Chapter 5 Time Value of Money 93

Case

A PV3 = ($12,000 ÷ 0.07) × [1 − (1 + 0.07)-3] × (1 + 0.07) = $33,696.22

E PV5 = ($22,500 ÷ 0.10) × [1 − (1 + 0.10)-5] × (1 + 0.10) = $93,821.97

Present value of an annuity due may be in Excel with the bracketed formula

[=PV(r, n, –CF0,0,1)], where the final “1” inside the parentheses denotes annuity due.

P5-21 Personal finance: Time value—annuities (LG 3; Challenge)

a. The future value of the ordinary annuity is $32,951.99 when the interest rate is 6% and

$39,843.56 when the interest rate is 10%. The future value of the annuity due is

$32,134.78 when the interest rate is 6% and $40,321.68 when the interest rate is 10%.

b. When the interest rate is 6%, the ordinary annuity has a higher future value, but when

P5-22 Personal finance: Retirement planning (LG 3; Challenge)

a. The correct framework is the future value of an ordinary annuity. Specifically, FV with

end-of-year $2,000 contributions, an interest rate of 10% and 40 years to retirement, is

$885,185.11.

© 2019 Pearson Education, Inc.

P5-26 Perpetuities (LG 3; Basic)

Case Equation Present Value

P5-27 Perpetuities (LG 3; Intermediate)

a. The present value of the perpetuity is $100 ÷ 0.07 = $1,428.57. To see this is the correct answer,

suppose you invested $1,428.57 invested in an account right now paying 7% interest. If you

P5-28 Perpetuities (LG 3; Intermediate)

a. Present value is $75 ÷ 1.10 = $68.18.

b. In 100 years, the payment will be $75 × 1.0499 = $3,642.18. The present value of this payment

P5-29 Personal finance: Creating an Endowment (LG 4; Intermediate)

a. Cost next year = $600 × (1.02) = $612.

98 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

b.

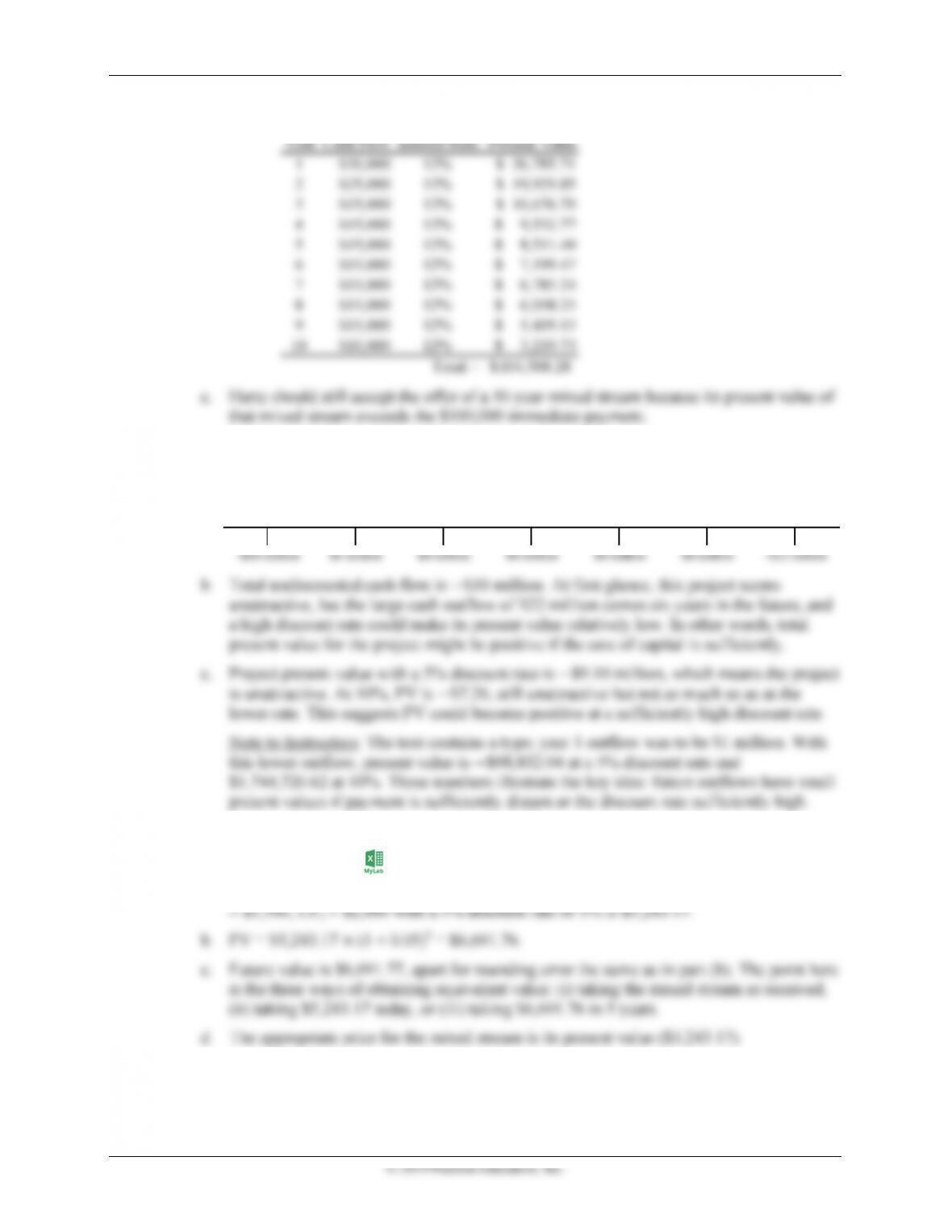

P5-35 Value of a mixed stream (LG 1 and LG 4; Intermediate)

a.

P5-36 Relationship between future value and present value-mixed stream

(LG 4; Intermediate)

a. The present value of end-of-year cash flows CF1 = $800, CF2 = $900, CF3 = $1,000, CF4

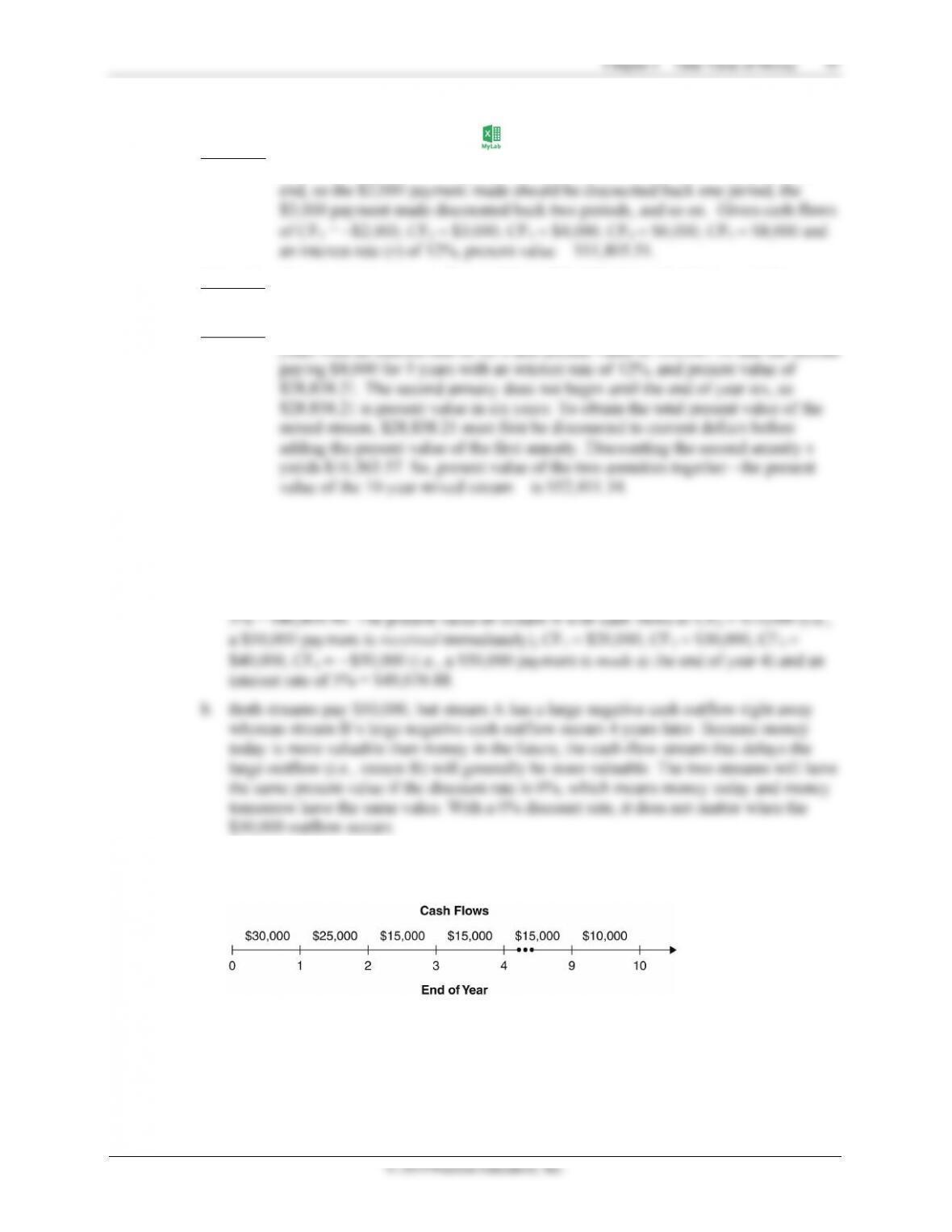

Year

5

6

2

3

4

0

1

© 2019 Pearson Education, Inc.

P5-42 Personal finance: Annuities and compounding (LG 3 and LG 5; Intermediate)

a. For the ordinary annuity with annual compounding: n = 10, r = 8%, PMT = $300, and

P5-43 Deposits to accumulate growing future sum (LG 6; Basic)

Using the framework for future value of an annuity:

P5-44 Personal finance: Creating a retirement fund (LG 6; Intermediate)

P5-45 Personal finance: Accumulating a growing future sum (LG 6: Intermediate)

Step 1: Determining cost of home in 20 years: Given n = 20, r = 6%, and PV = $185,000,

P5-46 Personal finance: Inflation, time value, and annual deposits (LG 2, LG 3, and LG 6;

Challenge)

a. n = 25, r = 5%, PV = $200,000. Solve for FV25 = $677,270.99.

© 2019 Pearson Education, Inc.

P5-47 Loan payment (LG 6; Basic)

A: Given n = 3, r = 8%, and PV = $12,000, solve for PMT = $4,656.40.

P5-48 Personal finance: Loan-amortization schedule (LG 6; Intermediate)

a. Treat the problem like an ordinary annuity with n= 3, r = 4%, PV = $45,000, and solve

for PMT. Loan payment is $16,215.68.

b.

P5-49 Loan-interest deductions (LG 6; Challenge)

a. Use the ordinary annuity framework with n = 3, r = 13%, PV (loan amount) = $10,000,

and solve for PMT. Annual end-of-year loan payments = $4,235.22.

P5-50 Personal finance: Monthly loan payments (LG 6; Challenge)

a. Use the ordinary annuity framework with n = 12 × 3 = 36, r = 6% ÷ 12 = 0.005,

© 2019 Pearson Education, Inc.

Group Exercise

This chapter’s exercises provide each group with opportunities to use time value of money