212 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

b. To find the number of years $10,000 would have to be received to make the project acceptable

by the IRR decision rule, use the NPER command in Excel. The proper syntax is:

c. To find the minimum cash inflows over 10 years that would make the project acceptable, use the

PMT command in Excel. The proper syntax is:

P10-19 NPV and IRR (LG 3, 4; Intermediate)

a. NPV = Present value of cash inflows – Initial investment ($18,250). In Excel, the present value of

cash inflows = PV(0.10,7,-4000) = $19,473.68. So, NPV = $19,473.68 – $18,250 = $1,223.68.

P10-20 NPV, with rankings (LG 3, 4; Intermediate)

15%

IRR = 9.70% IRR = 15.63% IRR = 19.44% IRR = 17.51%

Discount Rate =

Project A Project DProject B Project C

Note: IRR was obtained in Excel and the following syntax (cash flows arranged in the first four rows

© 2019 Pearson Education, Inc.

the IRR decision criterion indicates project A should be accepted.

Project B

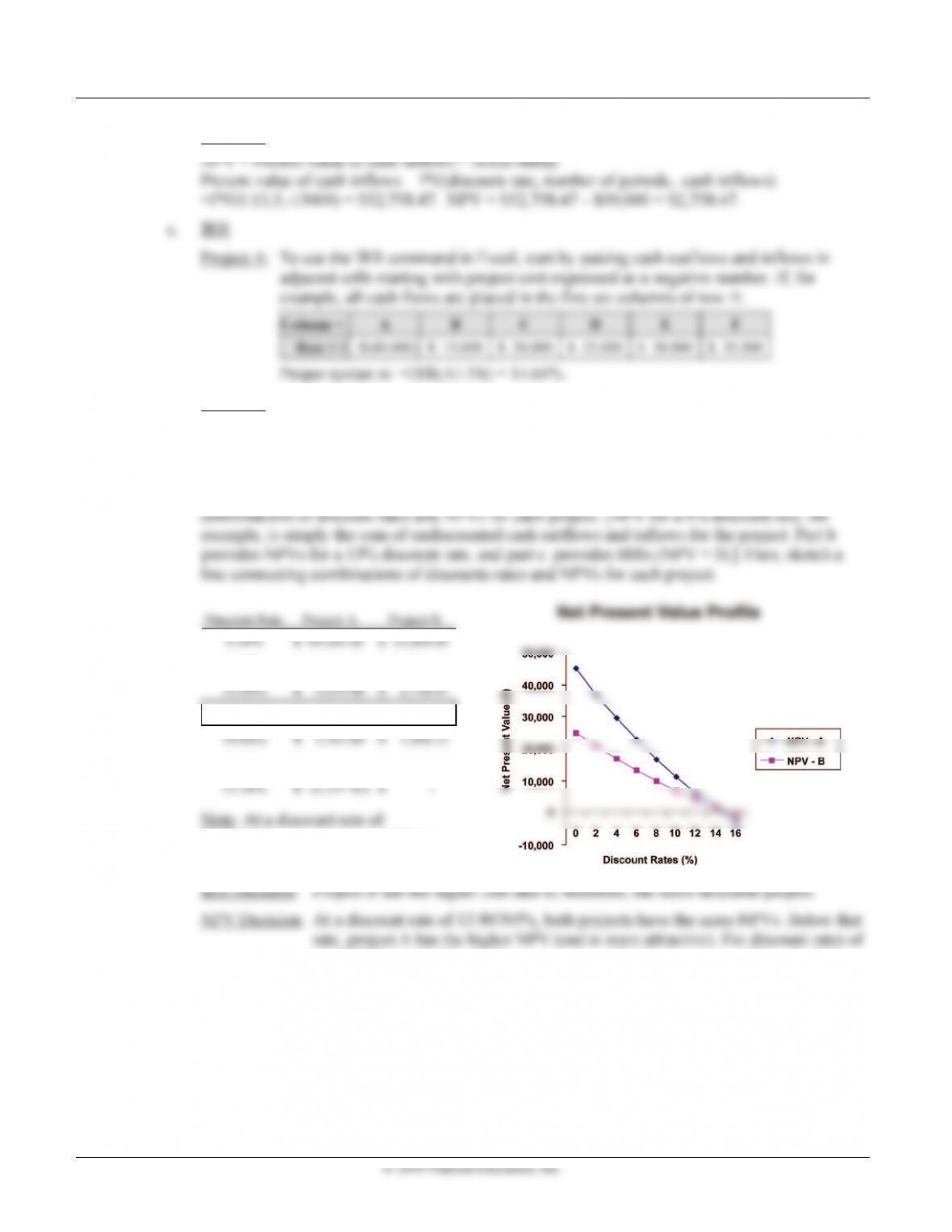

NPV: In Excel, put 40000 in A1, 35000 in A2, 30000 in A3, 10000 in A4, and 5000 in A5.

Then, use the NPV command to obtain the present value of these inflows; proper syntax:

=NPV(discount rate,A1:A5) = NPV(0.12,A1:A5) = $94,161.79 . Now, to obtain project

17.75%. Given these points, the NPV profiles for project A and B may be drawn:

Note the two projects have NPVs

16.06%, both projects are profitable, but project B has a slightly higher NPV (and is, therefore,

more desirable). For discount rates below 14.777%, project A has the higher NPV (and is,

therefore, preferred).

Chapter 10 Capital Budgeting Techniques 217

© 2019 Pearson Education, Inc.

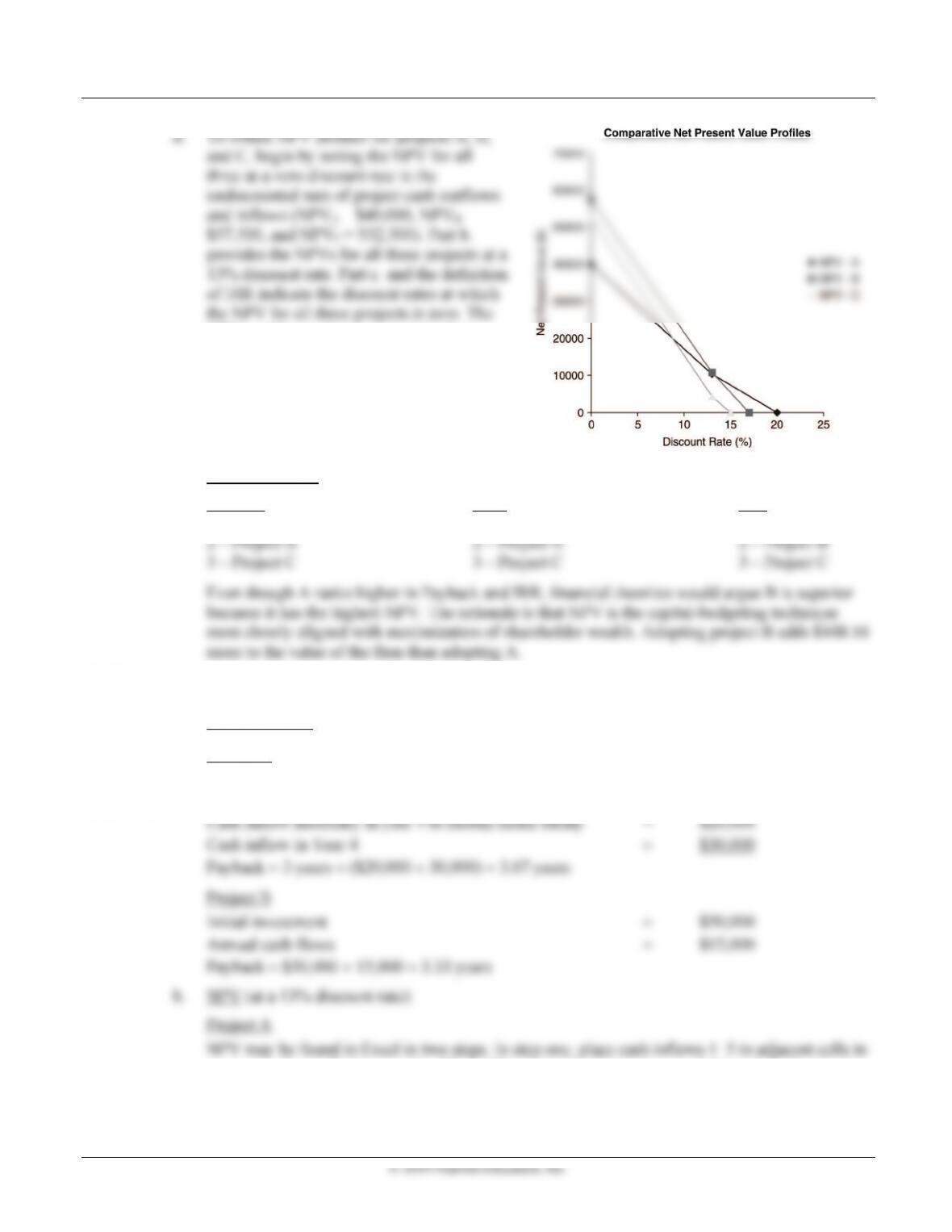

d. To obtain NPV profiles for projects A, B,

and C, begin by noting the NPV for all

three at a zero discount rate is the

undiscounted sum of project cash outflows

and inflows (NPVA = $40,000, NPVB =

$57,500, and NPVC = $52,500). Part b.

provides the NPVs for all three projects at a

13% discount rate. Part c. and the definition

of IRR indicate the discount rates at which

the NPV for all three projects is zero. The

NPV profiles are lines connecting these

three points for each project.

e. Project rankings:

Payback:

1 – Project A

NPV:

1 – Project B

IRR:

1 – Project A

P10-25 All techniques with NPV profile—mutually exclusive projects (LG 2, 3, 4, 5, 6; Challenge)

a. Payback period:

Project A

Initial investment = $80,000

Cash inflows in year 1 + year 2 + year 3 = $60,000

a row or column. If, for example, CF1 to CF5 appear in column A, rows 1 through 5, the present

value of cash inflows = NPV(A1:A5) = $83,659.68. In step two, subtract project cost from the

present value of cash inflows to find project NPV: NPVA = $83,659.68 – $80,000 = $3,659.68.

218 Zutter/Smart • Principles of Managerial Finance Brief, Eighth Edition

Project B

Project B: To use the IRR command in Excel, start by putting cash outflows and inflows in

adjacent cells starting with project cost expressed as a negative number. If, for

example, all cash flows are placed in the first six columns of row A:

Proper syntax is: =IRR(A1:F6) = 15.24%.

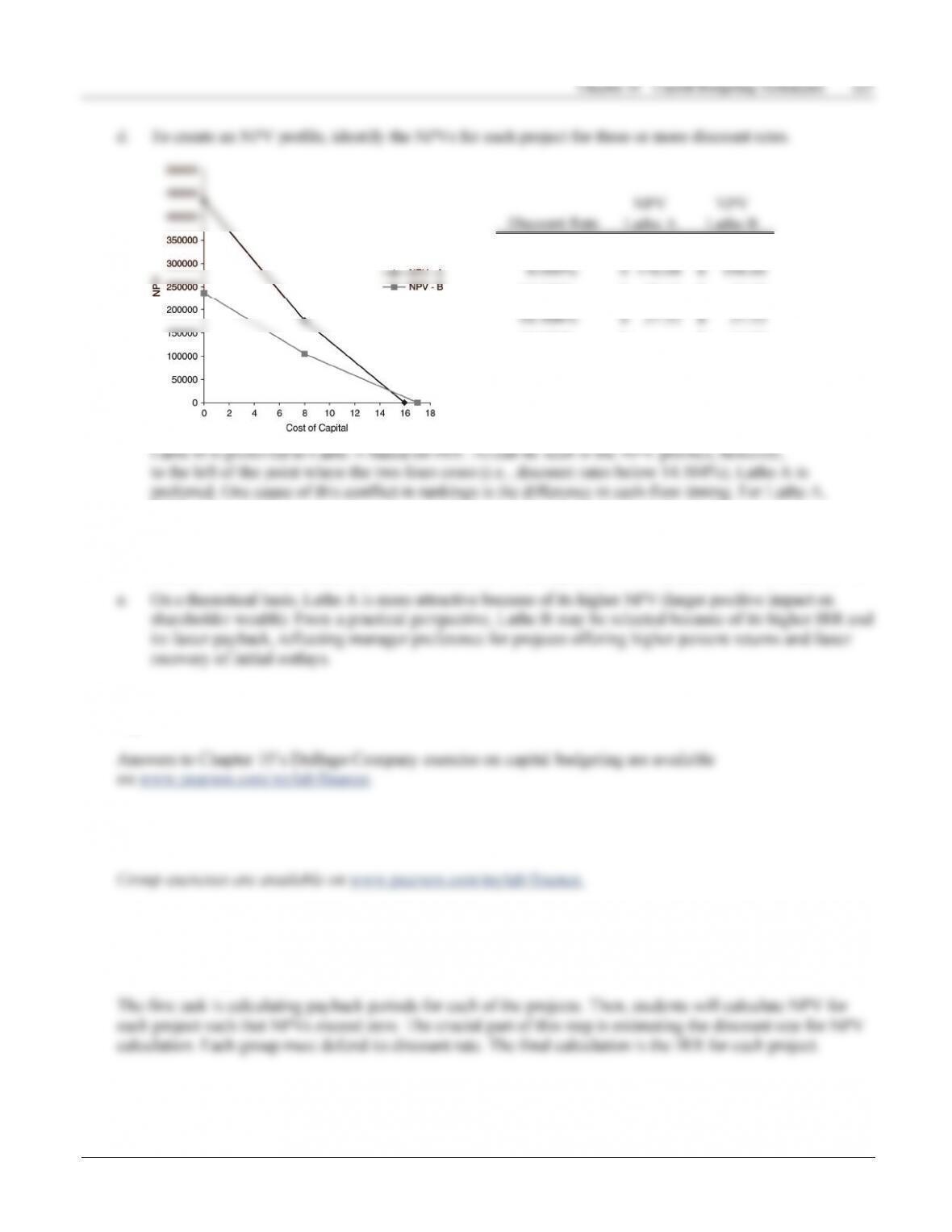

d. To find the NPV profiles for projects A and B, begin by generating a set of points representing

5.00% 26,126.73$ 14,942.15$

13.86765% 1,660.45$ 1,660.45$

14.61% –$ 750.15$

13.86765%, projects A and B have

the same NPV ($1,660.45)

13.86765% to 14.61%, both projects are profitable, but project B has the higher

NPV and is more attractive. Project A is more attractive at lower interest rates

because a greater percentage of its cash flows occur in later years.

© 2019 Pearson Education, Inc.

P10-26 Integrative—Multiple IRRs (LG 6; Basic)

a. Calculating the payback period for this project is difficult because of its unusual pattern of cash

flows. For example, there is no initial cash outflow; the cash flow in year 0 is an inflow. Outflows

occur in years 1 and 3. After 2 years, the project’s outflows are greater than its inflows, but that

reverses in year 3. Oscillating cash flows (positive-negative-positive-negative-positive)

NPV (13%) 1 2

IRR 2 1

© 2019 Pearson Education, Inc.

IRR= 15.95% IRR= 17.34%

NPV and IRR

The NPV decision criterion indicates both lathes are acceptable because NPVA and NPVB > 0. Lathe A

ranks ahead of B because of its larger NPV. IRR is the discount rate that makes project NPV = 0 for the

N

PV $58.13 $43.48

IRR 15.95% 17.34%

Rank 2 1

be excluded from the ranking of admissible

© 2019 Pearson Education, Inc.

434.00$ 237.00$

58.13$ 43.48$

–$ 13.08$

(25.07)$ –$

0.000%

15.950%

17.340%

13.000%

56.5% of cash inflows occur in years 4 and 5, compared with 49.1% for Lathe B. Changes in the

discount rate, other things equal, have a larger impact on the NPVs of projects with greater cash flows in

later years. For example, at a discount rate of 15.95%, NPVA = $0 and NPVB = $13.08. But as the rate

falls, NPVA rises faster than NPVB. As a result, NPVs are equal at 14.504%, and NPVA > NPVB at 13%.

Spreadsheet Exercise

Group Exercise

This assignment builds on the long-term investment projects in the previous chapter. Because students were

required to estimate relevant cash flows before reading this chapter, some numbers may have to be altered to

ensure each project has sensible payback periods. Allowing students to revisit previous estimates should make

their numbers more realistic and easier to work with.

© 2019 Pearson Education, Inc.