7.8 Tralor Corporation manufactures and sells several different lines of small electric

components. Its internal audit department completed an audit of its expenditure

processes. Part of the audit involved a review of the internal accounting controls for

payables, including the controls over the authorization of transactions, accounting for

transactions, and the protection of assets. The auditors noted the following items:

1 Routine purchases are initiated by inventory control notifying the purchasing

2 For efficiency and effectiveness, purchases of specialized goods and services are

3 Accounts payable maintains a list of employees who have purchase order approval

4 Prenumbered vendor invoices are recorded in an invoice register that indicates the

5 Prior to making entries in accounting records, the accounts payable clerk checks

6 All approved invoices are filed alphabetically. Invoices are paid on the 5th and

7 The treasurer signs the checks and cancels the supporting documents. An original

8 Prenumbered blank checks are kept in a locked safe accessible only to the cash

Review the eight items listed and decide whether they represent an internal control

strength or weakness

a For each internal control strength you identified, explain how the procedure

helps achieve good authorization, accounting, or asset protection control.

b For each internal control weakness you identified, explain why it is a weakness

and recommend a way to correct the weakness

Adapted from the CMA Examination

# a. Why it is a strength b. Why it is a weakness b. Recommendation to

correct weakness

1 User authorization means the

A purchase order copy should not be used

The receiving report is prepared

2

4 Numbering and recording

control over invoices and

helps ensure their recording in

accounting records.

Failure to follow-up on open invoices

lack of follow-up.

A periodic review and

5 The transaction audit helps

minimize errors and helps

ensure that only properly

authorized transactions are

recorded.

7 Proper separation of duties

exists

8 Proper protection of blank

checks (locked safe only

Unlimited access to cash disbursement

documents (other than blank checks)

or a loss of assets – as well as improper or

inaccurate accounting or destruction of

records.

A policy limiting access to and

physical protection of accounts

7 Lancaster Company makes electrical parts for contractors and home improvement

retail stores. After their annual audit, Lancaster’s auditors commented on the

following items regarding internal controls over equipment:

1 The operations department that needs the equipment normally initiates a

2 When the purchasing department receives either an inventory or an equipment

3 When equipment arrives, the user department installs it. The property, plant, and

equipment control accounts are supported by schedules organized by year of

4 When equipment is retired, the plant manager notifies the accounting department

5 There has been no reconciliation since the company began operations between the

Weakness Recommendation

1 No authorization form describing the

2 Equipment purchases over a certain

The purchase requisition should include an item

and management approval.

3 Purchase requisitions for fixed assets

4 No mention of pre-numbered purchase

requisitions or purchase orders.

Authorized equipment acquisitions should be processed

Pre-numbered purchase requisitions and purchase orders

should be used so that all documents can be accounted for.

5 Plant engineering is not inspecting

6 Equipment is not tagged and controlled

Machinery and equipment should be subject to normal

All new machinery and equipment should be assigned a

control number and tagged at the time of receipt.

Machinery and equipment accounting procedures,

9 Equipment retirement schedules are

Equipment retirement schedules, which provide

Periodically, a physical inventory of fixed assets should be

7.10 The Langston Recreational Company (LRC) manufactures ice skates for racing,

figure skating, and hockey. The company is located in Kearns, Utah, so it can be

close to the Olympic Ice Shield, where many Olympic speed skaters train.

Given the precision required to make skates, tracking manufacturing costs is very

important to management so it can price the skates appropriately. To capture and

collect manufacturing costs, the company acquired an automated cost accounting

system from a national vendor. The vendor provides support, maintenance, and data

and program backup service for LRC’s system.

LRC operates one shift, five days a week. All manufacturing data are collected and

recorded by Saturday evening so that the prior week’s production data can be

processed. One of management’s primary concerns is how the actual manufacturing

process costs compare with planned or standard manufacturing process costs. As a

result, the cost accounting system produces a report that compares actual costs with

standards costs and provides the difference, or variance. Management focuses on

significant variances as one means of controlling the manufacturing processes and

calculating bonuses.

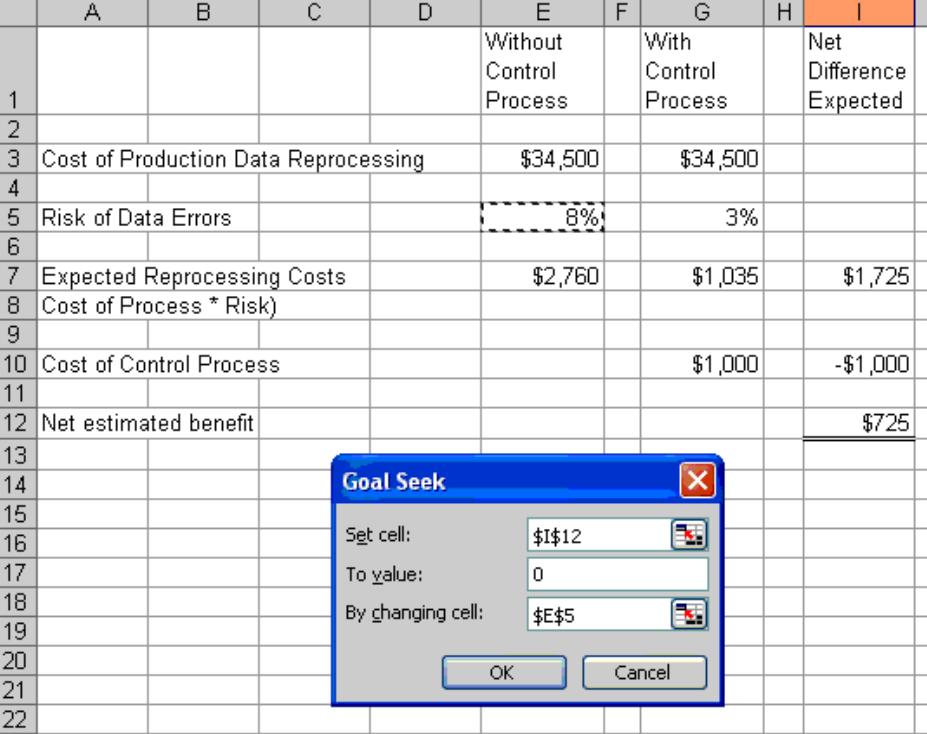

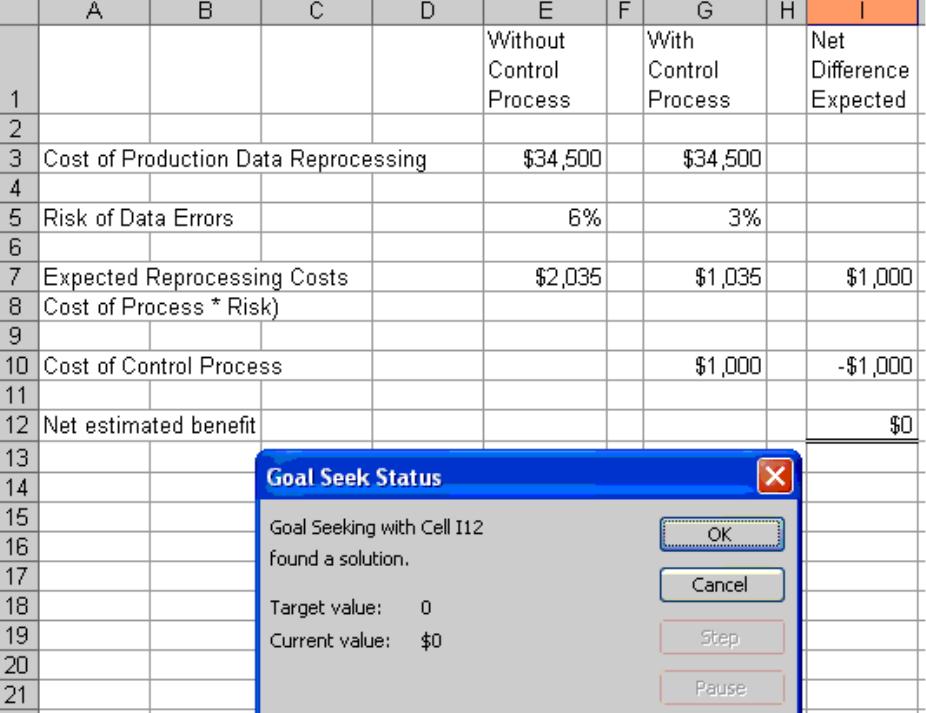

Occasionally, errors occur in processing a week’s production cost data, which

requires the entire week’s cost data to be reprocessed at a cost of $34,500. The

current risk of error without any control procedures is 8%. LRC’s management is

currently considering a set of cost accounting control procedures that is estimated to

reduce the risk of the data errors from 8% to 3%. This data validation control

procedure is projected to cost $1,000 per week.

a. Perform a cost/benefit analysis of the data-validation control procedures.

Without

Control

Process

With

Control

Process

Net

Difference

Expected

Cost of Production Data Reprocessing $34,500 $34,500

Risk of Data

b. Based on your analysis, make a recommendation to management regarding the

control procedure.

c The current risk of data errors without any control procedures is estimated to be

8%. The data control validation procedure costs $1,000 and reduces the risk to

3%. At some point between 8% and 3% is a point of indifference—that is, Cost of

reprocessing the data without controls = Cost of processing the data with the

controls + Cost of controls. Use a spreadsheet application such as Excel Goal Seek

to find the solution

Solution: 6%

Without

Control

Process

With

Control

Process

Net

Difference

Expected

Goal Seek Setup:

Goal Seek Solved:

7.11 Spring Water Spa Company is a 15-store chain in the Midwest that sells hot tubs,

supplies, and accessories. Each store has a full-time, salaried manager and an

assistant manager. The sales personnel are paid an hourly wage and a commission

based on sales volume.

The company uses electronic cash registers to record each transaction. The

salesperson enters his or her employee number at the beginning of his/her shift. For

each sale, the salesperson rings up the order by scanning the item’s bar code, which

then displays the item’s description, unit price, and quantity (each item must be

scanned). The cash register automatically assigns a consecutive number to each

transaction. The cash register prints a sales receipt that shows the total, any discounts,

the sales tax, and the grand total.

The salesperson collects payment from the customer, gives the receipt to the customer,

and either directs the customer to the warehouse to obtain the items purchased or

makes arrangements with the shipping department for delivery. The salesperson is

responsible for using the system to determine whether credit card sales are approved

and for approving both credit sales and sales paid by check. Sales returns are handled

in exactly the reverse manner, with the salesperson issuing a return slip when

necessary.

At the end of each day, the cash registers print a sequentially ordered list of sales

receipts and provide totals for cash, credit card, and check sales, as well as cash and

credit card returns. The assistant manager reconciles these totals to the cash register

tapes, cash in the cash register, the total of the consecutively numbered sales invoices,

and the return slips. The assistant manager prepares a daily reconciled report for the

store manager’s review.

Cash sales, check sales, and credit card sales are reviewed by the manager, who

prepares the daily bank deposit. The manager physically makes the deposit at the

bank and files the validated deposit slip. At the end of the month, the manager

performs the bank reconciliation. The cash register tapes, sales invoices, return slips,

and reconciled report are mailed daily to corporate headquarters to be processed with

files from all the other stores. Corporate headquarters returns a weekly Sales and

Commission Activity Report to each store manager for review.

Please respond to the following questions about Spring Water Spa Company’s

operations: (CMA exam adapted)

a. The fourth component of the COSO ERM framework is risk assessment. What

risk(s) does Spring Water face?