240 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

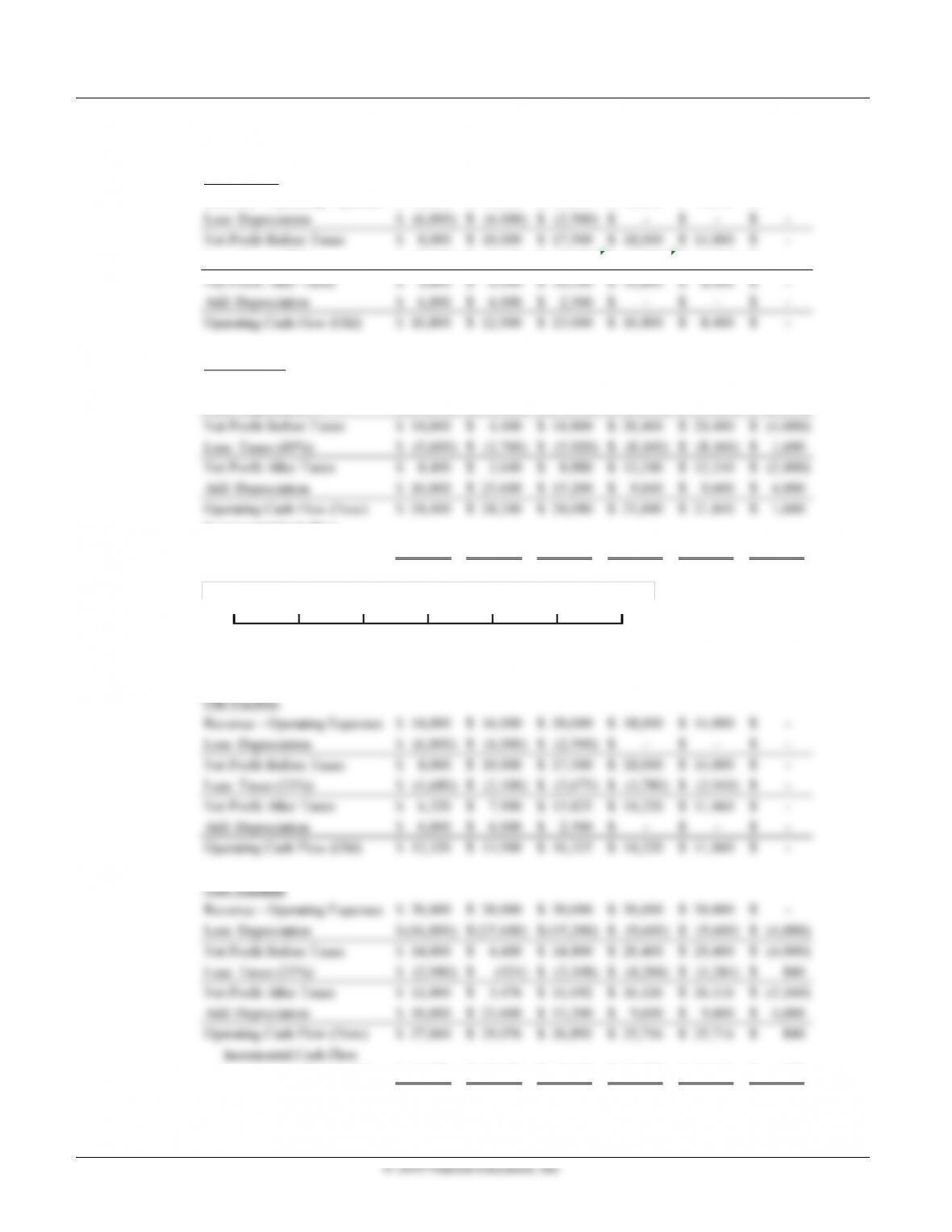

b. and c. (40% tax rate)

Year = (1) (2) (3) (4) (5) (6)

Old Machine

Revenue – Operating Expenses 14,000$ 16,000$ 20,000$ 18,000$ 14,000$ –$

Less: Taxes (40%) (3,200)$ (4,000)$ (7,000)$ (7,200)$ (5,600)$ –$

New Machine

Revenue – Operating Expenses 30,000$ 30,000$ 30,000$ 30,000$ 30,000$ –$

Less: Depreciation (16,000)$ (25,600)$ (15,200)$ (9,600)$ (9,600)$ (4,000)$

Incremental Cash Flow

(New – Old) = 13,600$ 16,240$ 11,080$ 11,040$ 13,440$ 1,600$

5601234

Cash Flows (40% Tax Rate)

-$41,200 $13,600 $16,240 $11,080 $11,040 $13,440 $1,600

b. and c. (21% tax rate)

Year = (1) (2) (3) (4) (5) (6)

(New – Old) = 14,740$ 15,176$ 10,567$ 11,496$ 14,656$ 840$

Chapter 11 Capital Budgeting Cash Flows and Risk Refinements 241

012

Cash Flows (21% Tax Rate)

-$33,505 $14,740 $15,176 $10,567 $11,496 $14,656 $840

3456

d. If the new machine is eligible for 100% bonus depreciation, then there would be a larger tax benefit

initially (the entire cost would be depreciated right away, reducing taxes) and there would be a higher tax

liability in subsequent years (because depreciation deductions would be zero after the initial cost is fully

expensed).

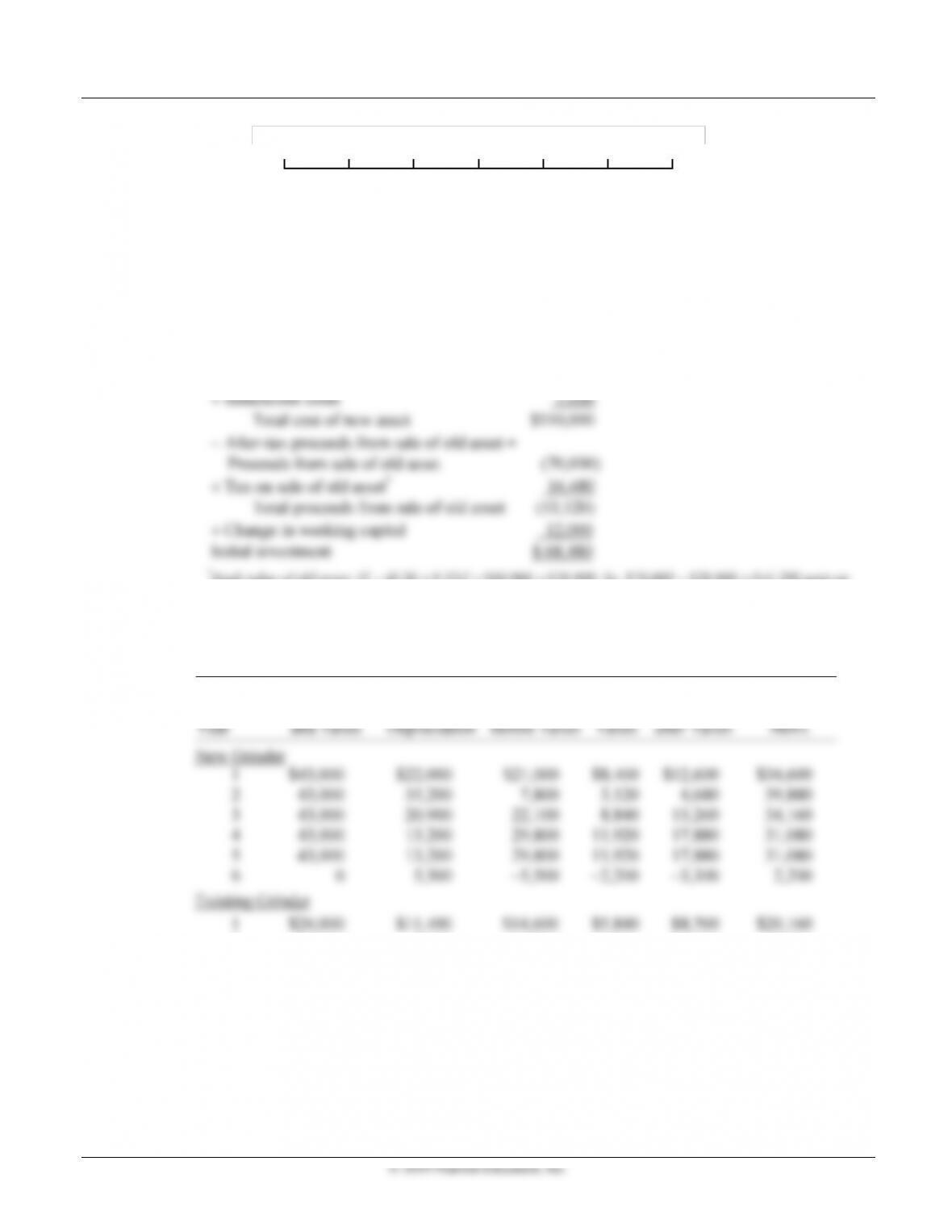

P11-17 Integrative: Determining relevant cash flows (LG 3, 4, 5, 6; Challenge)

a. Initial investment:

Installed cost of new asset =

Cost of new asset $105,000

−

(0.20

+

0.32)]

×

$60,000

=

$28,800. So, $70,000

−

$28,800

=

$41,200 gain on

asset sale. The tax consequences are: $31,200 recaptured depreciation

×

0.40

=

$12,480 plus $10,000 capital

gain

×

0.40

=.

$4,000. Hence, the total tax of sale of asset

=

$16,480.

b.

Calculation of Operating Cash Flows

Profits before

Depreciation

Net Profits

Net Profits

Operating

Cash

2 24,000 7,200 16,800 6,720 10,080 17,280

3 22,000 7,200 14,800 5,920 8,880 16,080

4 20,000 3,000 17,000 6,800 10,200 13,200

5 18,000 0 18,000 7,200 10,800 10,800

6 0 0 0 0 0 0

© 2019 Pearson Education, Inc.

After-tax proceeds from sale of new asset =

Proceeds from sale of new asset $29,000

−Tax on sale of new asset* (9,400)

Total proceeds from sale of new asset 19,600

−After-tax proceeds from sale of old asset =

P11-18 Recognizing risk (LG 1; Basic)

a. and b.

Project Risk Reason

A Low The cash flows from the project can be easily determined because this

244 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

generate a positive NPV (obtained by summing probabilities for ranges above the breakeven

range) is 30% for the standard plant but 45% for the custom plant.

e. A firm wishing to minimize the likelihood of negative NPV should opt for the standard plant

because of the lower cumulative probability cash flows will fall below the breakeven level (10%

P11-20 Basic scenario analysis (LG 2; Basic)

a. and b.

Project Life (Years) = 15

Cost of Capital = 9.30%

PROJECT A PROJECT B

Initial Investment

(Both Projects) = (12,200)$

© 2019 Pearson Education, Inc.

P11-22 Personal Finance: Impact of inflation on investments (LG 2; Easy)

a. − c.

Investment

Current

Higher

Inflation

Lower

Inflation

P11-23 Simulation (LG 2; Intermediate)

a. Ogden Corporation could use a computer simulation to generate the probability distribution for

P11-24 Risk-adjusted discount rates: Basic (LG 4; Intermediate)

a.

15%

Year Cash Flows Discounted Cash Flows Discounted Cash Flows Discounted

Project E Project F Project G

Cost of Capital (All Projects) =

© 2019 Pearson Education, Inc.

P11-25 Risk-adjusted discount rates—Tabular (LG 4; Intermediate)

a.

Project A

Project B

P11-26 Personal Finance: Mutually exclusive investment and risk (LG 4; Intermediate)

a. Number of years = 6, cost of capital = 8.5%, annual cash inflows = $3,000;

upfront project cost = $10,000.

NPV = Present value of cash inflows – Upfront project cost

Solve for PV = 13,660.76

NPV = $13,660.76 − $10,000 = $3,660.76

b. Number of years = 6, cost of capital = 10.5%, annual cash inflows = $3,800;

upfront project cost = $12,000

Solve for PV = $16,310.28

NPV = $16,310.28 − $12,000 = $4,310.28

c. Using NPV as her guide, Lara should select the second investment with the higher NPV.

d. The second investment is riskier. The higher required return implies a higher risk factor.

Chapter 11 Capital Budgeting Cash Flows and Risk Refinements 249

© 2019 Pearson Education, Inc.

License

Cash flows: project cost (CF0) = −$200,000, CF1 = $250,000, CF2 = $100,000, CF3 = $80,000,

CF4 = $60,000, CF5 = $40,000; and cost of capital = 12%.

Solve for NPV = $220,704.25

Manufacture

Cash flows: project cost (CF0) = −$450,000, CF1 = $200,000, CF2 = $250,000, CF3 = $200,000,

CF4 = $200,000, CF5 = $200,000, CF6 = $200,000.

Cost of capital = 12%. Solve for NPV = $412,141.16

Rank Alternative

1 Manufacture

2 License

3 Sell

b. Sell

Number of years= 2, cost of capital = 12%, PV = $177,869.90

Solve for ANPV (annual payment equivalent project NPV) = $105,245.28

P11-31 NPV and ANPV decisions (LG 5; Challenge)

a. – b. Unequal-Life Decisions

Annualized Net Present Value (ANPV)

Samsung Sony

© 2019 Pearson Education, Inc.

P11-32 Real options and the strategic NPV (LG 6; Intermediate)

a. Value of real options = value of abandonment + value of expansion + value of delay

Value of real options = (0.25 × $1,200) + (0.30 × $3,000) + (0.10 × $10,000)

P11-33 Capital rationing—IRR and NPV approaches (LG 6; Intermediate)

a. Rank by IRR

Project IRR Initial Investment Total Investment

F 23% $2,500,000 $2,500,000

E 22 800,000 3,300,000

A 400,000 5,000,000

C 300,000 2,000,000

B 300,000 800,000

D 100,000 1,500,000

G 100,000 1,200,000

© 2019 Pearson Education, Inc.

P11-34 Capital Rationing: NPV Approach (LG 6; Intermediate)

a. Project Initial investment NPV at 13% PV

A $300,000 $ 84,000 $384,000

B 200,000 10,000 210,000

P11-35 Ethics problem (LG 4; Challenge)

Student answers will vary. Some students might argue that companies should be held accountable for any and

a. 1. Plan X

Cash flows: CF0 (project cost) = −$2,700,000, CF1 = $470,000, CF2 = $610,000,

CF3 = $950,000, CF4 = $970,000, and CF5 = $1,500,000.