Chapter 9

The Cost of Capital

NOTE TO INSTRUCTORS: Shortly after the first press run for the 15th edition, Congress passed the Tax Cuts

and Jobs Act of 2017, which included changes in the corporate tax rate relevant to this chapter. In subsequent

printing runs, the text was updated to reflect the new tax law, but these updates may not appear in every student’s

9-1 The cost of capital represents the firm’s cost of long-term financing (in percentage terms). Managers

use the cost of capital (i) as a discount rate in NPV calculations when evaluating projects, (ii) as a

9-2 The cost of capital provides a benchmark for evaluating expected rates of return on potential projects.

9-3 Capital structure is the mix of debt and equity the firm employs. It represents the cumulative long-term

© 2019 Pearson Education, Inc.

9-11 CAPM uses beta” to explicitly incorporate the firm’s non-diversifiable risk in the required rate of

9-13 The weighted average cost of capital (WACC), rwacc, is the firm’s average cost of long-term finance. It

9-14 Target capital structure is the mix of debt and equity financing a firm desires over the long run. Actual

9-15 Sometimes—as with Netflix from 2012 to 2016—the market value of common equity rises rapidly, not

because the firm is issuing common stock but because the price of common stock is soaring. The run-

up is stock price can be so dramatic that it is difficult for the firm to sell bonds fast enough to maintain

the target mix of debt and equity. In such cases, the weights assigned by the firm when calculating

weighted average cost of capital, rwacc, should reflect the firm’s target capital structure rather than its

actual capital structure. The choice of weights is important because investments have long lives, and

the cost of capital used to evaluate those investments should reflect the capital structure that the firm

plans to adopt over the long term. Using actual rather than target weights during a run-up in stock price

leads to a higher cost of capital and, possibly, rejection of attractive investment projects. [Note: This

argument works in reverse should the market value of the firm’s common equity fall rapidly.]

Suggested Answer to Focus on Ethics Box:

“The Cost of Capital Also Rises”

Many feel only muscular government regulation––supported by severe punishment for transgressions––can

deter corporations from unethical acts. How did markets punish Wells Fargo? In your opinion, how much of

a role should markets play in policing corporate ethics?

© 2019 Pearson Education, Inc.

E9-1 Cost of Long-Term Debt

E9-2 Cost of preferred stock

E9-3 Cost of common stock equity

where 8.33% is the return shareholders expect on dividends, and 3% is the return expected from

capital gains.

E9-4 Weighted average cost of capital

© 2019 Pearson Education, Inc.

E9-5 Weighted average cost of capital

P9-1 Concept of cost of capital (LG 1; Basic)

a. Project North is expected to earn an 8% return. If the analyst expects the cost of debt to be 7%,

she will recommend accepting the project because the expected return exceeds financing cost.

b. Project South is expected to earn 15%, but financing (retained earnings) costs 16%. So, the

P9-2 Cost of debt using both methods (LG 3; Intermediate)

1–15

−

70 Coupon Payments (Before Tax)

15

−

1,000 Principal

c. Before-tax cost of debt:

186 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

P9-5 The cost of debt (LG 3; Intermediate)

In Excel, the RATE command will generate the before-tax interest rate (rd) with the following syntax:

=rate(years, coupon in dollars, -net proceeds, par value). For bond sales, net proceeds = Par value +

Premium (Discount) – Flotation costs. For Alternative A, net proceeds = $1,000 + $250 – $30 =

P9-6 After-tax cost of debt (LG 3; Intermediate)

a. The after-tax cost of borrowing from the motorcycle dealer is the same as the pretax cost, 5%.

P9-7 Cost of preferred stock (LG 4; Basic)

The cost of preferred stock is given by rp = Dp ÷ Np, where Dp is annual preferred dividends (in

P9-8 Cost of preferred stock (LG 4; Basic)

The cost of preferred stock is given by rp = Dp ÷ Np, where Dp is annual preferred dividends (in

dollars) and Np is net proceeds from issuing preferred stock.

190 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

© 2019 Pearson Education, Inc.

b. Weighted average cost of capital (rWACC) with target market weights:

Column →1 2 3 = 1 x 2

Type of Capita

l

Weight Cost Weighted Cos

t

Long-term debt 0.30 4.20% 1.26%

Preferred stock 0.15 9.50% 1.43%

Common equity* 0.55 13.00% 7.15%

1.00 Sum (r

WACC

) = 9.84%

*The firm has plenty of retained earnings available to finance new projects, so the cost of

P9-16 Cost of capital (LG 3, LG 4, LG 5, and LG 6; Challenge)

a. Cost of retained earnings: The price of Edna stock (P0) is $40. Expected dividend growth (g) is

6%, and the last dividend was $1.26, so the next dividend (D1) will be $1.26 × 1.06 = $1.34. No

flotation or underpricing costs are incurred when using retained earnings, so the cost of common

equity is the required return on stock, rs = (D1 ÷ P0) + g = ($1.34 ÷ $40) + 0.06 = 9.35%.

5.98% × (1 – 0.40) = 3.59%; with a 21% tax rate, the after-tax cost is 4.72%.

Chapter 9 The Cost of Capital 191

e. If retained earnings supply the needed equity, and the tax rate is 40%, the weighted average cost

of capital (rWACC) is:

Column →1 2 3 = 1 x 2

P9-17 Calculation of individual costs and WACC (LG 3, LG 4, LG 5, and LG 6; Challenge)

a. Cost of debt: Net proceeds from the bond sale = Par value + Premium – Flotation costs. Flotation

costs are 3% × $1,000 = $30. So net proceeds = $1,000 + $20 – $30 = $990. The before-tax cost

of debt is the interest rate that makes the following equation hold:

Bn =

rate, the after-tax cost of debt is 0.0714 × (1 – 0.40) = 0.0429 = 4.29%. With a 21% tax rate, the

after-tax cost of debt is 0.0714 × (1 – 0.21) = 5.64%.

b. Cost of preferred stock: The cost of new preferred stock (rp) is given by (Dp ÷ Np), where Dp is

the expected perpetual annual dividend on preferred stock, and Np is net proceeds from the sale of

new preferred stock. Np = Sales price of new preferred stock – Flotation costs = $98 – $2 = $96.

Cost of new common stock: The cost of new common stock (rn) is given by (D1 ÷ Nn) – g, where

Nn is the net proceeds from the sale of new stock. Flotation costs are $2 per share. Net proceeds =

Price of common stock (net of underpricing) – Flotation costs = ($59.43 – $1.50 – $2) = $55.93,

so the cost of new common stock is ($4.16 ÷ $55.93) + 0.0401 = 0.07438 + 0.0401 = 11.45%.

d. If retained earnings can be tapped for needed common equity, and the tax rate is 40%, rWACC is:

g

g

g

k

r

Type of Capital Weight Cost Weighted Cost

Lon

g

-term debt 0.400 4.29% 1.714%

Preferred stoc

k

0.100 8.33% 0.833%

Common stoc

k

0.500 11.45% 5.724%

Sum (

r

WACC

) = 8.27%

P9-18 Personal finance problem: Weighted-average cost of capital (LG 6; Intermediate)

194 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

P9-20 Weighted-average cost of capital (LG 6; Intermediate)

a. The weighted average cost of capital, rWACC = [wd × rd × (1 – T)] + [wp × rp]+ [ws× rs], where

wd, wp, and ws are the weights for debt, preferred stock, and common stock respectively, and

rd × (1 – T), rp, and rs are the after-tax costs of debt, preferred stock, and common stock

P9-21 Ethics problem (LG 1; Intermediate)

GE’s long string of good earnings reports made the company seem less risky, thereby reducing

7.51%. For bond sales exceeding $450,000, before-tax cost is given as 13.0% for a 40% rate, implying

the after-tax cost is 0.13 × (1 – 0.40) = 7.80%. With a 21% tax rate, after-tax cost is 10.27%.

Chapter 9 The Cost of Capital 195

Cost of preferred stock: rp = Dp ÷ Np, where Dp is the constant preferred dividend and Np is the net

1.

L

ong-term debt ≤ $450,000 and common equity less ≤ $1,500,000:

2.

L

ong-term debt > $450,000 and common equity ≤ $1,500,000:

1.00 rWACC = 15.25%

3.

L

ong-term debt > $450,000 and common equity > $1,500,000:

1.00 rWACC = 16.85%

With a 21% tax rate, rWACC for case 1 is 15.16%, case 2 is 15.99%, and case 3 is 17.59%.

(2) To find the retained-earnings threshold where rWACC rises, recognize 60 cents of every dollar raised

(3) There is no need to look at the case where Star borrows less than $450,000 and uses more than $1.5

million in retained earnings because cheap debt is exhausted at the $1.5 million level of total

funding but cheap equity (retained earnings) is not exhausted until the $2.5 million level.

196 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

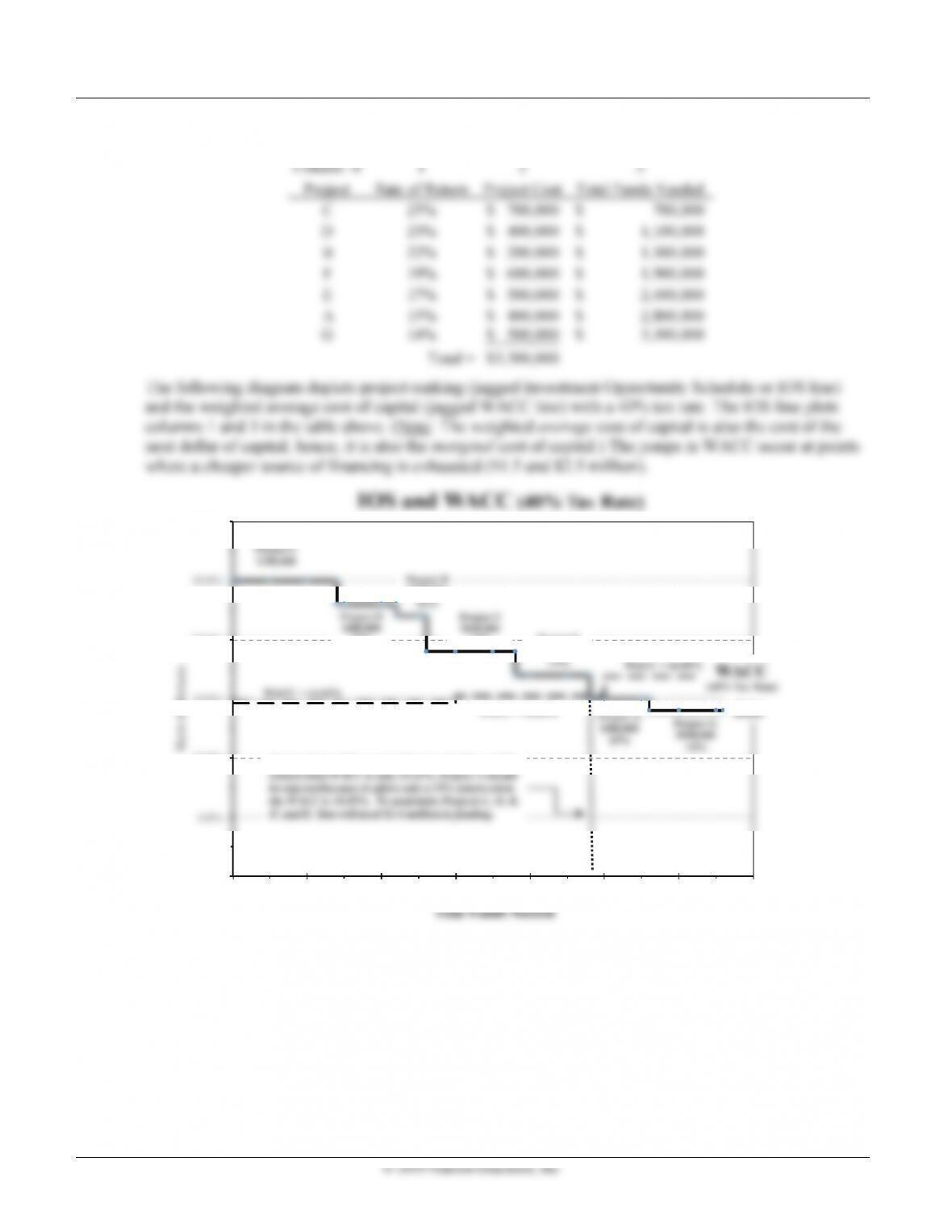

d. Ranking investment projects from highest to lowest rate of return:

0.0%

10.0%

15.0%

20.0%

30.0%

$0 $500,000 $1,000,000 $1,500,000 $2,000,000 $2,500,000 $3,000,000 $3,500,000

Rate of Return

Total Funds Needed

IOS and WACC

(40% Tax Rate)

IOS

Project C

$700,000

23%

$200,000

19% Project E

$500,000

Project A

$400,000

15%

Project G

$500,000

14%

WACC = 15.25%

Project E should be accepted because it offers a 17%

© 2019 Pearson Education, Inc.

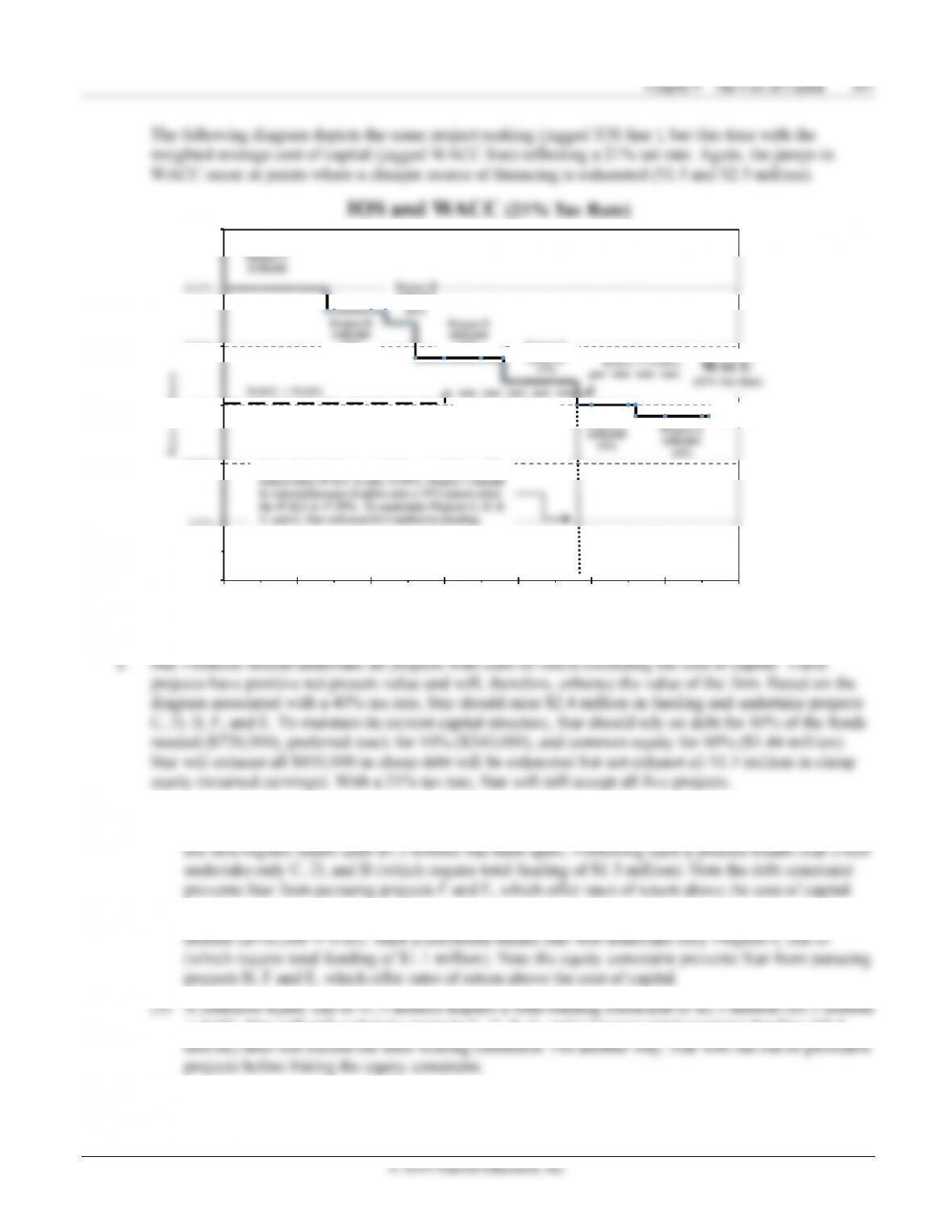

0.0%

10.0%

15.0%

20.0%

30.0%

$0 $500,000 $1,000,000 $1,500,000 $2,000,000 $2,500,000 $3,000,000 $3,500,000

Total Funds Needed

IOS

23%

19% Project E

$500,000

Project A

$400,000

15%

Project G

$500,000

(21% Tax Rate)

WACC = 15.16%

WACC = 15.99%

Project E should be accepted because it offers a 17%

(1) If Star can sell only $450,000 in debt, its total funding constraint is $1.5 million ($450,000.÷ 0.30).

Given this constraint, the firm will accept projects starting with the highest return (C) and moving to

(2) If Star can use no more than $750,000 in common equity, its total funding constraint is $1.25

÷ 0.60). Star will still undertake projects C, D, B, F, and E because total requiring funding ($2.4