Ch 13: The Expenditure Cycle

13.10 Last year the Diamond Manufacturing Company purchased over $10 million worth

of office equipment under its “special ordering” system, with individual orders

ranging from $5,000 to $30,000. Special orders are for low-volume items that have

been included in a department manager’s budget. The budget, which limits the

types and dollar amounts of office equipment a department head can requisition, is

approved at the beginning of the year by the board of directors. The special

ordering system functions as follows:

Purchasing A purchase requisition form is prepared and sent to the purchasing

department. Upon receiving a purchase requisition, one of the five purchasing

agents (buyers) verifies that the requester is indeed a department head. The buyer

next selects the appropriate supplier by searching the various catalogs on file. The

buyer then phones the supplier, requests a price quote, and places a verbal order. A

prenumbered purchase order is processed, with the original sent to the supplier and

copies to the department head, receiving, and accounts payable. One copy is also

filed in the open-requisition file. When the receiving department verbally informs

the buyer that the item has been received, the purchase order is transferred from

the open to the filled file. Once a month, the buyer reviews the unfilled file to follow

up on open orders.

Receiving The receiving department gets a copy of each purchase order. When

equipment is received, that copy of the purchase order is stamped with the date and,

if applicable, any differences between the quantity ordered and the quantity

received are noted in red ink. The receiving clerk then forwards the stamped

purchase order and equipment to the requisitioning department head and verbally

notifies the purchasing department that the goods were received.

Accounts Payable Upon receipt of a purchase order, the accounts payable clerk

files it in the open purchase order file. When a vendor invoice is received, it is

matched with the applicable purchase order, and a payable is created by debiting

the requisitioning department’s equipment account. Unpaid invoices are filed by

due date. On the due date, a check is prepared and forwarded to the treasurer for

signature. The invoice and purchase order are then filed by purchase order number

in the paid invoice file.

Treasurer Checks received daily from the accounts payable department are

sorted into two groups: those over and those under $10,000. Checks for less than

$10,000 are machine signed. The cashier maintains the check signature machine’s

key and signature plate and monitors its use. Both the cashier and the treasurer sign

all checks over $10,000.

a. Describe the weaknesses relating to purchases and payments of “special orders”

by the Diamond Manufacturing Company.

b. Recommend control procedures that must be added to overcome weaknesses

identified in part a.

c. Describe how the control procedures you recommended in part b should be

modified if Diamond reengineered its expenditure cycle activities to make

maximum use of current IT (e.g., EDI, EFT, bar-code scanning, and electronic

forms in place of paper documents).

Weakness Control Effect of new IT

1. Buyer does not verify that

Compare requested amounts

System can automatically compare the

5. Written notice of

Send written notice of

Receiving data and comments entered

6. Written notice of

Send written notice of

Configure system to notify accounts

7. Mathematical accuracy of

Verify mathematical accuracy

Automatic verification of mathematical

8. Invoice quantity not

Compare/verify invoiced

System verifies invoice quantity with

9. Notification of

Obtain confirmation from

Configure system to require

10. Voucher package not sent

Send voucher package

Configure system to match invoices

11. Voucher package not

Treasurer should mark

Configure system to mark supporting

12. No mention of bank

Bank account should be

Bank account should be reconciled by

Ch 13: The Expenditure Cycle

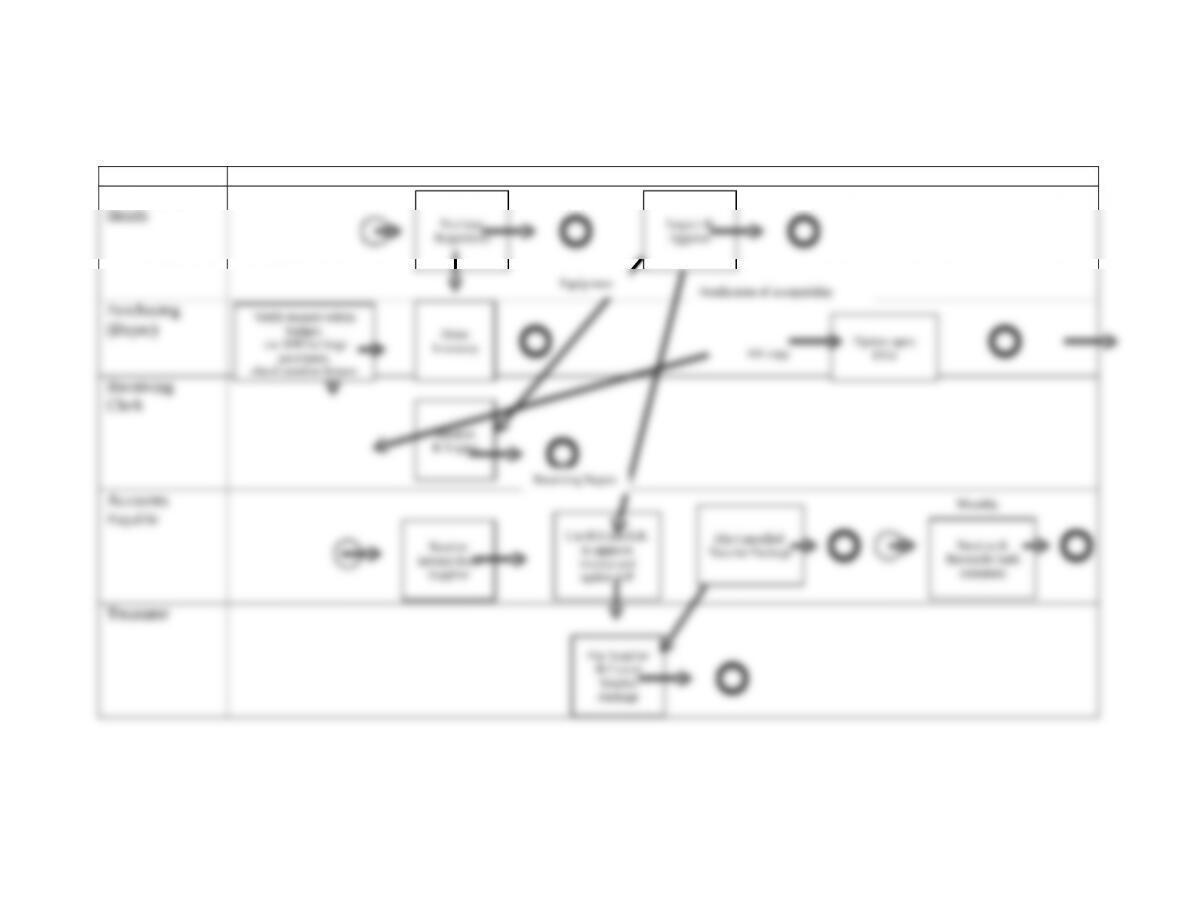

d. Draw a BPMN diagram that depicts Diamond’s reengineered expenditure cycle. (CPA Examination, adapted)

Solution will vary depending upon which weaknesses were corrected. This BPMN addresses all the weaknesses listed above.

Employee Activity Performed (sequential, left-to-right across all rows)

Department

Heads

Payable

Treasurer

Use P.O and R.R.

to approve

invoice and

update A/P

Receive

Invoice from

Supplier

Pay Supplier

& Cancel

Voucher

Package

Receive &

Reconcile bank

statement

File Cancelled

Voucher Package

Accounting Information Systems

13.11 The ABC Company performs its expenditure cycle activities using its integrated

ERP system as follows:

Employees in any department can enter purchase requests for items they note as being

The company maintains a perpetual inventory system.

Each day, employees in the purchasing department process all purchase requests from

Receiving department employees have read-only access to outstanding purchase

Receiving department employees compare the quantity delivered to the quantity

Inventory is stored in a locked room. During normal business hours an inventory

Occasionally, special items are ordered that are not regularly kept as part of inventory,

All supplier invoices (both regular and one-time) are routed to accounts payable for

Required:

a. Identify weaknesses in ABC’s existing expenditure cycle procedures, explain the

resulting problems, and suggest as solution.

Weakness/Problem Applicable Control

A formal inventory control system (EOQ,

A formal inventory control system should be

There is no mention of periodic physical

Regular physical counts of inventory need to

Any purchasing agent can add new

suppliers to the approved supplier master

suppliers.

Restrict the number of employees who can

make changes to the approved supplier list.

Selection of suppliers is based solely on

Criteria for selecting suppliers should include

Receiving department employees have

access to the quantities ordered on

Reconfigure the system and do not permit

receiving department employees’ to access

Receiving department employees

sometimes unload deliveries without

Create a policy requiring receiving

department employees to always verify the

Receiving department employees inform

purchasing of discrepancies between

Configure the system to compare quantities

received to quantities ordered. The system

The identity of employees removing

The identity of employees removing

Accounts payable clerks can create

one-time supplier records without review

The system should be configured to print a

list of all one-time suppliers. Management

There is no indication that supporting

The system should be configured to mark

Checks are returned to accounts payable

Checks should be mailed by the cashier or the

The treasurer, who has the ability to write

Someone other than the cashier or treasurer

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

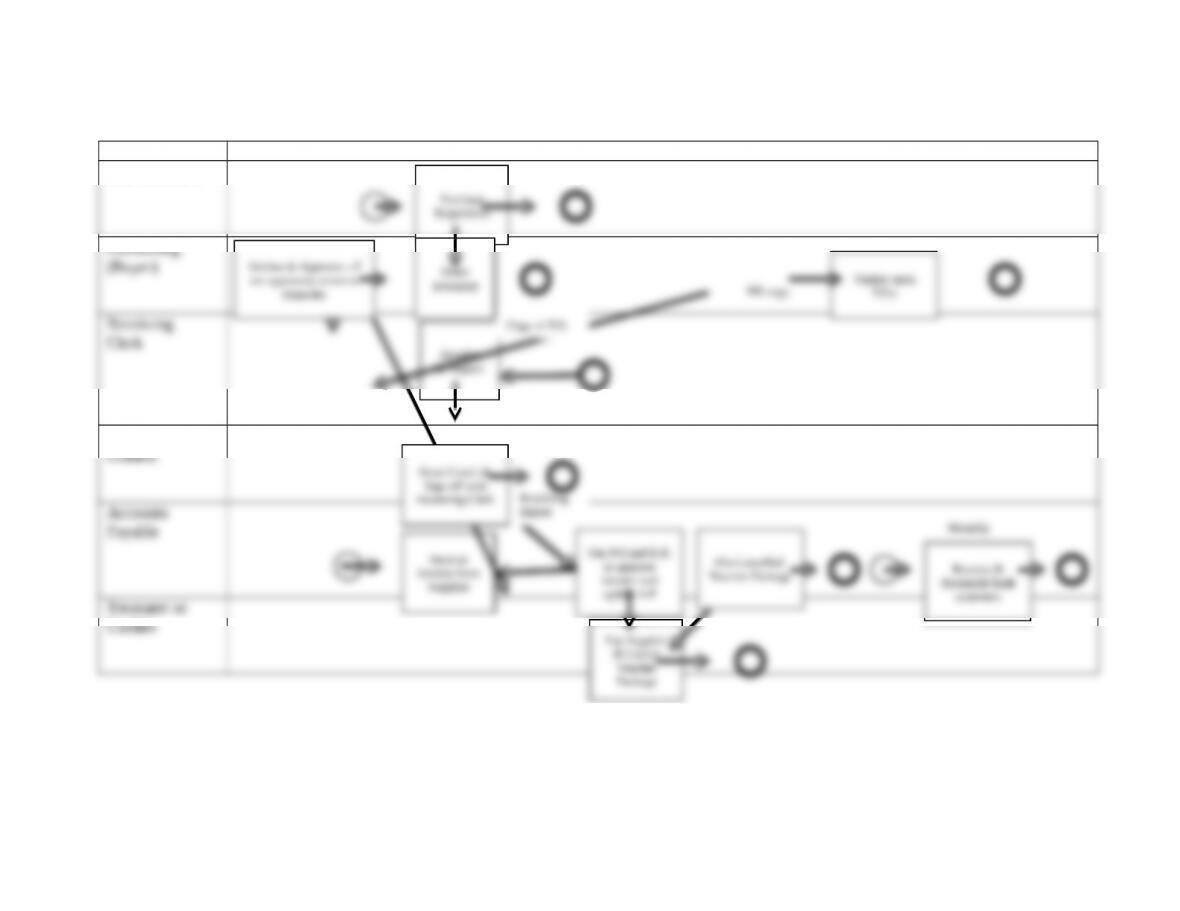

b. Draw a BPMN that reflects the ABC Company’s reengineered expenditure cycle processes.

Actual solution will depend upon which weaknesses were identified; this diagram addresses all the weaknesses.

Employee Activity Performed (sequential, left-to-right across all rows)

Any Employee

Receiving

Clerk

Inventory

Control

Treasurer or

Cashier

Receive

& Inspect

Use P.O and R.R.

to approve

invoice and

update A/P

Receive

Invoice from

Supplier

Pay Supplier

& Cancel

Voucher

Package

Receive &

Reconcile bank

statement

Copy of P.O.

File Cancelled

Voucher Package

Accounting Information Systems

13.12 Figure 13-11 depicts the basic activities performed in Lexsteel’s expenditure cycle.

The following additional information supplements that figure:

Because of cash flow problems, Lexsteel always pays suppliers on the last possible day

The purchasing manager reviews and approves all purchases prior to e-mailing them to

After counting and inspecting incoming deliveries, the receiving clerk enters the

After entering that information, the receiving clerk takes the inventory to the inventory

Access to the inventory control department is restricted.

Inventory is only released to production when properly authorized request is received.

Physical counts of inventory are taken every three months. Discrepancies between the

Required

Identify at least three control weaknesses in Lexsteel’s expenditure cycle. For each weakness,

explain the threat and suggest how to change the procedures to mitigate that threat.

1. Weakness: No timely resolution/follow-up if there are differences between quantities

a. Threat: may end up paying for items not received.

b. Recommendation: timely reconciliation of receiving report against purchase order

2. Weakness: Voucher package not cancelled upon payment.

a. Threat: Uncancelled documents can be used to make duplicate or fraudulent

3. Weakness: treasurer makes EFT transactions and reconciles bank statements.

a. Threat: Treasurer can steal funds and conceal by adjusting the bank reconciliation.

4. Weakness: Lexsteel does not take advantage of discounts for early payment.

5. Weakness: Receiving clerk has custody of inventory and updates records

6. Weakness: Copy of RR sent to A/P is not signed by inventory control.

a. Threat: theft of inventory with no way to determine accountability.

7. Weakness: no indication that receiving verifies that all incoming deliveries are

authorized.

a. Threat: time and cost of receiving and then returning unordered merchandise.

Problem 13.13 Excel Problem

Required: Download the spreadsheet for this problem from the course website and perform

the following tasks:

1. Explore Excel’s AutoFilter function.

a. At the bottom of the table, in cell C79 enter the words “Total (sum)” and in cell

b. At the bottom of the table, in cell C80 enter the words “Total (subtotal)” and in

c. Use AutoFilter to display all purchases from suppliers in Zipcode 85110. What is

2. Use the AutoFilter and Sort functions to identify the following warning signs of

potentially fraudulent supplier invoices:

a. Suppliers that have only initials for the name

Solution steps for Problem 13.13

1. Requirement 1 – autofilter and subtotal versus sum.

a. Sum totals all rows, whether or not visible. Subtotal only sums visible rows, so

2. Requirement 2 – fraud investigation

a. Sort by supplier names in alpha order will show many variants on DFR

13.14 Answer the following multiple-choice questions:

1. The control procedure of comparing a voucher package to vendor invoices is designed to

reduce the risk of

a. Failure to take advantage of discounts for prompt payment

b. Mistakes in posting to accounts payable

c. Paying for items not received

d. Theft of inventory

e. Making duplicate payments

2. Which of the following statements are true?

a. Issuing employees procurement cards is an example of the control procedure referred to

as “general authorization”

b. Organizations can reduce the risk of fraudulent disbursements by sending their bank a list

of all checks issued, a process referred to as “Positive Pay”

c. Both of the statements above are true

d. None of the statements above are true

3. The control procedure of prohibiting employees from accepting gifts is designed to

reduce the risk of

a. Theft of inventory

b. Kickbacks

c. Fraudulent cash disbursements

d. Stockouts

e. None of the above

4. The control procedure of cancelling the documents in a voucher package is designed to

reduce the risk of

a. Making duplicate payments

b. Paying for items not received

c. Fraudulent cash disbursements

d. Failure to take advantage of discounts for prompt payment

e. Theft of inventory

5. Which of the following control procedures is designed to reduce the risk of check

alteration fraud?

a. ACH blocks on accounts not used for payments

b. Use of dedicated computer and browser for online banking

c. Establishing “Positive Pay” arrangements with banks

d. Access controls for EFT terminals

e. Prenumbering all checks

6. Which of the following control procedures is designed to reduce the risk of theft of

inventory?

a. Restriction of physical access to inventory

b. Periodic physical counts of inventory and reconciliation to recorded quantities on

hand

c. Documentation of all transfers of inventory between employees

d. All of the above

e. None of the above

7. Which of the following control procedures is designed to reduce the risk of ordering

unneeded inventory?

a. Tracking and monitoring product quality by supplier

b. Purchasing only from approved suppliers

c. Holding purchasing managers responsible for rework and scrap costs

d. All of the above

e. None of the above

8. Which of the following documents is no longer needed if a company uses the evaluated

receipts system (ERS) with its suppliers?

a. Purchase Order

b. Receiving Report

c. Supplier Invoice

d. Debit Memo

e. None of the above

9. Kickbacks are a problem because they increase the risk of

a. Purchasing inventory that is not needed

b. Purchasing inferior quality items

c. Purchasing at inflated prices

d. All of the above

e. None of the above

10. Which threat is most likely to result in the largest losses in a short period of time?

a. Alteration of checks or EFT payments

b. Theft of inventory

c. Duplicate payments to suppliers

d. All of the above

e. None of the above

SUGGESTED ANSWERS TO THE CASES

CASE 13-1 RESEARCH PROJECT: IMPACT OF IT ON EXPENDITURE

CYCLE ACTIVITIES, THREATS, AND CONTROLS

Search popular business and technology magazines (Business Week, Forbes,

Fortune, CIO, etc.) to find an article about an innovative use of IT that can be used

to improve one or more activities in the expenditure cycle. Write a report that:

a. Explains how IT can be used to change expenditure cycle activities

Solutions will vary depending upon articles read.

b. Discusses the control implications. Refer to Table 13-2 and explain how the new

procedure changes the threats and appropriate control procedures for mitigating

those threats.

Be sure that the report adequately addresses the relevant issues from Table 13-2.