a. What is the dollar cost of this debt if the pound depreciates from $2.0260/£ to $1.9460/£ over the year?

b. What is the dollar cost of this debt if the pound appreciates from $2.0260/£ to $2.1640/£ over the year?

Assumptions a) Depreciating £b) Appreciating £

Principal borrowed (British pounds) £5,000,000 £5,000,000

Pound interest rate, one year (percent per annum) 7.375% 7.375%

Beginning of year spot rate, $/£2.0260 2.0260

End of year spot rate, $/£1.9460 2.1640

Calculation of Principal and Interest

Pound-denominated debt, in pounds sterling:

Principal £5,000,000.00 £5,000,000.00

Interest 368,750.00 368,750.00

Principal and interest due at end of year £5,368,750.00 £5,368,750.00

Cost of funds if pound depreciates versus dollar

Repayment cost of pounds, in US dollars (ending spot rate) 10,447,587.50$ 11,617,975.00$

Divided by the US dollar value of initial pound debt proceeds 10,130,000.00$ 10,130,000.00$

(at beginning of period spot rate)

Equals 1.03135 1.14689

Minus 1 1.00000 1.00000

Equals the implied US dollar cost of pound-denominated debt 0.03135 0.14689

US dollar cost of pound (£) debt 3.135% 14.689%

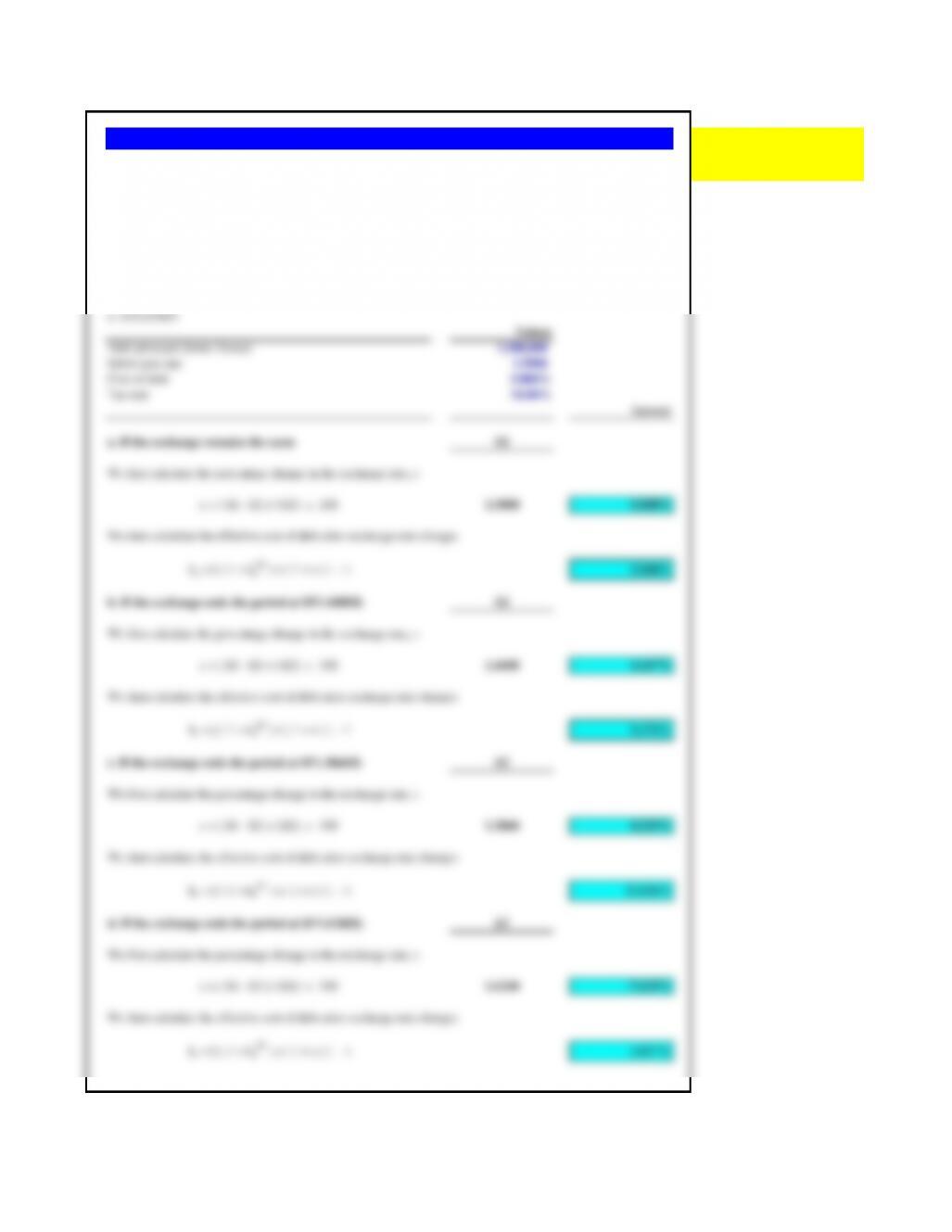

Problem 14.1 Copper Mountain Group (USA)

The Copper Mountain Group, a private equity firm headquartered in Boulder, Colorado (US), borrows £5,000,000 for one year at

7.375% interest.

a. SF1.5000/$

b. SF1.4400/$

c. SF1.3860/$

d. SF1.6240/$

Values

Debt principal (Swiss francs) 1,500,000

Initial spot rate 1.5000

Cost of debt 5.000%

Tax rate 34.00%

Answer

a. If the exchange remains the same S2

We first calculate the percentage change in the exchange rate, s

We then calculate the effective cost of debt after exchange rate changes

b. If the exchange ends the period at SF1.4400/$: S2

We first calculate the percentage change in the exchange rate, s

We then calculate the effective cost of debt after exchange rate changes

c. If the exchange ends the period at SF1.3860/$: S2

We first calculate the percentage change in the exchange rate, s

We then calculate the effective cost of debt after exchange rate changes

d. If the exchange ends the period at SF1.6240/$: S2

We first calculate the percentage change in the exchange rate, s

We then calculate the effective cost of debt after exchange rate changes

Problem 14.2 Foreign Exchange Risk and the Cost of Swiss francs

The chapter demonstrated that a firm borrowing in a foreign currency could potentially end up paying a very

different effective rate of interest than what it expected. Using the same baseline values of a debt principal of

SF1.5 million, a one year period, an initial spot rate of SF1.5000/$, a 5.000% cost of debt, and a 34% tax rate,

what is the effective cost of debt for one year for a U.S. dollar-based company if the exchange rate at the end of

the period was:

does NOT match problem

given in the textbook

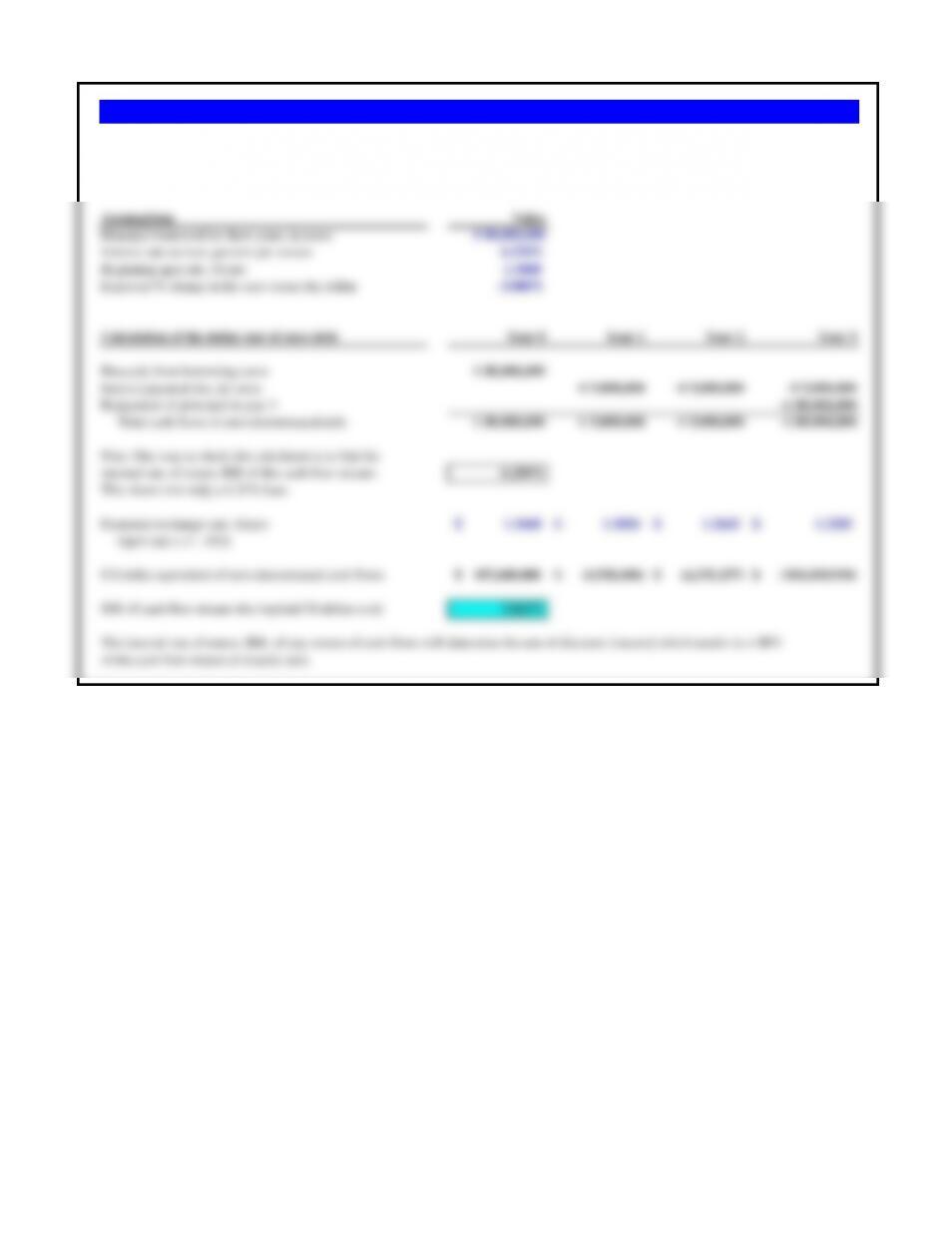

Assumptions Value

Principal borrowed for three years, in euros € 80,000,000

Interest rate on loan, percent per annum 6.250%

Beginning spot rate, $/euro 1.3460

Expected % change in the euro versus the dollar -3.000%

Calculation of the dollar cost of euro debt Year 0 Year 1 Year 2 Year 3

Proceeds from borrowing euros € 80,000,000

Interest payment due, in euros -€ 5,000,000 -€ 5,000,000 -€ 5,000,000

Repayment of principal in year 3 -€ 80,000,000

Total cash flows of euro-denominated debt € 80,000,000 -€ 5,000,000 -€ 5,000,000 -€ 85,000,000

Note: One way to check this calculaton is to find the

internal rate of return, IRR of this cash flow stream: 6.250%

This shows it is truly a 6.25% loan.

Expected exchange rate, $/euro 1.3460$ 1.3056$ 1.2665$ 1.2285$

(spot rate x (1 – .03))

US dollar equivalent of euro-denominated cash flows 107,680,000$ (6,528,100)$ (6,332,257)$ (104,418,918)$

IRR of cash flow stream (the implied US dollar cost) 3.063%

The internal rate of return, IRR, of any stream of cash flows will determine the rate of discount (interest) which results in a NPV

of the cash flow stream of exactly zero.

Problem 14.3 McDougan Associates (USA)

McDougan Associates, a U.S.-based investment partnership, borrows €80,000,000 at a time when the exchange rate is $1.3460/€. The entire

principal is to be repaid in three years, and interest is 6.250% per annum, paid annually in euros. The euro is expected to depreciate vis à vis

the dollar at 3% per annum. What is the effective cost of this loan for McDougan?

a. Borrow US$25,000,000 in Eurodollars in London at 7.250% per annum

Assumptions Value

Working capital debt needed for one year 5,000,000$

Borrowing US dollars in London:

Interest rate, percent per annum 7.250%

Principal borrowed 5,000,000$

Borrow Hong Kong dollars in Hong Kong

Interest rate, percent per annum 7.000%

Initial spot rate, HK$/US$ 7.8000

Principal borrowed 39,000,000

Calculation of the breakeven exchange rate

Cost of repaying the Hong Kong dollar loan in HK$ 41,730,000

Cost of repaying the US dollar loan in US$ 5,362,500$

Breakeven exchange rate (HK$ cost/US$ cost) 7.7818

Breakeven is the equivalent of “indifferent.”

Problem 14.4 Morning Star Air (China)

Morning Star Air, headquartered in Kunming, China, needs US$25,000,000 for one year to finance

working capital. The airline has two alternatives for borrowing:

b. Borrow HK$39,000,000 in Hong Kong at 7.00% per annum, and exchange these Hong Kong dollars

at the present exchange rate of HK$7.8/US$ for U.S. dollars.

At what ending exchange rate would Morning Star Air be indifferent between borrowing U.S. dollars and

borrowing Hong Kong dollars?

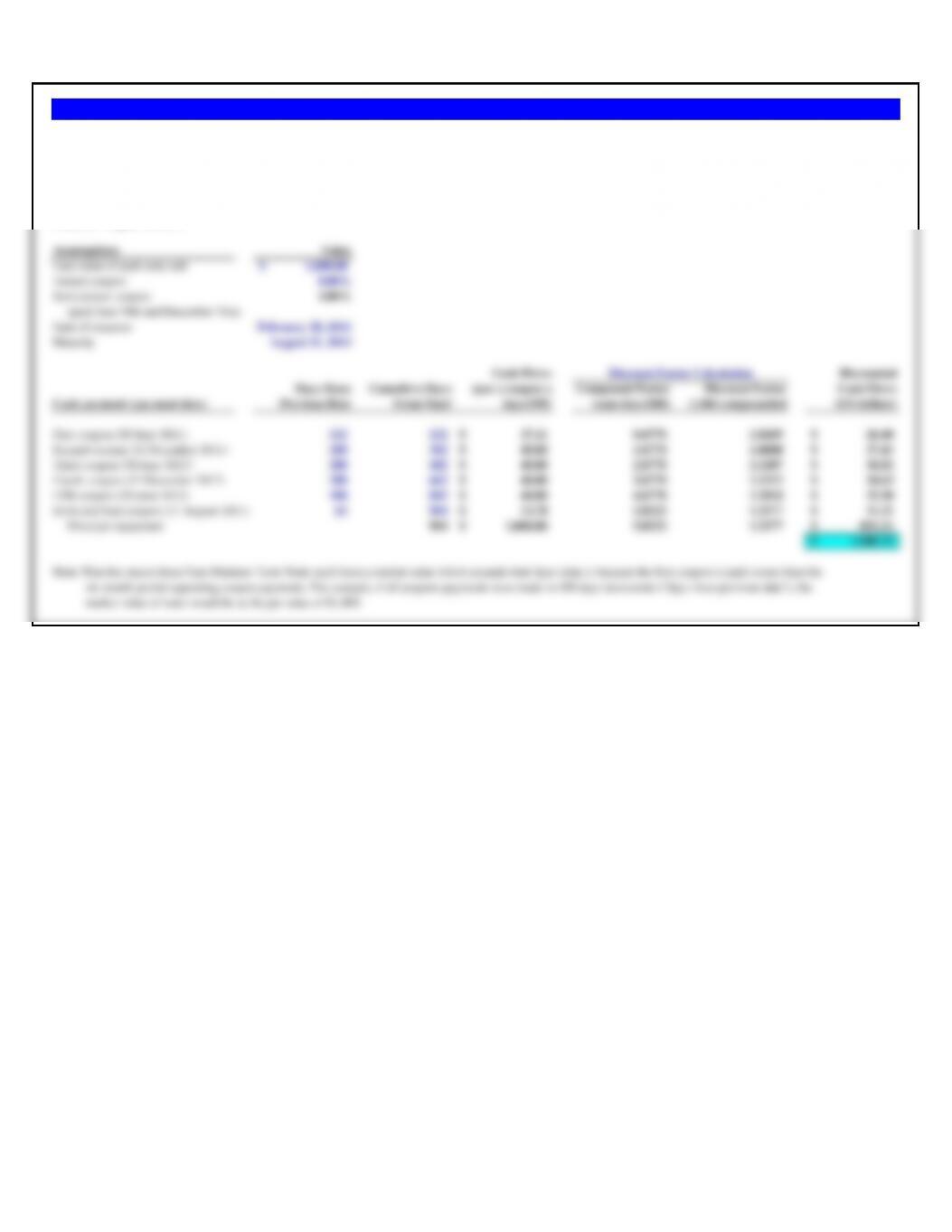

Coupon rate: 8.00% payable semiannually on June 30 and December 31

Date of issuance: February 28, 2011

Maturity: August 31, 2013

Assumptions Value

Face value of each note sold 1,000.00$

Annual coupon 8.00%

Semi-annual coupon 4.00%

(paid June 30th and December 31st)

Date of issuance February 28, 2011

Maturity August 31, 2013

Cash Flows Discounted

Days Since Cumultive Days (par x coupon x Compound Factor Discount Factor Cash Flows

Cash payment (payment date) Previous Date From Start days/180) (cum days/180) (1.04) compounded (US dollars)

First coupon (30 June 2011) 122 122 27.11$ 0.6778 1.0269 26.40$

Second coupon (31 December 2011) 180 302 40.00$ 1.6778 1.0680 37.45$

Third coupon (30 June 2012) 180 482 40.00$ 2.6778 1.1107 36.01$

Fourth coupon (31 December 2012) 180 662 40.00$ 3.6778 1.1552 34.63$

Fifth coupon (30 June 2013) 180 842 40.00$ 4.6778 1.2014 33.30$

Sixth and final coupon (31 August 2013) 62 904 13.78$ 5.0222 1.2177 11.31$

Principal repayment 904 1,000.00$ 5.0222 1.2177 821.21$

1,000.31$

Note: That the reason these Euro Medium Term Notes each have a market value which exceeds their face value is because the first coupon is paid sooner than the

six month period separating coupon payments. For example, if all coupons payments were made in 180 days increments (“days since previous date”), the

market value of notes would be at the par value of $1,000.

Problem 14.5 Pantheon Capital, S.A.

If Pantheon Capital, S.A., is raising funds via a medium-term euronote with the following characteristics, how much in dollars will Pantheon receive for each $1,000 note sold?

Coupon rate: 8.00% payable semiannually on June 30 and December 31

Discount Factor Calculation

Assumptions Value

Principal of Euro Commercial Paper issuance 2,000,000$

Maturity (days) 60

Yield to maturity at issuance 6.000%

Proceeds of issuance Value

Face value 2,000,000.00$

Discount rate (1 + ((days/360) x (ytm))) 1.01000

Proceeds equal (Face value / Discount rate) 1,980,198.02$

Problem 14.6 Westminster Insurance Company

Westminster Insurance Company plans to sell $2,000,000 of euro-commercial paper

with a 60-day maturity and discounted to yield 4.60% per annum. What will be the

immediate proceeds to Westminster Insurance?

Assumption Value

Tax rate 30.00%

10-year euro bonds (euros) € 6,000,000

20-year yen bonds (yen) 750,000,000

Spot rate ($/euro) 1.2400

Spot rate ($/pound) 1.8600

Spot rate (yen/$) 109.00

Weighted

US Dollar Pre-tax Post-tax Component

Component Amount Proportion Cost (%) Cost (%) Cost (%)

25 year US dollar bonds 10,000,000$ 12.77% 6.000% 4.200% 0.5363%

5 year US dollar euronotes 4,000,000 5.11% 4.000% 2.800% 0.1430%

10 year euro bonds 7,440,000 9.50% 5.000% 3.500% 0.3325%

20 year yen bonds 6,880,734 8.79% 2.000% 1.400% 0.1230%

Shareholders’ equity 50,000,000 63.84% 20.000% 20.000% 12.7680%

Total 78,320,734$ 100.00% WACC = 13.9027%

The component coupon costs (for example the 6% coupon on the 25-year US dollar bonds) are the same as the current yields to maturity that would be

needed to sell similar bonds in the marketplace today. Current yields to maturity is the proper rate to use. The interest costs used for the euro and yen

bonds reflect actual expected interest costs after any exchange rate changes. This calculation assumes there is no expected change in the exchange rate

over the life of the debt issue (which is indeed highly unlikely).

Problem 14.7 Sunrise Manufacturing, Inc.

Sunrise Manufacturing, Inc, a U.S. multinational company, has the following debt components in its consolidated capital section. Sunrise’s finance

staff estimates their cost of equity to be 20%. Current exchange rates are also listed below.

Income taxes are 30% around the world after allowing for credits. Calculate Sunrise’s weighted average cost of capital. Are any assumptions implicit

in your calculation?

Initial Issuance Value

Principal borrowed for six years, in US$ 650,000,000$

Issuance fees 1.20%

Interest Costs First 6-months 2nd 6-months

LIBOR 4.000% 4.200%

Spread over LIBOR 0.800% 0.800%

Total interest cost 4.800% 5.000%

Calculation of the effective cost of funds Issuance First 6-months 2nd 6-months

Face value of syndicated loan 650,000,000$

less fees for issuance (7,800,000)

Net proceeds of syndicated loan 642,200,000$

Interest payment due at end of 6-month period (15,600,000)$ (16,250,000)$

(annual rate divided by 2 for 6-month period)

Total interest payments in first year of loan (31,850,000)$

Effective interest cost (interest payment/proceeds) 4.960%

Problem 14.8 Petrol Ibérico

Petrol Ibérico, a European gas company, is borrowing US$650,000,000 via a syndicated eurocredit for 6 years at 80 basis points over

LIBOR. LIBOR for the loan will be reset every six months. The funds will be provided by a syndicate of eight leading investment

bankers, which will charge up-front fees totaling 1.2% of the principal amount. What is the effective interest cost for the first year if

LIBOR is 4.00% for the first six months and 4.20% for the second six months?

Assumptions Value

A-Malaysia (in ringgits):

Long-term debt 11,400,000

Shareholders’ equity 15,200,000

A-Mexico (in pesos):

Long-term debt 20,000,000

Shareholders’ equity 60,000,000

Adamantine Architectonics (non-consolidated)

Investment in subsidiaries (US dollars):

in A-Malaysia 4,000,000$

in A-Mexico 6,000,000$

Parent long-term debt 12,000,000$

Common stock 5,000,000$

Retained earnings 20,000,000$

Current exchange rates:

Malaysian ringgit per dollar (RM/$) 3.80

Mexican pesos per dollar (Ps/$) 10.00

Consolidated Balance Sheet (US$) Value Percent

Debt:

Malaysian ringgit debt (RM converted to US$) 3,000,000$

Mexican peso debt (Ps converted to US$) 2,000,000

Parent company debt 12,000,000

Consolidated long-term debt 17,000,000$ 40.48%

Shareholders’ equity (common + retained) 25,000,000$ 59.52%

Total capital 42,000,000$ 100.00%

Problem 14.9 Adamantine Architectonics

Adamantine Architectonics consists of a U.S. parent and wholly owned subsidiaries in Malaysia (A-Malaysia)

and Mexico (A-Mexico). Selected portions of their non-consolidated balance sheets, translated into U.S. dollars,

are shown below.

What are the debt and equity proportions in Adamantine’s consolidated balance sheet?

Note that the equity accounts of the subsidiaries are matched by “investment in subsidiaries” asset account held

in the non-consolidated books of the parent company. In consolidation these two accounts cancel each other out.

Petrobrás of Brazil: Estimating its Weighted Average Cost of Capital

Problems 10-15. Petrobras of Brazil

Petrobrás Petróleo Brasileiro S.A. or Petrobras is the national oil company of Brazil. It is publicly

traded, but the government of Brazil holds the controlling share. It is the largest company in the

Southern Hemisphere by market capitalization and the largest in all of Latin America. As an oil

company, the primary product of its production has a price set on global markets—the price of

oil—and much of its business is conducted the global currency of oil, the U.S. dollar. Problems

10–15 examine a variety of different financial institutions’ attempts to estimate the company’s cost

Petrobrás Lukoil

Capital Cost Components (Brazil) (Russia)

Risk Free Rate 4.800% 4.800%

Sovereign Risk 7.000% 3.000%

Equity Risk Premium 4.500% 5.700%

Market Cost of Equity 16.300% 13.500%

Beta (relevered) 0.87 1.04

Cost of equity 18.981% 18.840%

Cost of Debt 8.400% 6.800%

Tax rate 28.000% 28.000%

Cost of debt, after-tax 6.048% 4.896%

Debt/Capital ratio 33.300% 47.500%

Equity/Capital ratio 66.700% 52.500%

WACC (calculated) 14.674% 12.217%

WACC (I-Bank report) 14.700% 12.300%

JPMorgan’s Latin American Equity Research department produced the following WACC

calculation for Petrobrás of Brazil versus Lukoil of Russia in their June 18, 2004 report.

Evaluate the methodology and assumptions used in the calculation. Assume a 28% tax rate

for both companies.

This approach applies the sovereign risk premium to the cost of equity for both companies,

but not to their cost of debt. Since the comparison is for two oil companies from two

different countries, and the same risk free rate is used for both, it is implied, though not

stated, that the WACC calculation is based in US dollars.

Source: “Petrobras: A Diamond in the Rough,” JP Morgan, Latin American Equity Research, June 18,

2004, p. 24.

Problem 14.10 JPMorgan

Capital Cost Components 2004

Risk Free Rate 4.500%

Levered Beta 0.99

Market Premium 6.000%

Country Risk Premium 5.500%

Cost of equity (US$) 15.940%

Exchange Rate 2.000%

Cost of equity (R$) 18.259%

Cost of Debt 8.600%

Tax rate 34.000%

Cost of debt, after-tax (R$) 5.676%

Debt/Capital ratio 40.000%

Equity/Capital ratio 60.000%

WACC (R$) calculated 13.23%

WACC (R$) (I-bank report) 13.20%

Source: “Petrobras: Reinitiation of Coverage,” UNIBANCO, August 12, 2004, p.4.

UNIBANCO estimated the weighted average cost of capital for Petrobrás to be

13.2% in Brazilian reais in August of 2004. Evaluate the methodology and

assumptions used in the calculation.

This calculation adds the country risk premium to the risk free rate in the cost of

equity, but not the cost of debt (as was the case in the previous problem). This cost

of equity in US$, however, is then compounded by a percentage change in the

expected exchange rate of the reais against the dollar to arrive at a cost of equity in

reais. The cost of debt, which indicates reais-denomination, is not adjusted for the

country risk premium or the expected currency movement.

Problem 14.11 UNIBANCO

Capital Cost Components 2003A 2004E 2003A 2004E

Risk free rate 9.400% 9.400% 9.000% 9.000%

Levered Beta 1.07 1.09 1.08 1.10

Risk Premium 5.500% 5.500% 5.500% 5.500%

Cost of equity 15.285% 15.395% 14.940% 15.050%

Cost of debt 8.400% 8.400% 9.000% 9.000%

Tax rate 28.500% 27.100% 28.500% 27.100%

Cost of debt, after-tax 6.006% 6.124% 6.435% 6.561%

Debt/capital ratio 32.700% 32.400% 32.700% 32.400%

Equity/capital ratio 67.300% 67.600% 67.300% 67.600%

WACC 12.20% 12.30% 12.10% 12.30%

WACC (calculated) 12.25% 12.39% 12.16% 12.30%

Source: “Petrobras,” Citigroup SmithBarney, March 8, 2005, and July 28, 2005.

This approach uses a relatively high assumed value for the risk free rate of interest in the cost of equity calculation, without

expressly charging the company a country risk premium. Since the U.S. dollar risk-free rate at this time was somewhere around

4%, this risk-free rate must implicitly include a country risk premium. The cost of debt, before-tax, is actually below the risk-

free rate, which is difficult to understand or rationalize.

Problem 14.12 Citigroup SmithBarney (dollar)

Citigroup regularly performs a U.S. dollar-based discount cash flow (DCF) valuation of Petrobrás in its coverage. That DCF

analysis requires the use of a discount rate which they base on the company’s weighted average cost of capital. Evaluate the

methodology and assumptions used in the 2003 Actual and 2004 Estimates of Petrobras’s WACC below.

July 28, 2005

March 8, 2005

Petrobras Cost of Equity June 2003

Risk-free rate (Brazilian C-Bond) 9.90%

Petrobras levered beta (β) 1.40

Market risk premium 5.50%

Cost of equity 17.60%

Petrobras Cost of Debt

Petrobras cost of debt 10.00%

Brazilian corporate tax rate 34.00%

Cost of debt, after-tax 6.60%

WACC Calculation (in R$)

Petrobras cost of debt, after-tax 6.60%

Long-term debt ratio (% of capital) 50.60%

Petrobras cost of equity 17.60%

Long-term equity ratio (% of capital) 49.40%

WACC (I-bank report) 12.00%

WACC (calculated) 12.03%

Source: “Petroleo Brasileiro S.A.,Citigroup Smith Barney, June 17, 2003, p.17.

In a report dated June 17, 2003, Citigroup SmithBarney calculated a WACC for

Petrobrás denominated in Brazilian reais (R$). Evaluate the methodology and

assumptions used in this cost of capital calculation.

Identifying the risk-free rate as the Braizilian C-Bond rate, and using a relatively

high value of beta compared to other analyst estimates, the cost of equity is

relatively high. The cost of debt, also high compared to the other estimates,

results in a final WACC calculation, in Brazilian reais, which is similar in value

to other estimates.

Problem 14.13 Citigroup SmithBarney (Reais)

Cost of Capital Component 2003 Estimate 2004 Estimate

US 10-year risk-free rate (in US$) 4.10% 4.40%

Country risk premium (in US$) 6.00% 4.00%

Petrobras premium “adjustment” 1 -1.00% -1.00%

Petrobras risk-free rate (in US$) 9.10% 7.40%

Petrobras Cost of Equity

Petrobras risk-free rate (in US$) 9.10% 7.40%

Petrobras beta (β) 0.80 0.80

Market risk premium (in US$) 6.00% 6.00%

Cost of equity (in US$) 2 13.90% 12.20%

Projected 10-year currency devaluation 2.50% 2.00%

Cost of equity (in R$) 3 16.75% 14.44%

Petrobras Cost of Debt

Petrobras cost of debt (in R$) 8.50% 8.50%

Brazilian corporate tax rate 35.00% 35.00%

Cost of debt, after-tax (in US$) 5.53% 5.53%

WACC Calculation (in R$)

Petrobras cost of debt, after-tax 5.53% 5.53%

Long-term debt ratio (% of capital) 31.00% 28.00%

Petrobras cost of equity 16.75% 14.44%

Long-term equity ratio (% of capital) 69.00% 72.00%

WACC (calculated) 13.27% 11.95%

WACC (I-Bank report) 13.30% 12.00%

Notes:

Problem 14.14 BBVA Investment Bank

BBVA utilized a rather innovative approach to dealing with both country and currency risk in their December

20, 2004 report on Petrobras. Evaluate the methodology and assumptions used in this cost of capital calculation.

This analysis clearly begins with a U.S. dollar-based risk-free rate, 4.1% and 4.4%, adds a country risk premium

to it, and then adjusts the sum downward for a Petrobras premium. The Petrobras premium is the analyst’s

opinion that Petrobras is an oil and gas company, and therefore operates in a global dollar market which is in

many ways less risky than a pure-play on a Brazilian firm. The resulting cost of equity is then converted from

reais to dollars with the application of a currency devaluation multiplier, a stated average expectation for the

coming decade.The cost of debt assumed is very low –– 5.53% — which is clearly a dollar cost and not a reais

cost as stated. The final WACC in reais terms is roughly equivalent to the various estimates from the previous

problems.

1 Petrobras premium adjustment is the reduction in country risk given an oil and gas company operating in a global industry

which operates in a market of US dollar denominated returns.

Source: “Petrobras,” BBVA Securities, Latin American Research, December 20, 2004, p. 7.

JPMorgan Citigroup ($) UNIBANCO Citigroup (R$) BBVA

Capital Cost Components (June 18, 2004) (March 8, 2005) (Aug 12, 2004) (June 17, 2003) (Dec 20, 2004)

Risk Free Rate 4.800% 9.400% 4.500% 9.900% 4.400%

Sovereign/Country Risk Premium 7.000% 0.000% 5.500% 0.000% 4.000%

Petrobras Company Premium 0.000% 0.000% 0.000% 0.000% -1.000%

“Adjusted” Risk Free Rate 11.800% 9.400% 10.000% 9.900% 7.400%

Levered Beta 0.87 1.09 0.99 1.40 0.80

Market/Equity Risk Premium 4.500% 5.500% 6.000% 5.500% 6.000%

Cost of equity (US$) 18.981% 15.395% 15.940% 17.600% 12.200%

Exchange Rate 2.000% 0.000% 2.000%

Cost of equity (R$) 18.259% 17.600% 14.444%

Cost of Debt 8.400% 8.400% 8.600% 10.000% 8.500%

Tax rate 28.000% 27.100% 34.000% 34.000% 35.000%

Cost of debt, after-tax 6.048% 6.124% 5.676% 6.600% 5.525%

Debt/Capital ratio 33.300% 32.400% 40.000% 50.600% 28.000%

Equity/Capital ratio 66.700% 67.600% 60.000% 49.400% 72.000%

WACC (calculated) 14.7% 12.4% 13.2% 12.0% 11.9%

WACC (I-bank report) 14.7% 12.3% 13.2% 12.0% 12.0%

The various estimates of the cost of capital for Petrobras of Brazil appear to be very different, but are they? Reorganize your answers to Problem 14.11 through 14.14 into those

costs of capital which are in U.S. dollars versus Brazilian reais. Use the estimates for 2004 as the basis of comparison.

U.S. dollar WACCs

Brazilian reais WACCs

Problem 14.15 Petrobras’s WACC Comparison

Which course of action do you recommend Grupo Modelo take and why?

Japanese euro US dollar

Alternatives yen bonds bonds bonds

Coupon rate 3.000% 7.000% 5.000%

Current spot rate, yen/$ 106.00 1.1960$

Expected change in the value of the foreign currency 2.000% -2.000% 0.000%

Principal needed by Grupo Modelo 100,000,000$

Calculation of the dollar cost debt alternatives Year 0 Year 1 Year 2 Year 3 Year 4

Japanese yen bonds:

Proceeds and principal and interest payments 10,600,000,000 (318,000,000) (318,000,000) (318,000,000) (10,918,000,000)

Expected exchange rate (yen/$) 106.00 103.92 101.88 99.89 97.93

US dollar equivalent in expected cash flows 100,000,000$ (3,060,000)$ (3,121,200)$ (3,183,624)$ (111,490,512)$

IRR of US$ cash flow stream (cost of funds) 5.060%

euro-denominated bonds:

Proceeds and principal and interest payments € 83,612,040 -€ 5,852,843 -€ 5,852,843 -€ 5,852,843 -€ 89,464,883

Expected exchange rate (yen/$) 1.1960 1.1721 1.1486 1.1257 1.1032

US dollar equivalent in expected cash flows 100,000,000$ (6,860,000)$ (6,722,800)$ (6,588,344)$ (98,693,393)$

IRR of US$ cash flow stream (cost of funds) 4.860%

US dollar bonds:

Proceeds and principal and interest payments 100,000,000$ (5,000,000)$ (5,000,000)$ (5,000,000)$ (105,000,000)$

IRR of US$ cash flow stream (cost of funds) 5.000%

Given the expected exchange rate changes, the euro-denominated bonds have the lowest all-in-cost of funds for the Mexico-based company, Grupo Modelo.

(Note that it is the expected changes in exchange rates which determine this outcome. In the event that all currencies were expected to remain fixed, an expected

change of 0%, then the Japanese yen bonds are clearly the cheapest source of capital.)

c. Sell U.S. dollar bonds at par yielding 5% per annum.

Problem 14.16 Grupo Modelo S.B.A de C.V.

Grupo Modelo, a brewery out of Mexico that exports such well-known varieties as Corona, Modelo and Pacifico, is Mexican by incorporation. However, the company evaluates all

business results, including financing costs, in U.S. dollars. The company needs to borrow $10,000,000 or the foreign currency equivalent for four years. For all issues, interest is

payable once per year, at the end of the year. Available alternatives are:

b. Sell euro-denominated bonds at par yielding 7% per annum. The current exchange rate is $1.1960/€, and the euro is expected to weaken against the dollar by 2% per annum.

a. Sell Japanese yen bonds at par yielding 3% per annum. The current exchange rate is ¥106/$, and the yen is expected to strengthen against the dollar by 2% per annum.