Solutions to Problems

P10-1 Payback period (LG 2; Basic)

b. The company should accept the project because payback period (7.23 years) is less than the

maximum acceptable period (8 years).

P10-2 Payback comparisons (LG 2; Intermediate)

b,c. The maximum acceptable payback period is 5 years. Only Machine 1 has a faster payback, so

Nova should accept only that project.

d. Yes, Machine 2 has returns that last 20 years while Machine 1 has only 7 years of returns. The

P10-3 Choosing between two projects with acceptable payback periods (LG 2; Intermediate)

a.

Both projects have payback periods of exactly 4 years.

b. Based on the maximum acceptable payback period of 4 years set by John Shell, both projects

are equally attractive. If the projects are mutually exclusive projects, John should accept B.

c. Project B is preferred because it offers larger cash flows in the early years. [Note: By the end of

P10-4 Personal finance: Long-term investment decisions, payback period (LG 2; Intermediate)

a. and b. Project A Project B

Year Annual

Cash Flow Cumulative

Cash Flow Annual

Cash Flow Cumulative

Cash Flow

1 $2,200 $2,200 $1,500 $1,500

2 2,500 4,700 1,500 3,000

c. Project A is more attractive than project B because of its shorter payback period.

d. One shortcoming of the payback method is its disregard of total cash flows over project life.

Here, for example, project A generates $11,000 in total cash flows (implying an NPV at a zero

discount rate of $2,000), while total cash flows for project B equal $12,000, implying an NPV

P10-5 NPV (LG 3; Basic)

NPV Present value of cash inflows from project Initial investment. All projects have 15-year

inflows is:

a. Annual cash inflows = $150,000, so present value = PV(.09, 15, -150000) = $1,209,103.26

NPV $2,942,151.28 $3,000,000 = $ NPV is negative, so project should be

rejected.

P10-6 NPV for varying cost of capital (LG 3; Basic)

NPV Present value of cash inflows from project Initial investment. All projects have 8-year

lives, an initial cost of $360,000, and annual cash inflows of $62,650. The Excel command for

a. Cost of capital = 6%, so present value of cash inflows = PV(0.06,8,62650) = $389,043.58.

b. Cost of capital = 8%, so the present value of cash inflows = PV(0.08,8,62650) = $360,026.93.

amount).

P10-7 NPV: Independent projects (LG 3; Intermediate)

All cash flows in thousands. NPV = Present value of all cash outflows and inflows.

Year

Cash Flows Discounted Cash Flows Discounted Cash Flows Discounted Cash Flows Discounted Cash Flows Discounted

0 (250)$ (250)$ (375)$ (375)$ (550)$ (550)$ (750)$ (750)$ (1,150)$ (1,150)$

1 50$ 45.45$ 45$ 40.91$ 350$ 318.18$ 200$ 182$ 80$ 72.73$

2 90$ 74.38$ 55$ 45.45$ 210$ 173.55$ 235$ 194$ 135$ 111.57$

3 140$ 105.18$ 65$ 48.84$ 165$ 123.97$ 250$ 188$ 190$ 142.75$

4 80$ 54.64$ 55$ 37.57$ 55$ 37.57$ 265$ 181$ 255$ 174.17$

5

NPV = 29.66$

45$ 27.94$ 45$ 27.94$ 100$ 62$ 315$ 195.59$

6 35$ 19.76$ 10$ 5.64$ 50$ 28$ 380$ 214.50$

7 25$ 12.83$

NPV = 136.85$ NPV = 85.18$

275$ 141.12$

8 15$ 7.00$ 100$ 46.65$

9 5$ 2.12$ 45$ 19.08$

10

NPV = (132.59)$

25$ 9.64$

NPV = (22.20)$

Project E

ACCEPT

ACCEPT

ACCEPT

ACCEPT

REJECT

Project A

Project B

Project C

Project D

P10-8 NPV (LG 3; Challenge)

a. In Excel, the present value of a 5-year, $385,000 annuity (paid at year-end), discounted at 9%

is:

present-value terms than the one-time immediate payment of $1.5 million.

b. In Excel, the series of year-end payments over 5 years with a present value of $1.5 million is:

c. The payment stream is now $385,000 today and 4 end-of-year payments of $385,000. In

Excel, the present value of the 4 end-of-year payments is:

Now, Simes would prefer the one-time immediate payment of $1.5 million because it is less

than the present value of five, beginning of year payments of $385,000.

d. The present value of the cash inflows expected from the solar-powered toy car is given by:

Simes should choose the payment option with the lowest present value.

P10-9 NPV and maximum return (LG 3; Challenge)

a. NPV = Present value of cash inflows – initial investment ($150,000). In Excel, present value

of cash inflows =PV(0.10,4,44400) = $140,742.03.

figure, NPV will be positive, and project should be accepted.

P10-10 NPV: Mutually exclusive projects (LG 3; Intermediate)

a.,b., c, d and e.

Cash flows in thousands. Negative numbers are outflows; positive inflows. Profitability Index

P10-11 Personal finance: Long-term investment decisions, NPV method (LG 3; Intermediate)

Upfront cost of MBA program $100,000

($50,000 for tuition and $50,000 for lost earnings)

Incremental benefit (higher salary per year) $20,000

P10-12 Payback and NPV (LG 2, 3; Intermediate)

a.

Project Payback Period Payback Rank

A $40,000 $13,000 3.08 years 2

b.

c. With a 16% cost of capital, Project C offers the highest NPV and the shortest payback period.

Project C has relatively high cash flows in the early years; indeed, 87.5% of project cost is

important criterion is NPV because of its connection to shareholder wealth maximization.

P10-13 NPV and EVA (LG 3; Intermediate)

a. NPV = Present value of cash inflows – Initial outlay ($2.5 million). Because cash inflows are a

b. Annual EVA Annual cash inflow – Annual opportunity cost of capital

c. Overall EVA Present value of annual EVA, discounted at the cost of capital = $15,000

same.

P10-14 Internal rate of return (LG 4; Intermediate)

For a given set of cash flows, IRR is the interest rate that makes project NPV = 0:

To obtain IRR in Excel , start by arranging the cash inflows in adjacent cells in a row or column

beginning with the cash outflow in year 0. For example, if the cash flows for project A are placed in

IRR.

P10-15 Internal rate of return (LG 4; Intermediate)

For Peach of Mind, inc. (PMI), offering extended warranties is profitable only if the

marginal benefit (price customer pays) exceeds the marginal cost (present value of outlays

costs, so PMI should offer extended warranties.

Another approach is to compute the

compare that IRR to the 7% cost of

capital:

Project IRR is only 4%. Usually, when the cost of capital exceeds IRR, the firm should

reject the project. Here, however, cash flows have the opposite sign from usual (i.e., there

P10-16 IRR: Mutually exclusive projects (LG 4; Intermediate)

a. and b.

Annual project cash outflows and

inflows appear in the columns under

the project heading.

P10-17 Personal Finance: Long-term investment decisions, IRR method (LG 4; Intermediate)

a.

b. IRR is the discount rate such that NPV = 0. Here, project NPV = 0 for discount rates of 0%,

10%, 20%, and 30%—implying IRR can take all four values. The unconventional cash-flow

pattern (multiple sign changes) explains the multiple IRRs. With multiple IRRs, it is not clear

c. The largest cash outflow (–$602.6) occurs in year 3. Other things equal, a change in the

discount rate will have a larger impact on present value when the outflow or inflow occurs

P10-18 IRR, investment life, and cash inflows (LG 4; Challenge)

a. In Excel, arrange the one cash outflow (–$61,450) and 10 cash inflows ($10,000) in 11

b. To find the number of years $10,000 would have to be received to make the project acceptable

by the IRR decision rule, use the NPER command in Excel. The proper syntax is:

c. To find the minimum cash inflows over 10 years that would make the project acceptable, use

the PMT command in Excel. The proper syntax is:

P10-19 NPV and IRR (LG 3, 4; Intermediate)

a. NPV = Present value of cash inflows – Initial investment ($18,250). In Excel, the present value of cash

inflows = PV(0.10,7,-4000) = $19,473.68. So, NPV = $19,473.68 – $18,250 = $1,223.68.

b. To find IRR in Excel, place the one cash outflow (-18250) and 7 cash inflows (4000) in

P10-20 NPV, with rankings (LG 3, 4; Intermediate)

Note: IRR was obtained in Excel and the following syntax (cash flows arranged in the first four

9.7%.

P10-21 All techniques, conflicting rankings (LG 2, 3, 4: Intermediate)

a., b., c., and d.

Project NPVs

At a 0% discount rate, each year’s discounted cash flow equals the undiscounted cash flow. so:

NPVA Present value of cash flows ($270,000) – Initial outlay ($150,000) $120,000.

Project IRRs

To find IRR in Excel, place cash flows in adjacent cells in a row or column starting with

project cost expressed as a negative number, and use the IRR command. Answers appear in the

table.

e. Project Rankings by Various Approaches to Capital Budgeting:

Project Payback NPV IRR

Nicholson Roofing should use the NPV ranking (and choose project A) because NPV is more closely tied to

maximizing shareholder wealth. Indeed, NPV indicates exactly how much a project will benefit shareholders.

f. Project NPVs (at a 12% rate):

the NPV of both projects but had a smaller impact on project B’s NPV because a larger

percentage of the project annual cash flows occur in the early years.

P10-22 Payback, NPV, and IRR (LG 2, 3, 4; Intermediate)

a. Payback period:

b. NPV computation

(12% discount rate):

Another approach is to use the NPV command in Excel. This command is misleading in that it

generates the present value of an unequal stream of cash inflows, not actual NPV. To obtain

project NPV, the initial outlay must be subtracted from the figured generated by the NPV

c. To find IRR in Excel, arrange cash outflows and inflows in adjacent cells in a row or column

and use IRR command. If, for example, CF0 ($95,000) is in A1; CF1 ($20,000) is in A2; CF2

d. NPV approach: NPV , so project should be accepted.

The project should be undertaken because it satisfies the decision criteria for both NPV and

IRR approaches to capital budgeting.

P10-23 NPV, IRR, and NPV profiles (LG 3, 4, 5; Challenge)

a. and b.

Project A

NPV: In Excel, put CF1 (25000) in A1; CF2 (35000) in A2; CF3 (45000) in A3; CF4 (50000) in

A4; and CF5 (55000) in A5. Then, use the NPV command to obtain the present value of

decision criterion, project A should be accepted.

IRR: In Excel, put cash flows in adjacent cells starting with project cost (expressed as a

negative number because it is an outflow). If, for example, cash flows appear in the first

six rows of column A with CF0 (-130000) in A1, CF1 (25000) in A2, CF2 (35000) in A3,

Project B

NPV: In Excel, put 40000 in A1, 35000 in A2, 30000 in A3, 10000 in A4, and 5000 in A5.

Then, use the NPV command to obtain the present value of these inflows; proper

NPV > 0, so project B should be accepted.

IRR: In Excel, put cash flows in adjacent cells starting with project cost (expressed as a

negative number because it is an outflow). If, for example, cash flows appear in the first

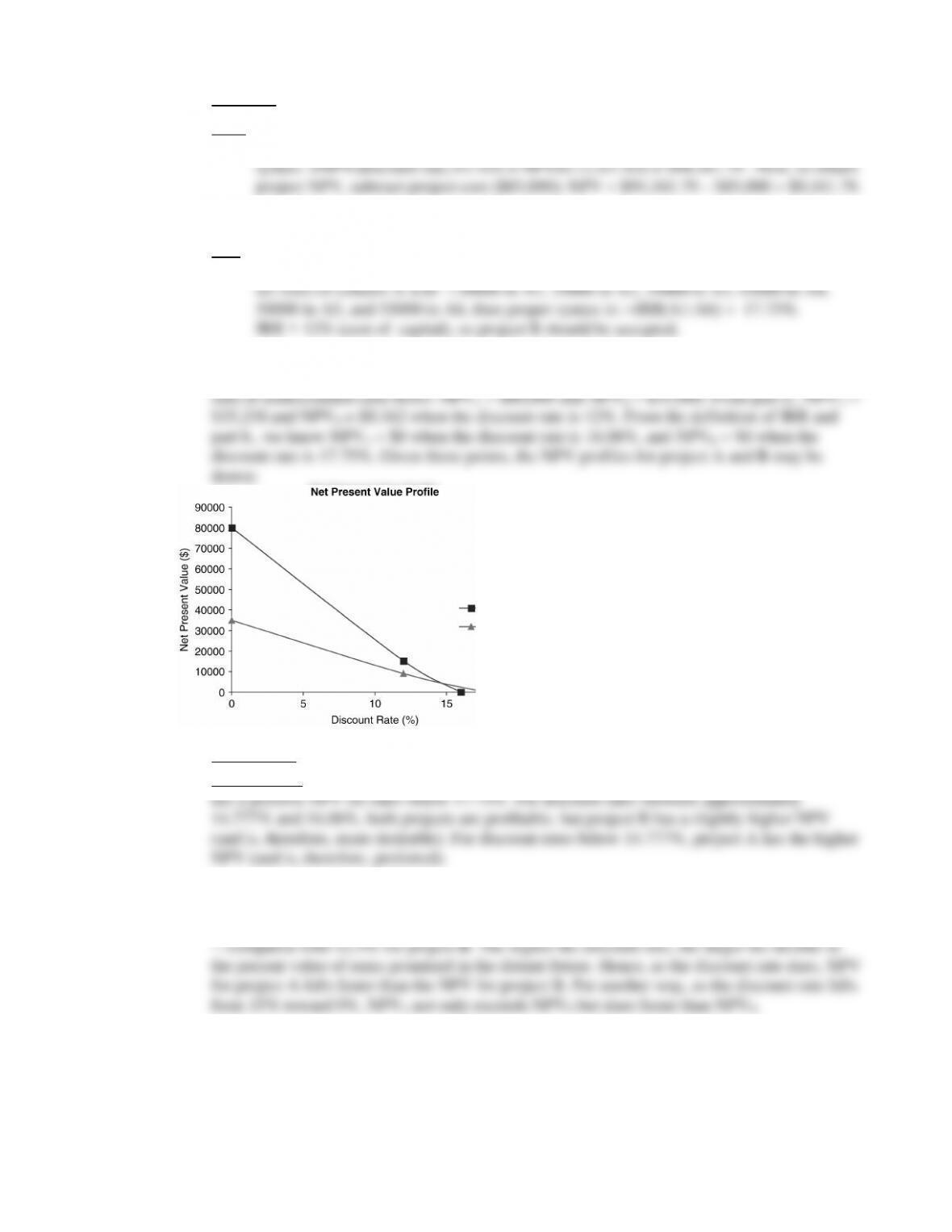

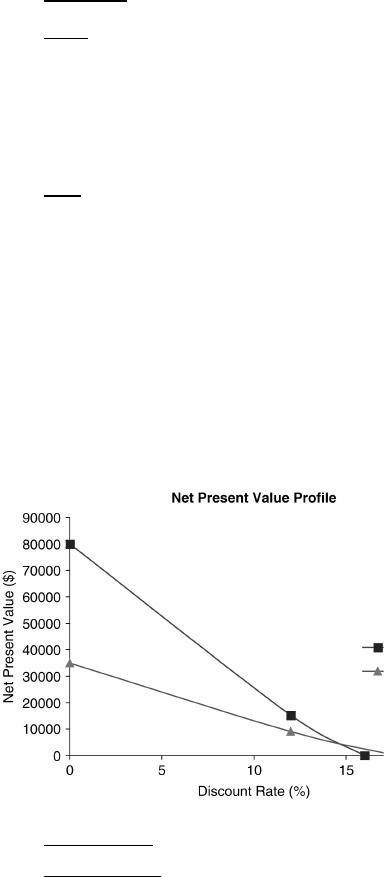

c. To draw NPV profiles for projects A and B, find NPVs for both projects over a range of

discount rates. Start with the NPV for both projects at a 0% discount rate (which is simply the

Note the two projects have

NPVs of roughly $4,532

when the discount rate is

14.777%.

d. IRR ranking: IRRA = 16.06% and IRRB = 17.75%, so project B is always preferred.

NPV ranking: Project A has a positive NPV for discount rates below 16.06%, and project B

e. The change in rankings above and below 15% stems from the different cash-flow patterns of

the two projects. Total undiscounted cash inflows are $80,000from project A and $35,000

from project B. But 50% of project A’s undiscounted cash inflows occur in the last two years