Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Part 3

Valuation of Securities

Chapters in This Part

Chapter 6 Interest Rates and Bond Valuation

Chapter 7 Stock Valuation

Chapter 6

Interest Rates and Bond Valuation

Instructor’s Resources

Chapter Overview

This chapter introduces interest-rate and bond-market fundamentals, beginning with the distinction between

nominal and real interest rates and the role of expected inflation in linking the two. Risk premia are added to

highlight components of the nominal return on a risky security, namely the (i) real risk-free rate, (ii) expected

inflation rate, and (iii) risk premium on the security. Next, the discussion turns to the relationship between the

nominal interest rate on a bond and its term to maturity—formally referred to as the term structure of interest

rates and represented pictorially by the yield curve. The exposition notes the general upward slope of the yield

curve—that is, that long-term interest rates tend to exceed short-term rates—and offers three explanations: (a)

expectations about future short-term rates, (ii) general investor preference for short-term, liquid debt, and (iii)

segmentation of short- and long-term debt markets. The focus then moves to bond-market institutions with a

catalogue of the major types of issues along with their legal issues, risk characteristics, and indenture provisions.

The role of rating agencies is also emphasized. The chapter concludes by presenting the basic model for bond

valuation as a special case of the general model for valuing assets (i.e., value is simply the present value of

expected cash flows from the asset). Examples are provided of the impact of variation in coupon/principal

payments, timing of coupon/principal payments, and required rates of return on the market price of a bond. The

final topic is yield to maturity—explained as nothing more than the interest rate equating the present value of a

bond’s remaining coupons and principal payments with its market price.

Answers to Review Questions

6-1 The real rate of interest measures the return on an investment, not in dollars, but in terms of how much the

investment increases one’s purchasing power. The nominal rate of interest is the actual rate of interest

charged by suppliers and paid by demanders of funds; it differs (approximately) from the real rate of

interest by expected inflation. Specifically, let r* be the real rate of interest, r the nominal interest rate, and

6-2 The term structure of interest rates is the relationship between nominal rate of return and time to maturity

1

1

12 Zutter/

S

that is,

a

interest

c

Why do

y

run-up

t

S

mart • Princip

l

a

ward a ratin

g

c

osts down.

y

ou think N

R

t

o the Great

R

l

es of Manageri

a

g

indicating l

o

SROs inflate

d

R

ecession?

a

l Finance

B

rie

f

o

wer default

r

d

ratings for

n

f

, Eighth Editio

n

r

isk than just

i

n

ew complex

n

i

fied by the i

s

MBSs but n

o

s

suer’s finan

c

o

t traditional

c

c

ial informati

o

corporate bo

n

o

n.—to keep

n

ds in the

© 2019 Pearson Education, Inc.

E6-3 Calculating inflation expectation (LG 1)

E6-4 Real returns (LG 1)

© 2019 Pearson Education, Inc.

P6-1 Interest-rate fundamentals: The real rate of return (LG1; Basic)

Real rate of return (r*) ≈ nominal interest rate (r) – expected inflation (i) = 1.5% − 0.5% ≈1.0%

P6-2 Equilibrium rate of interest (LG 1; Intermediate)

a,b and c.

P6-3 Personal finance: Real and nominal rates of interest (LG 1; Intermediate)

a. $100 budget ÷ $2.5 per pair of socks = 40 pair of socks.

b. Nominal return on $100 invested at 9% for one year =$100 × (1.09)1 = $109.

c. Price of a pair of socks in one year with a 5% inflation rate = $2.50 × (1.05)1 = $2.625.

Point O: Initial Equilibrium

Point N: New Equilibrium

1

1

16 Zutter/

S

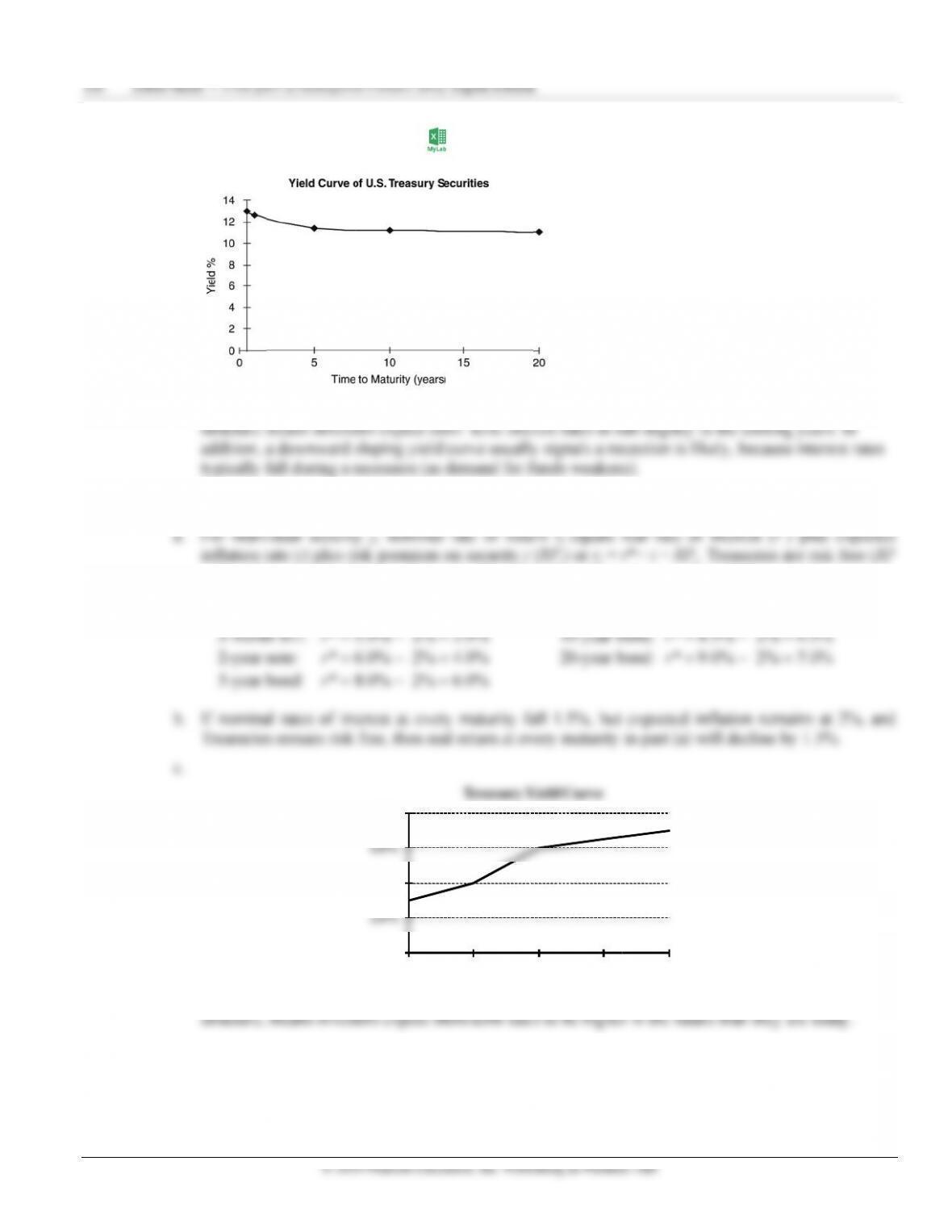

P6-4

Y

a

b

S

mart • Princip

l

Y

ield curve (

L

a

.

b

. The yield

l

es of Manageri

a

L

G 1; Inter

m

curve is slig

h

a

l Finance

B

rie

f

m

ediate)

h

tly downwa

r

f

, Eighth Editio

n

r

d sloping, w

h

n

h

ich under t

h

h

e expectatio

n

n

s theory of t

h

h

e term

Chapt

e

e

r 6 Interest R

a

a

tes and Bond

V

V

aluation 11

7