CHAPTER 2

OVERVIEW OF TRANSACTION PROCESSING

AND ENTERPRISE RESOURCE PLANNING SYSTEMS

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

2.1 Table 2-1 lists some of the documents used in the revenue, expenditure, and human

resources cycle. What kinds of input or output documents or forms would you find in

the production (also referred to as the conversion cycle)?

Students will not know the names of the documents but they should be able to identify the

tasks about which information needs to be gathered. Here are some of those tasks

Requests for items to be produced

Documents to plan production

Schedule of items to be produced

2-1

©2018 Pearson Education, Inc.

Ch. 2: Overview of Business Processes

2.2 With respect to the data processing cycle, explain the phrase “garbage in, garbage

out.” How can you prevent this from happening?

When garbage, defined as errors, is allowed into a system that error is processed and the

resultant data stored. The stored data at some point will become output. Thus, the phrase

garbage in, garbage out. Data errors are even more problematic in ERP systems because the

error can affect many more applications than an error in a non-integrated database.

Companies go to great lengths to make sure that errors are not entered into a system. To

prevent data input errors:

Data captured on source documents and keyed into the system are edited by the

Companies use turnaround documents to avoid the keying process.

Companies use source data automation devices to capture data electronically to avoid

Well-designed documents and screens improve accuracy and completeness by

Data input screens are preformatted to list all the data the user needs to enter.

2-2

©2018 Pearson Education, Inc.

Accounting Information Systems

2.3 What kinds of documents are most likely to be turnaround documents? Do an

internet search to find the answer and to find example turnaround documents.

Documents that are commonly used as turnaround documents include the following:

Utility bills

Meter cards for collecting readings from gas meters, photocopiers, water meters etc

2-3

©2018 Pearson Education, Inc.

Ch. 2: Overview of Business Processes

2.4 The data processing cycle in Figure 2-1 is an example of a basic process found

throughout nature. Relate the basic input/process/store/output model to the functions

of the human body.

There are a number of ways to relate the input/process/store/output model to the human

body. Here are a few of them

Brain. We read, see, hear, and feel things. We process that input in order to understand

2.5 Some individuals argue that accountants should focus on producing financial

statements and leave the design and production of managerial reports to information

systems specialists. What are the advantages and disadvantages of following this

advice? To what extent should accountants be involved in producing reports that

include more than just financial measures of performance? Why?

There are no advantages to accountants focusing only on financial information. Both the

accountant and the organization would suffer if this occurred. Moreover, it would be very

2-4

©2018 Pearson Education, Inc.

Accounting Information Systems

SUGGESTED ANSWERS TO THE PROBLEMS

2.1 The chart of accounts must be tailored to an organization’s specific needs. Discuss

how the chart of accounts for the following organizations would differ from the one

presented for S&S in Table 2-4.

Some of the changes in the chart of accounts for each type of entity include the following:

a. University

No equity or summary drawing accounts. Instead, have a fund balances section

for each type of fund.

Several types of funds, with a separate chart of accounts for each. The current

b. Bank

Loans to customers would be an asset, some current others noncurrent, depending

upon the length of the loan.

c. Government Unit

No equity or summary drawing accounts. Instead, have fund balances.

2-5

©2018 Pearson Education, Inc.

Ch. 2: Overview of Business Processes

d. Manufacturing Company

Several types of inventory accounts (raw materials, work-in-process, and finished

e. Expansion of S&S

Additional digits to code:

2-6

©2018 Pearson Education, Inc.

Accounting Information Systems

2.2 Design a chart of accounts for SDC. Explain how you structured the chart of accounts

to meet the company’s needs and operating characteristics. Keep total account code

length to a minimum, while still satisfying all of Mace’s desires.

(Adapted from the CMA Exam)

A six-digit code (represented by letters ABCDEF) is sufficient to meet SDC’s needs:

A This digit identifies the 4 divisions plus the corporate office

B This digit represents major account types (asset, liability, equity, revenue,

2-7

©2018 Pearson Education, Inc.

Ch. 2: Overview of Business Processes

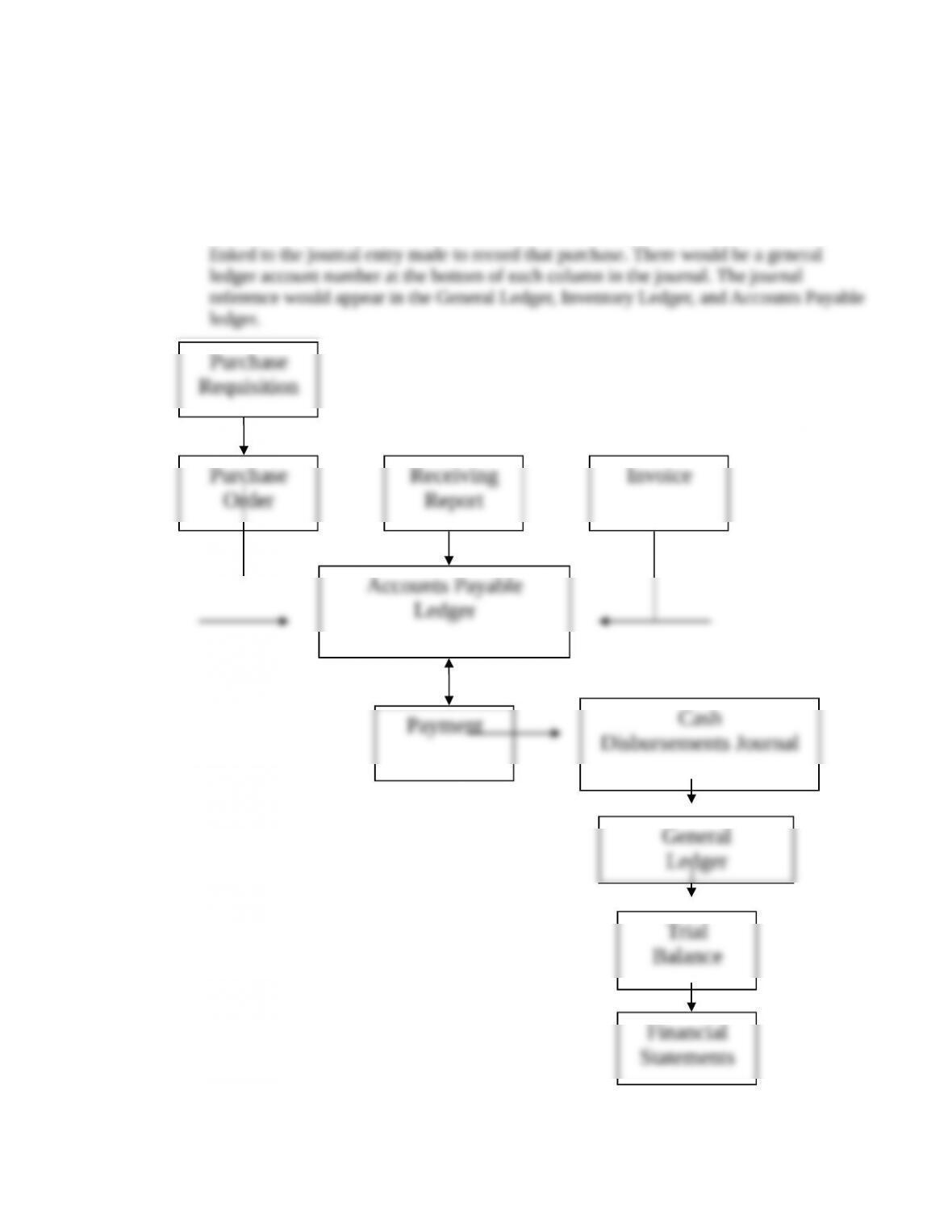

2.3 An audit trail enables a person to trace a source document to its ultimate effect on the

financial statements or work back from amounts in the financial statements to source

documents. Describe in detail the audit trail for the following:

a. The audit trail for inventory purchases includes linking purchase requisitions, purchase

orders, and receiving reports to vendor invoices for payment. All these documents

would be linked to the check or EFT transaction used to pay for an invoice and

recorded in the Cash Disbursements Journal. In addition, these documents would all be

2-8

©2018 Pearson Education, Inc.

Payment

Financial

Statements

Trial

Balance

Purchase

Requisition

General

Ledger

Cash

Disbursements Journal

Accounting Information Systems

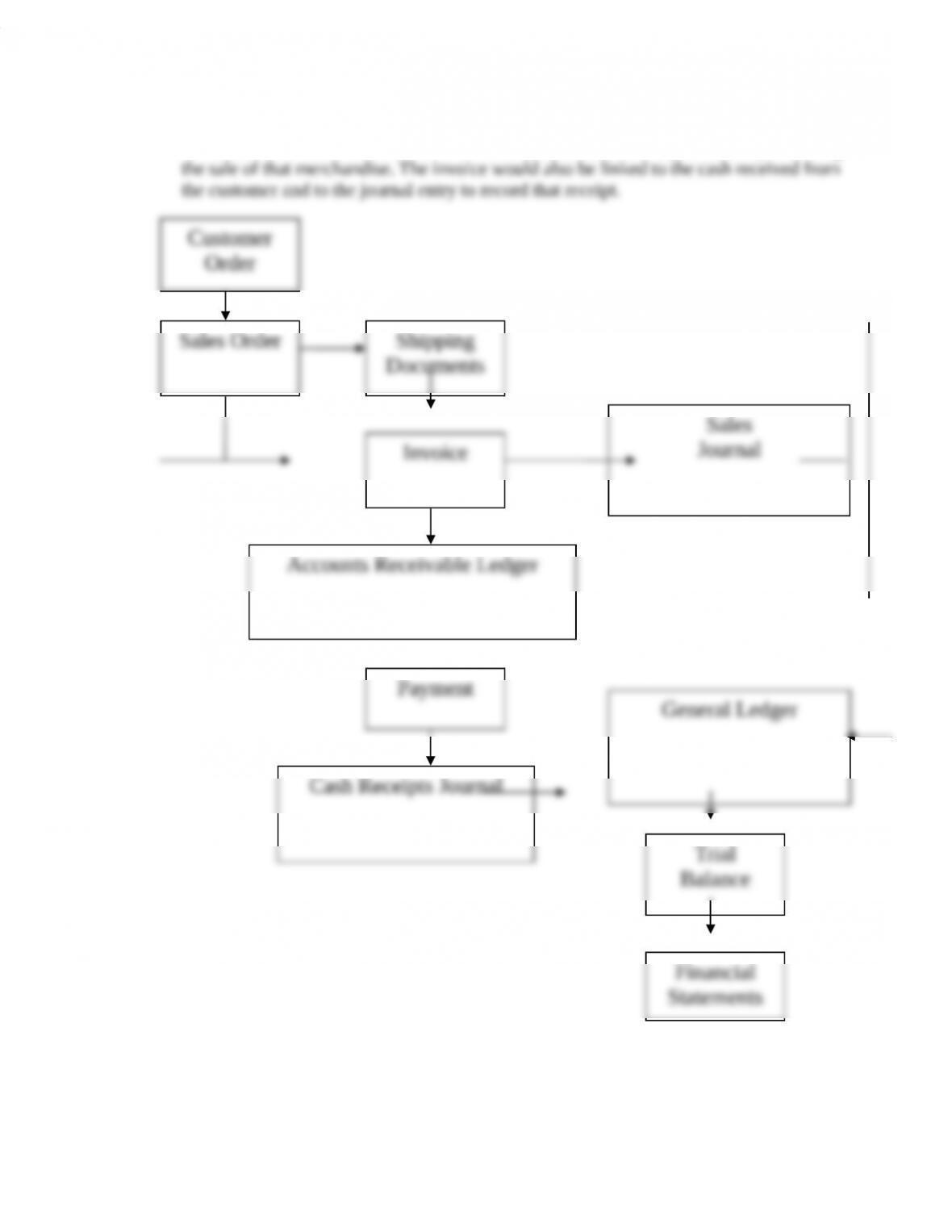

b. The audit trail for the sale of inventory links the customer order, sales order, and shipping

document to the sales invoice. These documents are linked to the journal entry recording

2-9

©2018 Pearson Education, Inc.

Financial

Statements

Trial

Balance

Ch. 2: Overview of Business Processes

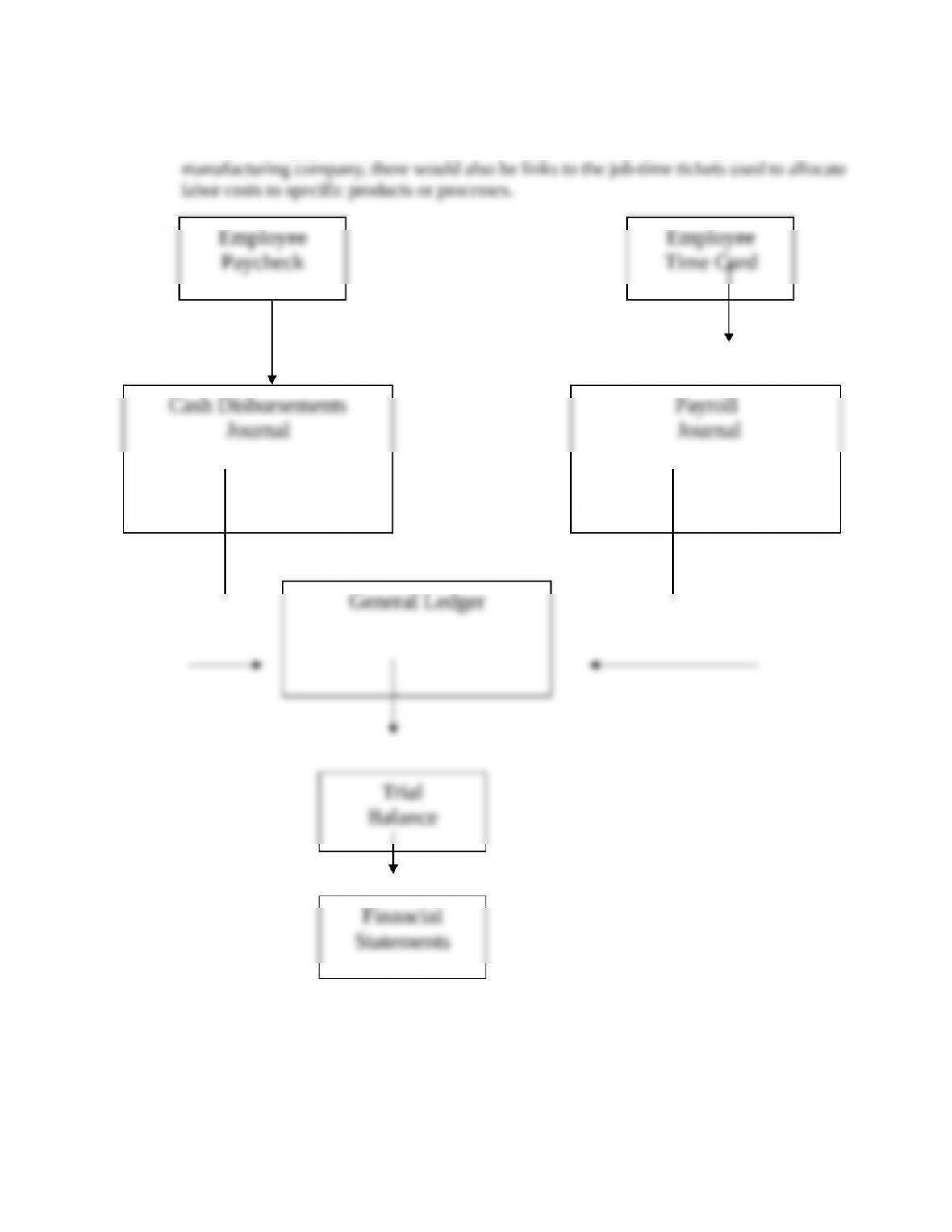

c. The audit trail for employee payroll links records of employee activity (time cards, time

sheets, etc.) to paychecks and to the journal entry to record payment of payroll. In a

2-10

©2018 Pearson Education, Inc.

Financial

Statements

Trial

Balance