CHAPTER 13

THE EXPENDITURE CYCLE:

PURCHASING TO CASH DISBURSEMENTS

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

13.1 In this chapter and in Chapter 12 the controller of AOE played a major role in

evaluating and recommending ways to use IT to improve efficiency and

effectiveness. Should the company’s chief information officer make these decisions

instead? Should the controller be involved in making these types of decisions? Why

or why not?

There are several reasons why accountants should be involved in decisions about investing in IT

and not leave such decisions solely to IS professionals.

13-1

©2018 Pearson Education, Inc.

Ch 13: The Expenditure Cycle

13.2 Companies such as Wal-Mart have moved beyond JIT to VMI systems. Discuss the

potential advantages and disadvantages of this arrangement. What special controls, if

any, should be developed to monitor VMI systems?

Vendor Managed Inventory (VMI) is essentially Electronic Data Interchange (EDI) where the retailer

has given their vendor access rights to their point-of-sale (POS) system. Some of the potential

advantages and disadvantages of moving to a VMI are:

Advantages:

Disadvantages:

Cost. Retailers and vendors must incur the costs of acquiring the technology and changing the

Security. The retailer puts one of their most valuable assets, their sales data, in the hands of their

Over supply. The vendor can ship more inventory than the retailer needs to meet the demand.

Controls:

The following controls could be implemented to monitor VMI systems:

1. Monitor inventory levels. At least at first, and then periodically thereafter, the retailer should

2. Analyze inventory costs. If VMI is working, then overall inventory costs should decline.

13-2

©2018 Pearson Education, Inc.

Accounting Information Systems

13.3 Procurement cards are designed to improve the efficiency of small noninventory

purchases. What controls should be placed on their use? Why?

Since the primary benefit of procurement cards is to give employee’s the ability to make small

non-inventory purchases necessary for their area of responsibility — be it office supplies, computer

or office equipment, or meals and/or travel expenses — a formal approval process for all purchases

13.4 In what ways can you apply the control procedures discussed in this chapter to paying

personal debts (e.g., credit card bills)?

Many people do not keep their credit card receipts as evidenced by receipts left at “pay-at-the-pump”

13-3

©2018 Pearson Education, Inc.

Ch 13: The Expenditure Cycle

13.5 Should every company switch from the traditional 3-way matching process (purchase

orders, receiving reports, and supplier invoices) to the 2-way match (purchase orders

and receiving reports) used in Evaluate Receipt Settlement (ERS)? Why (not)?

Switching to ERS simplifies accounts payable and eliminates a major source of problems:

13.6 Should companies allow purchasing agents to start their own businesses that produce

goods the company frequently purchases? Why? Would you change your answer if the

purchasing agent’s company was rated by an independent service, like Consumer

Reports, as providing the best value for price? Why?

The primary issue here is conflict of interest. If a purchasing manager owns a business that supplies

goods to his employer, how does the employer know that they are receiving the best quality goods for

the lowest prices? By allowing a purchasing manager to own an independent company that supplies

13-4

©2018 Pearson Education, Inc.

Accounting Information Systems

SUGGESTED ANSWERS TO THE PROBLEMS

13.1 a. A purchasing agent orders materials from a supplier that he partially owns.

Require a purchase requisition from an operating department as authorization for preparation

of all purchase orders.

b. Receiving-dock personnel steal inventory and then claim the inventory was sent to

the warehouse.

Count all deliveries and record counts on a receiving report.

c. An unordered supply of laser printer paper delivered to the office is accepted and

paid for because the “price is right.” After jamming all of the laser printers,

however, it becomes obvious that the “bargain” paper is of inferior quality.

The problem here is that office employees are seldom trained about proper procedures for

d. The company fails to take advantage of a 1% discount for promptly paying a

vendor invoice.

e. A company is late in paying a particular invoice. Consequently, a second invoice is

sent, which crosses the first invoice’s payment in the mail. The second invoice is

submitted for processing and also paid.

Review related supporting voucher package or records (receiving report and purchase order)

13-5

©2018 Pearson Education, Inc.

Ch 13: The Expenditure Cycle

f. Inventory records show that an adequate supply of copy paper should be in stock,

but none is available on the supply shelf.

g. The inventory records are incorrectly updated when a receiving-dock employee

enters the wrong product number at the terminal.

h. A clerical employee obtains a blank check and writes a large amount payable to a

fictitious company. The employee then cashes the check.

Store unused blank company checks in a secure location.

Segregate duties by having the person reconciling the bank account be different from the

i. A fictitious invoice is received and a check is issued to pay for goods that were never

ordered or delivered.

Program the system so that it only prints checks to approved suppliers listed in the database

Restrict access to the supplier master data.

13-6

©2018 Pearson Education, Inc.

Accounting Information Systems

j. The petty cash custodian confesses to having “borrowed” $12,000 over the last five

years.

Create a petty cash imprest fund and only replenish it based on receipts documenting how

k. A purchasing agent adds a new record to the supplier master file. The company

does not exist. Subsequently, the purchasing agent submits invoices from the fake

company for various cleaning services. The invoices are paid.

Restrict access to the supplier master file

l. A clerk affixes a price tag intended for a low-end flat panel TV to a top-of-the-line

model. The clerk’s friend then purchases that item, which the clerk scans at the

checkout counter.

Restrict access to price tags so that cashiers do not have access to price tags

13-7

©2018 Pearson Education, Inc.

Ch 13: The Expenditure Cycle

13.2 Match the terms in the left column with their appropriate definition in the right

column.

Terms Definitions

1. _n__ economic order quantity a. A document that creates a legal obligation to buy and pay

for goods or services.

2. __f_ materials requirements

planning (MRP)

b. The method used to maintain the cash balance in the petty

cash account.

r. A special purpose credit card used to purchase supplies.

s. A fraud in which a supplier pays a buyer or purchasing

agent in order to sell its products or services.

13-8

©2018 Pearson Education, Inc.

Accounting Information Systems

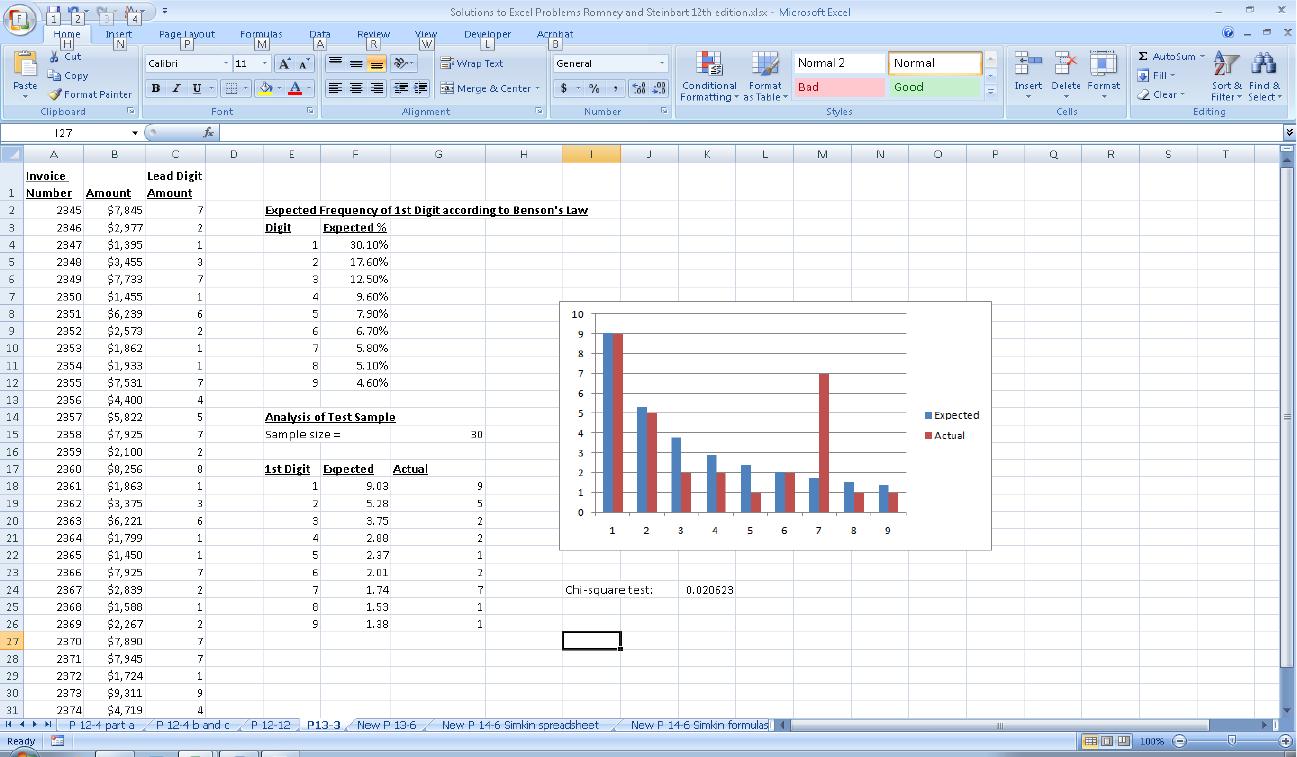

13.3 EXCEL PROJECT. Using Benford’s Law to Detect Potential Disbursements Fraud.

a. Read the article “Using Spreadsheets and Benford’s Law to Test Accounting Data,”

by Mark G. Simkin in the ISACA Journal, Vol. 1, 2010, available at www.isaca.org.

b. Follow the steps in the article to analyze the following set of supplier invoices:

Invoice

Number Amount

2345 $7,845

2346 $2,977

2347 $1,395

2348 $3,455

2359 $2,100

Invoice

Number Amount

2360 $8,256

2361 $1,863

2362 $3,375

2363 $6,221

2374 $4,719

13-9

©2018 Pearson Education, Inc.

Ch 13: The Expenditure Cycle

Hint: You may need to use the VALUE function to transform the results of using

the LEFT function to parse the lead digit in each invoice amount.

Accounting Information Systems

To apply Benford’s law, we need to write a formula that extracts the left-most digit from an invoice

number. Excel has a number of built-in functions that can parse characters in a string. The function

LEFT(cell, n) returns the left n characters from the specified cell. Thus, in our case, Left (C4,1) returns

the left-most digit from cell C4.

However, the various character-parsing functions (LEFT, RIGHT, MID) all return their results as

text. Therefore, we need to transform that result back into a number by using the VALUE

function.