Part 1

Introduction to Managerial Finance

Chapters in This Part

Chapter 1 The Role of Managerial Finance

Chapter 2 The Financial Market Environment

Chapter 1

The Role of Managerial Finance

Instructor’s Resources

Chapter Overview

This chapter introduces the field of finance through building-block terms and concepts. The discussion starts by

defining “firm” and stressing its principal goal—maximizing shareholder wealth. The importance of focusing on

shareholders rather than stakeholders broadly and stock price rather than current profits is explained. The

managerial-finance function is then described and differentiated from economics and accounting, with special

attention to the role ethics play in a financial manager’s efforts to maximize the firm’s stock price. Next, the

three basic legal forms of business organization (sole proprietorship, partnership, and corporation) are

discussed and the strengths and weaknesses of each form noted. The chapter concludes with an exploration of

the agency problem—the conflict arising when the managers and owners of the firm are not the same

people—and the private- and public-sector tools available to focus managerial attention on shareholder

NOTE: After this text went to press, Congress passed the Tax Cuts and Job Act of 2017, which dramatically

changed both corporate and personal tax rates. The first printing of this text did not reflect these tax changes,

but subsequent print runs do. For tax-related problems below, we provide solutions under both the old and the

new tax law. Of particular relevance to this chapter, the corporate tax rate is now a flat 21%. Individuals still

face a progressive rate schedule, so there is still value in explaining the progressive nature of the old corporate

structure as well as the difference between marginal and average tax rates (which are essentially the same

under a flat-rate structure). The change in the corporate tax code—in particular the introduction of a lower,

flatter rate—can serve as a useful discussion point throughout this text. For example, instructors may wish to

discuss the impact of a lower tax rate on the NPV of investments or a firm’s optimal capital structure.

Answers to Review Questions

1-1. The goal of a firm, and therefore of all financial managers, is maximizing shareholder wealth. The

proper metric for this goal is the price of the firm’s stock. Other things equal, an increasing price per

© 2019 Pearson Education, Inc.

E1-5. Agency costs (LG 6)

E1-6. Corporate tax liability (LG 5)

P1-1. Liability comparisons (LG 5; Basic)

a. Ms. Harper has unlimited personal liability, so she is liable for the firm’s $60,000 in unpaid debts.

© 2019 Pearson Education, Inc.

P1-5. Identifying agency problems, costs, and resolutions (LG 6; Intermediate)

a. The agency cost is wages paid to an idle employee whose responsibilities must be covered by

someone else. One solution is a time clock everyone must punch when arriving for work, take a

lunchbreak, and leave for the day. A punch clock would reduce agency costs by: (1) prompting

the receptionist to return from lunch on time or (2) reduce wages paid for unproductive time.

P1-6 Corporate taxes (LG 5; Basic)

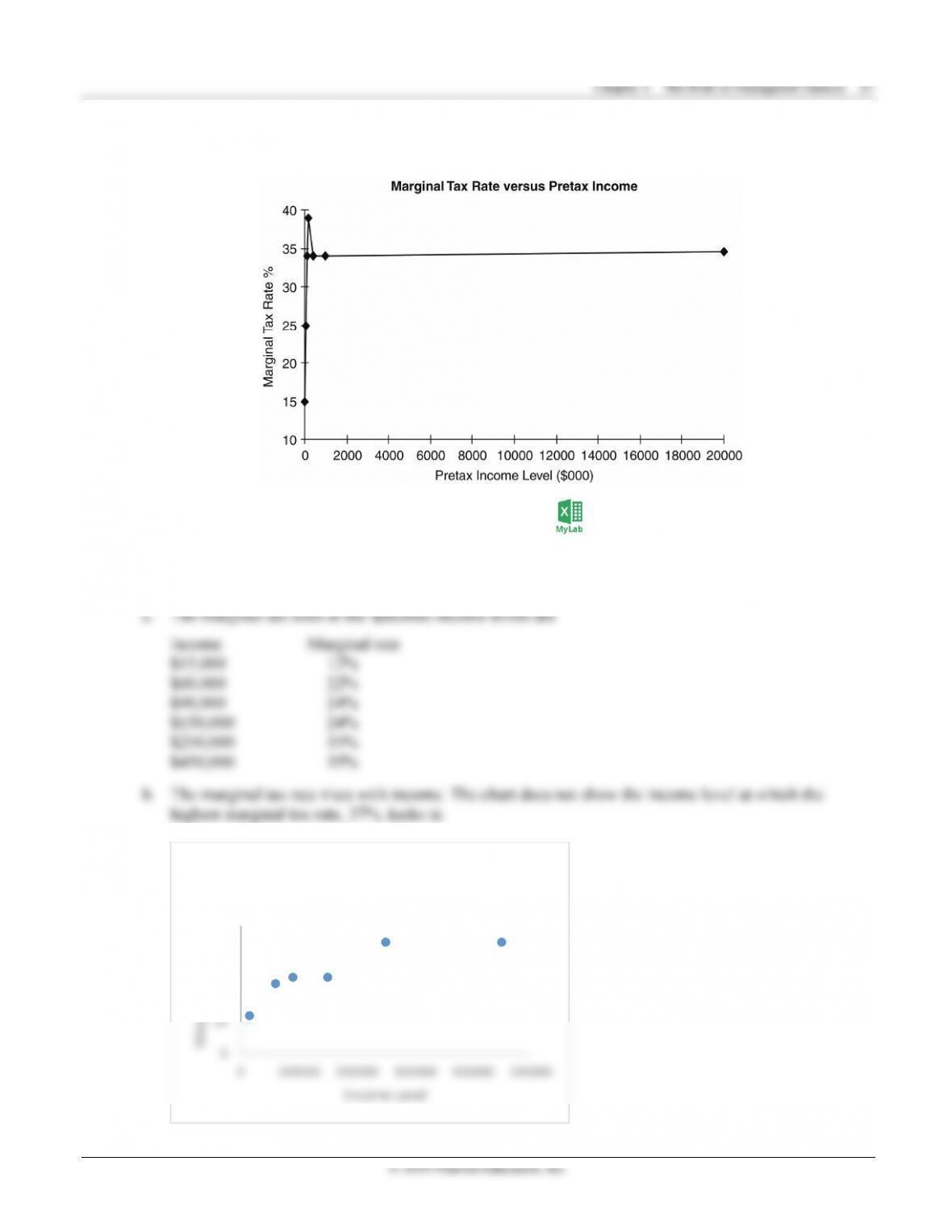

a. Firm’s tax liability on $92,500 using Table 1.2:

Total taxes due = $13,750 + [0.34 × ($92,500 – $75,000)] = $13,750 + $5,950 = $19,700

For students with the text updated with the latest tax information, the taxes due would be 21% ×

© 2019 Pearson Education, Inc.

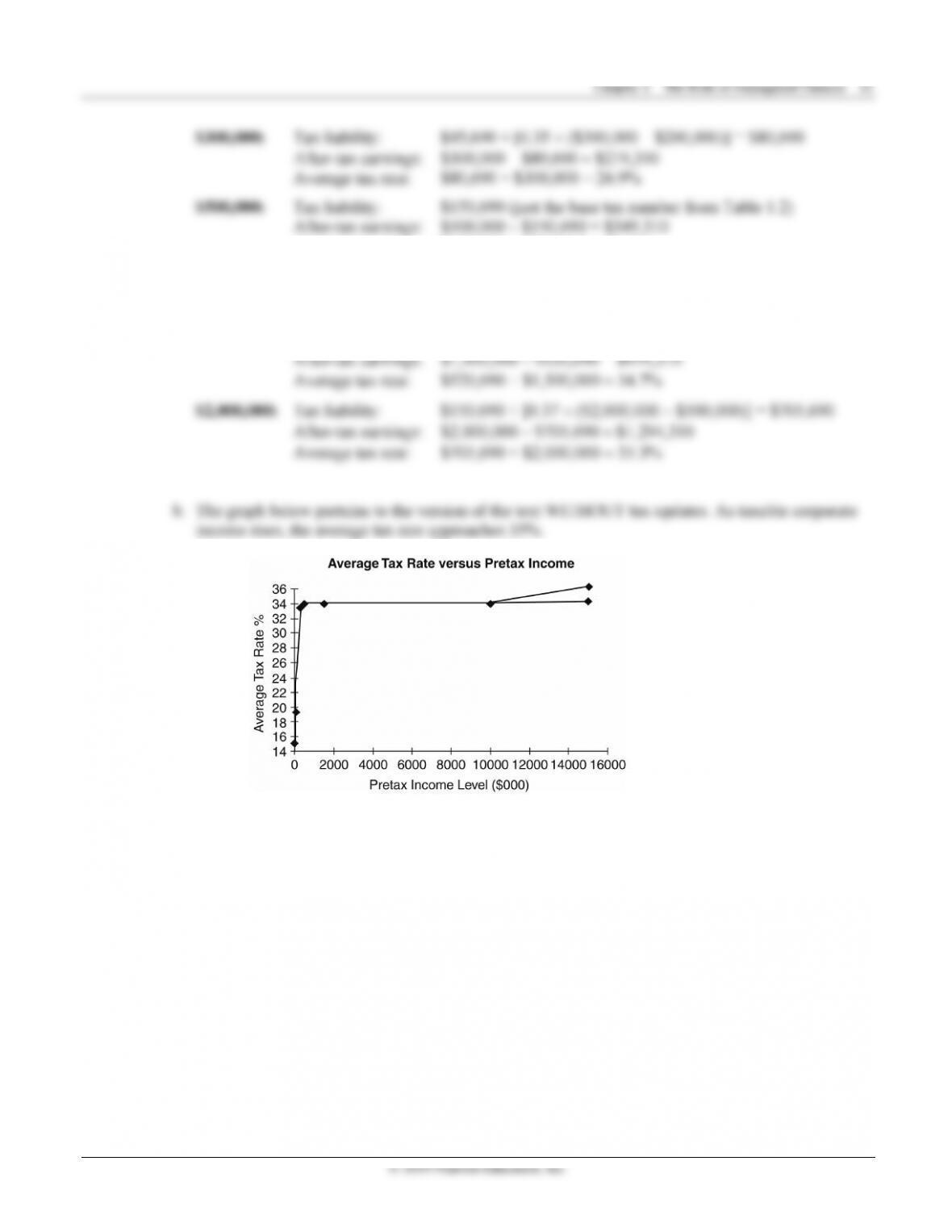

Average tax rate: $150,690 ÷ $500,000 = 30.1%

$1,000,000: Tax liability: $150,690 + [0.37 × ($1,000,000 – $500,000)] = $335,690

After-tax earnings: $1,000,000 – $335,690 = $664,310

Average tax rate: $335,690 ÷ $1,000,000 = 33.6%

$1,500,000: Tax liability: $150,690 + [0.37 × ($1,500,000 – $500,000)] = $520,690

© 2019 Pearson Education, Inc.

P1-10 Interest vs. dividend expense (LG 6; Intermediate)

The following answer is appropriate for the original printing of the text with old tax information.

Answers for the printing with updated tax information follow.

a. EBIT $50,000

Less: Interest expense 12,000

P1-11. Reducing tax exposure—Hemingway Corporation (LG 5; Intermediate)

a. With pre-tax income currently of $200,000, Hemingway’s current tax liability (using the tax rates

in Table 1.2) is $22,250 + 0.39 × ($200,000 – $100,000) = $22,250 + $39,000 = $61,250. Or using

the newer tax code reflecting the Tax Cuts and Jobs Act, the company faces a 21% flat tax, so its

tax bill is currently 21% × $200,000 = $42,000.

© 2019 Pearson Education, Inc.

$280,000. Taxes owed will equal $22,250 + 0.39 × (280,000 – $100,000) = $92,450. The new average

tax rate will be $92,450 / $280,000 = 0.330 or 33.0%. The average tax rate is higher than in part b,

again because added income from expansion is taxed at the marginal rate of 39%. However, the

average tax rate here is lower than in part c because Hemingway’s interest payments reduce its overall

tax bill and, hence, its average tax rate. Put another way, with debt financing, less of the additional

P1-12. Ethics problem (LG 2)

Maximizing shareholder wealth subject to “ethical constraints” means pursuing all opportunities to

boost stock price consistent with community ethical norms and applicable federal/state laws.

“Community ethical norms” refers to prevailing standards about right and wrong. Consistent,

knowing violation of such norms can reduce shareholder wealth by prompting stakeholder backlash

and punitive government action. For example, in 2017 sexual mistreatment of women in the

workplace became an overriding concern for many Americans. Firms with executives guilty of

harassing female subordinates were vulnerable to attacks by customers, employees, lawyers, the

media, and elected officials. If a firm knew an executive had a history of inappropriate behavior and

took no action (believing, perhaps, the executive was irreplaceable), the backlash was even worse

when the story inevitably came out. As a result, many high-profile executives were fired to head off

customer boycotts, employee defections, hostile-workplace lawsuits, and political retaliation (such as

Congressional hearings or targeted legislation) that could hammer the firm’s stock price. Similarly,

abiding by applicable federal and state laws protects shareholders wealth from punitive legal action

against the firm and its executives as well as backlash from stakeholders and elected officials.

Case