Part 6

Long-Term Financial Decisions

Chapters in This Part

Chapter 12 Leverage and Capital Structure

Chapter 13 Payout Policy

Chapter 12

Leverage and Capital Structure

Instructor Resources

Chapter Overview

This chapter introduces students to operating and financial leverage and the associated business and financial

risks. As a prelude to operating leverage, breakeven analysis is explained (and its limitations noted) with help

from pictures and algebra. Next, the degree of operating, financial, and total leverage are introduced and

developed as tools for measuring the risk of the firm associated with differing operating and financial

structures. Finally, the notion of optimal capital structure— the mix of debt and equity that maximizes firm

value—is introduced conceptually along with the EBIT-EPS and valuation model approaches to evaluating

capital structure. Chapter 12 concludes by showing how breakeven analysis, leverage, and risk arising from

borrowing will affect the personal as well as professional lives of students.

Note to instructors: After the first print run of this edition, Congress passed the Tax Cuts and Jobs Act, which

made sweeping changes to the corporate tax code. The original print run of this edition did not incorporate

any of the changes of that Act, but subsequent printings did. Some problems below have solutions for the

current 21% corporate tax rate (reflected in recent printings), as well as solutions for a tax rate (appearing in

the first print run) reflecting the older tax law.

Answers to Review Questions

12-1 Leverage refers to the use of fixed expenses to magnify shareholder returns. Operating leverage

refers to the use of fixed operating costs to magnify the impact of changes in sales revenue on

earnings before interest and taxes (EBIT). Financial leverage refers to the use of fixed financial costs

12-2 The firm’s operating breakeven point is the level of sales at which all fixed and variable operating

costs are covered, i.e., EBIT equals zero. An increase (decrease) in fixed operating costs and variable

12-3 Operating leverage is the ability to use fixed operating costs to magnify the effects of changes in

sales on earnings before interest and taxes. Operating leverage results from the existence of fixed

operating costs in the firm’s overall cost structure. The degree of operating leverage (DOL) is

12-4 Financial leverage refers to the use of fixed financial costs to magnify the effects of changes in EBIT on

earnings and earnings per share (EPS); it arises when a firm relies on funding sources with fixed costs

such as interest on debt and dividends on preferred stock. The degree of financial leverage (DFL) can

12-5 The total leverage of the firm is the combined effect of fixed costs (operating and financial) on EPS;

it reflects both operating and financial leverage. Increases in either type of leverage will increase the

12-6 A firm’s capital structure is the mix of long-term debt and equity it utilizes. The key differences

between debt and equity capital are summarized:

Characteristic Debt Equity

Voice in management* No Yes

12-7 In general, non-U.S. companies rely much more on debt than U.S. corporations. In large part, this

difference reflects the relative sophistication of U.S. capital markets, which offer a large menu of

financing options. Also, large commercial banks take an active role in financing foreign corporations.

12-8 The tax deductibility of interest is the major benefit of debt finance. In effect, the government

12-9 Business risk refers to fluctuations of the firm’s cash flows not traceable to fixed-cost financing.

Business risk reflects (i) fixed operating costs (operating leverage), revenue stability, and cost

stability. Revenue stability refers to the variability of the firm’s sales revenues, which in turn depends

12-10 An agency problem arises in borrowing because lenders provide funds based on their expectations

about firm risk. But firm managers can increase shareholder wealth by increasing risk after loan terms

12-11 Asymmetric information results when a firm’s managers have more information about operations and

future prospects than investors. This information edge could cause financial managers to raise funds

using a pecking order (a hierarchy of financing beginning with retained earnings, followed by debt,

12-12 As financial leverage increases, both the cost of debt and the cost of equity increase, with equity

rising at a faster rate. As reliance on debt rises, the overall cost of capital first decreases to a

12-13 The EBIT-EPS approach shows how different capital structures affect EPS over a range of EBIT. The

EBIT-EPS approach involves selecting the capital structure providing maximum EPS, which

12-14 It is unlikely that attempts to maximize value would produce the same capital structure as attempts to

12-15 The firm should find the capital structure that balances risk and return to maximize share value. This

requires estimating EPS and required rates of return for different levels of debt then choosing the

debt-equity mix that produces the highest share price. In addition to quantitative considerations, the

firm should take into account factors related to business risk, agency costs, and asymmetric

Answers to Warm-Up Exercises

E12-1 Breakeven analysis

E12-2 Changing costs and the operating breakeven point

E12-3 Degree of operating leverage (DOL)

E12-4 Degree of financial leverage (DFL)

E12-5 Net operating profits after taxes (NOPAT)

P12-1 Breakeven point: Algebraic (LG1; Basic)

Q = Fixed Cost ÷ (Price – Variable Cost) = $12,350 ÷ ($24.95 – $15.45) = 1,300.

P12-2 Breakeven comparisons: Algebraic (LG 1; Basic)

()

$18.00 $6.75

− Firm H:

()

$30.00 $12.00

−

()

$21.00 $13.50

−

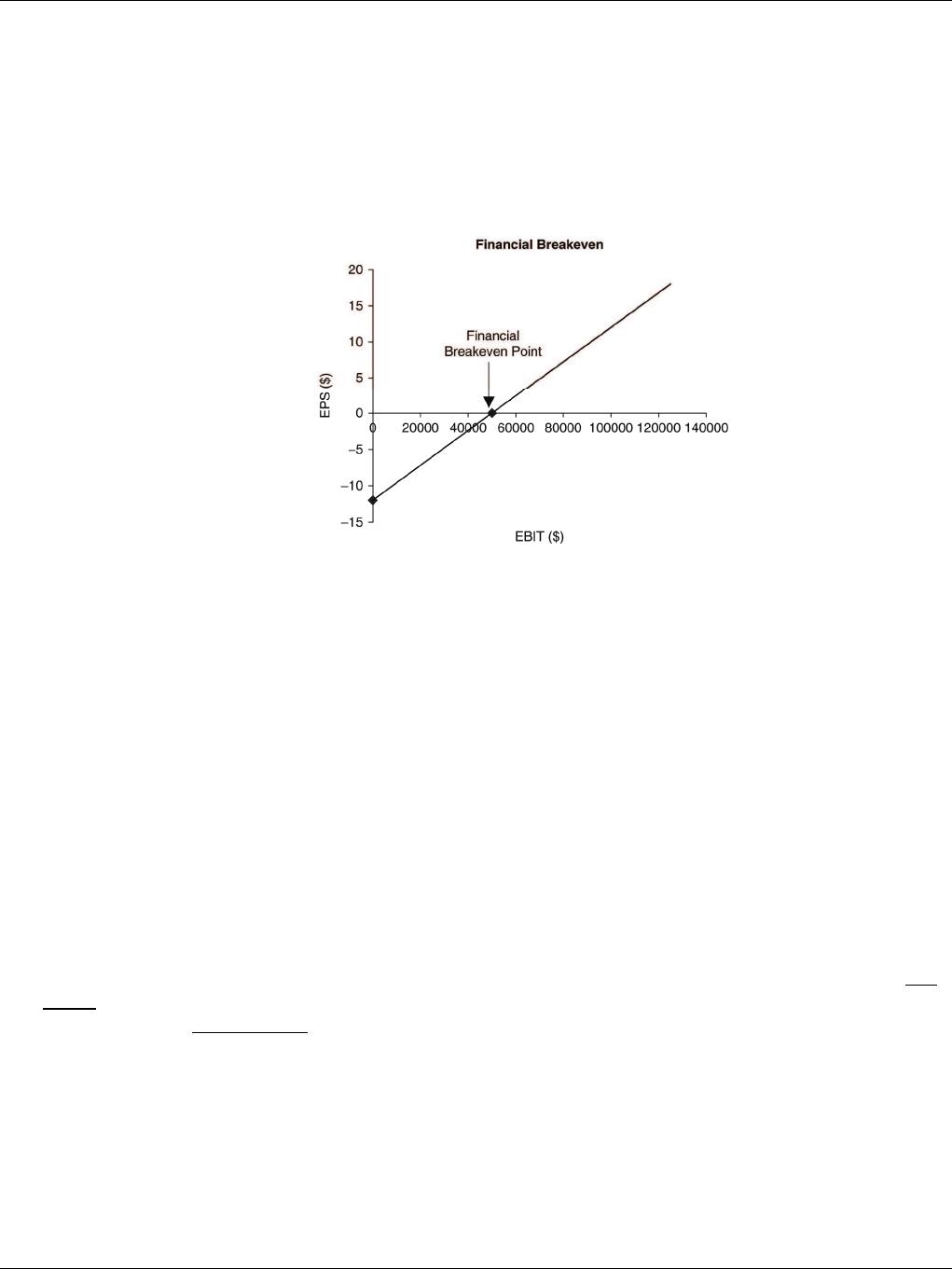

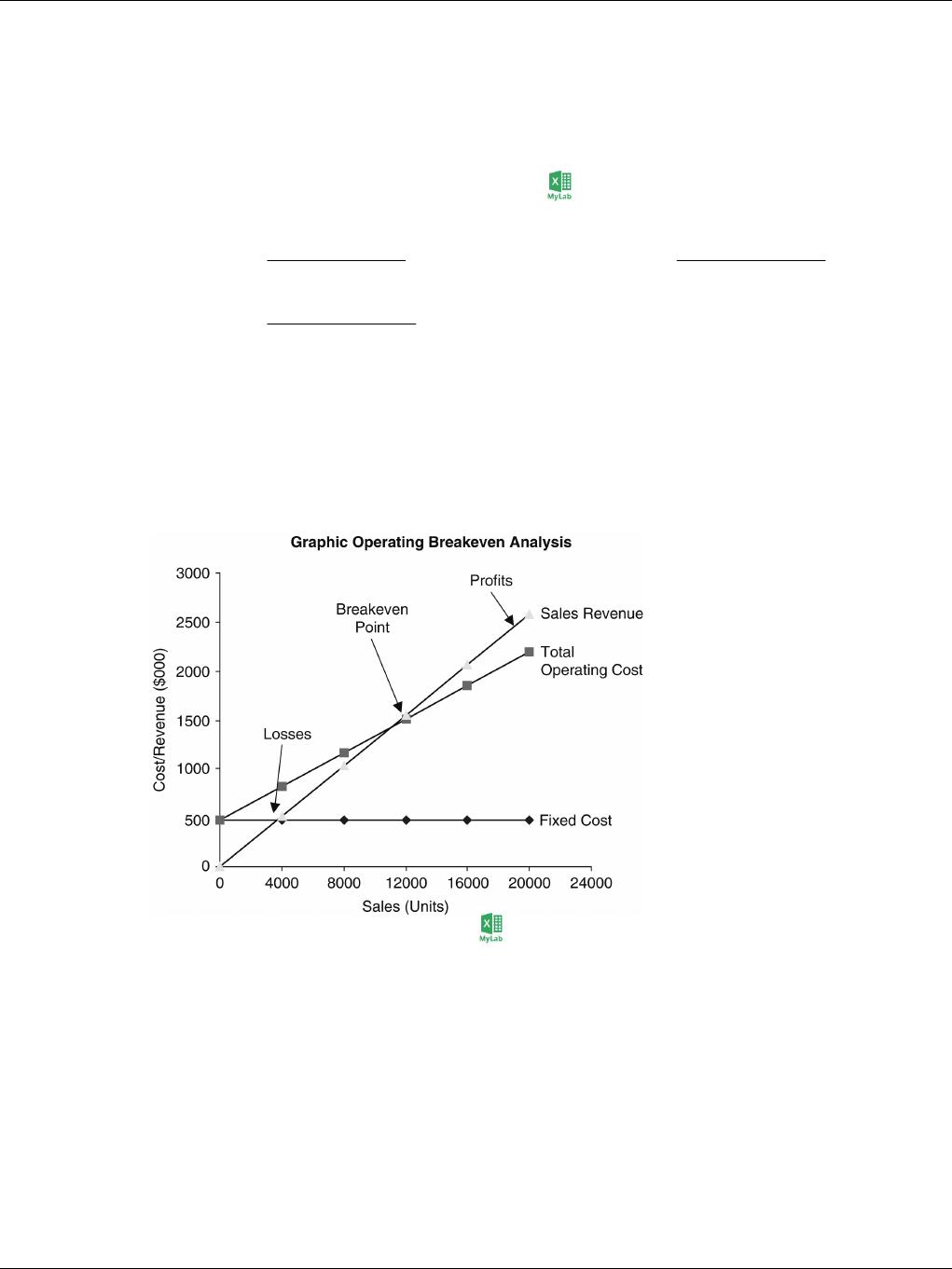

P12-3 Breakeven point: Algebraic and graphical (LG 1; Intermediate)

P12-4 Breakeven analysis (LG 1; Intermediate)

a. Let QBE = breakeven level of unit sales, FC = fixed cost, P = price, and VC = variable cost per

unit. QBE = FC ÷ (P – VC) = $73,500 ÷ ($13.98 – $10.48) = 21,000 books.

P12-5 Personal finance: Breakeven analysis (LG 1; Easy)

a. Breakeven point in months = fixed cost ÷ (monthly benefit – monthly variable costs)

P12-6 Breakeven point: Changing costs/revenues (LG 1; Intermediate)

Let QBE = breakeven level of unit sales, FC = fixed cost, P = price, and VC = variable cost per unit.

P12-7 Breakeven analysis (LG 1; Challenge)

Let Q = unit sales, FC = fixed cost, P = price, and VC = variable cost per unit.

a. QBreakeven = FC ÷ (P − VC) = $4,000 ÷ ($8.00 – $6.00) = 2,000 figurines.

b. Sales $10,000

Less:

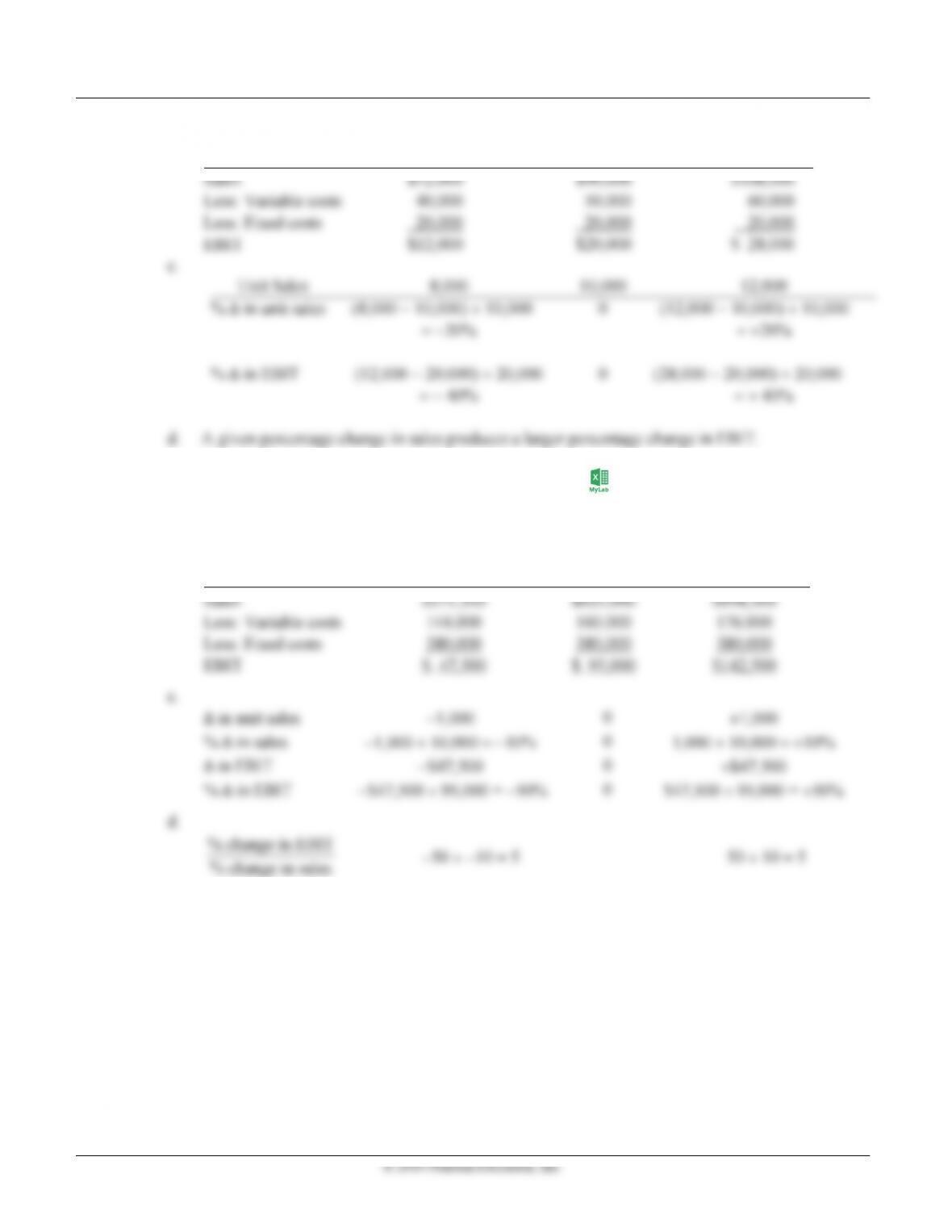

P12-8 EBIT sensitivity (LG 2; Intermediate)

264 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

a. and b.

8,000 Units 10,000 Units 12,000 Units

P12-9 Degree of operating leverage (DOL) (LG 2; Intermediate)

a. Let QBE = breakeven level of unit sales, FC = fixed cost, P = price, and VC = variable cost per

unit. QBE = FC ÷ (P − VC) = $380,000 ÷ ($63.50 − $16) = 8,000 units.

b.

9,000 Units 10,000 Units 11,000 Units

e

P12-10

D

L

a

b

c

d

e

u

o

D

egree of op

e

L

et Q = unit

s

a

. Breakev

e

b

. Degree

o

c

d

u

o

e

V

e

rating lever

a

s

ales, P = uni

t

e

n sales, Q

BE

o

f operating l

e

×−

[(

QP

V

=

V

e

s

V

a

ge (DOL):

G

t

price, VC =

= FC (P –

e

verage at ba

s

)]

V

C

V

e

s

,

G

raphical (L

G

variable cost

s

VC) = $72,0

0

s

e sales level

,

e

C

,

G

2; Interm

e

s, and FC =

f

0

0 ($9.75

–

,

Q, is given

b

b

e

diate)

f

ixed costs.

–

$6.75) = 24

b

y:

s

,000

P12-11 EPS calculations (LG 2; Intermediate)

a. Common earnings = EBIT – Interest – Taxes – Dividends on preferred stock

= (EBIT – Interest) × (1 – Tax rate) – Preferred dividends

P12-12 Degree of financial leverage (LG 2; Intermediate)

a.

EBIT $80,000 $120,000

Less: Interest 40,000 40,000

N

et profits before taxes $40,000 $ 80,000

N

⎢⎥

⎜⎟

−

⎝⎠

⎣⎦

T = tax rate

$80,000

N

N

==

DFL 1.25

P12-13 Personal finance: Financial leverage (LG 2; Challenge)

a.

Current DFL Initial Values Future Value % ∆

DFL = 18.2% ÷ 10% = 1.82

b. and c.

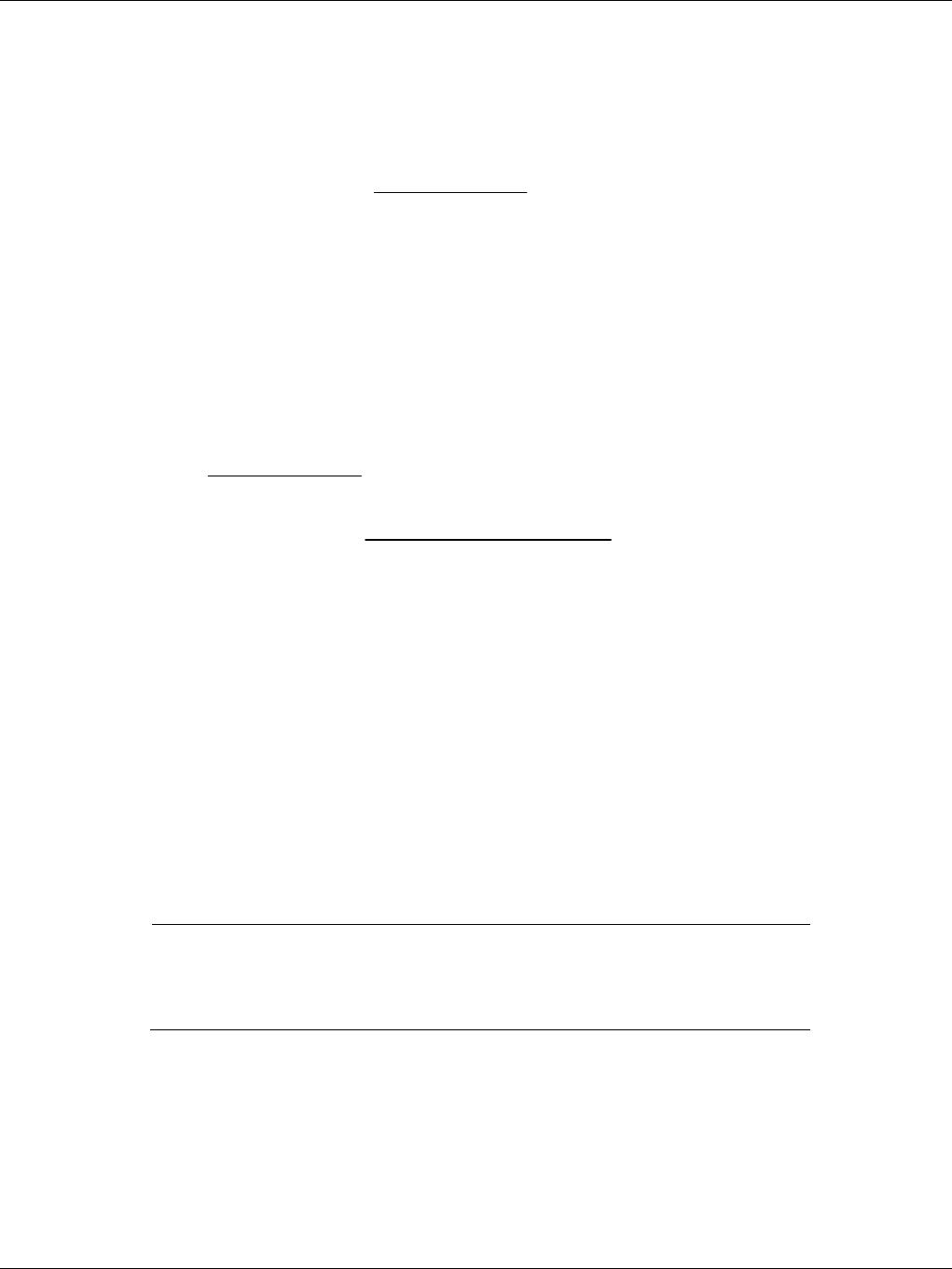

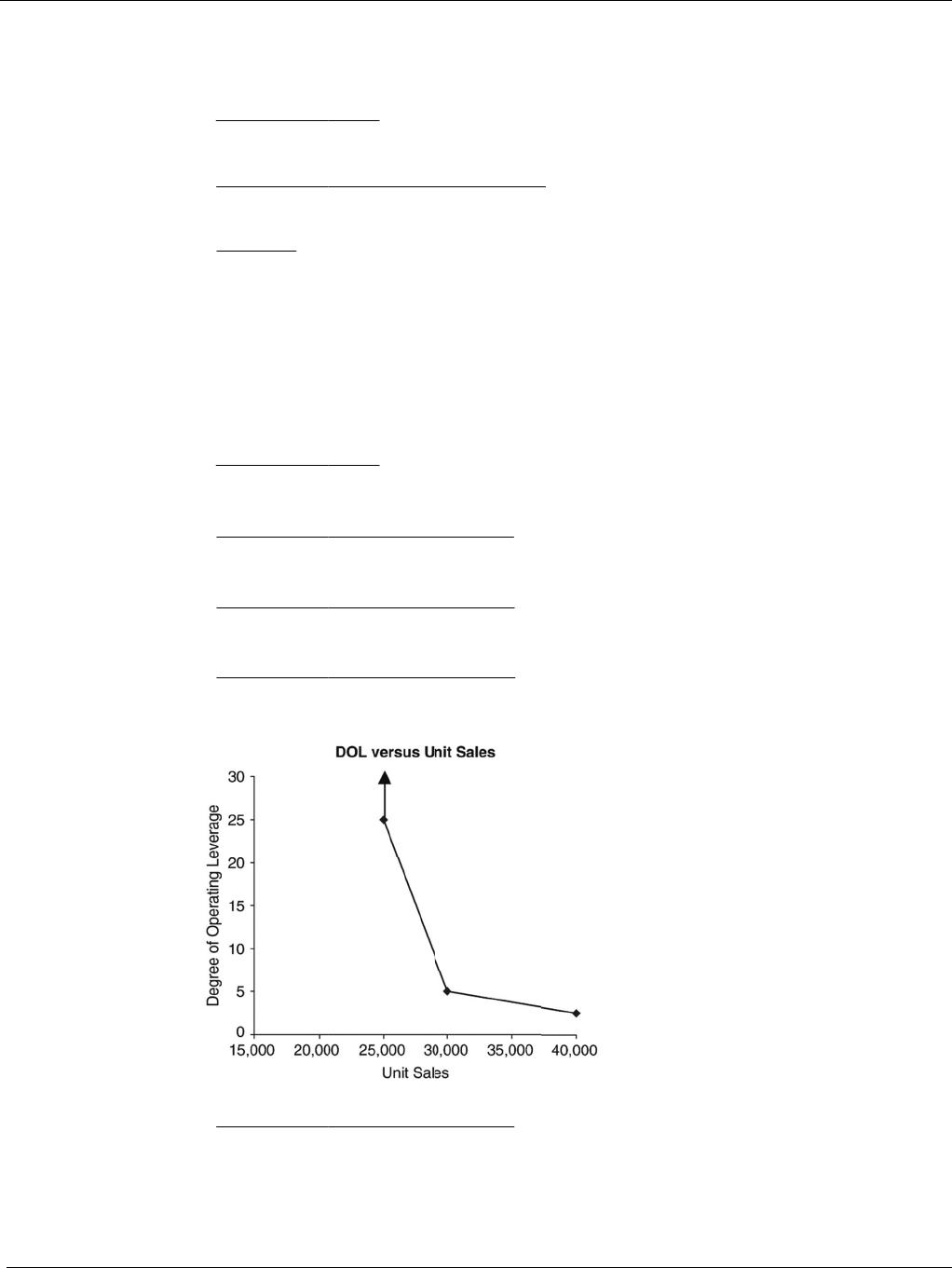

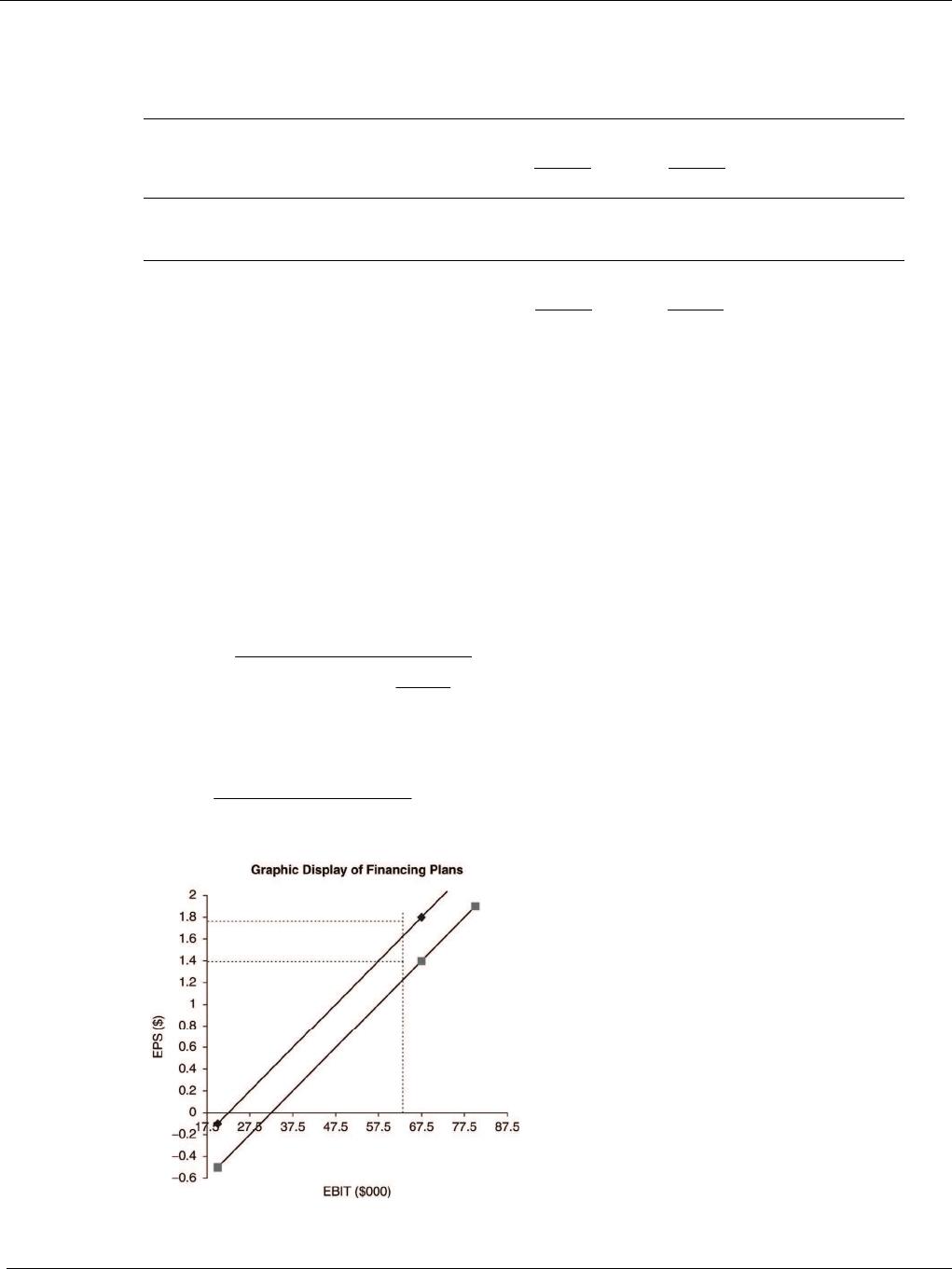

P12-14 DFL and graphic display of financing plans (LG 2, 5; Challenge)

a. Degree of financial leverage (DFL) is given by:

=⎡⎤

EBIT

DFL 1

where:

==

−−

DFL 1.5

[$67,500 $22,500 0]

b.

268 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

$67,500

financing

plan

15,000

−−

P12-15 Integrative: Multiple leverage measures (LG 1, 2; Intermediate)

Let Q = unit sales, P = unit price, VC = variable costs, and FC = fixed costs.

===

×− −

DOL 1.78

[400,000 ($1.00 $0.84)] $28,000 $36,000

c. Earnings before interest and taxes (EBIT) = (P × Q) − FC − (Q × VC)

EBIT = ($1.00 × 400,000) − $28,000 − (400,000 × $0.84) = $36,000

==

⎡⎤

⎛⎞

−−

⎢⎥

⎜⎟

−

DFL 1.35

$2,000

$36,000 $6,000 (1 0.4)

Note: With a 21% tax rate, DFL is 1.31.

===

DTL 2.40

P12-16 Integrative: Leverage and risk (LG 2; Intermediate)

a. Let Q = unit sales, P = unit price, VC = variable costs, and FC = fixed costs.

(

)

()

DOL at base sales level QPVC

QQ P VC FC

×−

=×− −

==

−

DFL 1.71

[$24,000 $10,000]

R

==

−

DFL 1.25

[$87,500 $17,500]

W

P12-17 Integrative—multiple leverage measures and prediction (LG 1, 2; Challenge)

a. Let Q = unit sales, P = unit price, VC = variable costs, and FC = fixed costs.

QBreakeven = FC ÷ (P − VC) = $50,000 ÷ ($6 − $3.50) = 20,000 latches

270 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

b. Sales ($6 × 30,000) $180,000

Note: If the tax rate is 21% then net profits are $9,480, and earnings available for common

stockholders is $2,480.

c.

(

)

()

DOL at base sales level QPVC

QQ P VC FC

×−

=×− −

−

⎝⎠

⎣⎦

T = tax rate

So, ===

$25,000 $25,000

DFL 75.00

so New EBIT = $25,000 + ($25,000 × 150%) = $62,500.

Now, DTL = %∆ EPS ÷ %∆ in sales = %∆ common earnings ÷ %∆ in sales because outstanding

shares did not change. So, %∆ common earnings = %∆ sales × DTL = 50% × 225% = 11,250%.

And, new common earnings

= Old common earnings + (Old common earnings × %∆ common earnings)