Chapter 4

Cash Flow and Financial Planning

Instructor’s Resources

Chapter Overview

This chapter introduces the financial-planning process, starting with an overview of long-term or strategic

planning and moving to a detailed exploration of short-term (operating) financial planning and its two key

components: cash and profit planning. Cash planning involves preparation of a cash budget, while profit

planning involves preparation of a pro forma income statement and balance sheet. Step-by-step examples of

cash budget and pro forma statement development are used to illustrate nuances students might find

challenging—such as depreciation expenses as a cash inflow and the distinction between operating and free

cash flow. The chapter ends by highlighting weaknesses of the simplified approaches to pro forma statements

(judgmental and percent-of-sales methods)—while still emphasizing the importance of these statements

(along with the cash budget) as tools for disciplining management thinking about the range of possible cash

flow and profitability outcomes and responses to those outcomes.

Answers to Review Questions

4-1. The financial-planning process is a two-step, highly collaborative endeavor to track the financial

implications of the firm’s specific plan for creating value for shareholders. Step one is long-term or

strategic planning, which involves detailing firm financial initiatives and the expected consequences of

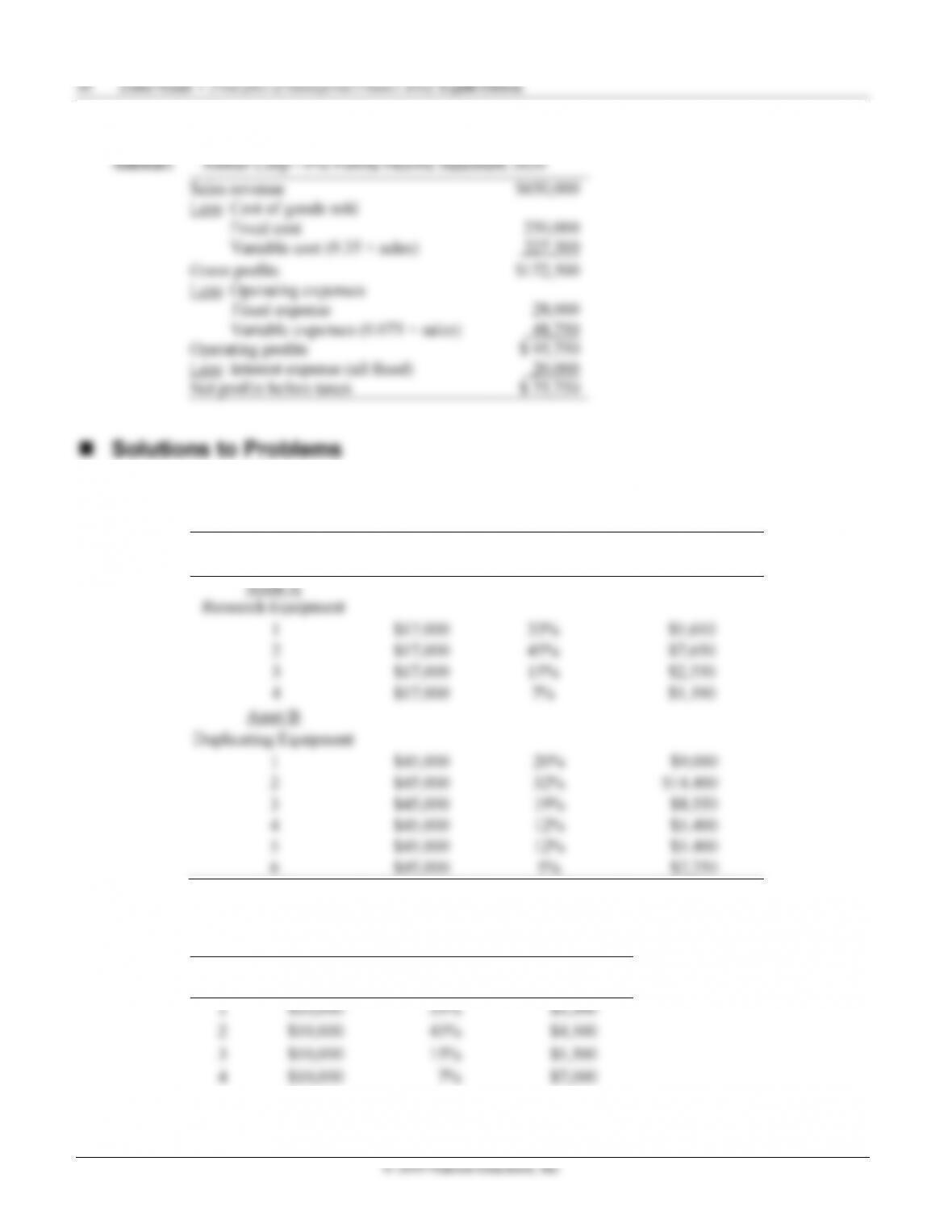

4-3 Property classes under the Modified Accelerated Cost Recovery System (MACRS) are categorized by

the length of the depreciation (recovery) period. The first four classes are 3-, 5-, 7-, and 10-years:

Recovery Period Definition

3 years Research and experiment equipment and certain special tools

© 2019 Pearson Education, Inc.

4-4. Cash flow from operating activities captures cash inflows/outflows related to the firm’s production cycle,

beginning with the purchase of raw materials and ending with the finished product. Expenses related to

4-5. A decrease in the cash balance is a source of cash flow because funds will be used for some other

4-6. In compiling a cash-flow budget, it is important to recognize depreciation is a noncash expenditure on

the firm’s income statement. Put another way, depreciation expense reduces taxable income but does

4-7. The statement of cash flows traces cash inflows/outflows from three different activities:

4-8. Operating cash flow isolates cash inflows/outflows from routine operations. Interest expense and taxes

4-9. Operating cash flow is cash flow generated from the firm’s regular production/sales of goods and

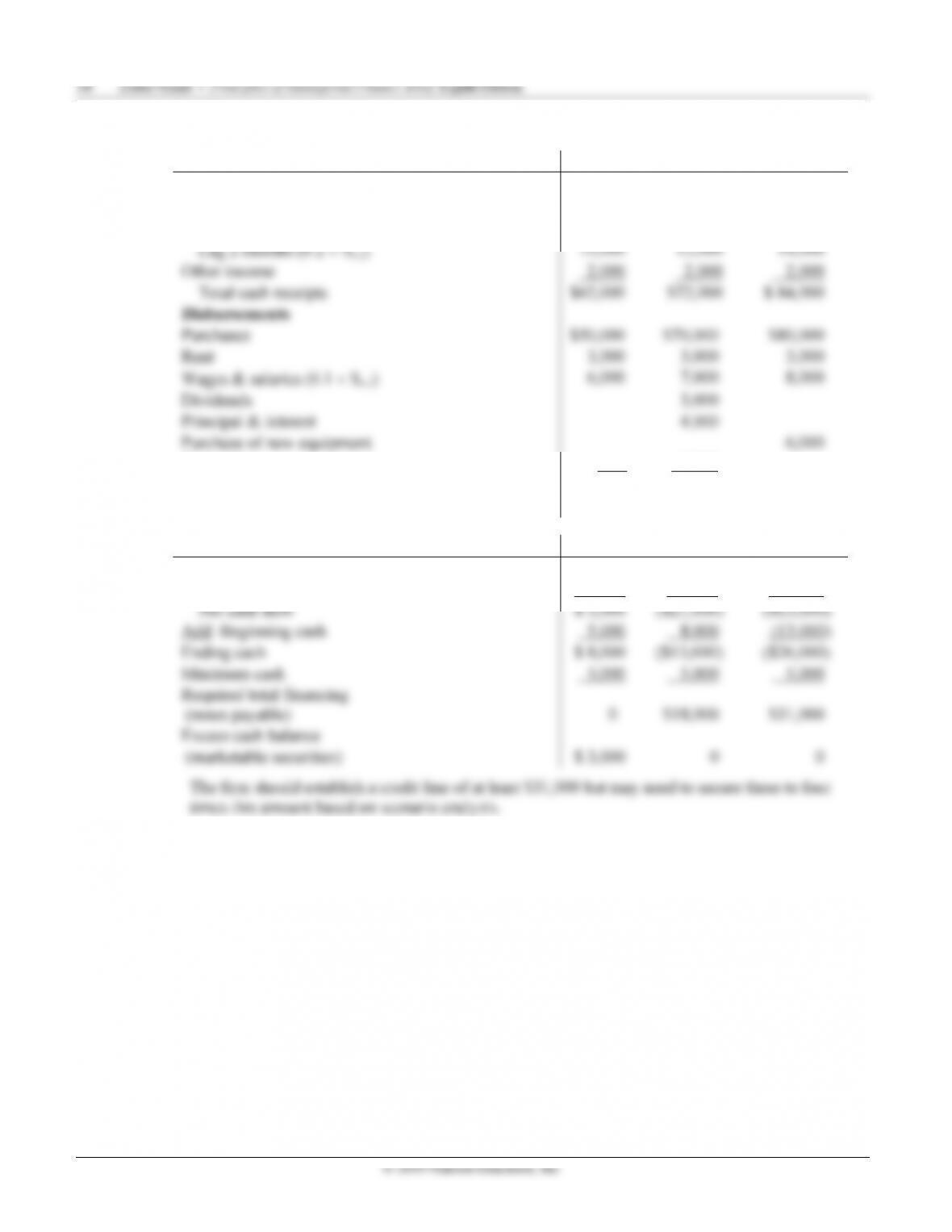

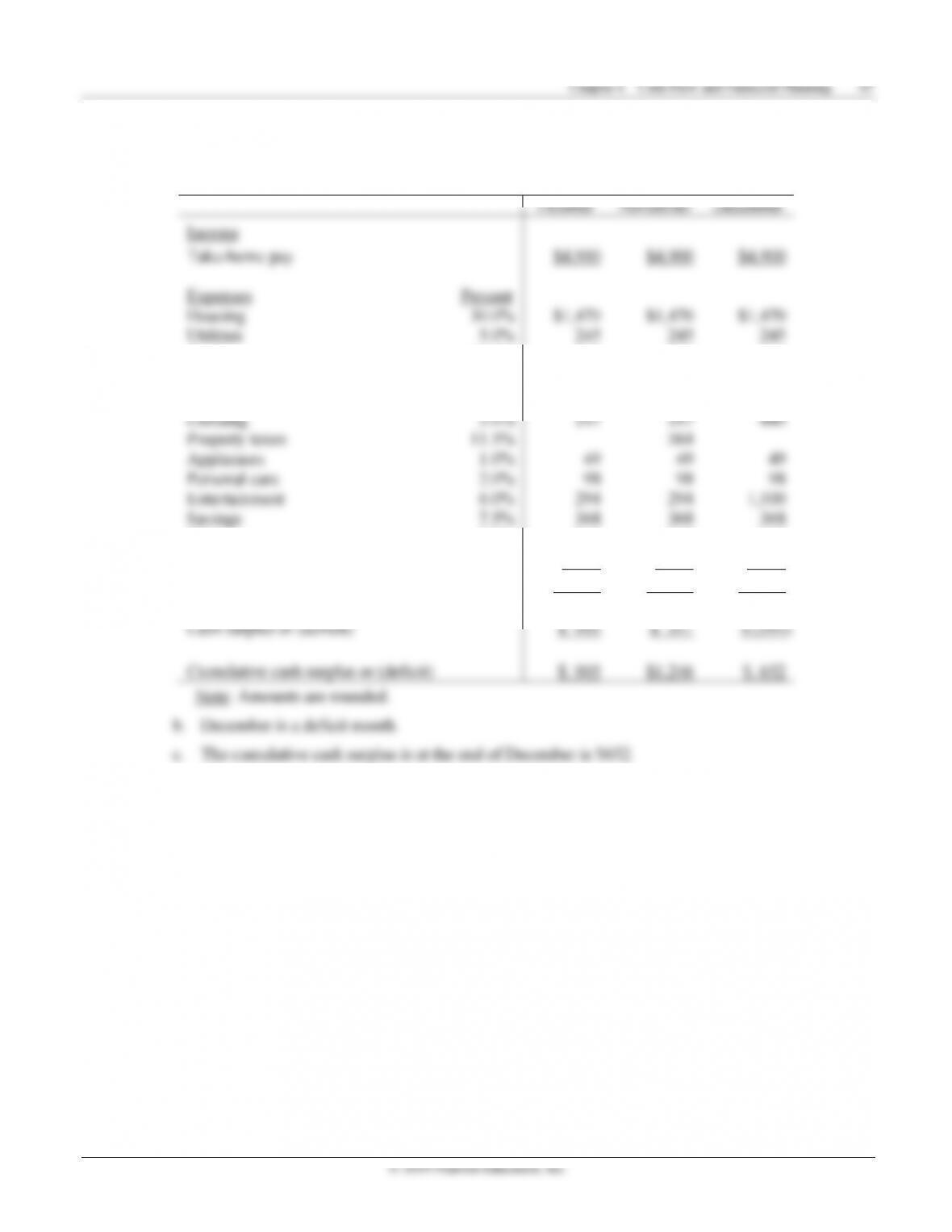

4-10. The cash budget is a statement of the firm’s planned cash inflows and outflows. Management uses this

© 2019 Pearson Education, Inc.

E4-1 Depreciation schedule (LG 2)

E4-2. Cash inflows and outflows (LG 3)

E4-3. Operating cash flow (LG 3)

E4-4. Free cash flow (LG 3)

© 2019 Pearson Education, Inc.

P4-7. Statement of cash flows (LG 3; Intermediate)

and 4.6, the increase in retained earnings may be broken down as follows:

Net profits after taxes $237

Less preferred dividends $10

Less common dividends $70

P4-8 Cash receipts (LG 4; Basic)

April May June July August