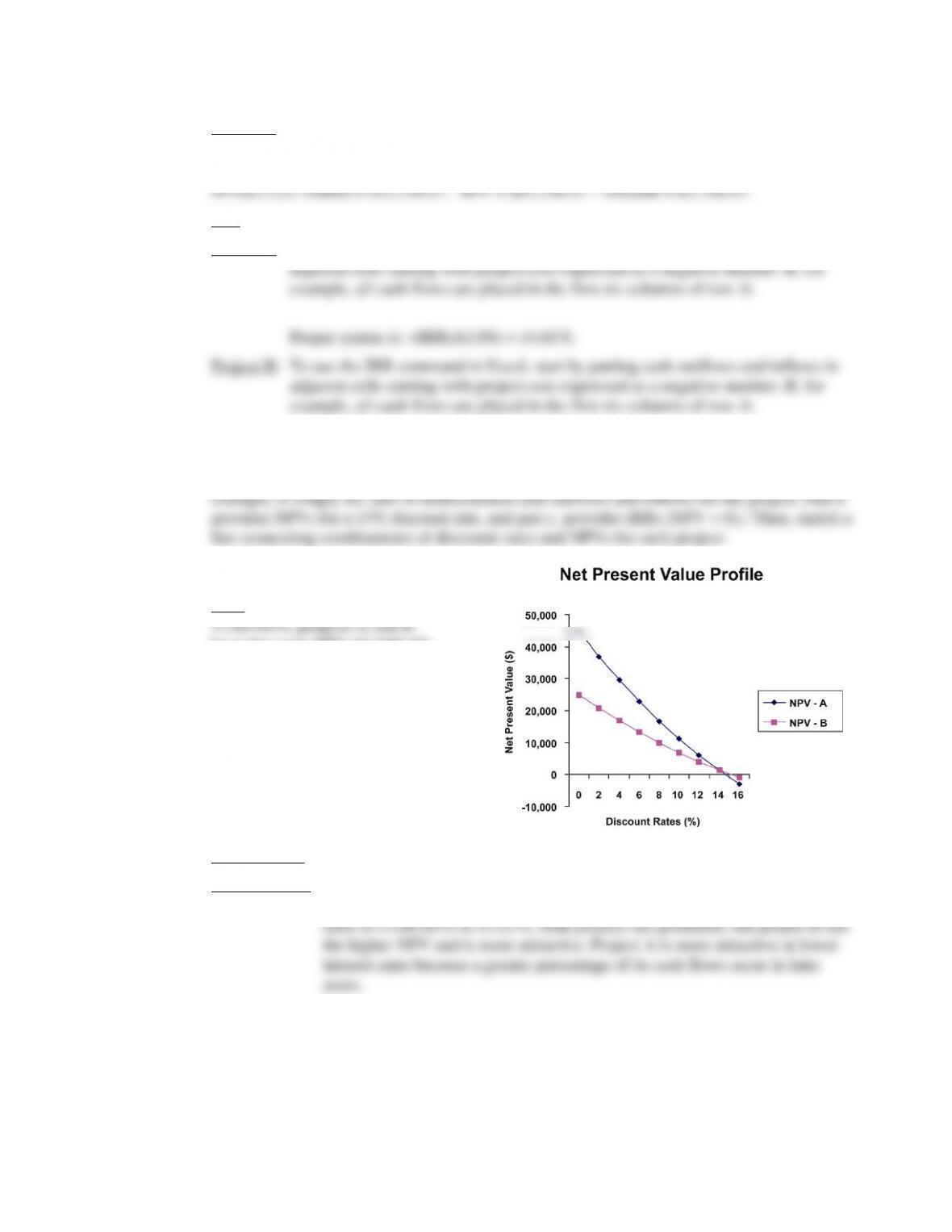

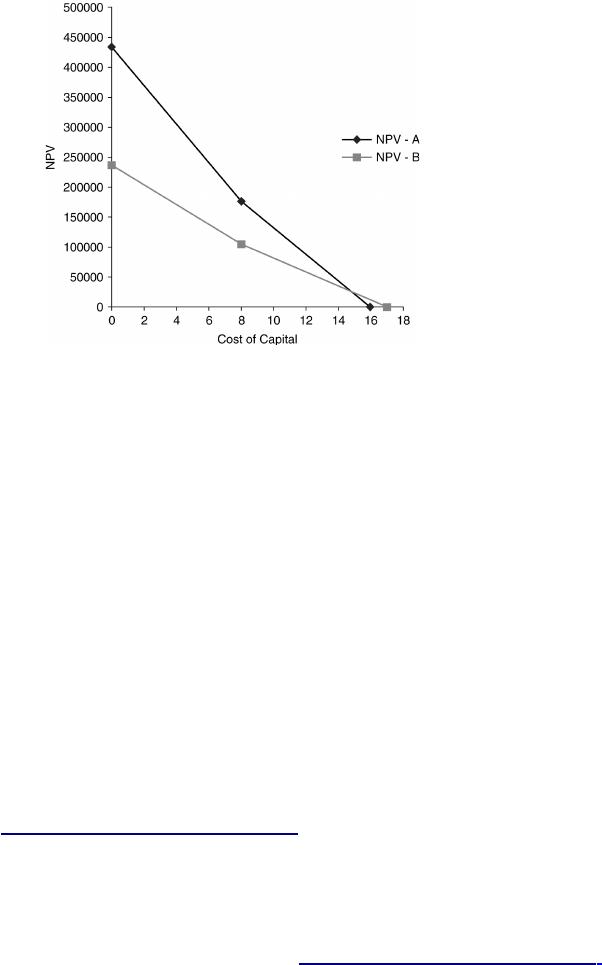

d. To obtain NPV profiles for projects A, B,

and C, begin by noting the NPV for all

three at a zero discount rate is the

projects is zero. The NPV

profiles are lines connecting

e. Project rankings:

Payback:

1 – Project A

IRR:

3 – Project C

Even though A ranks higher in Payback and IRR, financial theorists would argue B is superior

because it has the highest NPV. The rationale is that NPV is the capital-budgeting technique

P10-25 All techniques with NPV profile—mutually exclusive projects (LG 2, 3, 4, 5, 6; Challenge)

a. Payback period:

Project A

Initial investment

$80,000

Cash inflow necessary in year 4 to recoup initial outlay = $20,000

b. NPV (at a 13% discount rate):

Project A

NPV may be found in Excel in two steps. In step one, place cash inflows 1–5 in adjacent cells

in a row or column. If, for example, CF1 to CF5 appear in column A, rows 1 through 5, the

$3,659.68.

Project B

NPV = Present value of cash inflows – Initial outlay.

Present value of cash inflows = PV(discount rate, number of periods, -cash inflows)

c. IRR

Project A: To use the IRR command in Excel, start by putting cash outflows and inflows in

Proper syntax is: =IRR(A1:F6) = 15.24%.

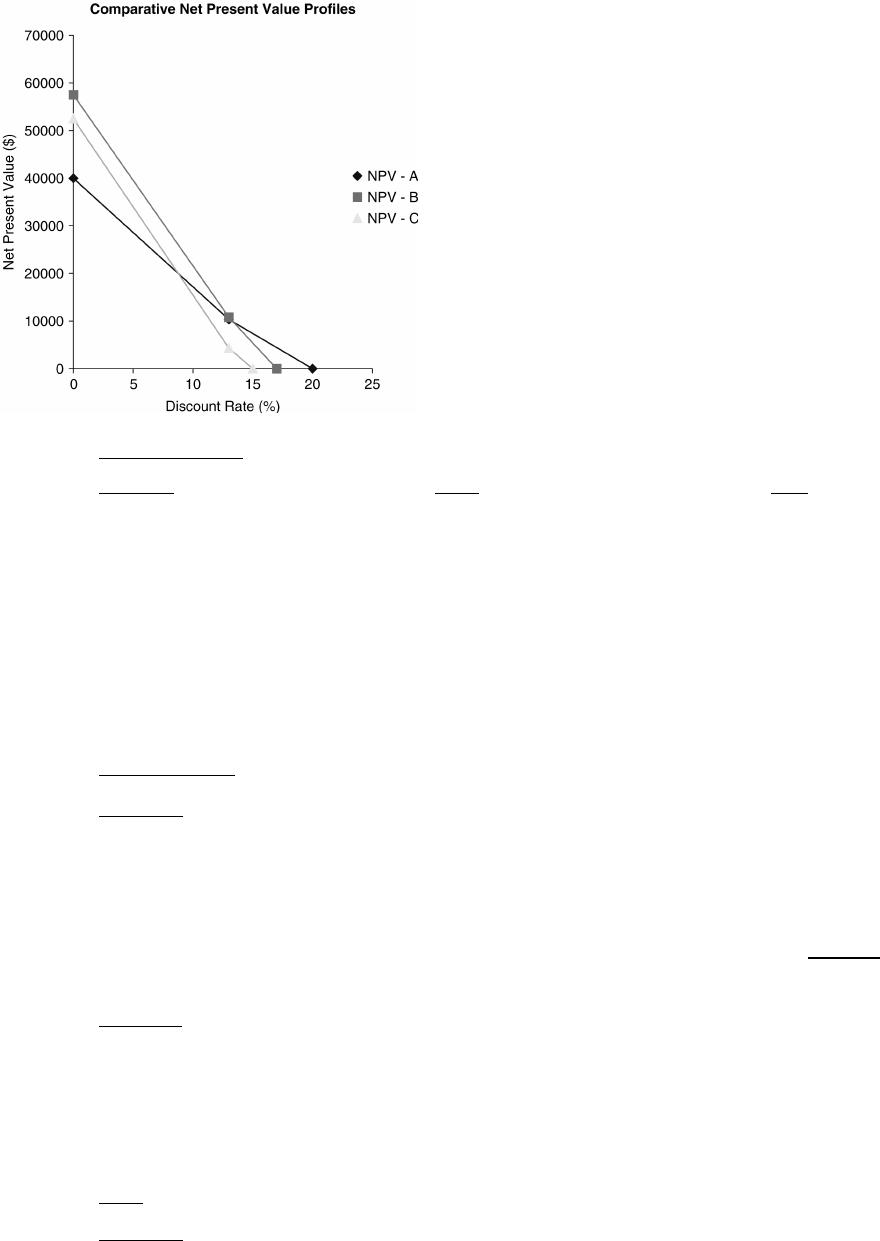

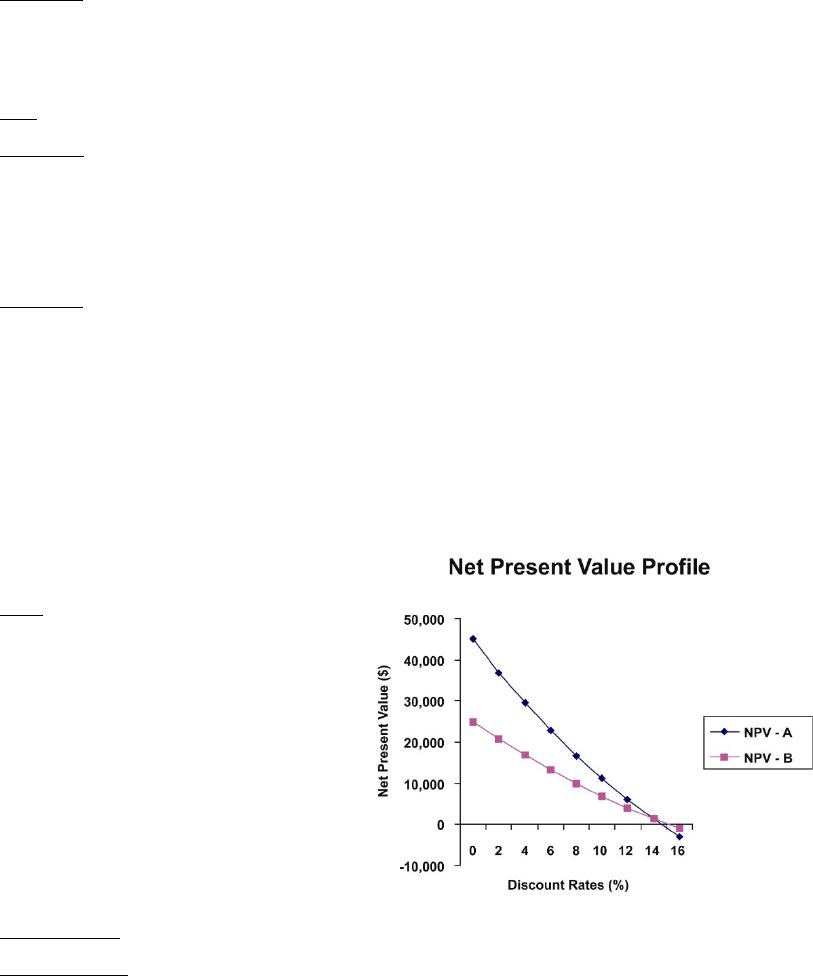

d. To find the NPV profiles for projects A and B, begin by generating a set of points representing

combinations of discount rates and NPVs for each project. [NPV for a 0% discount rate, for

Note: At a discount rate of

have the same NPV ($1,660.45)

IRR Decision: Project B has the higher IRR and is, therefore, the more desirable project.

NPV Decision: At a discount rate of 13.86765%, both projects have the same NPVs. Below

that rate, project A has the higher NPV (and is more attractive). For discount

e.

Project A Project B

Payback 2 1

NPV (13%) 1 2

IRR 2 1

RANKINGS

The capital-budget method most closely aligned

with maximizing shareholder wealth is NPV. Based

P10-26 Integrative—Multiple IRRs (LG 6; Basic)

a. Calculating the payback period for this project is difficult because of its unusual pattern of cash

flows. For example, there is no initial cash outflow; the cash flow in year 0 is an inflow.

b.

c. The project has multiple IRRs; four discount rates (0%, 10%, 20%, and 30%) yield zero NPVs.

d. Using the IRR approach to make an accept/reject decision for this project is difficult because it

is unclear which IRR should be compared with the cost of capital. The NPV approach yields

e. The NPV approach dominates when an unusual cash-flow pattern produces multiple IRRs.

(Note: NPV is the capital-budgeting method most closely aligned with maximizing

rate.)

P10-27 Integrative: Conflicting Rankings (LG 3, 4, 5; Intermediate)

a. and b.

Cash flows in thousands. Discount rate = 20%.

Year Cash Flows Discounted Cash Flows Discounted

0 (3,500)$ (3,500.00)$ (500)$ (500.00)$

1 1,500$ 1,250.00$ 250$ 208.33$

2 2,000$ 1,388.89$ 350$ 243.06$

3 2,500$ 1,446.76$ 375$ 217.01$

4 2,750$ 1,326.20$ 425$ 204.96$

NPV = 1,911.84$ 373.36$

NPV Rank: 1 2

IRR = 43.70% 52.33%

IRR Rank: 2 1

PI = 1.55 1.75

PI Rank: 2 1

Product Introduction

Plant Expansion

The rankings do not agree.

Plant expansion boasts the higher NPV, but project introduction offers the higher IRR and PI.

The rankings do not agree because the plant expansion has a much larger scale. NPV

d. High-Flying Growth should undertake plant expansion because it offers the higher NPV (and

would, therefore, add more to shareholder wealth, even though it has a lower rate of return).

P10-28 Problems with IRR (LG 4, 5; Intermediate)

a.

0.0% 5.0% 7.5% 10.0% 15.0% 20.0% 22.5% 25.0% 30.0%

Year Cash Flows Discounted Discounted Discounted Discounted Discounted Discounted Discounted Discounted Discounted

0 1,690,000$ 1,690,000$ 1,690,000$ 1,690,000$ 1,690,000$ 1,690,000$ 1,690,000$ 1,690,000$ 1,690,000$ 1,690,000$

1 (3,887,000)$ (3,887,000)$ (3,701,905)$ (3,615,814)$ (3,533,636)$ (3,380,000)$ (3,239,167)$ (3,173,061)$ (3,109,600)$ (2,990,000)$

2 2,225,025$ 2,225,025$ 2,018,163$ 1,925,387$ 1,838,864$ 1,682,439$ 1,545,156$ 1,482,732$ 1,424,016$ 1,316,583$

NPV = 28,025$ 6,259$ (427)$ (4,773)$ (7,561)$ (4,010)$ (329)$ 4,416$ 16,583$

Discount Rate =

b. Normally, NPV falls as the discount rate rises. Here, however, NPV falls as the rate rises from

should be accepted or rejected. Put another way, it is difficult to apply the IRR decision rule

unless all IRRs are above or below the cost of capital.

P10-29 Ethics problem (LG 1, 6; Intermediate)

a. Note: Cash flows in thousands, and

the discount rate is 10%. At this cost

of capital, the LED project has the

higher (and only positive) NPV, so

only that project should be accepted.

b.

Year Cash Flows Discounted Cash Flows Discounted

0 (4,200)$ (4,200.00)$ (500)$ (500.00)$

1 700$ 636.36$ 60$ 54.55$

2 700$ 578.51$ 60$ 49.59$

3 700$ 525.92$ 60$ 45.08$

4 700$ 478.11$ 60$ 40.98$

5 1,000$ 620.92$ 60$ 37.26$

6 700$ 395.13$ 60$ 33.87$

7 700$ 359.21$ 60$ 30.79$

8 700$ 326.56$ 60$ 27.99$

9 700$ 296.87$ 60$ 25.45$

10 700$ 269.88$ 60$ 23.13$

NPV = 287.47$ NPV = (131.33)$

Solar Project

LED Project

Combined project

part c.)

c. The projects are not, however, inseparable, and only the LED project has a positive NPV. So

pursuing the projects jointly would deprive shareholders of over $131,000 in value. [Put

Case: “Making Norwich Tool’s Lathe Investment Decision”

Case studies are available on www.pearson.com/mylab/finance.

Norwich Tool must use the capital-budgeting techniques introduced in this chapter to select one of

two lathes with different initial outlays and cash-inflow patterns to replace an existing lathe.

a., b., and c. Note: Cash flows in thousands.

Payback period

Lathe A:

Under the payback approach, Lathe A will be rejected because payback is longer than the 4-year

maximum accepted; Lathe B is acceptable because the payback period is less than the 4-year cutoff.

NPV and IRR

The NPV decision criterion indicates both lathes are acceptable because NPVA and NPVB > 0. Lathe A

ranks ahead of B because of its larger NPV. IRR is the discount rate that makes project NPV = 0 for

the given cash flows; the IRR for each lathe as calculated with the IRR command in Excel appears in

c. Summary:

Lathe A Lathe B

Payback period 4.04 years 3.65 years

Rank 2* 1

* Maximum acceptable payback period is 4

years, so strict application of that threshold

implies Lathe A is unacceptable (and,

therefore, should be excluded from the ranking

of admissible projects).

Only one lathe is needed, and IRR and NPV provide different recommendations. But NPV is the

superior capital-budgeting technique because it is most closely aligned with maximizing shareholder

wealth. The more attractive project by the NPV criterion is Lathe A because it has the higher NPV.

d. To create an NPV profile, identify the NPVs for each project for three or more discount rates.

Lathe B is preferred to Lathe A based on IRR. As can be seen in the NPV profiles, however,

to the left of the point where the two lines cross (i.e., discount rates below 14.504%), Lathe A is

e. On a theoretical basis, Lathe A is more attractive because of its higher NPV (larger positive

impact on shareholder wealth). From a practical perspective, Lathe B may be selected because

of its higher IRR and its faster payback, reflecting manager preference for projects offering

higher percent returns and faster recovery of initial outlays.

Spreadsheet Exercise

Answers to Chapter 10’s Drillago Company exercise on capital budgeting are available on

www.pearson.com/mylab/finance..

Group Exercise

Group exercises are available on www.pearson.com/mylab/finance .

This assignment builds on the long-term investment projects in the previous chapter. Because students were

required to estimate relevant cash flows before reading this chapter, some numbers may have to be altered to

ensure each project has sensible payback periods. Allowing students to revisit previous estimates should

make their numbers more realistic and easier to work with.

The first task is calculating payback periods for each of the projects. Then, students will calculate NPV for

each project such that NPVs exceed zero. The crucial part of this step is estimating the discount rate for

NPV calculation. Each group must defend its discount rate. The final calculation is the IRR for each project.

Given calculations of payback period, NPV, and IRR for each project, groups are next asked choose a

project. This process should be detailed to give students a sense of the challenges of weighing projects.

Groups should include a summary of the analysis based on each capital-budgeting method and a defense of the

interpretation of results should be included in their write-ups. Giving students a range of potential projects to

evaluate will help them master the capital-budgeting techniques presented in this chapter.