Chapter 12 Leverage and Capital Structure 271

P12-18 Personal finance: Capital structures (LG 3; Intermediate)

a. Monthly mortgage payment ÷ Monthly gross income = $1,100 ÷ $4,500 = 24.44%

P12-19 Various capital structures (LG 3; Basic)

Debt Ratio Debt Equity

10% $100,000 $900,000

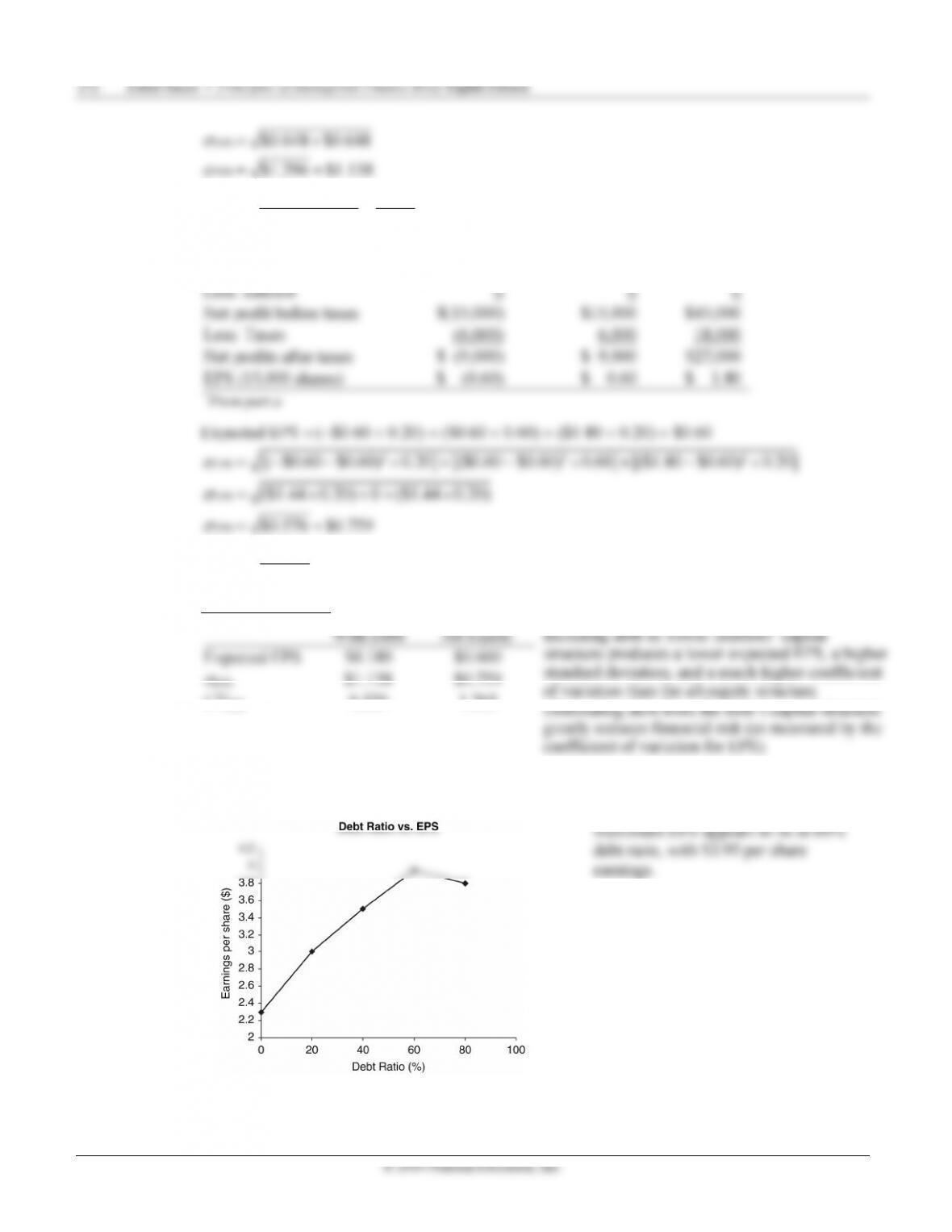

P12-20 Debt and financial risk (LG 3; Challenge)

a. EBIT Calculation:

Probability 0.20 0.60 0.20

Sales $200,000 $300,000 $400,000

Less: Variable costs (70%) 140,000 210,000 280,000

© 2019 Pearson Education, Inc.

σ

===

EPS

EPS 1.138 6.32

Expected EPS 0.18

CV

c.

EBIT * $(15,000) $15,000 $45,000

==EPS

$0.759 1.265

0.60

CV

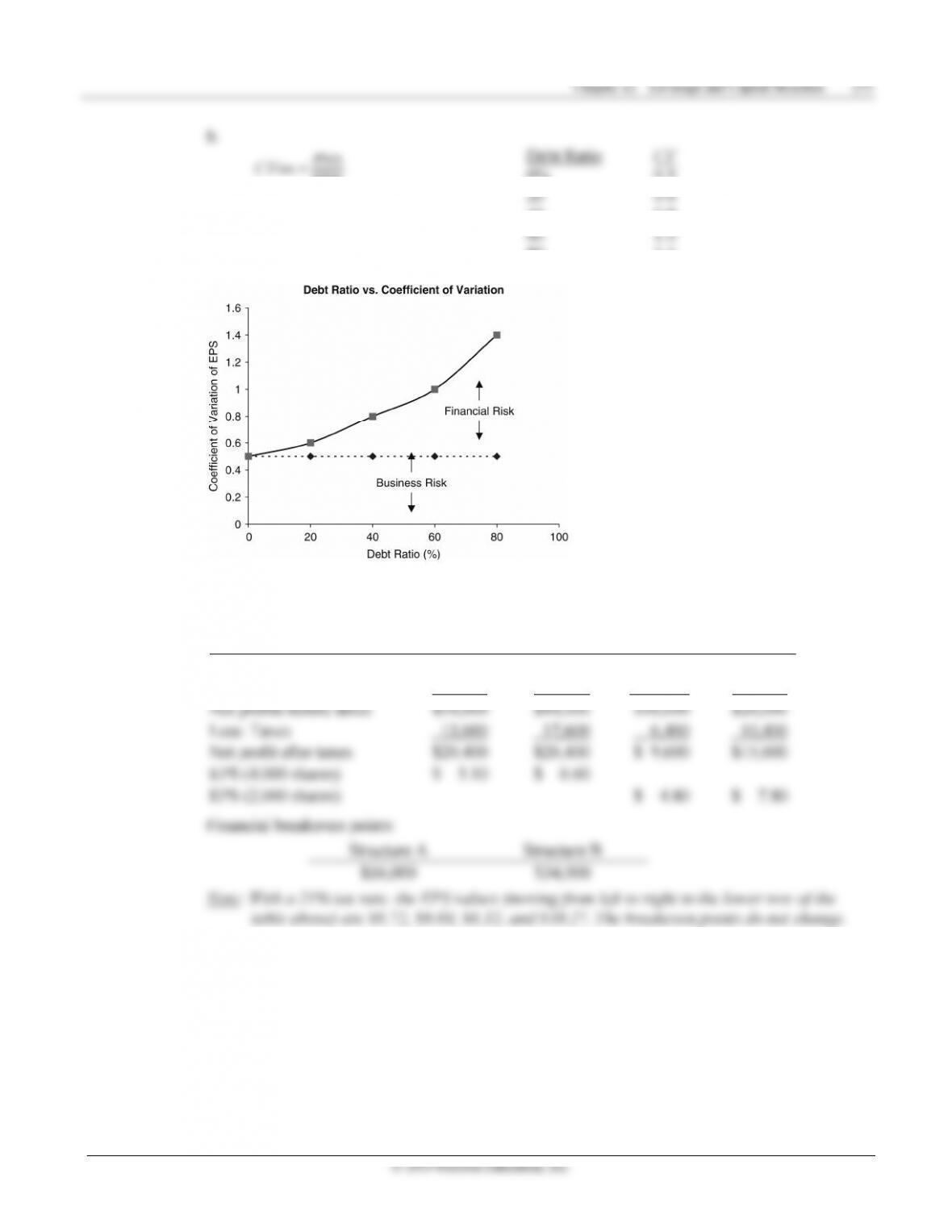

d. Summary statistics:

of variation than the all-equity structure.

Eliminating debt from the firm’s capital structure

greatly reduces financial risk (as measured by the

coefficient of variation for EPS).

CVEPS 6.320 1.265

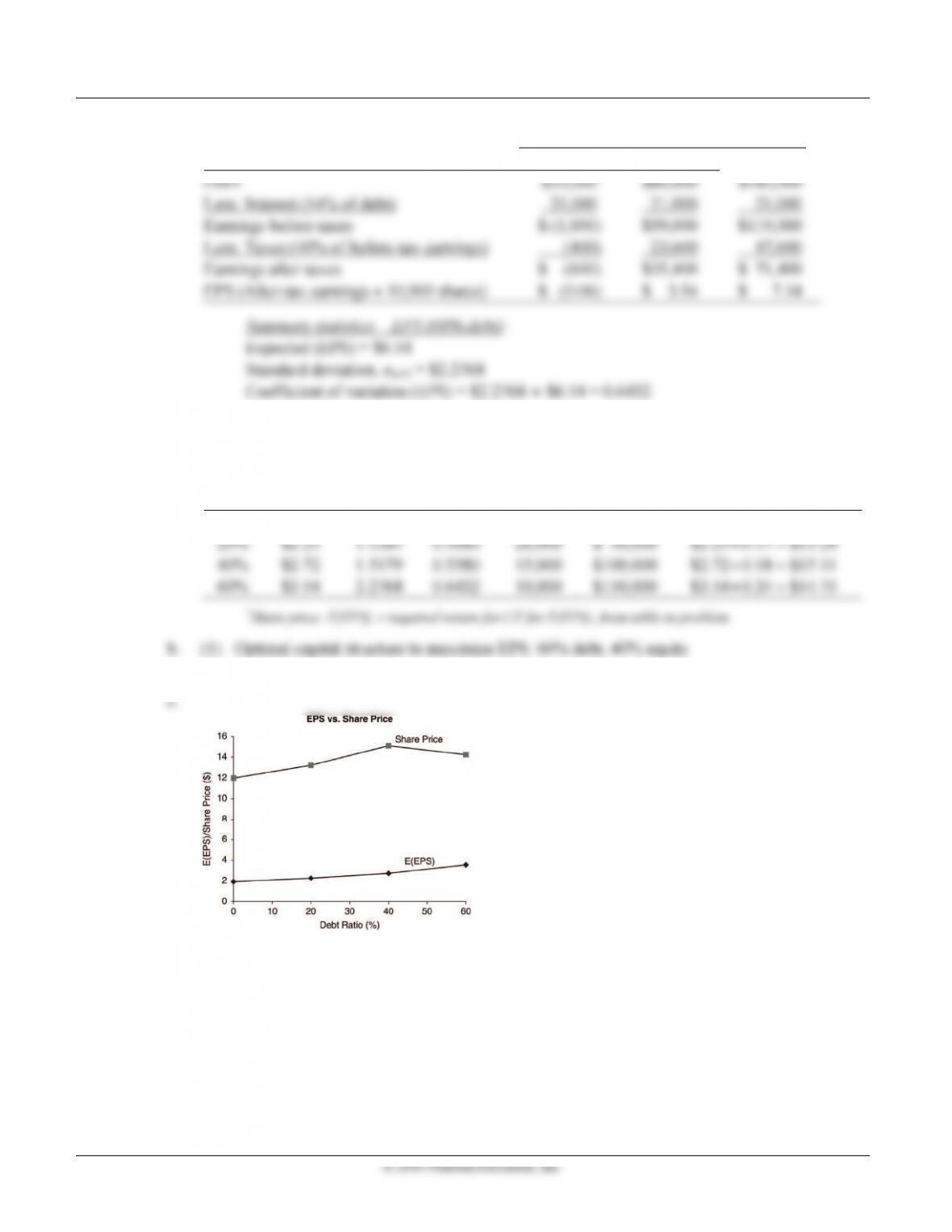

P12-21 EPS and optimal debt ratio (LG 4; Intermediate)

a.

© 2019 Pearson Education, Inc.

0% 0.5

40 0.8

80 1.5

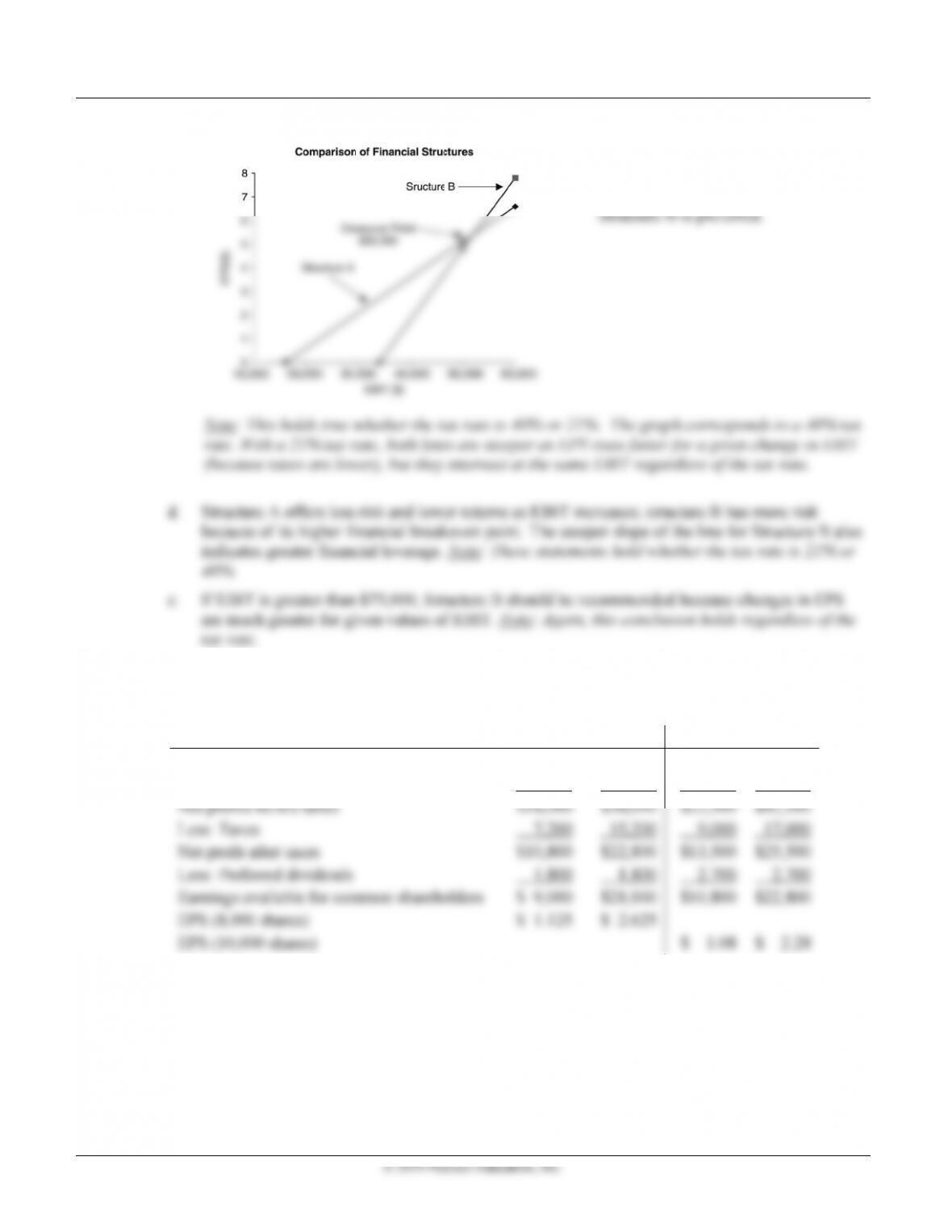

P12-22 EBIT-EPS and capital structure LG 5; Intermediate

a. Using $50,000 and $60,000 EBIT:

Structure A Structure B

EBIT $50,000 $60,000 $50,000 $60,000

Less: Interest 16,000 16,000 34,000 34,000

N

et profits before taxes $34,000 $44,000 $16,000 $26,000

Less: Taxes 13,600 17,600 6,400 10,400

N

et profit after taxes $20,400 $26,400 $ 9,600 $15,600

EPS (4,000 shares) $ 5.10 $ 6.60

EPS (2,000 shares) $ 4.80 $ 7.80

Financial breakeven points:

Structure A Structure B

$16,000 $34,000

Note: With a 21% tax rate. the EPS values (moving from left to right in the lower row of the

table above) are $6.72, $8.69, $6.32, and $10.27. The breakeven points do not change.

2

7

7

4 Zutter/S

m

b

.

t

t

0

S

S

m

art • Principl

e

and c.

i

i

e

e

8

a

a

m

o

o

2

1

1

2

e

s of Manageria

l

Finance Brief,

Eighth Edition

If

E

$5

2

if

E

u

E

BIT is expe

c

2

,000, Struct

u

E

BIT is expec

c

ted to fall be

l

u

re A is prefe

r

ted to top $5

2

l

ow

r

red and

2

,000,

o

.

o

c

s

n

i

b

c

n

E

u

E

l

u

B

l

b

u

u

i

u

i

Chapter

12 Leverage

a

a

nd Capital Stru

c

c

ture 275

278 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

Probability (p)

p

1 = 0.20 p2 = 0.60 p3 =0.20

***

Debt

Ratio

Expected

(EPS)

σ

(EPS)

CV(EPS)

Common

Shares

Total

Debt ($)

Share Price*

= Expected EPS

÷ Required Return

0% $1.92 0.9107 0.4743 25,000 0 $1.92÷0.16

=

$12.00

=

=

=

(2) Optimal capital structure to maximize share price: 40% debt, 60% equity

© 2019 Pearson Education, Inc.

$41.67, $42.82, $40.75, $36.70, and $30.19.

P12-27 Integrative: Optimal capital structure (LG 3, 4, 5, 6; Challenge)

0.30 0.40 0.30

Sales $600,000 $900,000 $1,200,000

Less: Variable costs (40%) 240,000 360,000 480,000

Less: Fixed costs 300,000 300,000 300,000

EBIT $ 60,000 $240,000 $ 420,000

t

t

c.

Deb

t

Ratio

Amoun

t

of Debt

Before-Tax

Cost of Debt

Annual

Interest

0% $ 0 0.0% $ 0

15% 150,000 8.0 12,000

© 2019 Pearson Education, Inc.

−

×

÷

=

−

×

÷

=

($240,000

−

$12,000)

×

(0.6)

÷

34,000 shares

=

4.02

($420,000

−

$12,000)

×

(0.6)

÷

34,000 shares

=

7.20

30% ($60,000 − $30,000) × (0.6) ÷ 28,000 shares = $0.64

($240,000

−

$30,000)

×

(0.6)

÷

28,000 shares

=

4.50

($420,000

−

$30,000)

×

(0.6)

÷

28,000 shares

=

8.36

−

×

÷

=

−

×

÷

=

−

×

÷

=

−

×

÷

=

×

+

×

+

×

0.27

+

1.44

+

1.89 = $3.60

15% 0.30 × (0.85) + 0.40 × (4.02) + 0.30 × (7.20)

+

+

0.19

+

1.80

+

2.51 = $4.50

45% 0.30 × (0.04) + 0.40 × (4.95) + 0.30 × (9.86)

+

+

−

0.47

+

2.07

+

3.58 = $5.18

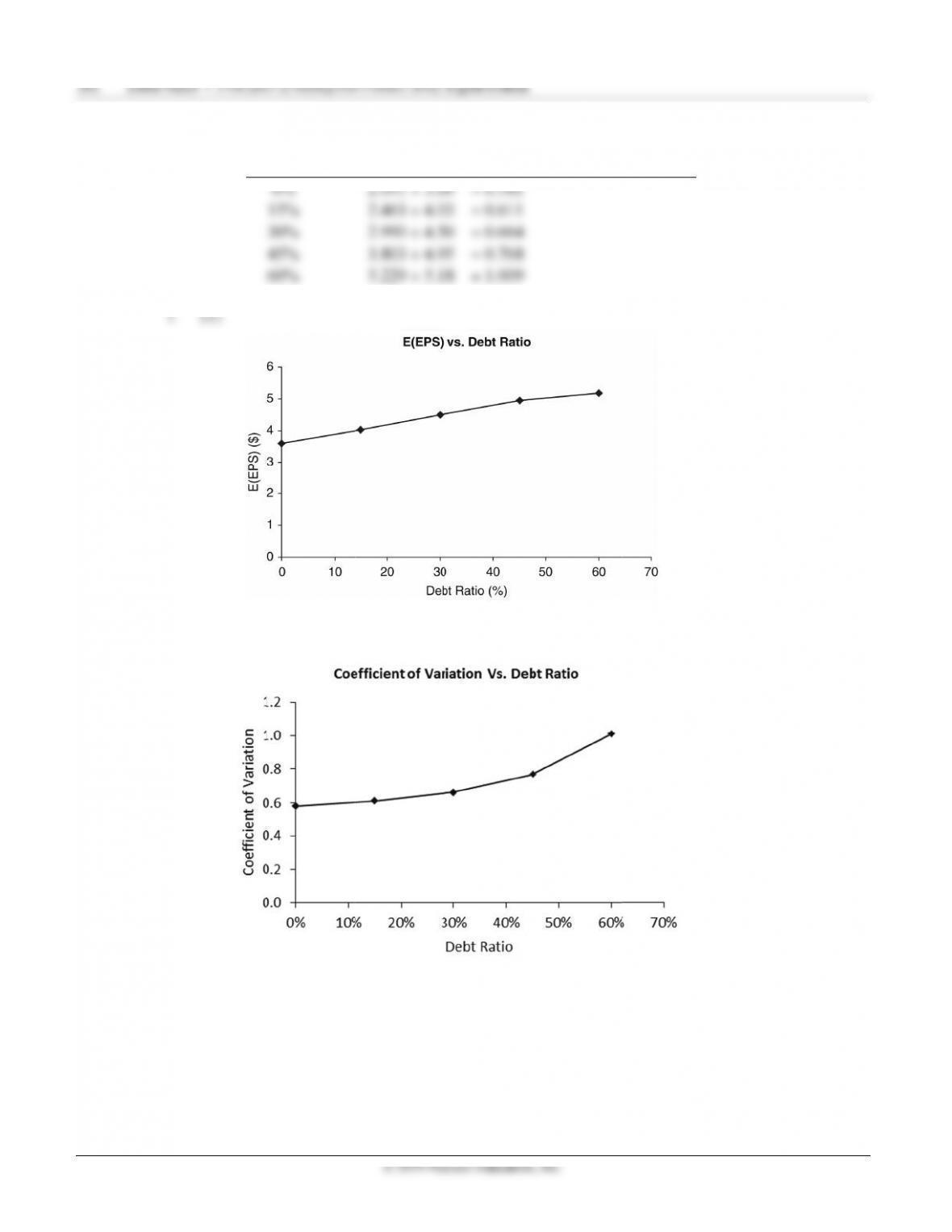

(2) Standard deviation of EPS,

σ

EPS:

Debt Ratio Calculation

222

σ

σ

σ

EPS 7.232 0 7.232

σ

=++

= 3.803

22 2

−

×

÷

=

© 2019 Pearson Education, Inc.

=(1 ) (EBIT )

EPS number of common shares outstanding

Set EPS 0% = EPS 30% and EPS 30% = EPS 60%. The first calculation, EPS 0% = EPS 30%, is

as follows:

−−−

=

[(1 0.4)(EBIT $0) 0]

EPS 40,000 shares

0% $3.60 ÷ 0.100 $36.00

15% $4.03 ÷ 0.105 $38.38

30% $4.50 ÷ 0.116 $38.79

45% $4.95 ÷ 0.140 $35.36

60% $5.18 ÷ 0.200 $25.90

© 2019 Pearson Education, Inc.

P12-28 Ethics problem (LG 3; Intermediate)

An information asymmetry occurs when one party has more information than other interested parties.

Such an asymmetry can occur when managers overleverage or lead a company buyout Existing

bondholders and possibly stockholders could be harmed by the financial risk of overleveraging, and

existing stockholders will be harmed if they accept a buyout price below that consistent with accurate

c. Giv

e

slo

p

rati

o

of e

tha

n

abo

u

d. Rec

Alt

e

e. Alt

e

the

f

wit

h

stru

c

Sprea

Answers

on www

.

Grou

p

Group e

x

This cha

p

income

s

fixed/va

r

their fict

i

b

reakev

e

highligh

t

Returnin

Likewis

e

will con

c

shadow

a

e

n Tampa M

a

p

e of the line

s

o

. Although

E

ach alternati

v

n

shareholder

u

t $750,000

(

all, share pri

c

e

rnative A—

3

e

rnative A, 3

0

f

inancial risk

h

4 times cov

e

c

ture allows

t

dsheet

E

to Chapter 1

2

.

pearson.co

m

p

Exercis

x

ercises are

a

p

ter integrate

s

tatement of t

h

r

iable operati

n

i

tious firm.

A

e

n point of th

e

t

ing the brea

k

g to their sha

e

, groups will

c

lude with st

u

a

nd fictitious

a

nufacturing’

representin

g

E

PS is highes

t

v

e. The draw

b

wealth. Put

a

(

intersection

o

c

e can be esti

m

3

0%: $7.71

÷

0

% debt, app

e

is high; time

e

rage of inte

r

t

he firm to b

e

E

xercise

2

’s Starstruc

k

m

/mylab/finan

c

e

a

vailable on

w

s leverage in

t

h

eir shadow

f

n

g costs. Usi

n

A

fter assignin

g

e

ir fictitious

f

k

even sales u

n

d

ow firm, th

e

calculate the

u

dents using

e

firms.

© 2019

P

s EBIT of $1

g

higher debt

l

t

at 50%, the

b

ack to the E

B

a

nother way,

i

o

f 10% and 3

0

m

ated using:

0.13

=

$59.3

e

ars to be the

s interest ear

n

est earned, a

n

e

nefit from fi

n

k

Company e

x

c

e.

w

ww.pearson

t

o valuation

o

f

irm—focusi

n

n

g this infor

m

g

a pe

r

-unit p

r

f

ir

m

(using a

s

n

it level). Ne

x

e

groups will

shadow firm

’

e

quation 12.1

2

P

earson Educati

o

,200,000, EP

l

evels demon

company mu

B

IT-EPS app

r

i

t does not su

0

% debt), EP

P

0

=

EPS

÷

r

1, and altern

a

best alternat

i

n

ed is only 2

n

d provides i

n

n

ancial lever

a

x

ercise on o

p

.com/mylab/

f

o

f the firm. S

t

n

g on measur

e

m

ation, group

s

r

ice for their

s

imple graph

x

t, groups wi

l

also calculat

e

’

s DTL at cu

r

2

(and infor

m

Chapter

o

n, Inc.

S is highest

w

strates finan

c

u

st also take i

n

r

oach is its e

m

u

fficiently co

n

P

S is higher

w

r

s

. So, curren

t

a

tive B—50

%

i

ve. Althoug

h

times. Alter

n

n

creased mar

k

a

ge while not

p

timal capital

f

inance.

t

udents will

b

es related to

l

s

will assem

b

product, gro

u

of sales reve

n

l

l calculate t

h

e

DFL at curr

r

rent sales an

d

m

ation from e

a

12 Leverage

a

w

ith the 50%

c

ial leverage

i

n

to considera

t

m

phasis on

m

n

sider risk. A

l

w

ith a capital

s

t

price: $6.66

%

: $9.00

÷

0.

1

h

EPS is high

e

n

ative A has

a

k

et value. C

h

taking on to

o

structure are

b

egin by retri

e

l

everage, suc

h

b

le a similar i

n

u

ps will calc

u

nue and total

h

e DOL at a b

r

ent levels of

E

d

EPS levels.

arlier exercis

a

nd Capital Stru

c

debt ratio. T

h

i

ncreases wit

h

t

ion the fina

n

m

aximizing E

P

l

so, if EBIT

f

s

tructure of 1

÷

0.12

=

$55

1

8

=

$50.00

e

r with Alter

n

a

moderate ri

s

h

oosing this c

a

o

much finan

c

available

e

ving the mo

s

h

as EBI and

n

come state

m

u

late the oper

a

operating co

ase sales lev

e

E

PS and EBI

T

This chapte

r

es) to value t

h

c

ture 285

h

e steeper

h

the debt

n

cial risk

P

S rather

f

alls below

0%.

.50.

n

ative B,

s

k level,

a

pital

c

ial risk.

s

t recent

m

ent for

a

ting

sts and

e

l.

T

.

r

’s exercise

h

eir