12.7 O’Brien Corporation is a midsize, privately owned, industrial instrument

manufacturer supplying precision equipment to manufacturers in the Midwest. The

corporation is 10 years old and uses an integrated ERP system. The administrative

offices are located in a downtown building and the production, shipping, and

receiving departments are housed in a renovated warehouse a few blocks away.

Customers place orders on the company’s website, by fax, or by telephone. All sales

are on credit, FOB destination. During the past year sales have increased

dramatically, but 15% of credit sales have had to written off as uncollectible,

including several large online orders to first-time customers who denied ordering or

receiving the merchandise.

Customer orders are picked and sent to the warehouse, where they are placed near

the loading dock in alphabetical sequence by customer name. The loading dock is

used both for outgoing shipments to customers and to receive incoming deliveries.

There are ten to twenty incoming deliveries every day, from a variety of sources.

The increased volume of sales has resulted in a number of errors in which customers

were sent the wrong items. There have also been some delays in shipping because

items that supposedly were in stock could not be found in the warehouse. Although a

perpetual inventory is maintained, there has not been a physical count of inventory

for two years. When an item is missing, the warehouse staff writes the information

down in log book. Once a week, the warehouse staff uses the log book to update the

inventory records.

The system is configured to prepare the sales invoice only after shipping employees

enter the actual quantities sent to a customer, thereby ensuring that customers are

billed only for items actually sent and not for anything on back order.

1

©2018 Pearson Education, Inc.

Accounting Information Systems

Required:

a. Identify at least three weaknesses in O’Brien Corporation’s revenue cycle procedures,

explain the associated problem, and propose a solution. Present your answer in a

three-column table with these headings: Weakness, Problem, Solution.

b. Draw a BPMN diagram to depict O’Brien Corporation’s revenue cycle revised to

incorporate your solutions to step a.

(CMA Examination, adapted)

Weaknesses and Potential Problem(s)

Recommendation(s) to Correct Weaknesses

1. Orders from new customers do not require

Require digital signatures on all online orders

2. Customer credit histories are not checked

Customers’ credit should be checked and no

3. Outgoing shipments are placed near the

receive incoming deliveries. This increases the

risk of theft, which may account for the

unexplained shortages in inventory.

Separate the shipping and receiving docks.

4. Physical counts of inventory are not made at

Physical counts of inventory should be made at

5. Shipments are not reconciled to sales orders,

The system should be configured to match

6. The perpetual inventory records are only

unanticipated shortages that result in delays in

filling customer orders.

The warehouse staff should enter information

2

©2018 Pearson Education, Inc.

Ch. 12: The Revenue Cycle: Sales to Cash Collections

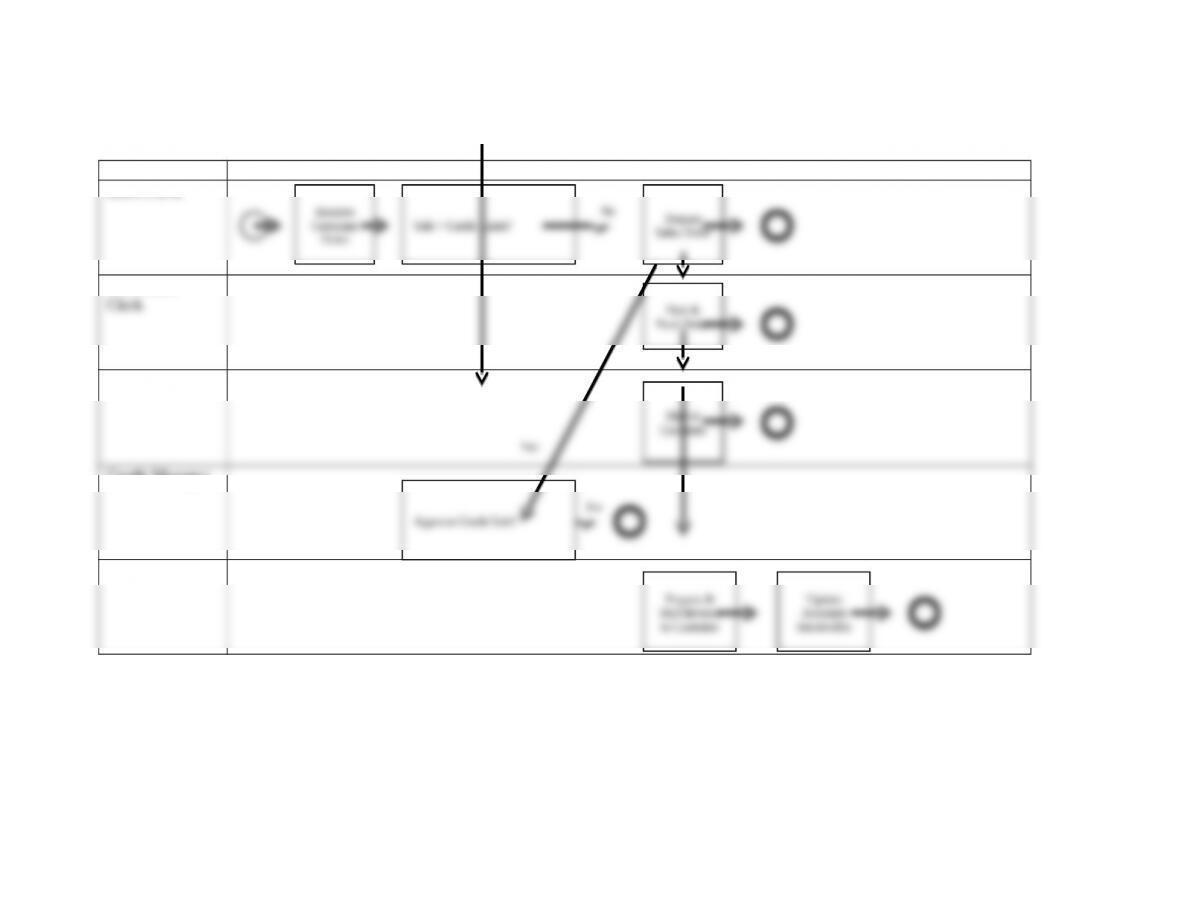

Solutions to part b will vary depending upon which weaknesses the students identified and corrected. The following corrects all six weaknesses

listed above.

Employee Activity Performed (sequential, left-to-right across all rows)

Sales Clerk

3

©2018 Pearson Education, Inc.

Accounting Information Systems

12.8 Parktown Medical Center, Inc. is a small health care provider owned by a publicly

held corporation. It employs seven salaried physicians, ten nurses, three support

staff, and three clerical workers. The clerical workers perform such tasks as

reception, correspondence, cash receipts, billing, and appointment scheduling. All

are adequately bonded.

Most patients pay for services rendered by cash or check on the day of their visit.

Sometimes, however, the physician who is to perform the respective services

approves credit based on an interview. When credit is approved, the physician files a

memo with one of the clerks to set up the receivable using data the physician

generates.

The servicing physician prepares a charge slip that is given to one of the clerks for

pricing and preparation of the patient’s bill. At the end of the day, one of the clerks

uses the bills to prepare a revenue summary and, in cases of credit sales, to update

the accounts receivable subsidiary ledger.

The front office clerks receive cash and checks directly from patients and give each

patient a prenumbered receipt. The clerks take turns opening the mail. The clerk

who opens that day’s mail immediately stamps all checks “for deposit only.” Each

day, just before lunch, one of the clerks prepares a list of all cash and checks to be

deposited in Parktown’s bank account. The office is closed from 12 noon until 2:00

p.m. for lunch. During that time, the office manager takes the daily deposit to the

bank. During the lunch hour, the clerk who opened the mail that day uses the list of

cash receipts and checks to update patient accounts.

The clerks take turns preparing and mailing monthly statements to patients with

unpaid balances. One of the clerks writes off uncollectible accounts only after the

physician who performed the respective services believes the account will not pay

and communicates that belief to the office manager. The office manager then issues

a credit memo to write off the account, which the clerk processes.

The office manager supervises the clerks, issues write-off memos, schedules

appointments for the doctors, makes bank deposits, reconciles bank statements, and

performs general correspondence duties.

Additional services are performed monthly by a local accountant who posts

summaries prepared by the clerks to the general ledger, prepares income

statements, and files the appropriate payroll forms and tax returns.

4

©2018 Pearson Education, Inc.

Accounting Information Systems

Required:

a. Identify at least three control weaknesses at Parktown. Describe the potential

threat and exposure associated with each weakness, and recommend how to best

correct them.

1. Weakness: The employees who perform services are permitted to approve credit

Control: Someone other than the physician performing the services (probably the

2. Weakness: The physician who approves credit also approves the write-off of

Threat: Accounts receivable could be understated and bad debts expense overstated

Control: Separate the duties of approving credit and approving the write-off of

3. Weakness: The employee who initially handles cash receipts also prepares billings

Threat: Theft by lapping could occur. Fees earned and cash receipts or accounts

Control: Segregate the functions of cash receipts handling and billing/accounts

4. Weakness: The employee who makes bank deposits also reconciles bank statements.

5. Weakness: The employee who makes bank deposits also issues credit memos.

Threat: The office manager could steal cash and cover up the shortage by issuing a

Control: Cash deposits should be made by an employee who does not have authority

6. Weakness: Trial balances of the accounts receivable subsidiary ledger are not

Threat: Any of fees earned, cash receipts, and uncollectible accounts expense could

Control: Periodic reconciliation of the subsidiary accounts receivable ledger to the

5

©2018 Pearson Education, Inc.

Accounting Information Systems

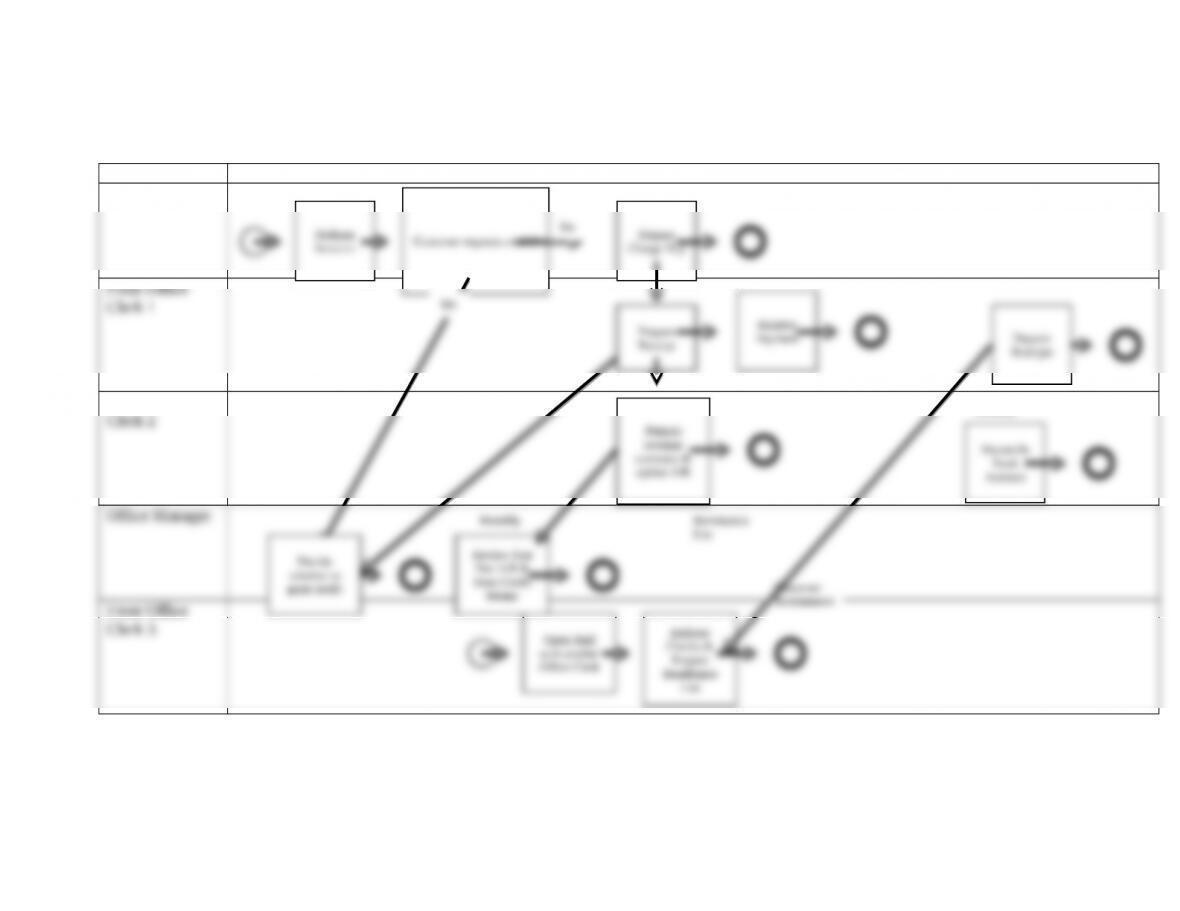

b. Draw a BPMN diagram to depict Parktown’s revenue cycle revised to incorporate your solutions to step a.

(CPA Examination, adapted)

Actual solution will depend upon which weaknesses were corrected: this figure addresses all weaknesses listed in part a.

Employee Activity Performed (sequential, left-to-right across all rows)

Physician

Front Office

Clerk 2

Office Manager

Front Office

Clerk 3

6

©2018 Pearson Education, Inc.

Open Mail

with another

Office Clerk

Prepare

No

Customer

Remittances

Endorse

Checks &

Prepare

Remittance

List

Monthly

Decide

whether to

grant credit

Review Past

Due A/R &

Issue Credit

Memo

Remittance

List

Monthly

Ch. 12: The Revenue Cycle: Sales to Cash Collections

12.9 Figure 12-20 depicts the activities performed in the revenue cycle by the Newton

Hardware Company. (CPA Examination, adapted)

a. Identify at least 3 weaknesses in Newton Hardware’s revenue cycle. Explain the

resulting threat and suggest methods to correct the weakness.

Weakness Threat/Problem Recommendation

Sales clerk issues credit memos. Sales to customers with

Credit manager should approve

Accountant receives customer

Fraud (lapping). Cash collections clerk should

Cash collections clerk handles

Theft and cover up by

Someone not involved in handling

7

©2018 Pearson Education, Inc.

Accounting Information Systems

b. Identify ways to use IT to streamline Newton’s revenue cycle activities. Describe

the control procedures required in the new system.

Some ways that Newton could use IT to improve efficiency include:

On-line data entry by sales staff. The system should include credit checks on

Controls that should be implemented in the new system include:

Passwords to limit access to authorized users, and to restrict the duties each

employee may perform and which files they may access

8

©2018 Pearson Education, Inc.