Chapter 7

Stock Valuation

Instructor’s Resources

Chapter Overview

This chapter focuses on equity—distinctions between equity and debt, different forms of equity, and

approaches to valuing equity instruments. The basic model for valuing equity is presented as an example of

the asset-valuation framework introduced in Chapter 5 and applied to bonds in Chapter 6. Specifically, the

value of a share or common of preferred stock is the present value of expected future cash flows from that

share, where the cash flows here are dividends. When capital markets are efficient, stock price should equal

the present value of expected dividends, and news about changes in risk or expected cash flows will be priced

immediately. The discussion then expands the common-stock valuation framework to accommodate different

assumptions about expected dividend growth. Other approaches to equity-valuation—ranging from variations

on dividend-discounting like the free-cash-flow model to models based on market benchmarks like

price/earnings multiples—are also compared and contrasted with the expected-dividend model. The chapter

ends with discussion of interrelationships among financial decisions, expected return, risk, and firm value.

Answers to Review Questions

7-1 Equity capital is permanent capital representing ownership, while debt capital is a loan that must be

repaid. Holders of equity capital receive a claim on firm income and assets subordinate to creditor

claims—that is, debt holders must receive all interest and principal owed prior to distributions of firm

7-2 A corporation’s owners are the common stockholders. As residual claimants, these stockholders are

not guaranteed a return, only what is left after other claims on firm income and assets have been

7-3 Rights offerings are financial instruments that allow existing stockholders to purchase additional shares

7-4 Authorized shares are the maximum number of shares a firm can sell without approval from existing

shareholders; this limit is stated in the corporate charter. Authorized shares sold to and held by the

7-5 Issuing stock outside their domestic markets can benefit corporations by broadening the investor base

and facilitating integration into the local economy. Specifically, a local stock listing increases

130 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

© 2015 Pearson Education, Inc.

community press coverage, thereby raising awareness about the firm. Locally traded stock also

facilitates acquisitions. American depository shares (ADSs) are dollar-denominated receipts for stocks

of foreign companies held by U.S. financial institutions overseas. American depository receipts (ADRs)

are securities that permit U.S. investors to hold shares of non-U.S. companies and trade them in U.S.

markets. ADRs are issued in dollars and subject to U.S. securities laws; they offer U.S. investors an

opportunity to diversify internationally.

7-6 Preferred stockholders have a fixed claim on firm income and assets behind creditors but ahead of

common stockholders.

7-7 Cumulative preferred stock gives the holder the right to receive any dividends in arrears prior to

dividend payment to common stockholders. A call feature allows the issuer to retire outstanding

7-8. The efficient market hypothesis (EMH) says, in equilibrium, the price of a stock or other security is an

unbiased estimate of its true value. Thus, in equilibrium, security prices are neither overvalued nor

undervalued. For a concrete example of what this means, suppose investors learn new information

7-9 According to the efficient market hypothesis (EMH):

a. Securities prices are in equilibrium (fairly priced with expected returns equal to required returns);

b. Securities prices reflect all public information and react quickly to new information; so

7-10 a. The zero growth model of common-stock valuation assumes constant dividends through time, so .

stock is valued as a perpetuity with today’s value (price), P0, depending on the perpetual dividend,

D1 and required return r as follows:

1

∞

© 2019 Pearson Education, Inc.

7-11 The free-cash-flow valuation model discounts future free cash flows rather than expected dividends.

Because this discounted value represents total firm value, the market value of total debt and preferred

7-12 Book value per share is the hypothetical amount common shareholders would receive if firm assets

were sold at book (accounting) value, liabilities (including preferred stock) were paid off at book value,

and the remainder divided by shares of common stock outstanding. Liquidation value is the amount

7-13 A useful way to think about the impact of financial decisions on the firm is with the constant-growth

stock-valuation model: P0 = D1 ÷ (r – g). Actions of financial managers affect stock price (and hence

7-14 A useful way to analyze the impact of events on stock price is to start with the constant-growth stock-

valuation model and assign hypothetical initial values. Accordingly, let the next expected dividend (D1)

be $5, expected rate of dividend growth (g) be 3%, and required rate of return (r)be 8%:

P0 = D1 ÷ (r – g) = $5 ÷ (0.08 – 0.03) = $100

a. Now, required return (r) = risk-free rate (RF) + risk premium (RP). So, an increase in RP means an

increase in r. Suppose r rises from 8% to 9%, but expected dividends (D1 and g) do not change:

$5 ÷ (0.09 – 0.03) = $83.33. In words, stock price will fall from $100 to $83.33.

b. Suppose r falls from 8% to 7%, but nothing else changes: $5 ÷ (0.07 – 0.03) = $125.00. Stock

price will rise from $100 to $125.

© 2015 Pearson Education, Inc.

Suggested Answer to Focus on Practice Box:

“Understanding Human Behavior Helps Understand Investor Behavior”

Theories of behavioral finance can apply to other areas of human behavior in addition to investing. Think of a

situation in which you may have demonstrated one of these behaviors. Share with a classmate.

Student answers will vary. Examples for discussion: (i) regret theory may hold true for social situations in

which a person makes a mistake and subsequently focuses on avoiding embarrassment at all costs; (ii) fear of

regret can sometimes be rationalized away with “everyone else is doing it” (herding theory), thereby

explaining why some people do silly things at parties; and (iii) students may react to grades as investors react

to news, placing more importance on recent events without recognizing the overall trend (anchoring).

Answers to Warm-Up Exercises

E7-1 Using debt ratio to calculate a firm’s total liabilities (LG 1)

E7-2 Determining net proceeds from the sale of stock (LG 2)

E7-3 Preferred and common stock dividends (LG 2)

E7-4 Price-earnings ratios (LG 3)

E7-5 Valuing stock with zero dividend growth (LG 4)

E7-6 Valuing stock with zero dividend growth (LG 6)

© 2019 Pearson Education, Inc.

P7-1 Authorized and available shares (LG 2; Basic)

a. Maximum shares = Authorized shares – Shares outstanding = 2,000,000 – 1,400,000 = 600,000.

P7-2 Preferred dividends (LG 2; Intermediate)

a. Annual dividend in dollars = Price of preferred stock × annual dividend rate

P7-3 Preferred dividends (LG 2; Intermediate)

Case Answer Explanation

Three quarters of passed dividends plus current quarter (4 quarters × $4 per

E $2.10

passed, so only current $2.10 dividend is due.

P7-4 Convertible preferred stock (LG 2; Challenge)

a. Conversion value or preferred stock = Conversion ratio × Common stock price = 5 × $20 = $100.

b. The investor should covert because value would be $100 while preferred stock price is only $96.

c. This question is trickier than it first appears. Students might note conversion of one share of

© 2019 Pearson Education, Inc.

$250.00. Present value of stock price at end of year 3 is $250.00 ÷ (1.11)3 = $182.80. For step 3,

P0 = $5.11 + $182.80 = $187.91.

P7-16 Personal finance: Common stock value—Free cash flow models (LG 4; Challenge)

a. Firm has no debt or preferred stock, so firm value (Vc) is present value of expected free cash flow

(FCF). If current FCF is not expected to change (FCF0 = FCF1), and required return (r) is 18%:

VC = FCF1 ÷ r = $42,500 ÷ 0.18 = $236,111

b. Free cash flow next year, FCF1 = $42,500 × 1.07 = $45,475. Now, because FCF is expected to

P7-17 Free cash flow (FCF) valuation (LG 5; Challenge)

a. Assumes 2020 is one year in the future. Firm value (VC) may be found in three steps:

Step 1: Present value of FCF from 2025 to infinity: FCF2025 = $390,000 × (1.03) = $401,700,

and present value of FCF2025 to infinity in 2024= $401,700 ÷ (0.11 − 0.03) = $5,021,250.

© 2015 Pearson Education, Inc.

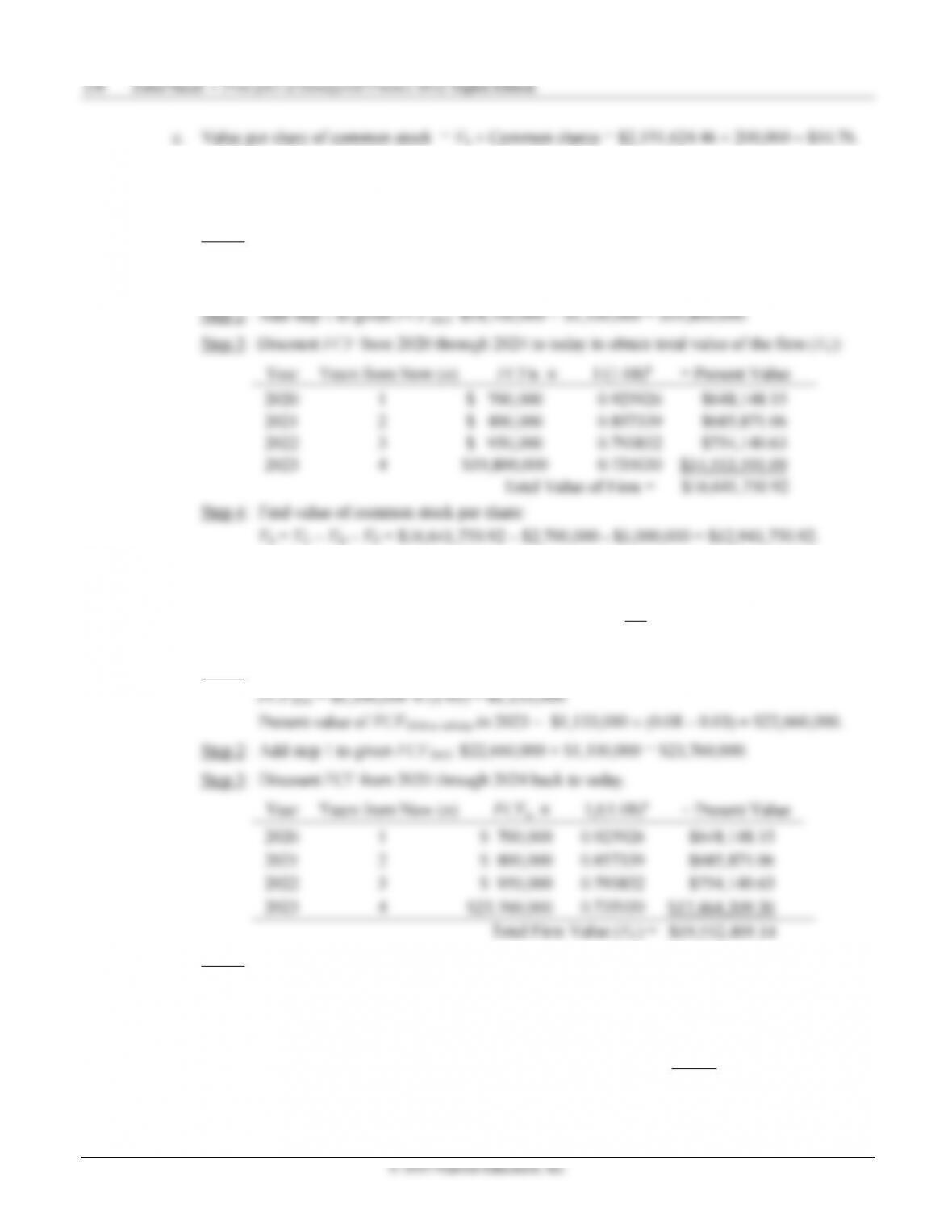

P7-18 Personal finance: Using the free-cash-flow valuation model to price an IPO (LG 5; Challenge)

a. The value of the firm’s common stock may be found in four steps:

Step 1: Find present value in 2023 of free cash flow (FCF) from 2024 to infinity:

FCF2024 = $1,100,000 × (1.02) = $1,122,000.

Present value of FCF2024 to infinity in 2023= $1,100,000 ÷ (0.08 − 0.02) = $18,700,000.

Value per share of common stock = Total value of common stock ÷ Common shares

= $12,941,750.92 ÷ 1,100,000 = $11.77.

b. IPO is overvalued by $0.73 ($12.50 − $11.77), so you should not buy the stock.

c. New value of common stock may be found in four steps:

Step 1: Present value in 2023 of FCF from 2024 to infinity:

Step 4: Find value of common stock per share:

VS = VC – VD – VP = $19,552,469.14 − $2,700,000 − $1,000,000 = $15,852,469.14.

Value per share of common stock =VS ÷ Common shares

= $15,852,469.14 ÷ 1,100,000 = $14.41.

The IPO is undervalued by $1.91 ($14.41 − $11.77), so you should buy the stock.

140 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

© 2015 Pearson Education, Inc.

Step 1: Given stock price (P0) of $50, next expected dividend (D1) of $3 per share, and expected

dividend growth (g) of 6.5%, solve for required return on the stock (r):

P0 = D1 ÷ (r − g)

$50 = $3.00 ÷ (rs − 0.065) → r = 0.125 or 12.5%

Step 2: Given a 12.5% required return (r) and a 4.5% risk free return (RF), solve for risk premium

(RP) on stock:

r = RF + RP

0.125 = 0.045 + RP → RP = 0.08 or 8.0%

P7-23 Integrative: Risk and valuation (LG 4 and LG 6; Challenge)

a. Given a 14.8% required return (r), and a 4% risk-free rate (RF), solve for risk premium (RP) on

Giant Enterprise stock:

r = RF + RP

P7-24 Integrative: Risk and valuation (LG 4 and LG 6; Challenge)

a. The maximum price to pay for Craft stock may be found in three steps:

of 7.02%, and required return (r) of 14%, solve for the maximum price (value) of Craft

stock: P0 = D2020 ÷ (r – g) = $3.68 ÷ (0.14 − 0.0702) = $52.72 per share.

b. Part (1): The new value of Craft stock with lower dividend growth may be found in two steps:

Step 1: Find new expected dividend for 2020 with expected growth rate two percentage

© 2015 Pearson Education, Inc.

$37.34). Additional dividends do not compensate for the impact on of additional risk on required return.