Solutions to Problems

P1-1. Liability comparisons (LG 5; Basic)

a. Ms. Harper has unlimited personal liability, so she is liable for the firm’s $60,000 in unpaid

debts.

P1-2. Accrual income vs. cash flow for a period (LG 4; Basic)

a. Sales $760,000

Cost of goods sold 300,000

Net profit $460,000

P1-3. Personal finance: cash flows (LG 4; Intermediate)

a. Total cash inflow: $450 $4,500 $4,950

d. Jane should examine anticipated cash flows in other months to verify August is typical. She

may, for instance, discover expenditures not in her August budget—like large quarterly

P1-4. Marginal benefit-marginal cost analysis and goal of the firm (LG 2 and LG 4; Challenging)

a. Marginal benefits of proposed robotics =

Marginal benefits of new robotics Marginal benefits of original robotics

$560,000 $400,000 $160,000

d. Provided cash flows from new and existing robotics are equally risky and either (i) cash flows

from each option have the same timing or (ii) the discount (interest rate) is zero, Ken Allen

should recommend new robotics because the marginal benefits exceed marginal costs.

e. Three other important factors are cash-flow risk, cash-flow timing, and interest rates. New

P1-5. Identifying agency problems, costs, and resolutions (LG 6; Intermediate)

a. The agency cost is wages paid to an idle employee whose responsibilities must be covered by

someone else. One solution is a time clock everyone must punch when arriving for work, take a

b. The agency costs are opportunity costs—money budgeted for inflated cost estimates that cannot

c. The agency cost is lost shareholder wealth; the CEO might agree to sell the firm for less than

fair-market value in return for a post-merger position with more income, wealth, power, or

d. Part-time or temporary workers are less productive than full-time workers for two reasons: (i)

new employees must learn their jobs, and (ii) fully trained employees obtain insights about

improving efficiency from experience. In the short run, any decline in service caused by part-

P1-6 Corporate taxes (LG 5; Basic)

a. Firm’s tax liability on $92,500 using Table 1.2:

For students with the text updated with the latest tax information, the taxes due would be 21% ×

b. After-tax earnings: $92,500 – $19,700 $72,800. For students with the text updated with the

c. Average tax rate: $19,700 ÷ $92,500 21.3%. For students with the text updated with the latest

d. Marginal tax rate: 34%. For students with the text updated with the latest tax information, the

P1-7 Average corporate tax rates (LG 6; Basic)

a. Tax calculations using Table 1.2:

$10,000: Tax liability: $10,000 0.15 $1,500

After-tax earnings: $10,000 – $1,500 $8,500

Average tax rate: $1,500 ÷ $10,000 15%

$300,000: Tax liability: $22,250 + [0.39 ($300,000 – $100,000)]

= $22,250 + $78,000 = $100,250

$1,500,000: Tax liability: $113,900 [0.34 ($1,500,000 –

$335,000)] = $113,900 $3,286,100 =$3,400,000

$18,333,333)] = $6,416,667 583,333 = $7,000,000

answers appear below. The answers assume that the person receiving this income flowing from a partnership has

no other income.

a. Tax calculations using Table 1.2:

$10,000: Tax liability: $953 $475 0.12 = $1,010

After-tax earnings: $10,000 – $1,010 $8,990

Average tax rate: $1,010 ÷ $10,000 10.1%

$300,000: Tax liability: $45,690 + [0.35 ($300,000 – $200,000)] =

$1,500,000: Tax liability: $150,690 + [0.37 ($1,500,000 –

Average tax rate: $705,690 ÷ $2,000,000 35.3%

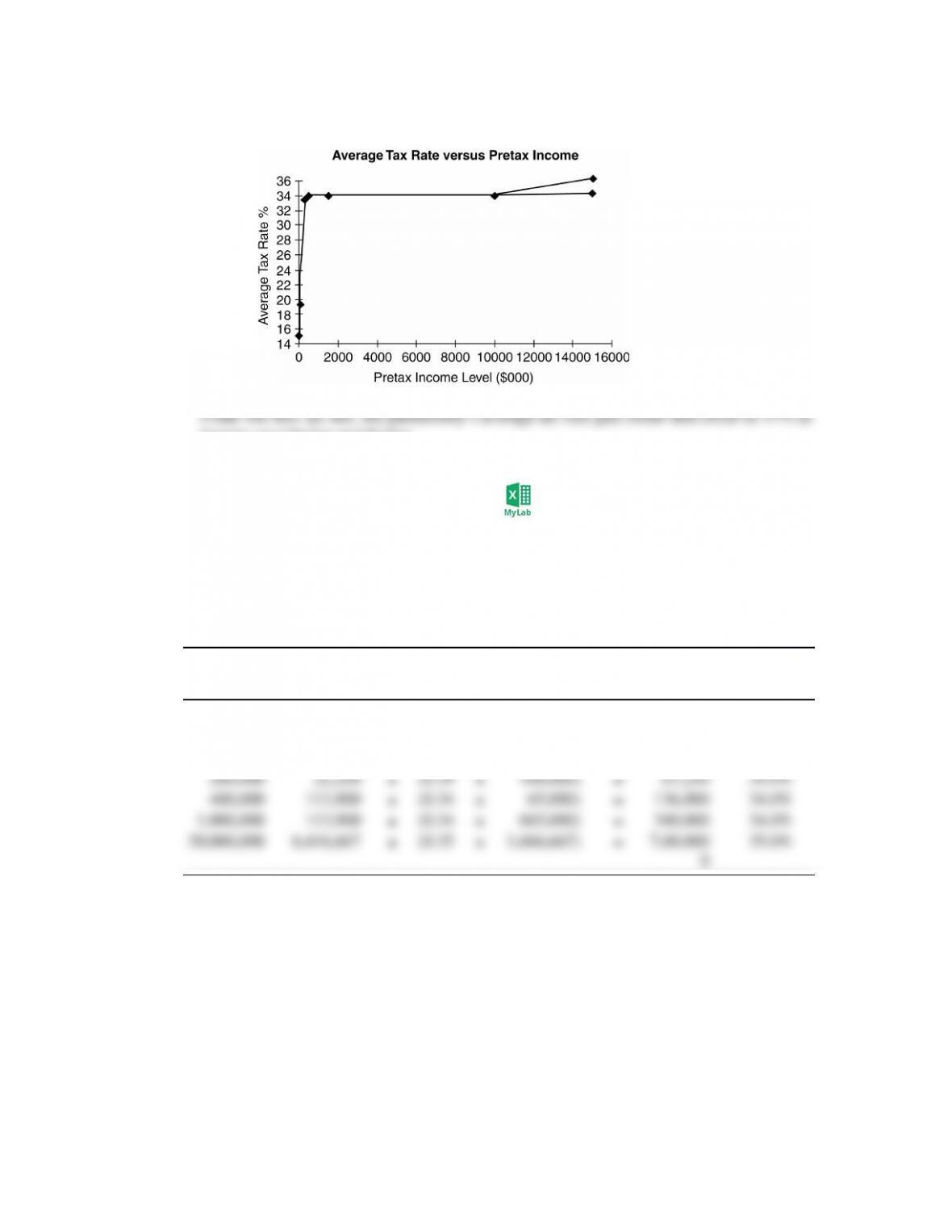

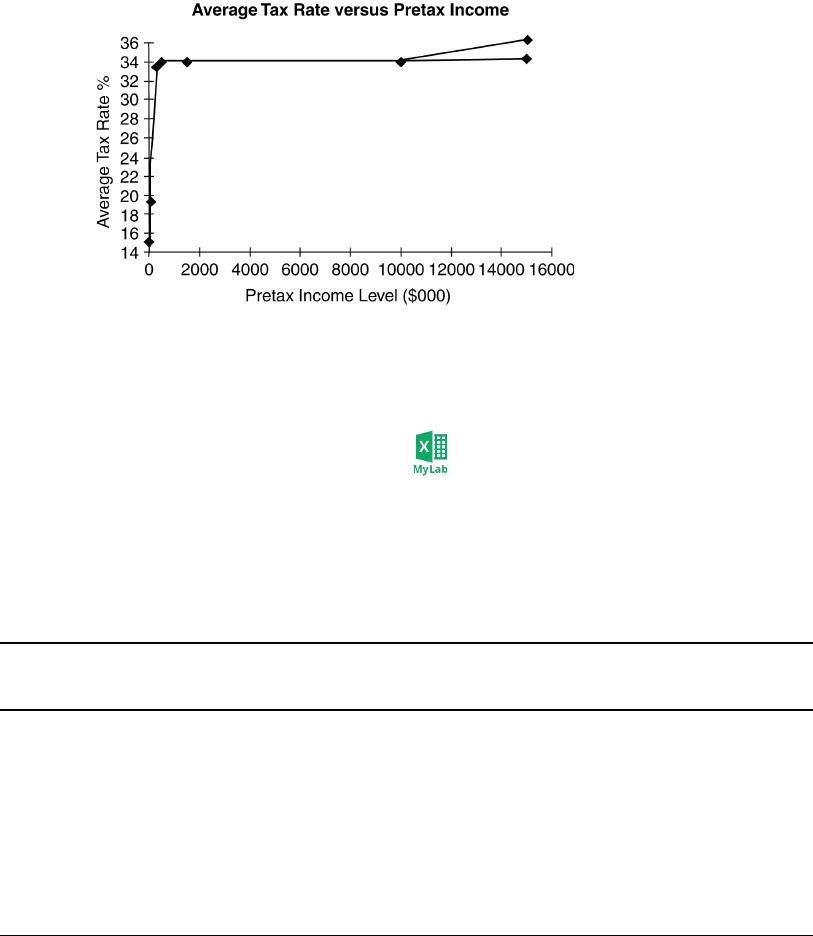

b. The graph below pertains to the version of the text WITHOUT tax updates. As taxable corporate

income rises, the average tax rate approaches 35%.

income goes higher and higher.

P1-8 Marginal corporate tax rates (LG 6; Basic)

As was true in the previous problem, there are different solutions depending on whether a student

has a book with updated tax information or a book with the old tax information. Following is the

solution for the original version of the problem.

a.

Pre-Tax

Income Base Tax %

Amount

Over Base

Total

Tax Marginal

Rate

$15,000 $ 0 (0.15 15,000) $ 2,250 15.0%

60,000 7,500 (0.25 10,000) 10,000 25.0%

90,000 13,750 (0.34 15,000) 18,850 34.0%

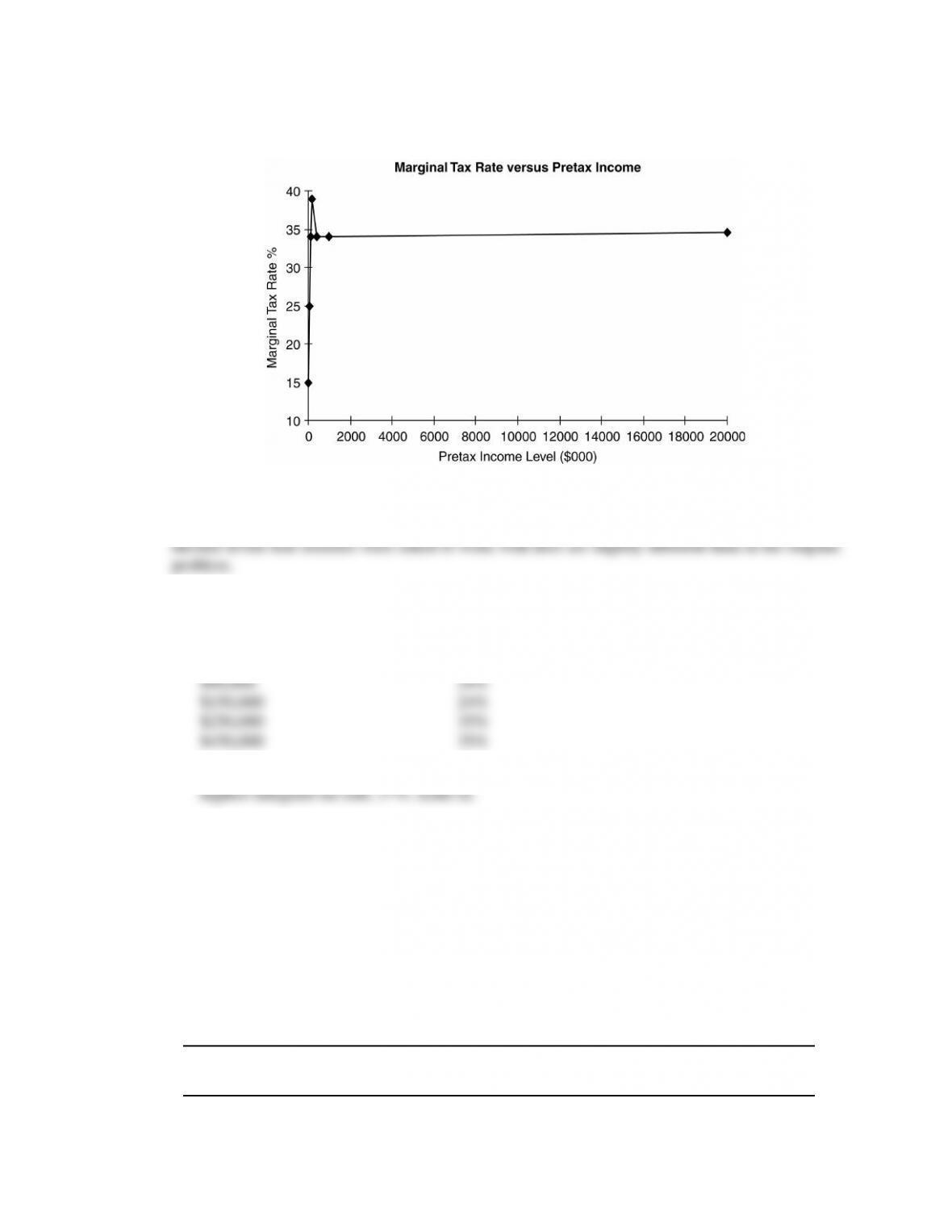

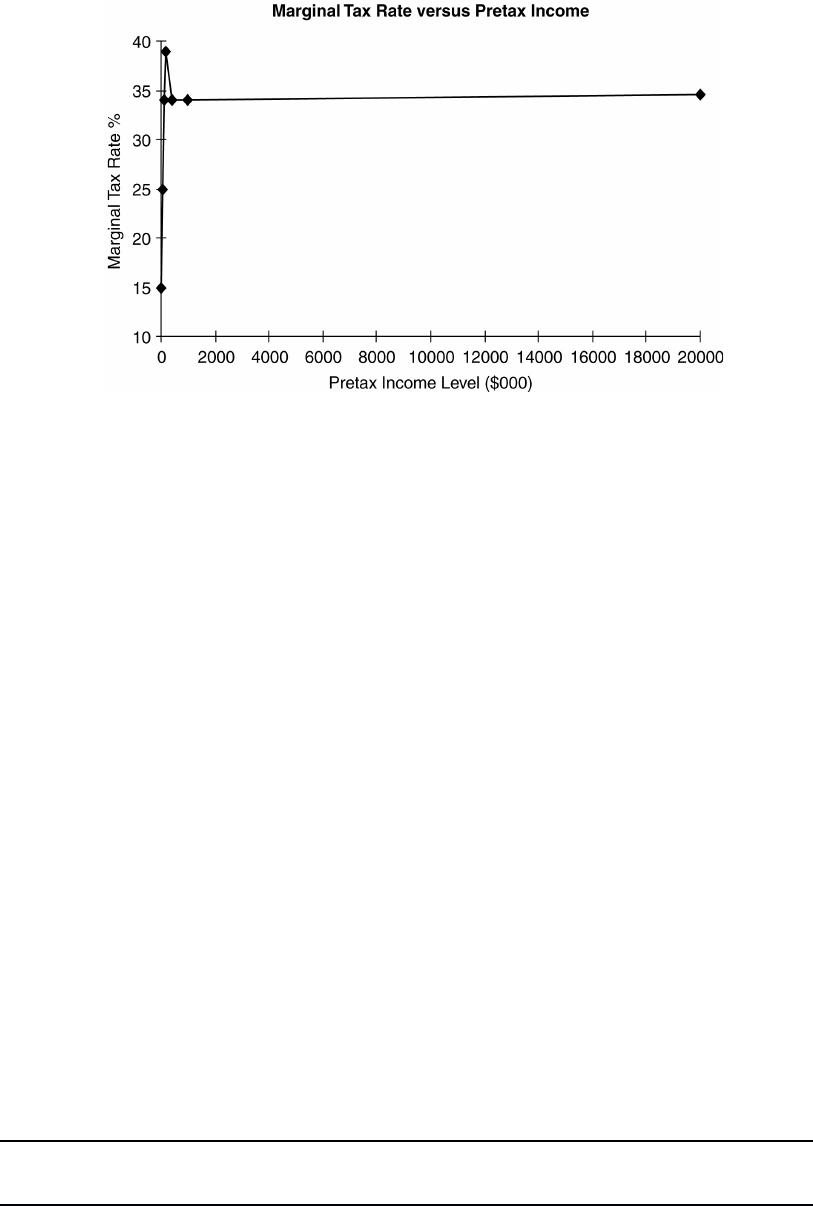

b. As income rises to $335,000, the marginal tax rate approaches a peak of 39%. For income

above $335,000, the marginal rate first dips to 34%, and then edges up to 35% after $10

million.

.

Here is a solution for the new version of the problem to reflect the updated tax code. Note that the

problem was revised to focus on proprietorship income rather than corporate income, and the

a. The marginal tax rates at the specified income levels are

Income Marginal rate

$15,000 12%

$60,000 22%

b. The marginal tax rate rises with income. The chart does not show the income level at which the

P1-9 Interest vs. dividend income (LG 6; Intermediate)

The initial set of answers below pertains to the version of the text without updated tax information.

Answers for the new version appear later.

a. Tax on operating earnings: $490,000 0.40 tax rate $196,000

b., c.

(b)

Interest Income (c)

Dividend Income

Before-tax amount $20,000 $20,000

d. After-tax dividends ($17,600) exceed after-tax interest ($12,000) because of the 70% dividend

attractive relative to purchases of corporate bonds.

e. Total tax liability:

Taxes on operating earnings (from a.) $196,000

Taxes on interest income (from b.) 8,000

book

a. The firm faces a 21% flat tax on operating earnings, so 21% × $490,000 = $102,900.

b., c.

(b)

Interest Income (c)

Dividend Income

Before-tax amount $20,000 $20,000

Less: Applicable exclusion 0 10,000 (0.50 $20,000)

d. The after-tax amount of interest was less than the after-tax dividends received because half the

P1-10 Interest vs. dividend expense (LG 6; Intermediate)

The answer below is appropriate for the original printing of the text with old tax information.

Answers for the printing with updated tax information follow.

a

.EBIT $50,000

Less: Interest expense 12,000

*This is also earnings available to common stockholders.

b. EBIT $50,000

Less: Taxes (35%) 17,500

Here are solutions for the printing that reflected the new tax law.

a. EBIT $50,000

Less interest 12,000

After-tax earnings $39,500

Less preferred div 12,000

P1-11. Reducing tax exposure—Hemingway Corporation (LG 5; Intermediate)

a. With pre-tax income currently of $200,000, Hemingway’s current tax liability (using the tax

rates in Table 1.2) is $22,250 + 0.39 ($200,000 – $100,000) = $22,250 + $39,000 = $61,250.

b. The current average tax rate equals taxes paid divided by taxable income—that is, $61,250 /

average tax rate and the marginal tax rate are the same, 21%.

c. If expansion is financed with cash reserves, then taxable income will be $350,000 with a

corresponding tax liability of $22,250 + 0.39 ($350,000 – $100,000) = $119,750. The average

d. If expansion is financed with debt financing, taxable income will be $350,000 – $70,000 =

$280,000. Taxes owed will equal $22,250 + 0.39 (280,000 – $100,000) = $92,450. The new

average tax rate will be $92,450 / $280,000 = 0.330 or 33.0%. The average tax rate is higher than in

part b, again because added income from expansion is taxed at the marginal rate of 39%. However,

e. Student answers might vary here. Under the old tax law, using debt lowers the average tax rate.

Under the new law that average tax rate is always 21%. Students might say (regardless of the tax

law), that income is lower when the company uses debt. That’s true, but again regardless of the

P1-12. Ethics problem (LG 2)

Maximizing shareholder wealth subject to “ethical constraints” means pursuing all opportunities to

boost stock price consistent with community ethical norms and applicable federal/state laws.

“Community ethical norms” refers to prevailing standards about right and wrong. Consistent,

took no action (believing, perhaps, the executive was irreplaceable), the backlash was even worse

when the story inevitably came out. As a result, many high-profile executives were fired to head off

Case

Case studies are available on www.pearson.com/mylab/finance.

Assessing the Goal of Sports Products, Inc.

a.The primary goal of Sports Products, Inc. should be maximizing shareholder wealth, which means

taking all legal and ethical actions to get firm stock price to the highest possible level. Unlike profit

b.Yes, there appears to be an agency problem. In this case, the stockholders (owners) of Sports Products

are the principals, and company management the agents. Stockholders want the highest possible stock

c.Sports Products’ approach to pollution control is ethically questionable and harmful to shareholders. It is

unclear whether polluting the stream was intentional or accidental; what is clear from the state-and-local-

government lawsuits is the firm violated the law. In the near term, litigation and judgment costs will

d.The corporate governance system at Sports Products appears weak. A management-compensation

system focused on profits, rather than stock price, indicates shareholder welfare is not a firm priority.

lower profits).

e.Recommendations to Sports Products could include:

Overhauling management compensation to strengthen incentives to focus on shareholder interests.

Specifically, Sports Products should consider distributing stock options to executives or awarding

Introducing an explicit system of “carrots and stocks” to reward ongoing management/employee

Establishing a corporate ethics policy, to be read and signed by all employees, along with a system

transgressions.

Recruiting new board members to enact policies to change the corporate culture to focus on

shareholder wealth and good corporate citizenship.

Spreadsheet Exercise

Answers to Chapter 1 spreadsheet problem (Monsanto) are available on www.pearson.com/mylab/finance.

Group Exercise

Group exercises are available on www.pearson.com/mylab/finance.

Notes for Adopters

Group exercises offer students an opportunity to apply chapter topics in a real-world setting using one

fictional and one actual company. Apart from reinforcing learning goals, this approach gives students

The first practical issue is assembling groups—should the instructor assign students to groups or let

students form their own? This project is semester-long, so group members must work well together for

The next issue is determining group size and leaders. Exercises generate workloads suitable for three or

more students. Larger groups reduce individual workloads but facilitate “slacking.” Apart from missing a

One final note—exercises were designed to give students the freedom to work largely independent of the

instructor. Accordingly, instructions for each assignment are self-explanatory.

Chapter 1

This first chapter asks students to name and describe their fictional firm. They must then justify the decision

The instructor should stress the importance of laboring over initial decisions because later work builds on

them. For example, the choice of shadow firm should be weighed carefully because students will apply real-