Chapter 11

Capital Budgeting Cash Flows and Risk Refinements

NOTE TO INSTRUCTORS: Shortly after the first press run for the 15th edition, Congress passed the Tax Cuts

and Jobs Act of 2017, which included changes in the corporate tax rate relevant to this chapter. In subsequent

printing runs, the text was updated to reflect the new tax law, but these updates may not appear in every student’s

copy of the text. Accordingly, solutions to problems P11-8, P11-10, P11-12, and P11-16 include answers based on

the new as well as the old corporate income tax rate.

Instructor Resources

Chapter Overview

This chapter expands upon capital-budgeting techniques presented in the previous chapter. Shareholder

wealth maximization relies upon selection of projects with positive net present values. The most important

and difficult aspect of the capital-budgeting process is developing good estimates of the relevant cash flows.

The first four sections of Chapter 11 focus on the basics of determining relevant after-tax cash flows of a

project, from the initial cash outlay to annual cash stream of costs and benefits and terminal cash flow. The

latter parts of Chapter 11 expand the discussion to include complications that often arise in real-world project

evaluation. The first complication is risk. To this point, all firm projects were assumed equally risky. In actual

practice, however, project risk can vary considerably, and project acceptance can raise or lower the firm’s

overall risk. The chapter explores three “behavioral” approaches to integrating risk into capital budgeting:

breakeven analysis, scenario analysis, and simulation. Next, the discussion turns to risk-adjusted discount

rates or RADR, a more quantitative approach to incorporating risk differences into capital budgeting. The

chapter concludes by presenting several additional refinements in capital budgeting— assessing mutually

exclusive projects with unequal lives, incorporating real options into NPV analysis, and selecting projects

under capital rationing.

Answers to Review Questions

11-1 The decision to invest (or to refrain from investing) should be based on whether the added benefits

justify the added costs. Thus, capital budgeting projects should be evaluated using incremental after-

tax cash flows. Evaluating projects in this way answers the question, how is the firm different if it

invests in this project relative to if it did not invest in the project? Only when the incremental cash

and (3) terminal cash flows. Expansion decisions are merely replacement decisions in which all cash

© 2019 Pearson Education, Inc.

11-17 RADRs are most often used in practice for two reasons: (1) financial decision makers prefer using

11-18 A comparison of NPVs of unequal-lived, mutually exclusive projects is inappropriate because it may

11-19 Real options are opportunities embedded in real assets that are part of the capital budgeting process.

Managers have the option of implementing some of these opportunities to alter the cash flow and risk

of a given project. Examples of real options include:

11-20 Strategic NPV incorporates the value of the real options associated with the project, while traditional

NPV includes only the identifiable relevant cash flows. Using strategic NPV could alter the final

11-21 Capital rationing occurs when a firm has only a limited amount of funds available for capital

11-22 The IRR and NPV approaches to capital rationing both involve ranking projects on the basis of IRRs.

Using the IRR approach, a cut-off rate and a budget constraint are imposed. The NPV first ranks

11-23 Student answers will vary because values are algorithmically generated in MyLab.

Chapter 11 Capital Budgeting Cash Flows and Risk Refinements 229

Suggested Answer to Focus on Ethics Box: “Fumbling Sunk Costs”

Recommitting to a losing project for emotional or reputational reasons can destroy shareholder wealth. What

safeguards could a firm use to remove such bias from recommitment decisions?

E11-1 Classification of project costs and cash flows

E11-2 Initial investment

E11-3 Initial investment

E11-4 Sensitivity analysis

© 2019 Pearson Education, Inc.

E11-5 Risk-adjusted discount rates

Answer:

Project Pita

RADR = 7.0% (for risk index of 6)

Project Grape Leaf

RADR = 8.0% (for risk index of 8)

E11-6 ANPV

Answer: ANPV may be obtained in two steps: (1) find NPV for projects S and T, and (ii) find the annual

Both projects have positive NPVs. If the two were independent – that is, Fiftycent had the option

of accepting projects S and T– the firm would maximize shareholder wealth by accepting both.

But, given the projects are mutually exclusive (i.e., only one may be chosen), Fiftycent should

© 2019 Pearson Education, Inc.

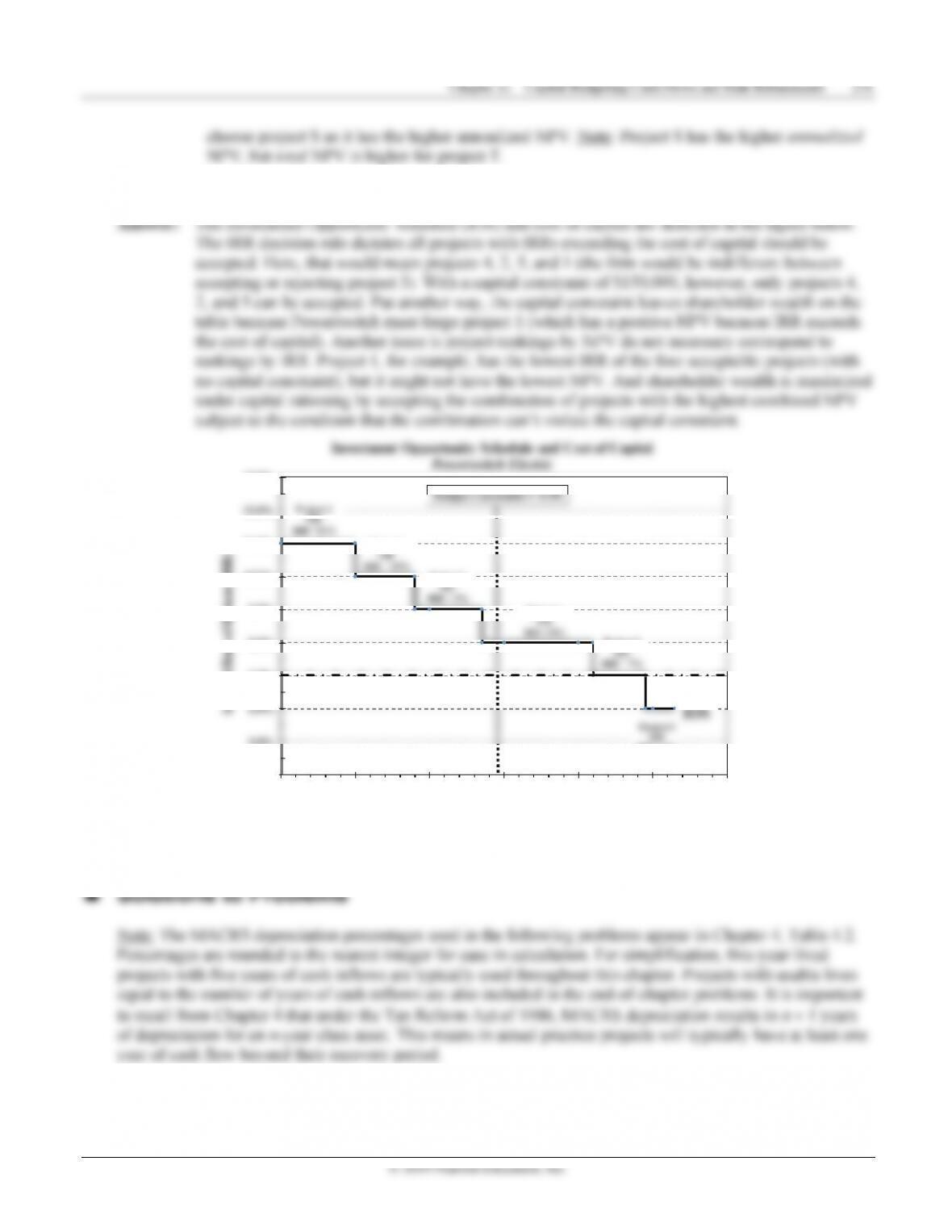

E11-7 IOS and IRR

4.0%

5.0%

8.0%

9.0%

10.0%

11.0%

$0 $50 $100 $150 $200 $250 $300

Total Investment ($000)

Project 2

Project 5

Project 1

Project 3

IRR = 6%

© 2019 Pearson Education, Inc.

P11-9 Initial investment at various sale prices (LG 3, 4; Intermediate)

(a) (b) (c) (d)

Installed cost of new asset:

Cost of new asset $24,000 $24,000 $24,000 $24,000

+ Installation cost 2,000 2,000 2,000 2,000

238 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

b. Calculation of incremental cash flows

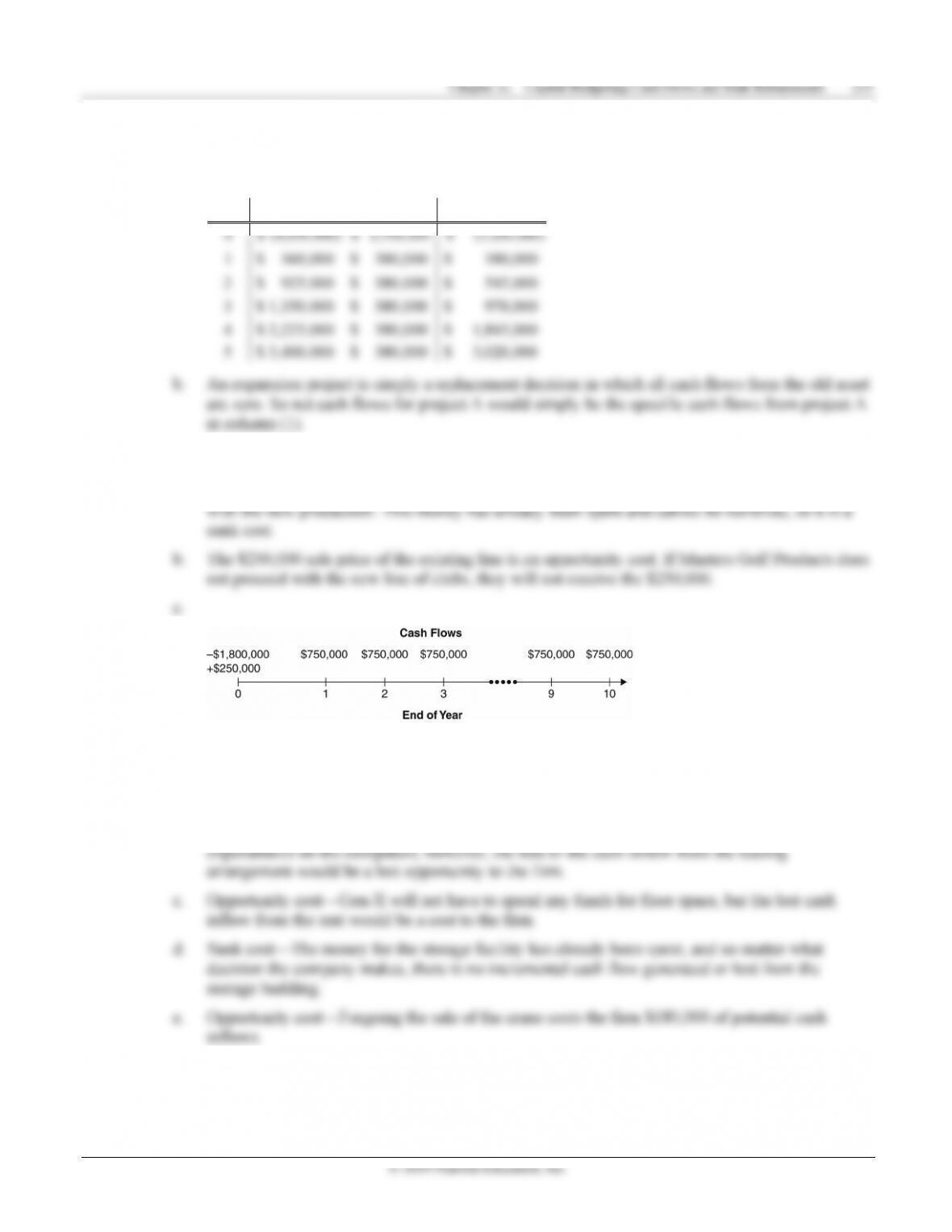

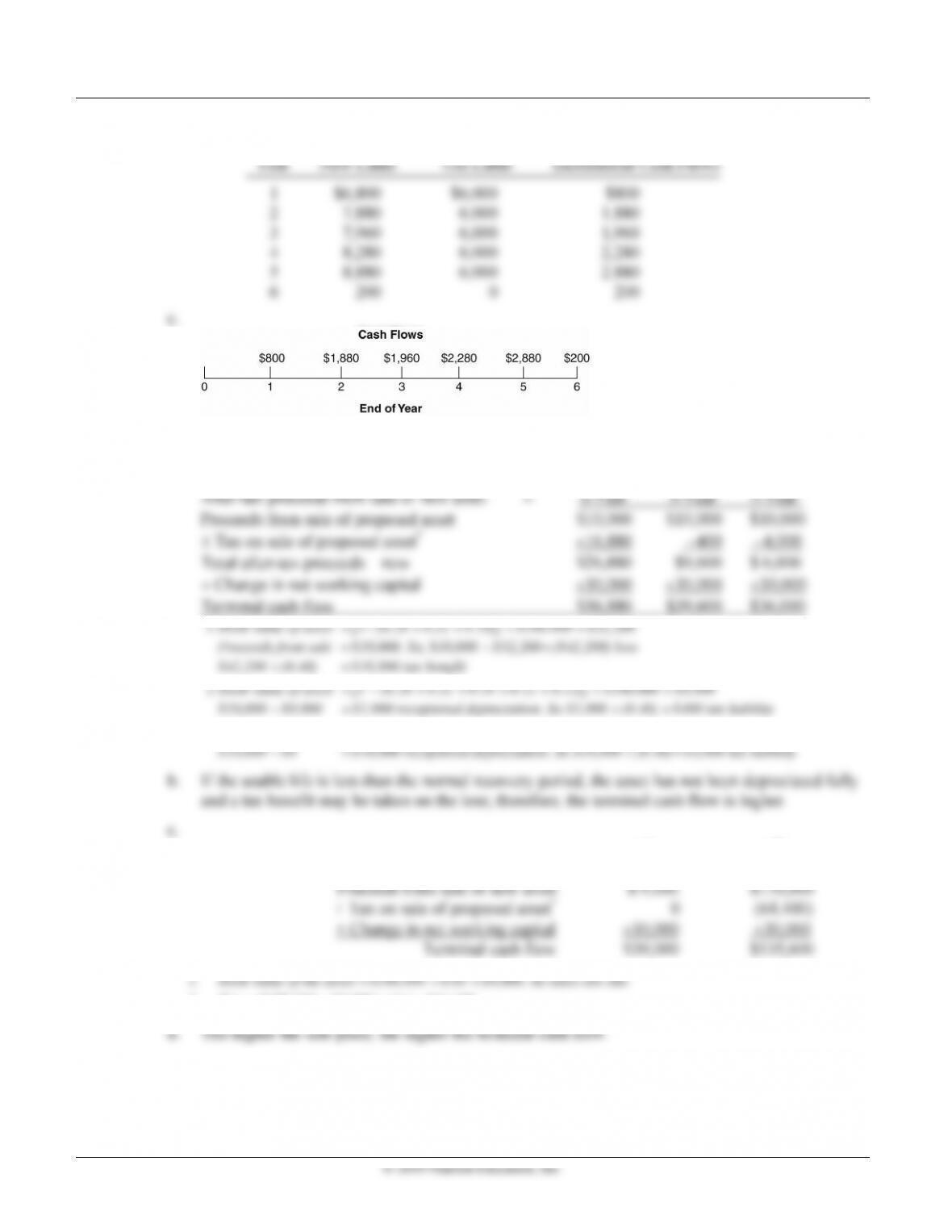

P11-14 Terminal cash flows: Various lives and sale prices (LG 6; Challenge)

a.

*1. Book value of asset

2. Book value of asset

3. Book value of asset

=

$0

(1) (2)

After-tax proceeds from sale of new asset =

2. Tax

=

($170,000

−

$9,000)

×

0.4

=

$64,400.