118 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

b. and c.

Five years ago, the yield curve was slightly upward sloping, suggesting (under the expectations

theory) investors expected future short-term interest rates to be only slightly higher than current

short-term rates. Two years ago, the yield curve had a sharp downward slope, suggesting investors

expected a dramatic decline in short-term interest rates (perhaps due to a coming recession). Today,

the yield curve is upward sloping, suggesting investors expect short-term rates to rise.

d. Consider two 10-year investment options five years ago: (i) a 10-year bond offering 9.5% or (ii) a 5-

year bond offering 9.3% and another 5-year bond in 5 years. Under the expectations theory of the

term structure, the options should offer the same return. Assuming the options offered the same

P6-8 Term structure (LG 1; Basic)

Consider two 2-year investment options: (i) a 2-year bond offering 5.5% or (ii) a 1-year bond offering

5% and another 1-year bond in 1 year. Under the expectations theory of the term structure, the options

P6-9 Risk premiums (LG 1; Intermediate)

a. The coupon rate (3.3%) on the Anheuser-Busch (AB) bond exceeds yield to maturity (2.82%, also

the current market interest rate on bonds of equivalent risk), so the AB bond sells at a premium. The

coupon rate on the Santander Holdings (SH) bond (3.571%) also exceeds yield to maturity (3.341%),

P6-10 Bond interest payments before and after taxes (LG 2; Intermediate)

a. Yearly interest = [($2,500,000 ÷ 2,500) × 0.07] = ($1,000 × 0.07) = $70.00

© 2019 Pearson Education, Inc.

P6-11 Bond prices and yields (LG 4; Basic)

a. 0.97708 × $1,000 = $977.08

b. (0.057 × $1,000) ÷$977.08 = $57.00

÷

$977.08 = 0.0583 = 5.83%

P6-12 Personal finance: Valuation fundamentals (LG 4; Basic)

a. In years 1 – 4, $6,000 is paid on property taxes and maintenance, but $10,000 is saved on rent. Also,

in year 4, the condo will sell for $125,000. So, the timeline is:

01234

Year

Chapt

e

e

r 6 Interest R

a

a

tes and Bond

V

V

aluation 12

1

1

1

22 Zutter/

S

P6-18

B

a

b

b

c

c

c

c

n

a

b

n

v

p

r

a

o

P

a

1

1

1

1

1

1

P

a

1

1

1

1

1

1

a

0

0

0

0

0

o

0

S

mart • Princip

l

B

ond value a

a

. Using th

e

R

e

t

t

a

n

l

es of Manageri

a

n

d time: Co

n

e

PV function

=p

v

e

quired

Y

a

l Finance

B

rie

f

n

stant requir

e

in Excel wit

h

v

(required re

t

Y

ears to

f

, Eighth Editio

n

e

d returns (L

h

the syntax:

t

urn, years to

n

L

G 5; Interm

maturity, co

u

P

ediate)

u

pon, par val

u

P

arValue

u

e)

Bond

© 2019 Pearson Education, Inc.

P6-20 Yield to maturity (LG 6; Basic)

P6-21 Yield to maturity (LG 6; Intermediate)

a. Yield to maturity (YTM) may be found in Excel using the RATE function with the following syntax:

=rate(n,C,−V0,M) = rate(15,60, −$867.59,1000) = 7.50%

P6-22 Yield to maturity (LG 6; Intermediate)

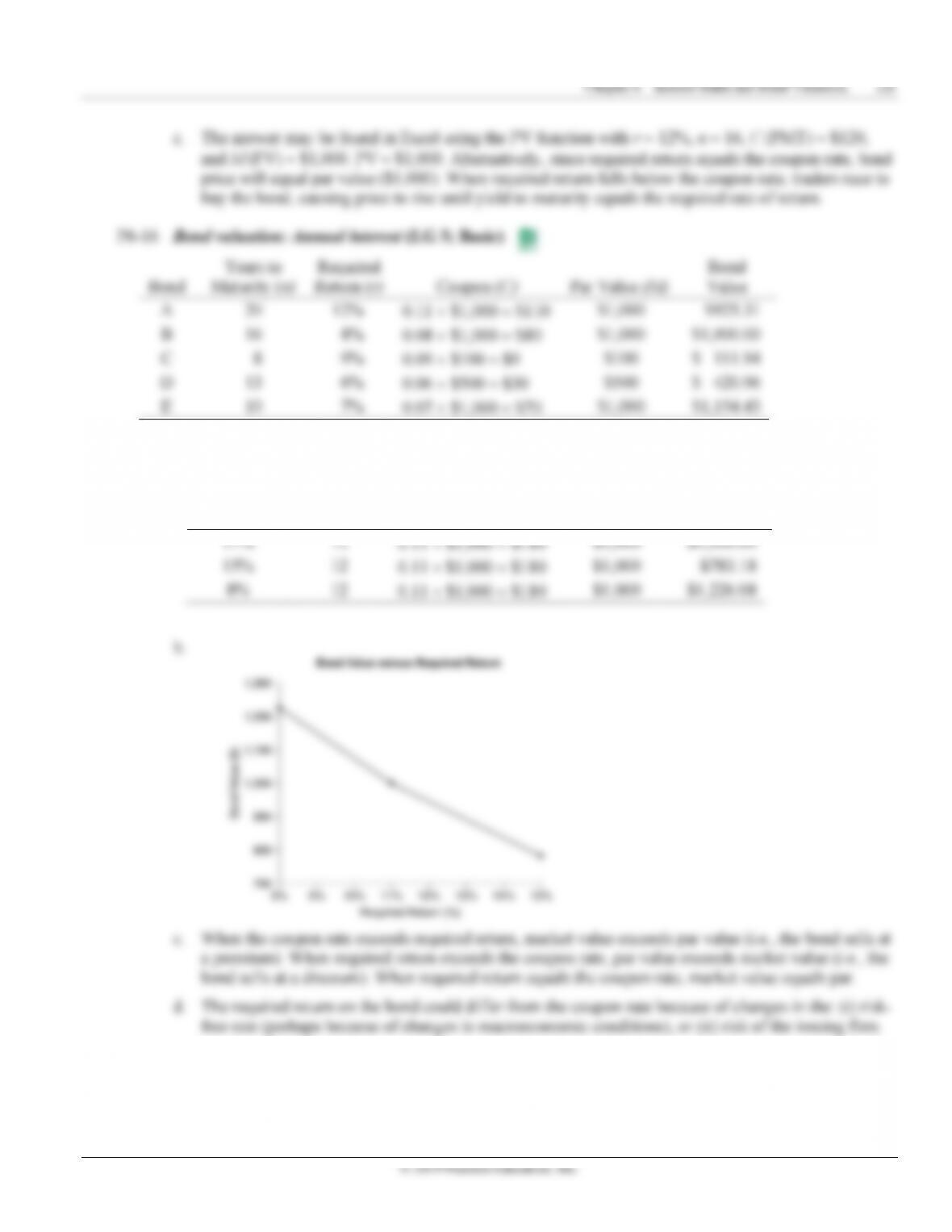

a. In Excel, the RATE function will generate a bond’s yield to maturity (YTM). For example, for bond

A in the table below, the proper syntax is:

=rate(periods, −payment,present value, −future value)

where periods (n) is number of periods to maturity, payment (C) is coupon payment, present value is

© 2019 Pearson Education, Inc. Publishing as Prentice Hall

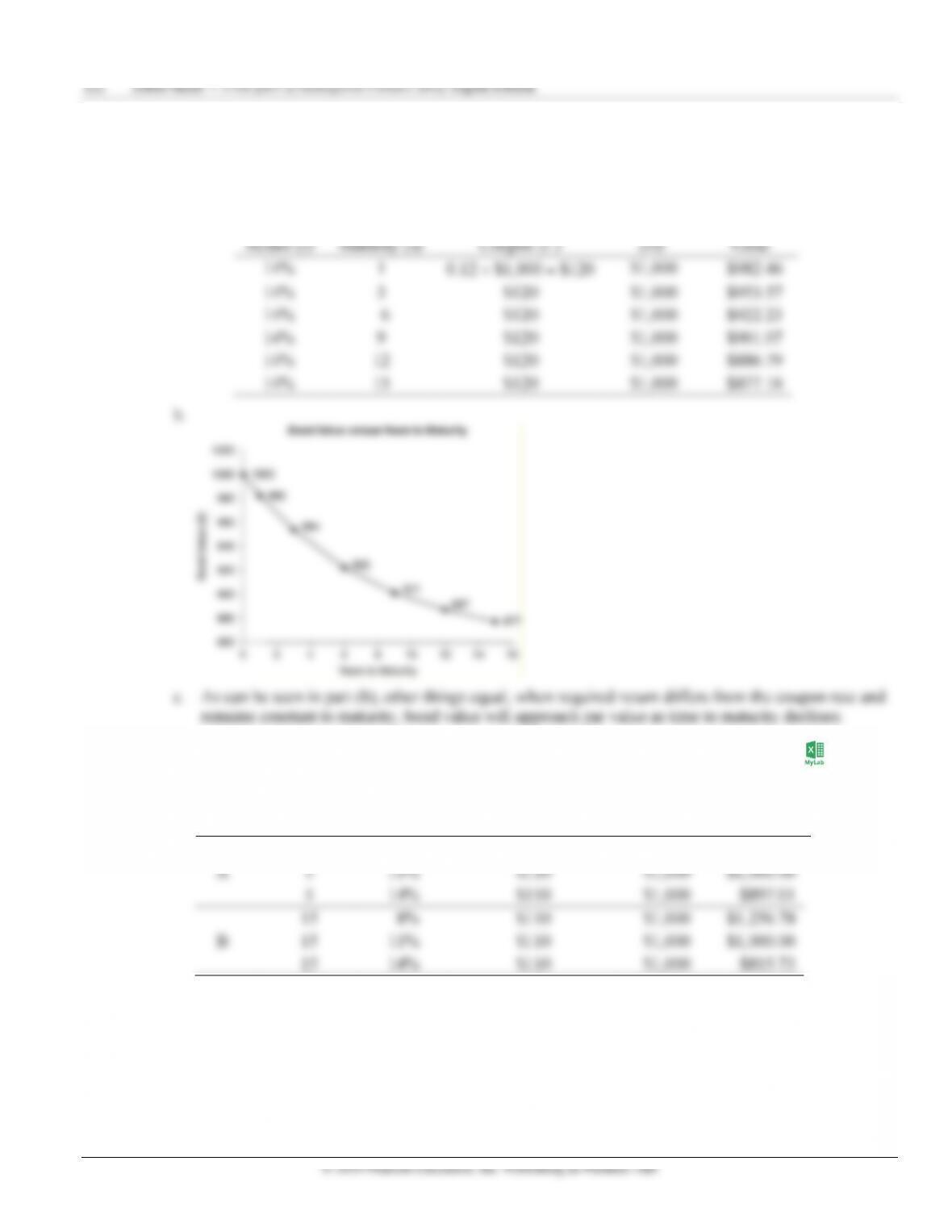

P6-23 Personal finance: Bond valuation and yield to maturity (LG 2, LG 5, and LG 6; Challenge)

a. Value of the Crabbe Waste bond may be found in Excel using the PV function and n = 5,

YTM = r = 7.5%, C = 0.06324 × $1,000 = $63.24, and M = $1,000:

1-5 and $21,000 (21 bonds × $1,000) in principal at the end of year 5. The future value of reinvested

interest may be found using the FV function in Excel with the following syntax:

=fv(r,n,𝐶𝐹) = rate(0.10,5,1328.04) = $8,107.82

where r is the required rate of return, n is years interest will be earned, and CF is total interest earned

126 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

Case: “Evaluating Annie’s Proposed Investment in

Atilier Industries Bonds”

to $901.77 (i.e., with n = 25, r = 9%, C = $80, and M = $1,000, present value = $901.77). This amount is the

maximum Annie should pay for the bond after the increase in expected inflation.

e. If the ratings downgrade raises expected return from 8% to 8.75%, bond price will fall to $924.81 (i.e., with

n = 25, r = 9%, C = $80, and M = $1,000, present value = $924.81). This amount is the maximum Annie

should pay for the bond after the ratings downgrade.

© 2019 Pearson Education, Inc.