CHAPTER 11

AUDITING COMPUTER-BASED INFORMATION SYSTEMS

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

11.1 Auditing an AIS effectively requires that an auditor have some knowledge of computers and

their accounting applications. However, it may not be feasible for every auditor to be a

computer expert. Discuss the extent to which auditors should possess computer expertise to

be effective auditors.

Since most organizations make extensive use of computer-based systems in processing data, it is

essential that computer expertise be available in the organization’s audit group. Such expertise

should include:

Not all auditors need to possess expertise in all of these areas. However, there is certainly some

minimum level of computer expertise that is appropriate for all auditors to have. This would

include:

An understanding of computer hardware, software, accounting applications, and controls.

11.2 Should internal auditors be members of systems development teams that design and

implement an AIS? Why or why not?

Many people believe that internal auditors should be involved in systems development projects in

order to ensure that newly developed systems are auditable and have effective controls. However,

There are indirect forms of auditor involvement that are appropriate. The auditor can

1. Recommend a series of control and audit guidelines that all new systems should meet.

In both cases, the auditor is working through management rather than with the systems

development team.

11-1

©2018 Pearson Education, Inc.

Ch. 11: Auditing Computer-Based Information Systems

11.3 At present, no Berwick employees have auditing experience. To staff its new internal audit

function, Berwick could (a) train some of its computer specialists in auditing, (b) hire

experienced auditors and train them to understand Berwick’s information system, (c) use a

combination of the first two approaches, or (d) try a different approach. Which approach

would you support, and why?

The most effective auditor is a person who has training and experience as an auditor and training

11.4 The assistant finance director for the city of Tustin, California, was fired after city officials

discovered that she had used her access to city computers to cancel her daughter’s $300 water

bill. An investigation revealed that she had embezzled a large sum of money from Tustin in

this manner over a long period. She was able to conceal the embezzlement for so long because

the amount embezzled always fell within a 2% error factor used by the city’s internal

auditors. What weaknesses existed in the audit approach? How could the audit plan be

improved? What internal control weaknesses were present in the system? Should Tustin’s

internal auditors have discovered this fraud earlier?

Audit approach weaknesses

1. The question implies Tustin’s internal auditors never bothered to investigate transactions below

Audit plan improvements

1. Audit software could be used to fully reconcile collections with billings, and list any

Internal control weaknesses

1. An assistant finance director should not have the authority to enter credits to customer

11-2

©2018 Pearson Education, Inc.

Accounting Information Systems

Should the auditors have detected the audit earlier?

The easy answer here is yes; they should have uncovered the fraud earlier. While she was able to

11.5 Lou Goble, an internal auditor for a large manufacturing enterprise, received an anonymous

note from an assembly-line operator who has worked at the company’s West Coast factory for

the past 15 years. The note indicated that there are some fictitious employees on the payroll

as well as some employees who have left the company. He offers no proof or names. What

computer-assisted audit technique could Lou use to help him substantiate or refute the

employee’s claim? (CIA Examination, adapted)

Computer-assisted audit tools and techniques (CAATTs) could have been used to identify employees

11.6. Explain the four steps of the risk-based audit approach, and discuss how they apply to the

overall security of a company.

The risk-based audit approach provides a framework for conducting information system audits. It

consists of the following 4 steps:

1. Determine the threats (fraud and errors) facing the company. This is a list of the accidental or

2. Identify the control procedures that prevent, detect, or correct the threats. These are all the

3. Evaluate control procedures. Controls are evaluated two ways. First, a systems review

4. Evaluate control weaknesses to determine their effect on the nature, timing, or extent of

The risk-based approach provides auditors with a clearer understanding of the overall security of a

company, including the fraud and errors that can occur in the company. It also helps them

11-3

©2018 Pearson Education, Inc.

Ch. 11: Auditing Computer-Based Information Systems

11.7. Compare and contrast the frameworks for auditing program development/acquisition and for

auditing program modification.

The two are similar in that:

They both deal with the review of software.

They both are exposed to the same types of errors and fraud.

They use many of the same control procedures, audit procedures (both systems review and

tests of controls), and compensating controls, except that one set applies to program

The two are dissimilar in that:

The auditor’s role in systems development is to perform an independent review of systems

There are some control procedures, audit procedures (both systems review and tests of

Auditors test for unauthorized program changes, often on a surprise basis, is several ways that

they do not have to test program development and acquisition. These include:

oUsing a source code comparison program to compare the current version of the program

oReprocessing data using the source code and comparing the output with the company’s

oParallel simulation, where the auditor writes a program instead of using the source code

11-4

©2018 Pearson Education, Inc.

Accounting Information Systems

SUGGESTED SOLUTIONS TO THE PROBLEMS

11.1 You are the director of internal auditing at a university. Recently, you met with Issa Arnita,

the manager of administrative data processing, and expressed the desire to establish a more

effective interface between the two departments. Issa wants your help with a new

computerized accounts payable system currently in development. He recommends that your

department assume line responsibility for auditing suppliers’ invoices prior to payment. He

also wants internal auditing to make suggestions during system development, assist in its

installation, and approve the completed system after making a final review.

Would you accept or reject each of the following? Why?

a. The recommendation that your department be responsible for the pre-audit of

supplier’s invoices.

Internal auditing should not assume responsibility for pre-audit of disbursements. Objectivity

is essential to the audit function, and internal auditors should be independent of the activities

b. The request that you make suggestions during system development.

It would be advantageous for internal auditing to make specific suggestions during the design

Determine that there are documentation standards and that they are being followed.

Determine that the project itself is under control and that there is a system for gauging

design progress.

c. The request that you assist in the installation of the system and approve the system after

making a final review.

The auditor must remain independent of any system they will subsequently audit. Therefore,

the auditor must refrain from giving overall approval of the system in final review. The

auditor may help in the installation or conversion of the system by continuing to offer

11-5

©2018 Pearson Education, Inc.

Ch. 11: Auditing Computer-Based Information Systems

11.2 As an internal auditor for the Quick Manufacturing Company, you are participating in the

audit of the company’s AIS. You have been reviewing the internal controls of the computer

system that processes most of its accounting applications. You have studied the company’s

extensive systems documentation. You have interviewed the information system manager,

operations supervisor, and other employees to complete your standardized computer internal

control questionnaire. You report to your supervisor that the company has designed a

successful set of comprehensive internal controls into its computer systems. He thanks you for

your efforts and asks for a summary report of your findings for inclusion in a final overall

report on accounting internal controls.

Have you forgotten an important audit step? Explain. List five examples of specific audit

procedures that you might recommend before reaching a conclusion.

The important audit step that has not been performed is tests of controls (sometimes called

Examples of audit procedures that would be considered tests of controls are:

Observe computer operations, data control procedures, and file library control procedures.

Inquiry of key systems personnel with respect to the way in which prescribed control

procedures are interpreted and implemented. A questionnaire or checklist often facilitates

such inquiry.

11-6

©2018 Pearson Education, Inc.

Accounting Information Systems

11.3 As an internal auditor, you have been assigned to evaluate the controls and operation of a

computer payroll system. To test the computer systems and programs, you submit

independently created test transactions with regular data in a normal production run.

List four advantages and two disadvantages of this technique.

a. Advantages b. Disadvantages

Does not require extensive programming

knowledge

Impractical to test all error

possibilities.

(CIA Examination, adapted)

11-7

©2018 Pearson Education, Inc.

Ch. 11: Auditing Computer-Based Information Systems

11.4 You are involved in the audit of accounts receivable, which represent a significant portion of

the assets of a large retail corporation. Your audit plan requires the use of the computer, but

you encounter the following reactions:

For each situation, state how the auditor should proceed with the accounts receivable audit.

a. The computer operations manager says the company’s computer is running at full

capacity for the foreseeable future and the auditor will not be able to use the system for

audit tests.

b. The computer scheduling manager suggests that your computer program be stored in

the computer program library so that it can be run when computer time becomes

available.

c. You are refused admission to the computer room.

The auditor’s charter should clearly provide for access to all areas and records of the

d. The systems manager tells you that it will take too much time to adapt the auditor’s

computer audit program to the computer’s operating system and that company

programmers will write the programs needed for the audit.

Auditors should insist on using their own computer audit program, since someone at the

(CIA Examination, adapted)

11-8

©2018 Pearson Education, Inc.

Accounting Information Systems

11.5 You are a manager for the CPA firm of Dewey, Cheatem, and Howe (DC&H). While

reviewing your staff’s audit work papers for the state welfare agency, you find that the test

data approach was used to test the agency’s accounting software. A duplicate program copy,

the welfare accounting data file obtained from the computer operations manager, and the test

transaction data file that the welfare agency’s programmers used when the program was

written were processed on DC&H’s home office computer. The edit summary report listing no

errors was included in the working papers, with a notation by the senior auditor that the test

indicates good application controls. You note that the quality of the audit conclusions obtained

from this test is flawed in several respects, and you decide to ask your subordinates to repeat

the test.

Identify three existing or potential problems with the way this test was performed. For each

problem, suggest one or more procedures that might be performed during the revised test to

avoid flaws in the audit conclusions.

Problems Suggested Solutions

Duplicate copy of the program may not be a

Source code comparison.

Programmer’s test data file

Auditor must devise their own test

Audit senior’s conclusion has no basis (no

Must predetermine the result of test data

11-9

©2018 Pearson Education, Inc.

Ch. 11: Auditing Computer-Based Information Systems

11.6 You are performing an information system audit to evaluate internal controls in Aardvark Wholesalers’

(AW) computer system. From an AW manual, you have obtained the following job descriptions for key

personnel:

Director of information systems: Responsible for defining the mission of the information systems

division and for planning, staffing, and managing the IS department.

Manager of systems development and programming: Reports to director of information systems.

Responsible for managing the systems analysts and programmers who design, program, test,

implement, and maintain the data processing systems. Also responsible for establishing and monitoring

documentation standards.

11-10

©2018 Pearson Education, Inc.

Manager of

Manager of

Data Entry

Supervision

Operations

Supervisor

Data Control

Clerk

a. Prepare an organizational chart for AW’s information systems division.

2. What is bad about this organization structure:

The manager of operations is responsible for systems programming, which is a

c. What additional information would you require before making a final judgment on the

adequacy of AW’s separation of functions in the information systems division?

Is access to equipment, files, and documentation restricted and documented?

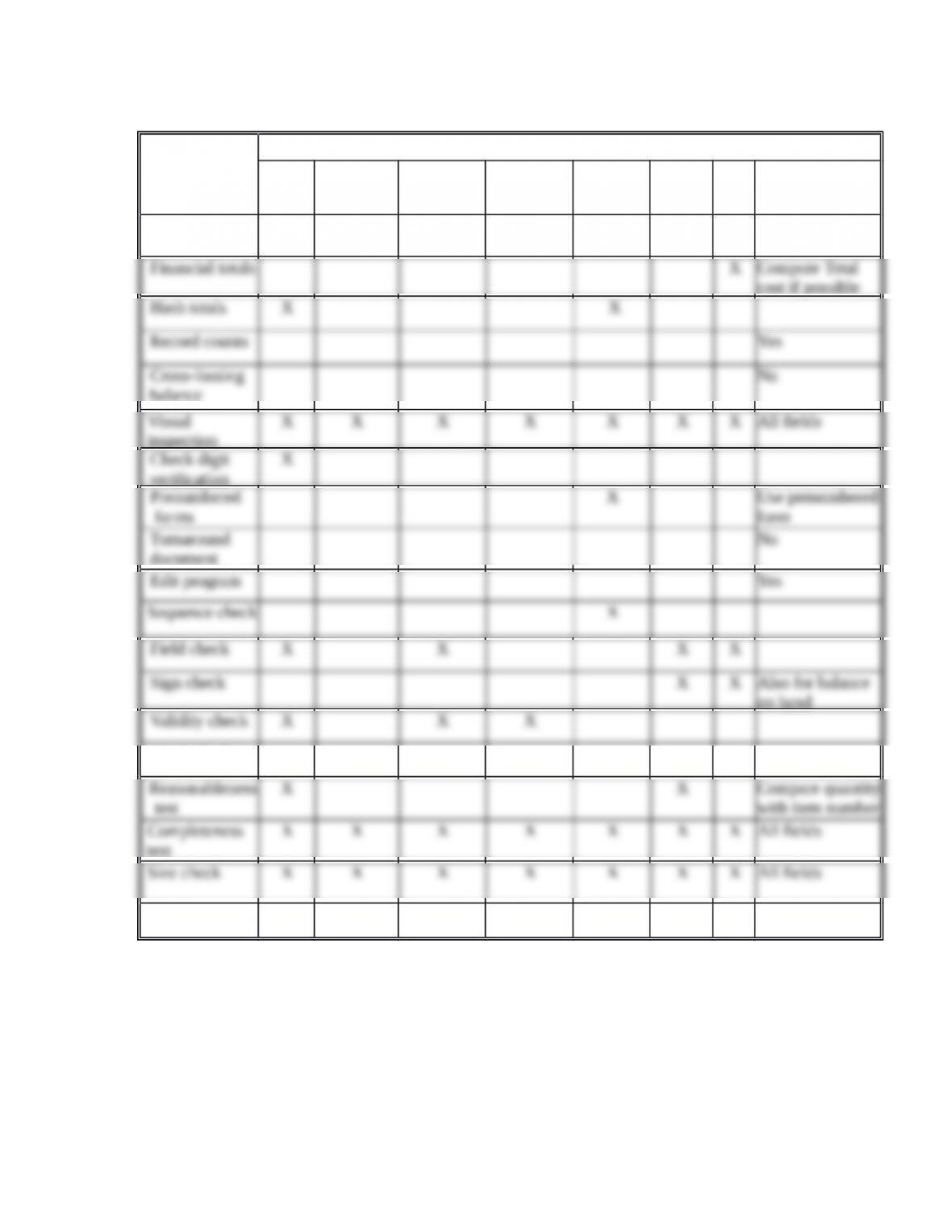

11.7 Robinson’s Plastic Pipe Corporation uses a data processing system for inventory. The input to

this system is shown in Table 11-7. You are using an input controls matrix to help audit the

source data controls.

Table 11-7 Parts Inventory Transaction File

Field Name Field Type

Item number Numeric

Prepare an input controls matrix using the format and input controls shown in Figure 11-3;

11-11

©2018 Pearson Education, Inc.

Ch. 11: Auditing Computer-Based Information Systems

Inventory transactions input control matrix:

RECORD

NAME:

Parts inventory

transactions

FIELD NAMES

Item

number

Description Transaction

date

Transaction

type

Document

number Quantity

Unit

cost Comments

INPUT

CONTROLS:

balance

inspection

verification

Limit check

Other:

11-12

©2018 Pearson Education, Inc.

Accounting Information Systems

11.8 As an internal auditor for the state auditor’s office, you are assigned to review the implementation of a

new computer system in the state welfare agency. The agency is installing an online computer system to

maintain the state’s database of welfare recipients. Under the old system, applicants for welfare

assistance completed a form giving their name, address, and other personal data, plus details about

their income, assets, dependents, and other data needed to establish eligibility. The data are checked by

welfare examiners to verify their authenticity, certify the applicant’s eligibility for assistance, and

determine the form and amount of aid.

Under the new system, welfare applicants enter data on the agency’s Web site or give their data to

clerks, who enter it using online terminals. Each applicant record has a “pending” status until a welfare

examiner can verify the authenticity of the data used to determine eligibility. When the verification is

completed, the examiner changes the status code to “approved,” and the system calculates the aid

amount.

Periodically, recipient circumstances (income, assets, dependents, etc.) change, and the database is

updated. Examiners enter these changes as soon as their accuracy is verified, and the system

recalculates the recipient’s new welfare benefit. At the end of each month, payments are electronically

deposited in the recipient’s bank accounts.

Welfare assistance amounts to several hundred million dollars annually. You are concerned about the

possibilities of fraud and abuse.

a. Describe how to employ concurrent audit techniques to reduce the risks of fraud and

abuse.

Audits should be concerned about a dishonest welfare examiner or unauthorized person

submitting fictitious transactions into the system. Fictitious transactions could cause

The most useful concurrent audit technique to minimize the risk of fraudulent update

transactions would be audit hooks. These program subroutines would review every record

Any welfare application record that is entered into the system by someone other than one

Any welfare record status change or modification that is entered into the system by

Assuming that it takes a minimum of n days for a welfare examiner to verify the

11-13

©2018 Pearson Education, Inc.

Ch. 11: Auditing Computer-Based Information Systems

Any welfare record modification transaction that causes a welfare recipient’s benefits to

Any welfare record that is modified more than two or three times within a short period,

Any record modification transaction that involves a change in the recipient’s address.

Any record entered into the system at a time of day other than during the agency’s normal

Undoubtedly, other useful audit hooks could be identified. The audit staff should

11-14

©2018 Pearson Education, Inc.