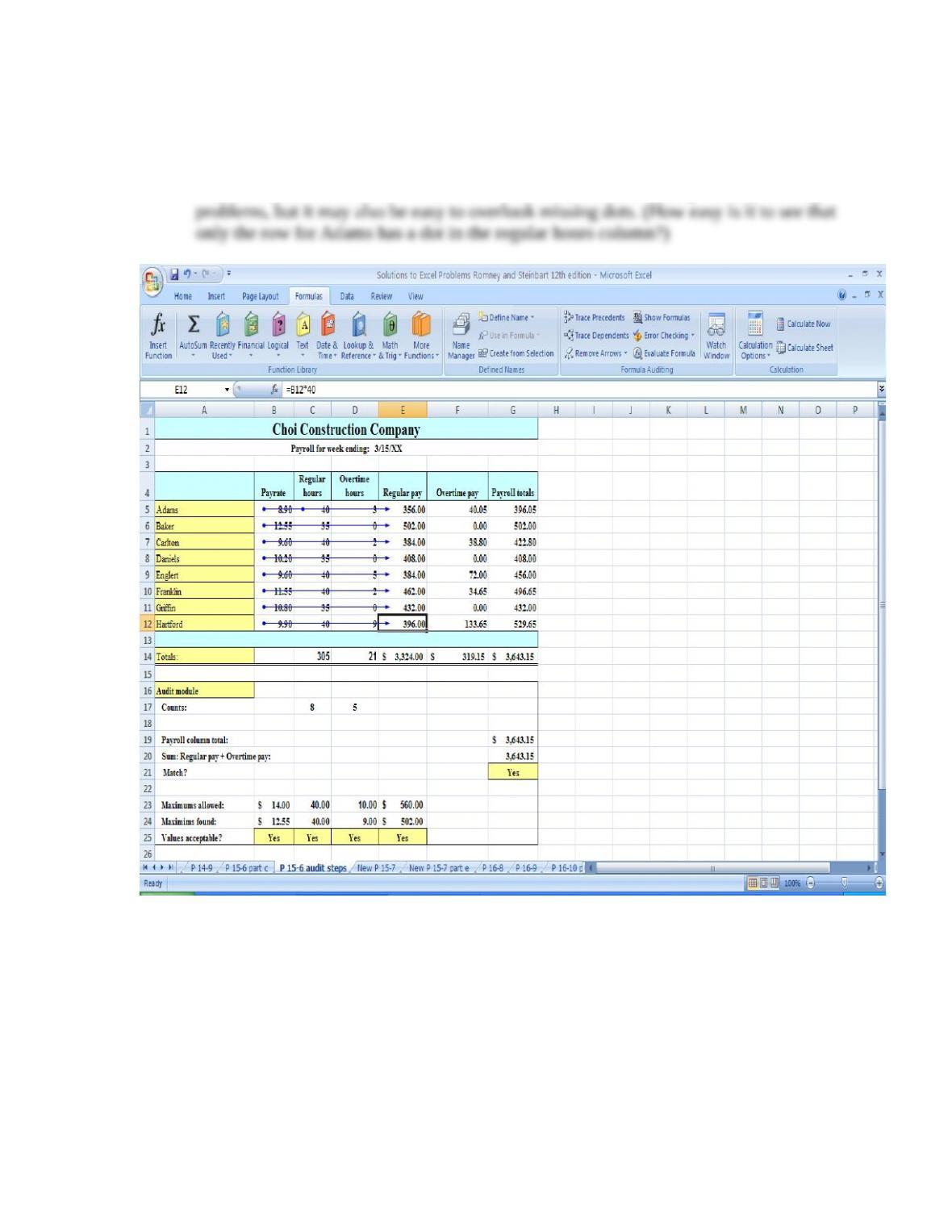

f. Follow the instructions to run the “trace precedents” audit tool. Print screen

shots that show the results, and save your work. How useful is this tool? What

are its limitations, if any?

The Trace Precedents tool is found on the formulas tab. It may help visually identify

15-1

©2018 Pearson Education, Inc.

Accounting Information Systems

g. Enter the following data for new employees (inserting new rows in proper order

to maintain alphabetical listing of employees):

Name = Able, payrate = 11.11, regular hours = 40, overtime hours = 5

Name = Easton, payrate = 10.00, regular hours = 40, overtime hours = 0

Name = Johnson, payrate = 12.00, regular hours = 35, overtime hours = 10

Which audit tests and validation rules change? Why? Print screen shots, and

save your work.

Several audit tests and validation rules changed because their parameters were

established with the unadjusted cell references. The following audit tests and validation

rules should be adjusted to include the new entries:

All input validation rules

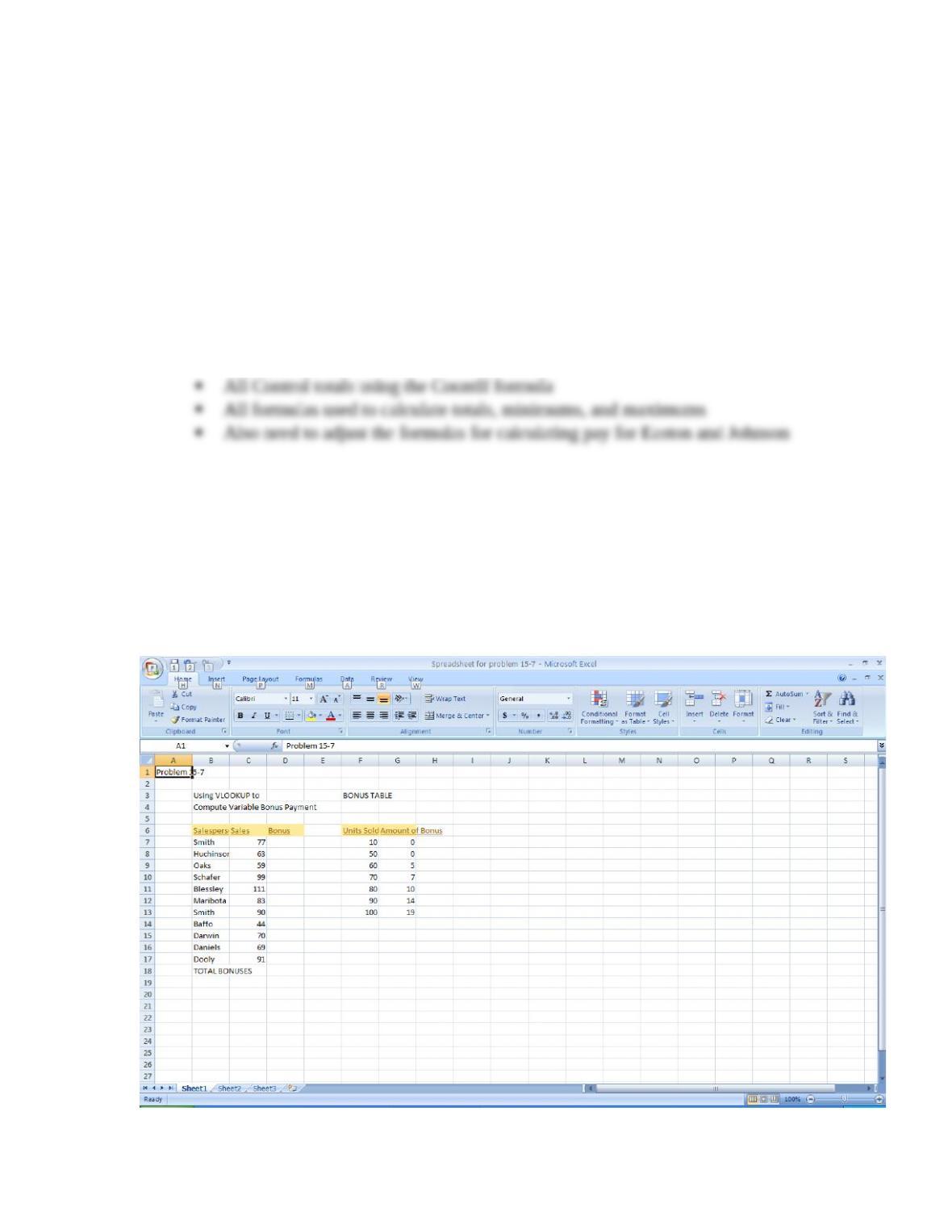

15.7 Excel Problem

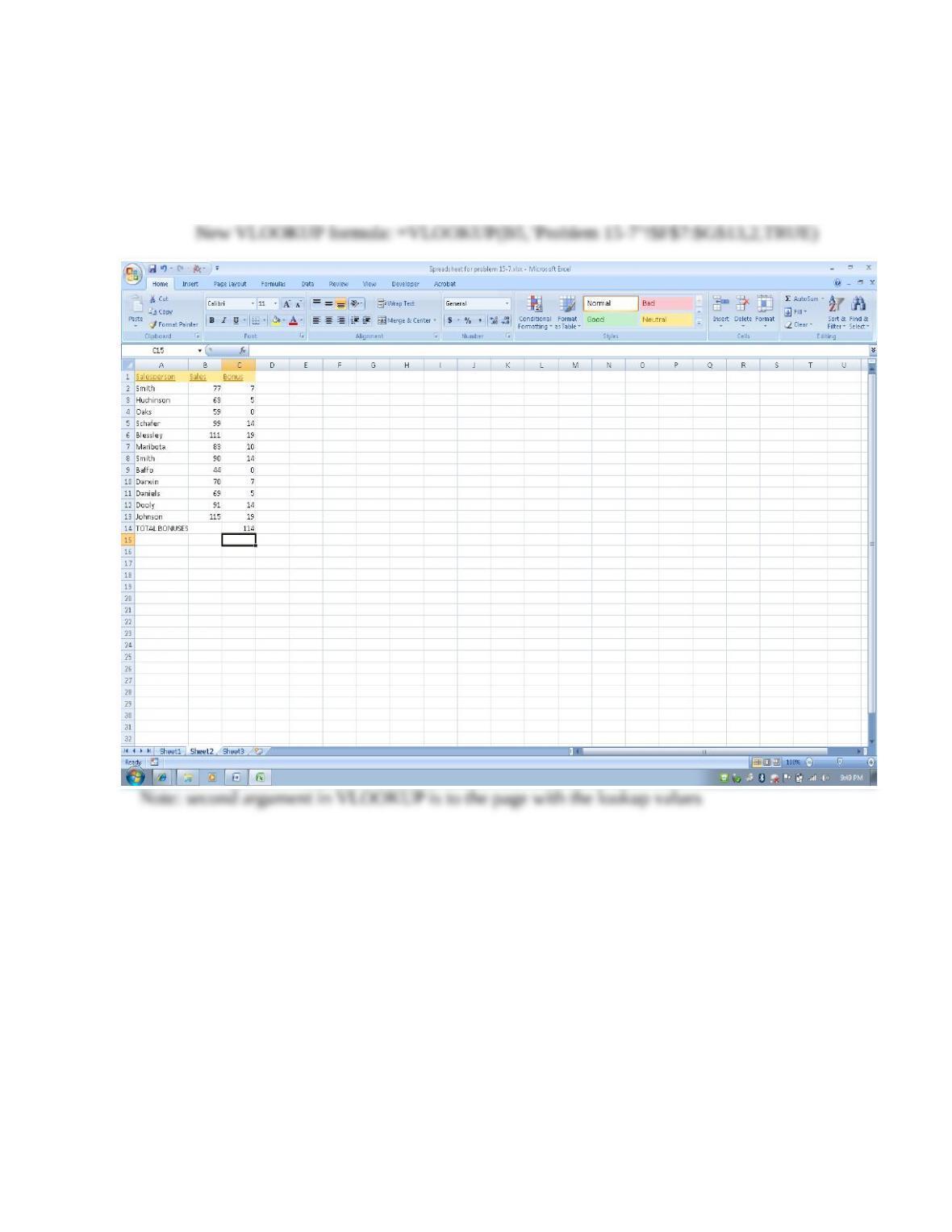

Objective: Learn how to use the VLOOKUP function for payroll calculations.

a. Read the article “Make Excel a Little Smarter” by Lois S. Mahoney and Charles

Kelliher in the Journal of Accountancy (July 2003). You can find a copy at

www.aicpa.org.

b. Read the section titled “Data in Different Places” and create the spreadsheet

illustrated in Exhibit 6. Print a screen shot of your work, and save your

spreadsheet.

15-2

©2018 Pearson Education, Inc.

Accounting Information Systems

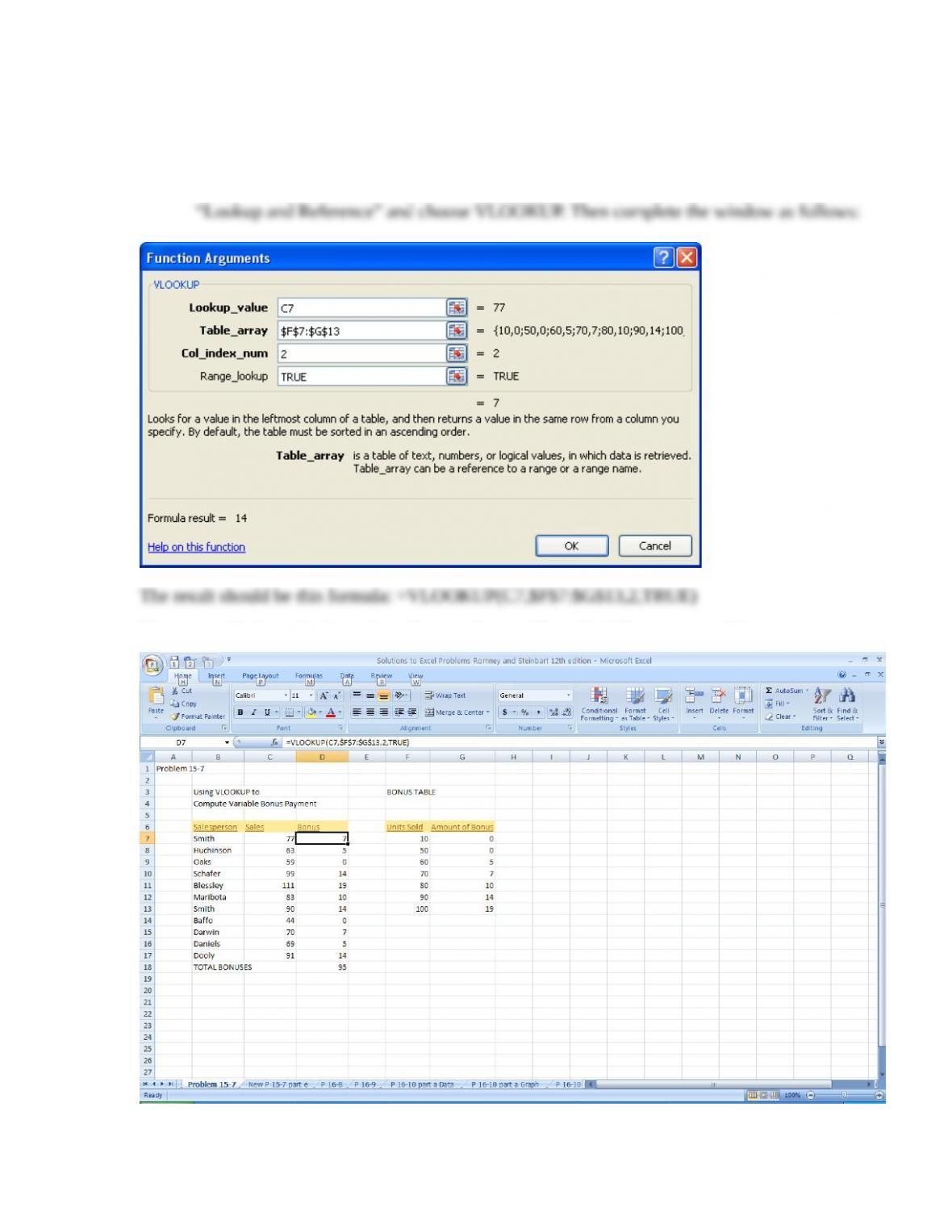

c. Create a formula that calculates total bonuses. Also create a cell entry that

indicates what that number represents. Print a screen shot of your work, and

save it.

In the Bonus column, click on the cell for the first Smith, choose the formulas tab, select

Then copy this formula down the column and you will get the following spreadsheet:

15-3

©2018 Pearson Education, Inc.

Accounting Information Systems

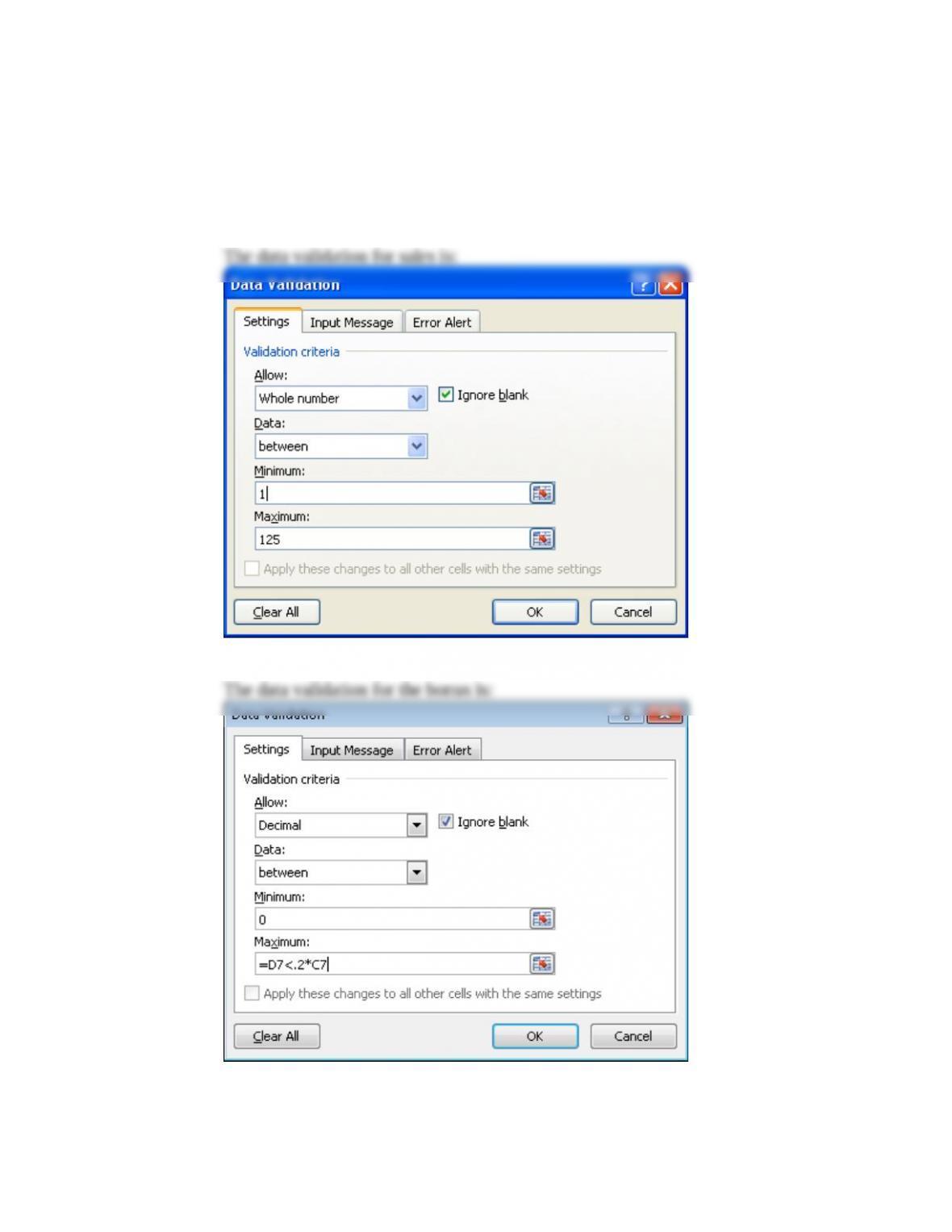

d. Add the following data validation controls to your spreadsheet, including

explanatory error messages. Save your work.

Sales must be positive.

Sales cannot exceed 125.

Amount of bonus must be nonnegative.

Amount of bonus cannot exceed 20% of unit sales.

15-4

©2018 Pearson Education, Inc.

Accounting Information Systems

e. Modify your worksheet by placing the sales data and resulting bonus on a

different worksheet from the bonus table. Name your table array, and modify

the VLOOKUP function accordingly. Then add another employee: Johnson, who

sold 115 units. Print a screen shot of your new worksheet showing the bonuses

for each employee, including Johnson. Save your work.

15-5

©2018 Pearson Education, Inc.

Accounting Information Systems

15.8 The local community feels that secondary school education is a necessity in our

society and that lack of education leads to a number of social problems. As a result,

the local school board has decided to take action to reverse the rising dropout rate.

The board has voted to provide funds to encourage students to remain in school and

earn their high school diplomas. The idea is to treat secondary education like a job

and pay students. The board, however, could not agree on the details for

implementing this new plan. Consequently, you have been hired to devise a system

to compensate students for staying in school and earning a diploma.

As you devise your compensation scheme, be sure it meets the following general

control objectives for the payroll cycle:

All personnel and payroll transactions are properly authorized.

All employees are assigned to do productive work, and they do it efficiently and

effectively.

All transactions are accurately recorded and processed.

Accurate records are maintained.

All disbursements are proper.

Write a proposal that addresses these five questions:

a. How should the students be compensated (e.g., for attendance, grades)?

b. How and by whom will the payments be authorized?

c. How will the payments be processed?

d. How should the payments be made (e.g., in cash or other means)?

e. When will the payments be made?

There is no one correct answer to this problem. Students should answer parts b, c, d and e

as if they were developing a payroll system, regardless of how they answer part a. The

following are some of the issues that need to be addressed:

Who will have custody over records relating to student activity?

15-6

©2018 Pearson Education, Inc.

Accounting Information Systems

15.9 What is the purpose of each of the following control procedures (i.e., what threats is

it designed to mitigate)?

a. Compare a listing of current and former employees to the payroll register.

b. Reconciliation of labor costs (based on job-time ticket data) with payroll (based

on time card data).

c. Direct deposit of paychecks.

d. Validity checks on Social Security numbers of all new employees added to the

payroll master file.

e. Cross-footing the payroll register.

f. Limit checks on hours worked for each time card.

To prevent overpaying employees.

g. Use of a fingerprint scanner in order for employees to record the time they

started and the time they quit working each day.

To ensure the validity of employee time and attendance data by preventing one

h. Encryption of payroll data both when it is electronically sent to a payroll service

bureau and while at rest in the HR/payroll database.

i. Establishing a separate payroll checking account and funding it as an imprest

account.

j. Comparison of hash totals of employee numbers created prior to transmitting

time-worked data to payroll provider with hash totals of employee numbers

created by payroll provider when preparing paychecks.

k. Periodic reports of all changes to payroll database sent to each department

manager.

15-7

©2018 Pearson Education, Inc.

Accounting Information Systems

l. Providing employees with earnings statements every pay period.

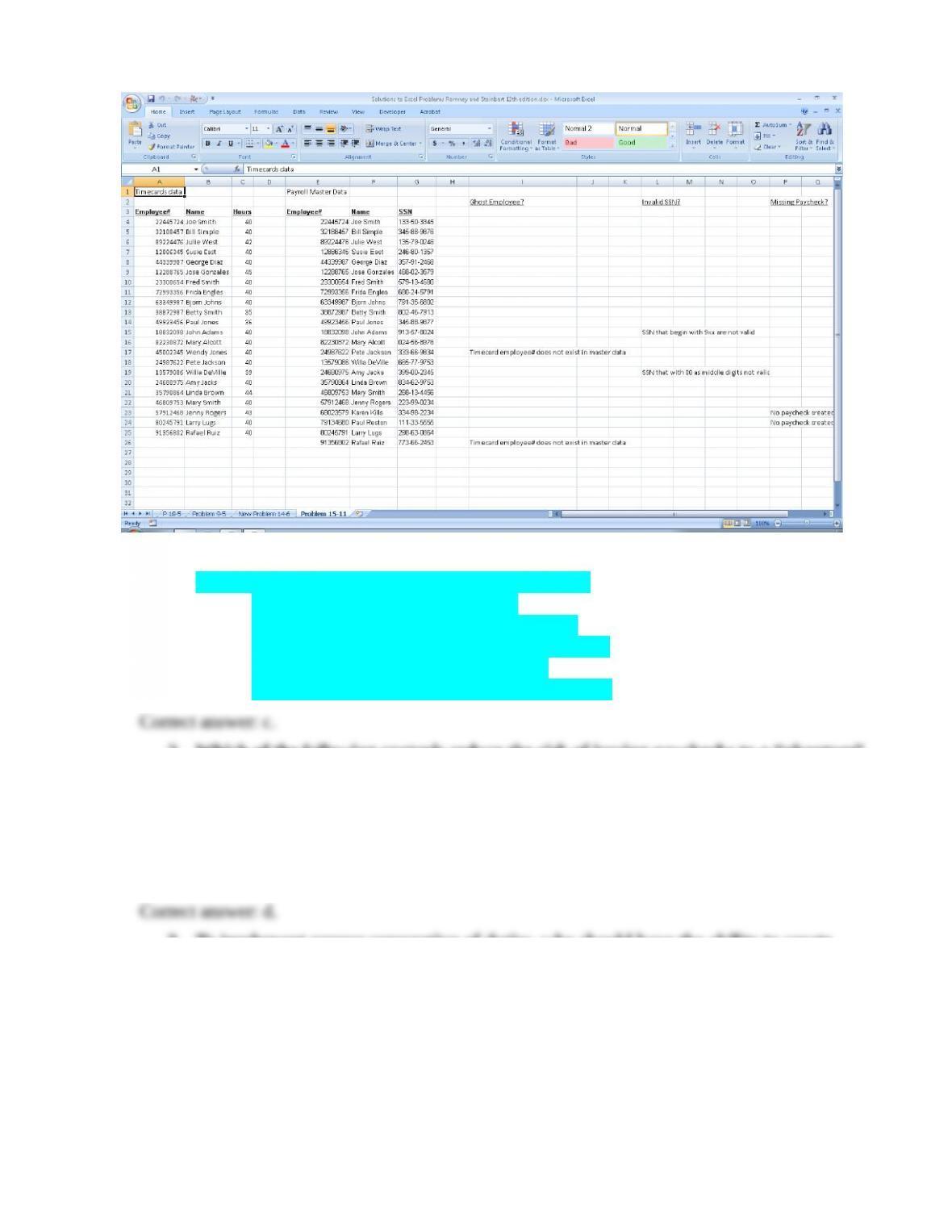

15.10 Excel Problem

Objective: Learn how to use text and array formulas to locate potential payroll

problems.

a. Download the spreadsheet for this problem from the course Web site.

b. In column I, under the label “Ghost Employee?” write a function that compares

the employee# in the timecards column to the employee# in the payroll master

data column and displays the message: “Timecard employee# does not exist in

master data” for any employee in the timecards columns who is not listed in the

payroll master data columns. The function should leave the cell blank if the

employee# in the timecards worksheet does exist in the payroll master file

worksheet. (Hint: Use the ISNA and MATCH functions.)

c. In column L, titled “Invalid SSN?” write a function to identify invalid Social

Security numbers. Assume that Social Security numbers that begin with the digit

9 or that have the digits 00 for the middle two numbers are invalid. Your

function should display a message that flags either of these two conditions or

which displays nothing otherwise. (Hint: there are text functions that examine

specific portions of a string, such as the left 3 characters, and there are also

functions that convert text to numeric values.)

15-8

©2018 Pearson Education, Inc.

Accounting Information Systems

Excel’s built-in text functions (MID and LEFT) are used here to parse social security

numbers. The function MID takes three arguments: the first one indicates the cell to

test (in this case, the social security numbers in column G); the second indicates the

position to begin with (in this case, the fifth character which is the one immediately

The entire nested IF function then works as follows:

1. Test if the middle two digits are zero. If they are, return a message that a Social

2. If the two middle digits are not zero, then the second IF test is performed, which

d. In column P, titled “Missing Paycheck?” write a function to check whether a

timecard exists for each employee in the master payroll data section of the

worksheet. The formula should return either the message “No paycheck created

for this employee” or display nothing.

The MATCH function checks to see if the employee number in the master payroll

If the employee number in the master payroll data (column E) does not exist in the

timecard data (column A) the MATCH function returns the value N/A. Therefore, the

The solution looks like this:

15-9

©2018 Pearson Education, Inc.

Accounting Information Systems

15.11 Answer all of the following multiple-choice problems:

1. Tokenization is a control that mitigates the risk of

a. Inaccurate or invalid master data

b. Unauthorized disclosure of sensitive data

c. Unauthorized changes to payroll master data

d. Inaccurate time and attendance data

e. Theft or fraudulent distribution of paychecks

2. Which of the following controls reduce the risk of issuing paychecks to a “phantom”

or “ghost” employee?

a. Restrict physical access to blank paychecks

b. Prenumber all payroll checks

c. Use an imprest account to clear payroll checks

d. All of the above

e. None of the above

3. To implement proper segregation of duties, who should have the ability to create

new records in the employee master file used for processing payroll?

a. A payroll clerk

b. Someone in HR

c. The new employee’s supervisor

d. Any of the three people listed above could perform this task

e. None of the three people listed above should perform this task

15-10

©2018 Pearson Education, Inc.

Accounting Information Systems

4. An application control that compares the amount of an employee’s raise to that

employee’s existing salary is called a(n):

a. Limit check

b. Range test

c. Reasonableness test

d. Check digit verification

e. Size check

5. The purpose of issuing earnings statements to employees is to mitigate the risk of

a. Unauthorized changes to payroll master data

b. Errors in processing payroll

c. Theft or fraudulent distribution of paychecks

d. Untimely payments

6. The use of biometrics as part of employee authentication is designed to primarily

reduce the risk of which threat?

a. Inaccurate updating of the master payroll file

b. Inaccurate time and attendance data

c. Failure to make required payroll tax payments

d. Errors in processing payroll

7. Which of the following control procedures is designed to reduce the risk of theft of

paychecks or fraudulent distribution of paychecks?

a. Restriction of access to blank payroll checks

b. Prenumbering and periodically accounting for all paychecks

c. Redepositing all unclaimed paychecks and investigating the reasons why the

paychecks were not claimed

d. All of the above

e. None of the above

8. Use of a separate checking account for payroll is designed to reduce the risk of the

threat of

a. Unauthorized changes to the payroll master file

15-11

©2018 Pearson Education, Inc.

Accounting Information Systems

b. Errors in processing payroll

c. Theft or fraudulent disbursement of paychecks

d. Failure to make required payments to government tax agencies

e. Loss or destruction of payroll data

SUGGESTED ANSWERS TO THE CASES

CASE 15-1 Research Report: HRM/Payroll Opportunities for CPAs

Payroll has traditionally been an accounting function and some CPAs have provided

payroll processing services to their clients. Today, CPAs are finding additional new

lucrative opportunities to provide not only payroll processing but also various HR

services. Write a brief report that compares the provision of payroll and HR services

by CPAs with that of national payroll providers. Perform the following research to

collect the data for your report:

1. Read the articles “Be an HR Resource for Your Clients,” by Michael Hayes and

“Hired Help: Finding the Right Consultant,” by Joanne Sammer, both of which

were published in the November, 2006 issue of the Journal of Accountancy.

2. Contact a local CPA firm that provides payroll and HR services and find out

what types of services they perform and what types of clients they serve.

Reports will of course vary from student to student; however, the following presents

some points that should appear in a student’s report:

1. CPA’s naturally have the necessary skills to provide payroll and human resource (HR)

services.

2. Although national payroll providers also provide the same services, CPA’s are in a

3. Even if a CPA does not offer payroll/HR services, they are in good position to help

4. Some of the payroll/HR services a CPA can offer are as follows:

a. Payroll administration

b. Benefits administration

15-12

©2018 Pearson Education, Inc.

Accounting Information Systems

15-13

©2018 Pearson Education, Inc.