Accounting Information Systems

13.4 Match threats in the first column to appropriate control procedures in the second

column. More than one control may be applicable.

Threat Control Procedure

1. _d,e__ Failing to take available purchase

discounts for prompt payment.

a. Only accept deliveries for which an

approved purchase order exists.

n. Regular backup of the expenditure cycle

database.

o. Train employees how to respond properly

to gifts or incentives offered by suppliers.

p. Hold purchasing managers responsible for

costs of scrap and rework.

q. Reconciliation of bank account by someone

other than the cashier.

13.5 Use Table 13-2 to create a questionnaire checklist that can be used to evaluate

controls for each of the basic activities in the expenditure cycle (ordering goods,

receiving, approving supplier invoices, and cash disbursements).

a. For each control issue, write a Yes/No question such that a “No” answer

represents a control weakness. For example, one question might be “Are

supporting documents, such as purchase orders and receiving reports, marked

“paid” when a check is issued to the vendor?”

A wide variety of questions is possible. Below is a sample list:

Question Yes No

1. Is access to supplier master data restricted?

2. Are additions to supplier master data regularly reviewed and all changes

investigated?

3. Is sensitive data encrypted while stored in the database?

4. Does a backup and disaster recovery plan exist?

5. Have backup procedures been tested within the past year?

6. Are appropriate data entry edit controls used?

7. Is a perpetual inventory maintained?

8. Are physical counts of inventory taken regularly and used to adjust the

perpetual inventory records?

9. Are competitive bids used when ordering expensive items?

10. Are purchasing agents required to disclose financial interests in

suppliers?

11. Are budgets set for service expenses and are variances investigated?

12. Is the system configured to generate purchase orders only to suppliers

listed in the database?

13. Are receiving dock employees trained to accept deliveries only when an

approved purchase order exists?

14. Are receiving dock employees trained about the importance of

accurately counting all items delivered?

15. Do receiving dock employees inspect all deliveries for quality?

16. Do both receiving dock employees and inventory control employees

sign off on the transfer of items?

17. Is physical access to inventory restricted?

18. Are invoices only approved for payment when accompanied by both a

purchase order and receiving report?

19. Is supporting documentation cancelled or marked “Paid” when a check

is generated?

20. Are invoices filed by due date (adjusted for any discounts for early

payment)?

21. Is access to blank checks restricted?

22. Is access to the EFT system restricted?

23. Is the bank account regularly reconciled by someone not involved in

issuing checks?

b.For each Yes/No question, write a brief explanation of why a “No” answer represents a

control weakness.

Question Reason a “No” answer represents a weakness

1 Unrestricted access to supplier master data could facilitate fraud by allowing the creation of

fake suppliers to whom checks can be issued.

2 Failure to investigate all changes to supplier master data may allow fraud to occur because

unauthorized suppliers may not be detected.

3 Failure to encrypt sensitive data can result in the unauthorized disclosure of banking-related

information about suppliers.

22 Unrestricted access to the EFT system increases the risk of misappropriation of funds.

23 Lack of an independent bank account reconciliation increases the risk of fraud going

undetected. It also precludes the timely identification of unauthorized disbursements,

possibly resulting in the bank refusing to correct the problem.

Accounting Information Systems

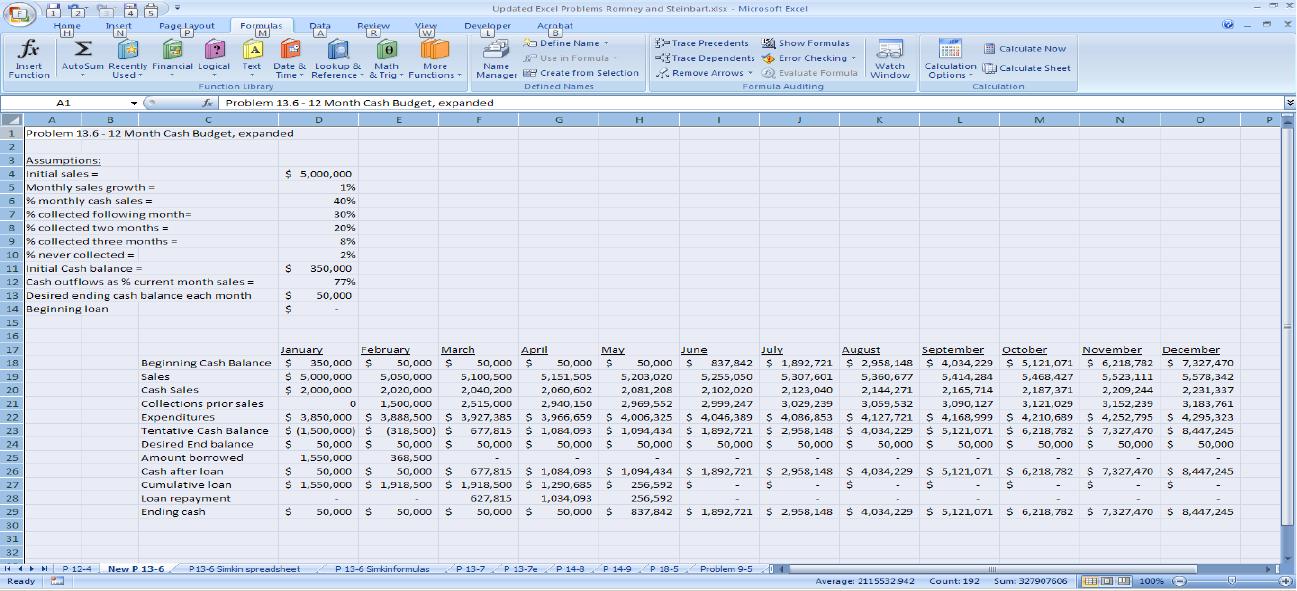

13.6 EXCEL PROJECT

a. Expand the cash budget you created in Problem 12.4 to include a row for expected cash outflows equal to 77% of the

current month’s sales.

b. Also add a row to calculate the amount of cash that needs to be borrowed, in order to maintain a minimum cash

balance of $50,000 at the end of each month.

c. Add another row to show the cash inflow from borrowing.

d. Add another row to show the cumulative amount borrowed.

e. Add another row to show the amount of the loan that can be repaid, being sure to maintain a minimum ending

balance of $50,000 each month.

Explanation of solution:

1. Always use references to assumption cells in the formulas. For example, the cash sales row formulas should be that column’s sales times cell

2. The solution rounds sales to the nearest dollar, to keep it looking clean, using this formula in February: =ROUND(D19*(100%+$D$5),0)

3. Collections from prior sales row is set to zero in January; then it gets progressively more complex as follows:

4. Tentative cash balance = beginning balance + cash sales that month + collections of prior month’s cash sales – current expenditures:

5. Amount borrowed = zero if tentative balance >= desired balance, otherwise the amount of the shortfall: =IF(D23>=D24,0,(D24-D23))

6. Cumulative loan initially = starting loan balance plus that month’s borrowing: =$D$14+D25. Subsequently, it equals prior month’s balance

7. Loan repayment is calculated as the excess of cash available over desired ending balance, but never more than the amount of the loan.

Accounting Information Systems

Problem 13-6 continued

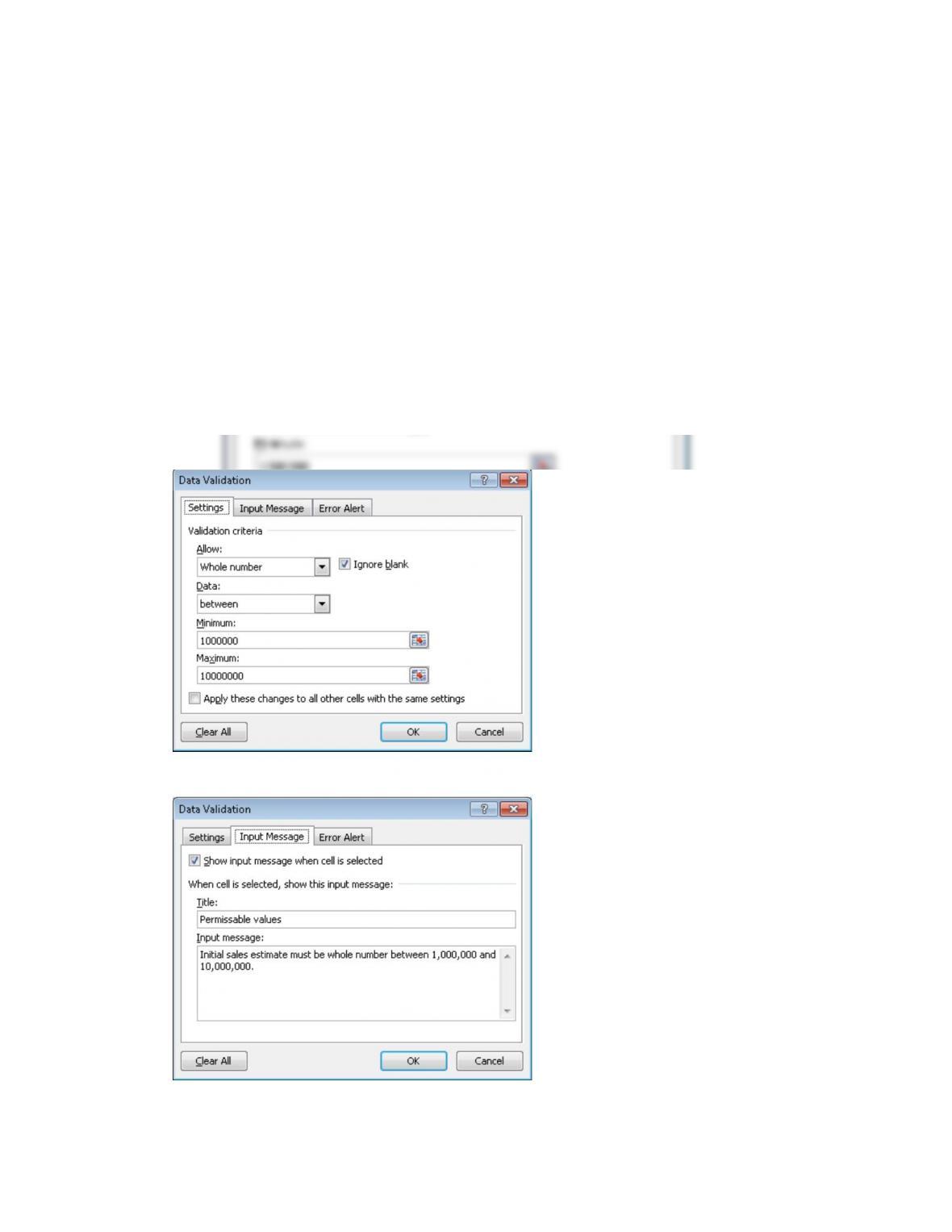

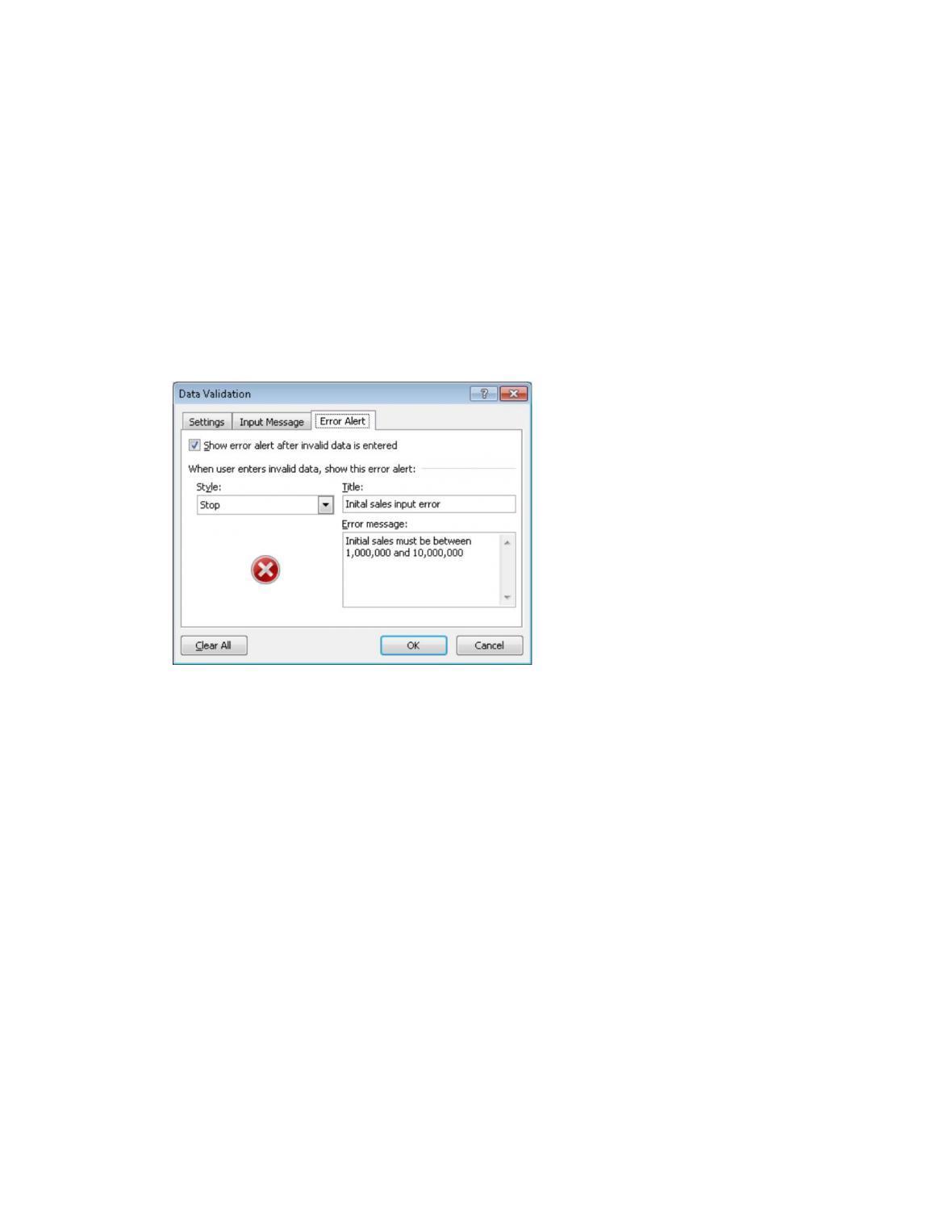

f. Add appropriate data validation controls to ensure spreadsheet accuracy.

The solutions manual for chapter 10 discussed data validation controls in detail. Possible

solutions include the following:

Also, include an appropriate input message:

And an appropriate error message:

2. Limit the sales growth, the percentage of sales made for cash, the percentages collected in

3. Limit desired ending cash balance to be greater than zero.

4. Students should also lock all the cells in the body of the spreadsheet so that users can only

Accounting Information Systems

13.7 13.7 The following table presents the results of using a CAAT tool to interrogate the XYZ Company’s ERP system for

expenditure cycle activities. It shows the number of times each employee performed a specific task.

13.8

13.9 13.10 O

rd

er

In

ve

nt

or

y

13.11 Mai

ntai

n

Sup

plier

Mas

ter

File

(add

,

dele

te,

edit)

13.12 R

ec

ei

ve

In

ve

nt

or

y

13.13 A

p

p

r

o

v

e

S

u

p

p

li

e

r

I

n

v

o

i

c

e

s

f

o

r

P

a

y

m

e

n

t

13.14 Pa

y

S

up

pl

ie

rs

Vi

a

E

F

T

13.15 S

i

g

n

C

h

e

c

k

s

13.16 M

ail

C

he

ck

s

13.17 Re

con

cile

Ba

nk

Ac

cou

nt

A 0

I

0

13.99

13.100

13.101 Required

13.102 Identify three examples of improper segregation of duties and explain the nature of each problem you find.

13.103

13.104

13.105 1. Employee A orders inventory and maintains supplier master – can alter supplier master to order from unapproved

suppliers.

13.106 2. Employee C places orders and approves invoices – could order for personal use.

13.107 3. Employee C maintains supplier master file and approves invoices, so could submit and approve payments to fictitious

vendors.

13.108 4. Employee D maintains supplier master and approves invoices – can submit and approve invoices from fictitious

suppliers.

13.109 5. Employee D approves invoices and makes EFT payments – could approve disbursal of funds to self.

13.110 6. Employee G approves invoices and mails checks – by getting custody of signed checks, has opportunity to alter.

Accounting Information Systems

13.111 13.8 The following list identifies several important control features. For each

control, (1) describe its purpose and (2) explain how it could be best implemented in

an integrated ERP system.

13.112 a. Cancellation of the voucher package by the cashier after signing the

check

13.113 b. Separation of duties of approving invoices for

payment and signing checks

13.114 c. Prenumbering and periodically accounting for all

purchase orders.

13.115 d. Periodic physical count of inventory.

13.116 e. Requiring two signatures on checks for large amounts

13.117 f. Requiring that a copy of the receiving report be

routed through the inventory stores department prior to going to accounts

payable.

13.118 g. Requiring a regular reconciliation of the bank account

by someone other than the person responsible for writing checks

13.119 h. Maintaining an approved supplier list and checking

that all purchase orders are issued only to suppliers on that list

13.121

13.122

Item

13.123 Part I – Purpose 13.124 Part II – ERP System Control

13.125

a.

13.126 Prevent resubmission of

invoices for double

payment

13.127 Control field in supplier invoice record to

indicate the document has been used

13.128 Control field in purchase order and receiving

report records to indicate the document has

been used to support payment.

g.

disbursements.

13.150

13.151 Ensure the purchase of

13.152 Validity check of supplier number on all

13.156

13.157

13.158 13.9 For good internal control, which of the following

duties can be performed by the same individual?

1. Approve purchase orders

2. Negotiate terms with suppliers

3. Reconcile the organization’s bank account

4. Approve supplier invoices for payment

5. Cancel supporting documents in the voucher package

6. Sign checks

7. Mail checks

8. Request inventory to be purchased

9. Inspect quantity and quality of inventory received

13.159

13.160

13.162

13.163Du

ty

13.164

1

13.165 213.166

3

13.167

4

13.168 513.169

6

13.170713.171

8

13.172

9

13.173113.174 13.175 13.176 13.177 13.178 13.179 13.180 13.181 13.182

13.183213.184

X

13.185 13.186 13.187 13.188 13.189 13.190 13.191 13.192

13.193313.194 13.195 13.196 13.197 13.198 13.199 13.200 13.201 13.202

13.263

13.264 Rationale:

13.265

1. The person who approves purchase orders should be in the purchasing function, which is also

2. The cashier should sign checks, cancel the supporting documents before returning them to

13.267

13.268

13.269