Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Translated Translated

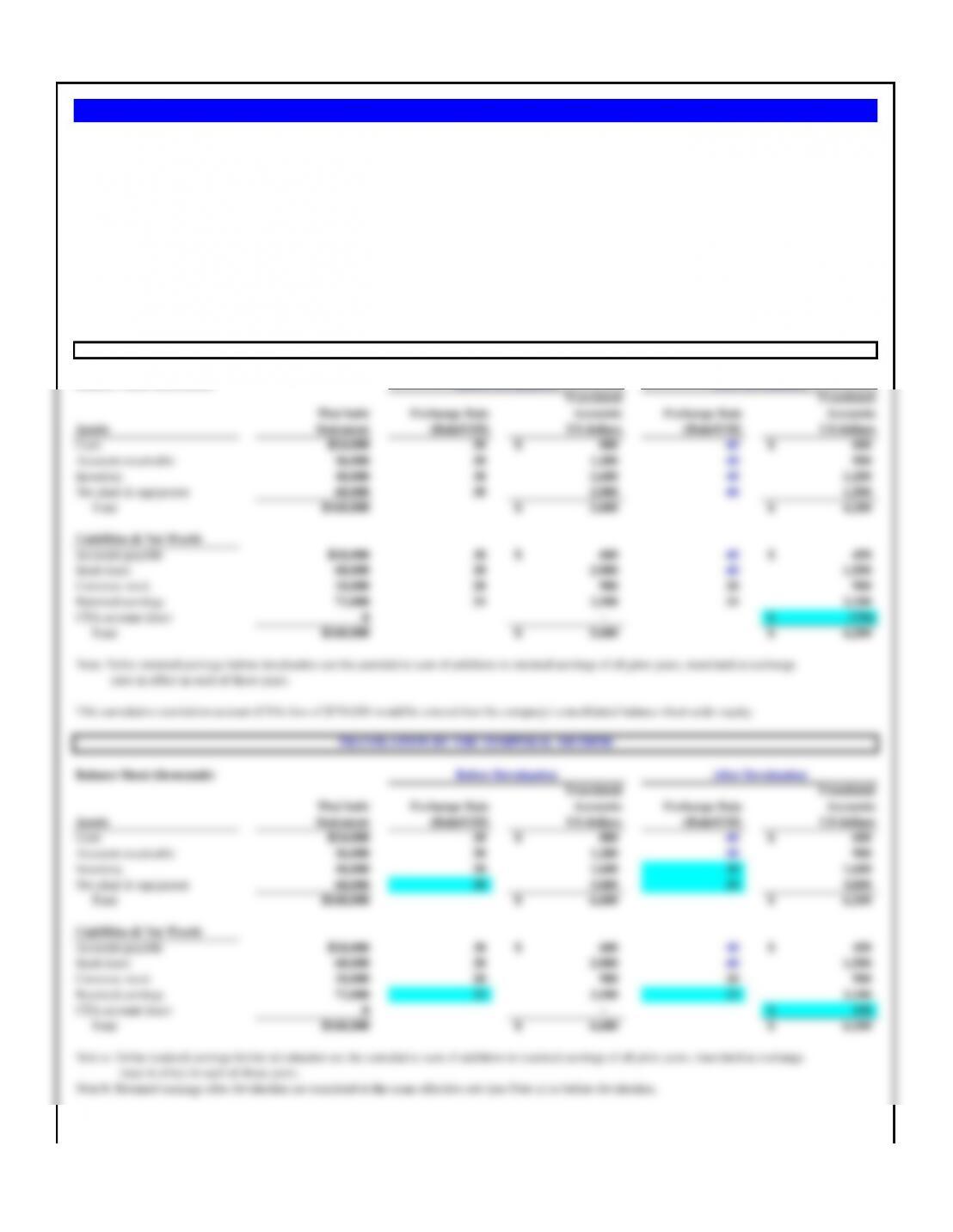

Euros Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (US$/euro) US dollars (US$/euro) US dollars

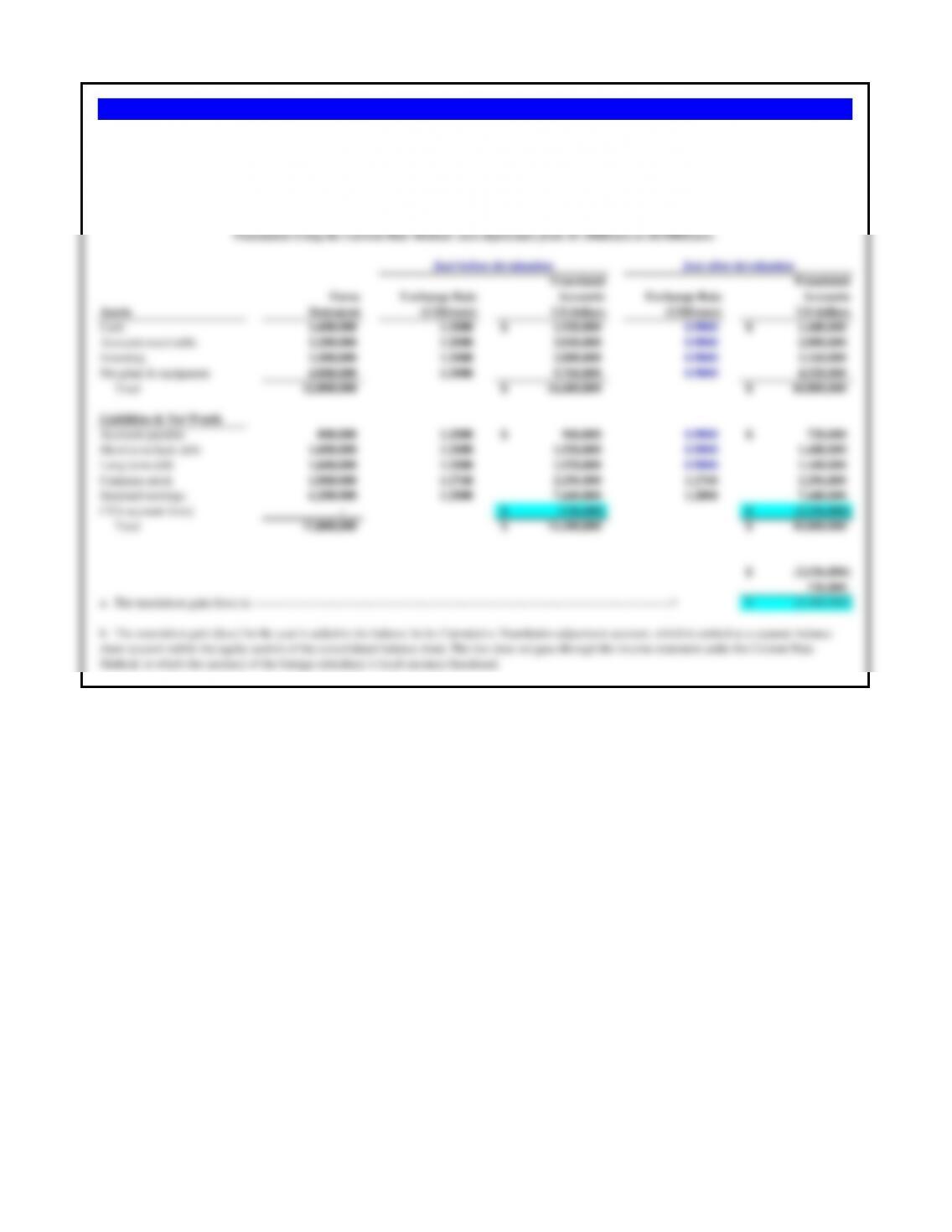

Cash 1,600,000 1.2000 1,920,000$ 0.9000 1,440,000$

Accounts receivable 3,200,000 1.2000 3,840,000 0.9000 2,880,000

Inventory 2,400,000 1.2000 2,880,000 0.9000 2,160,000

Net plant & equipment 4,800,000 1.2000 5,760,000 0.9000 4,320,000

Total 12,000,000 14,400,000$ 10,800,000$

Liabilities & Net Worth

Accounts payable 800,000 1.2000 960,000$ 0.9000 720,000$

Short-term bank debt 1,600,000 1.2000 1,920,000 0.9000 1,440,000

Long-term debt 1,600,000 1.2000 1,920,000 0.9000 1,440,000

Common stock 1,800,000 1.2760 2,296,800 1.2760 2,296,800

Retained earnings 6,200,000 1.2000 7,440,000 1.2000 7,440,000

CTA account (loss) - (136,800)$ (2,536,800)$

Total 12,000,000 14,400,000$ 10,800,000$

(2,536,800)$

136,800

a. The translation gain (loss) is ----------------------------------------------------------------------------------------------------------------> (2,400,000)$

b. The translation gain (loss) for the year is added to the balance in the Cumulative Translation adjustment account, which is carried as a separate balance

sheet account within the equity section of the consolidated balance sheet. The loss does not pass through the income statement under the Current Rate

Method, in which the currency of the foreign subsidiary is local currency functional.

Problem 11.1 Ganado Europe (A)

Using facts in the chapter for Ganado Europe, assume the exchange rate on January 2, 2006, in Exhibit 11.4 dropped in value from $1.2000/€ to $0.9000/€

(rather than to $1.0000/€). Recalculate Ganado Europe’s translated balance sheet for January 2, 2006 with the new exchange rate using the current rate

method.

a. What is the amount of translation gain or loss?

b. Where should the translation gain or loss appear in the financial statements?

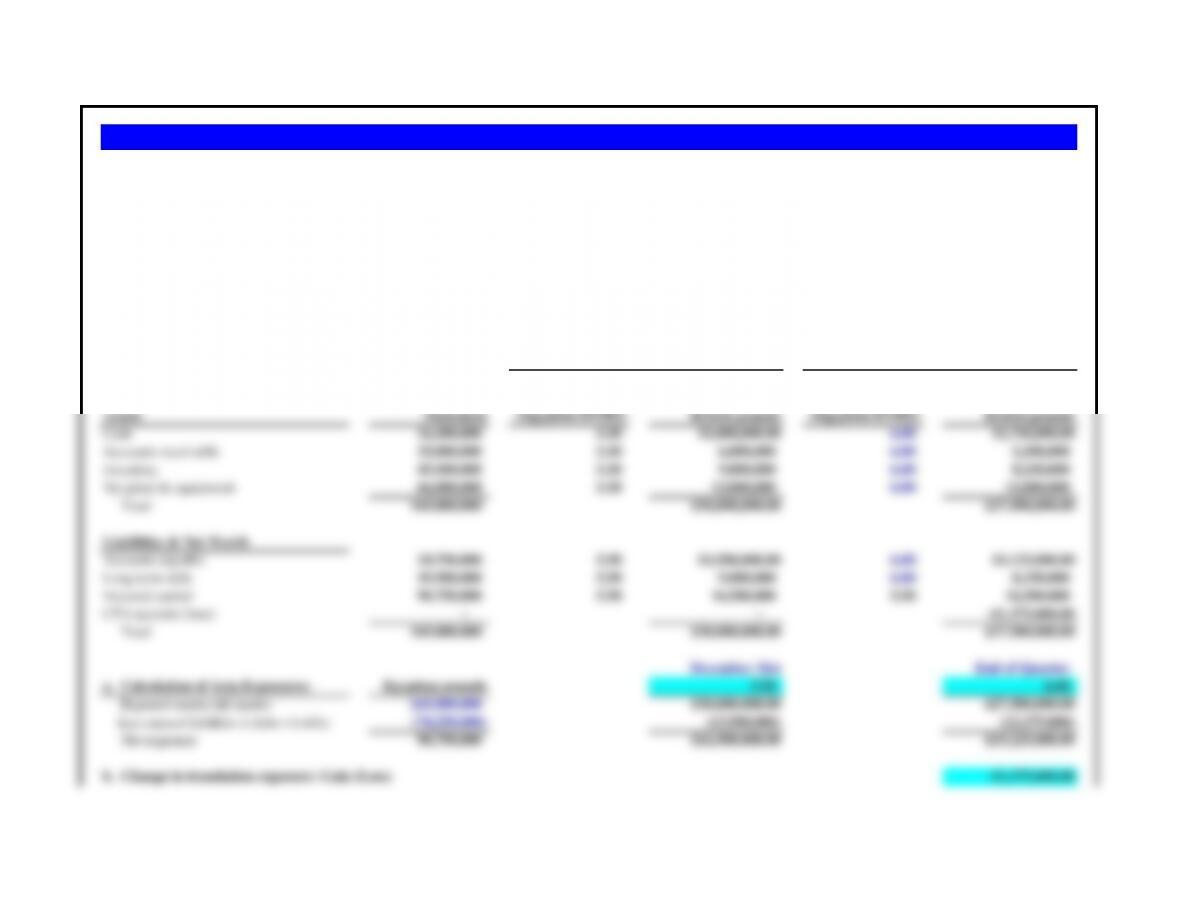

Translation Using the Current Rate Method: euro depreciates from $1.2000/euro to $0.9000/euro.

Just before devaluation

Just after devaluation

Translated Translated

Euros Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (US$/euro) (US dollars) (US$/euro) (US dollars)

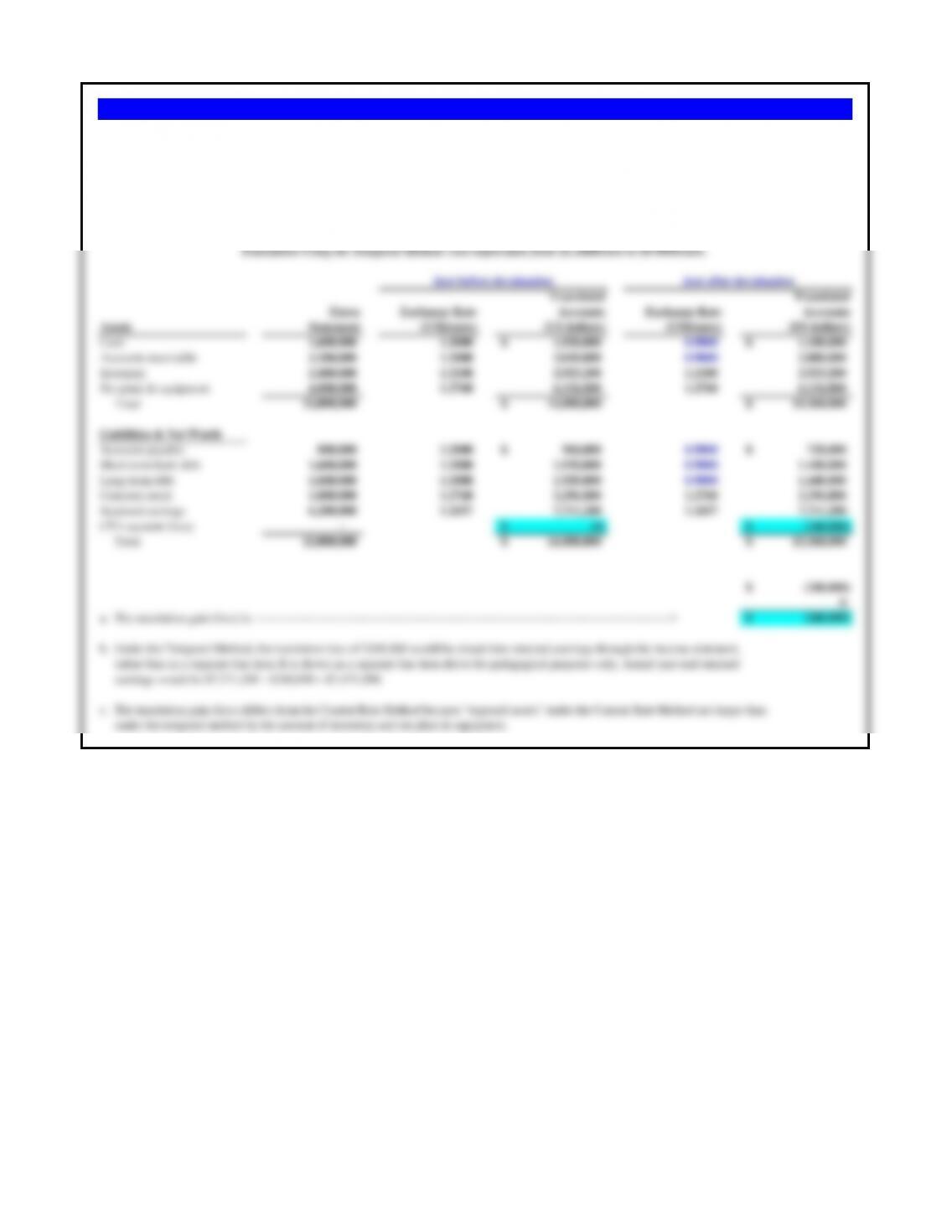

Cash 1,600,000 1.2000 1,920,000$ 0.9000 1,440,000$

Accounts receivable 3,200,000 1.2000 3,840,000 0.9000 2,880,000

Inventory 2,400,000 1.2180 2,923,200 1.2180 2,923,200

Net plant & equipment 4,800,000 1.2760 6,124,800 1.2760 6,124,800

Total 12,000,000 14,808,000$ 13,368,000$

Liabilities & Net Worth

Accounts payable 800,000 1.2000 960,000$ 0.9000 720,000$

Short-term bank debt 1,600,000 1.2000 1,920,000 0.9000 1,440,000

Long-term debt 1,600,000 1.2000 1,920,000 0.9000 1,440,000

Common stock 1,800,000 1.2760 2,296,800 1.2760 2,296,800

Retained earnings 6,200,000 1.2437 7,711,200 1.2437 7,711,200

CTA account (loss) - (0)$ (240,000)$

Total 12,000,000 14,808,000$ 13,368,000$

(240,000)$

0

a. The translation gain (loss) is: ---------------------------------------------------------------------------------------------------------------> (240,000)$

b. Under the Temporal Method, the translation loss of $240,000 would be closed into retained earnings through the income statement,

rather than as a separate line item. It is shown as a separate line item above for pedagogical purposes only. Actual year-end retained

earnings would be $7,711,200 - $240,000 = $7,471,200.

c. The translation gain (loss) differs from the Current Rate Method because "exposed assets" under the Current Rate Method are larger than

under the temporal method by the amount of inventory and net plant & equipment.

Problem 11.2 Ganado Europe (B)

Using facts in the chapter for Ganado Europe, assume as in question Ganado Europe (A) that the exchange rate on January 2, 2006, in Exhibit 11.4 dropped

in value from $1.2000/€ to $0.9000/€ (rather than to $1.0000/€). Recalculate Ganado Europe’s translated balance sheet for January 2, 2006 with the new

exchange rate using the temporal rate method.

Translation Using the Temporal Method: euro depreciates from $1.2000/euro to $0.9000/euro.

Just before devaluation

Just after devaluation

a. What is the amount of translation gain or loss?

b. Where should it appear in the financial statements?

c. Why does the translation loss or gain under the temporal method differ from the loss or gain under the current rate method?

a. What is the amount of translation gain or loss?

b. Where should it appear in the financial statements?

Translated Translated

Euros Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (US$/euro) US dollars (US$/euro) US dollars

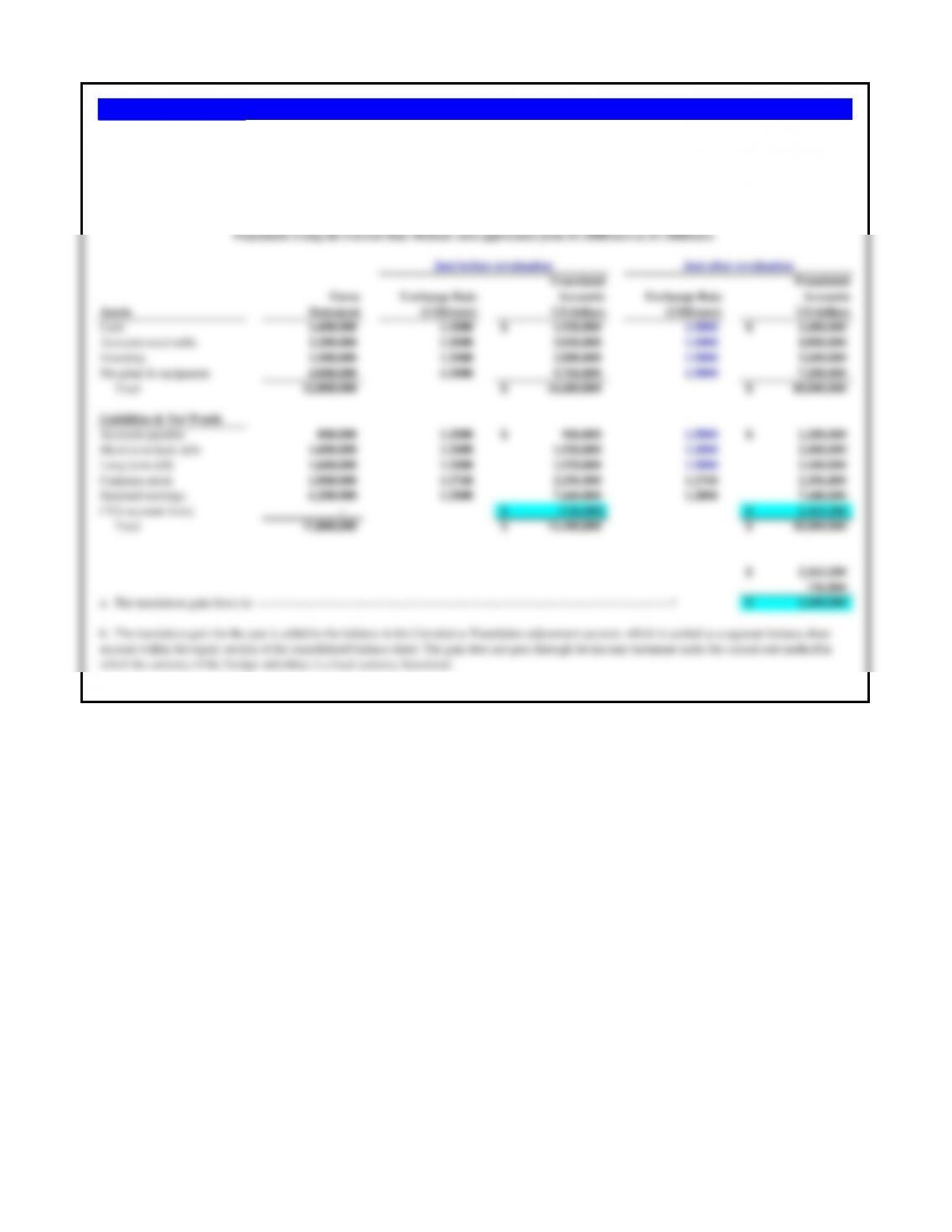

Cash 1,600,000 1.2000 1,920,000$ 1.5000 2,400,000$

Accounts receivable 3,200,000 1.2000 3,840,000 1.5000 4,800,000

Inventory 2,400,000 1.2000 2,880,000 1.5000 3,600,000

Net plant & equipment 4,800,000 1.2000 5,760,000 1.5000 7,200,000

Total 12,000,000 14,400,000$ 18,000,000$

Liabilities & Net Worth

Accounts payable 800,000 1.2000 960,000$ 1.5000 1,200,000$

Short-term bank debt 1,600,000 1.2000 1,920,000 1.5000 2,400,000

Long-term debt 1,600,000 1.2000 1,920,000 1.5000 2,400,000

Common stock 1,800,000 1.2760 2,296,800 1.2760 2,296,800

Retained earnings 6,200,000 1.2000 7,440,000 1.2000 7,440,000

CTA account (loss) - (136,800)$ 2,263,200$

Total 12,000,000 14,400,000$ 18,000,000$

2,263,200$

136,800

a. The translation gain (loss) is: ---------------------------------------------------------------------------------------------------------------> 2,400,000$

b. The translation gain for the year is added to the balance in the Cumulative Translation adjustment account, which is carried as a separate balance sheet

account within the equity section of the consolidated balance sheet. The gain does not pass through the income statement under the current rate method in

which the currency of the foreign subsidiary is a local currency functional.

Using facts in the chapter for Ganado Europe, assume the exchange rate on January 2, 2006, in Exhibit 11.4 appreciated from $1.2000/€ to $1.500/€.

Calculate Ganado Europe's translated balance sheet for January 2, 2006 with the new exchange rate using the current rate method.

Problem 11.3 Ganado Europe ( C )

Translation Using the Current Rate Method: euro appreciates from $1.2000/euro to $1.5000/euro.

Just before revaluation

Just after revaluation

a. What is the amount of translation gain or lose?

b. Where should it appear in the financial statements?

Translated Translated

Euros Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (US$/euro) (US dollars) (US$/euro) (US dollars)

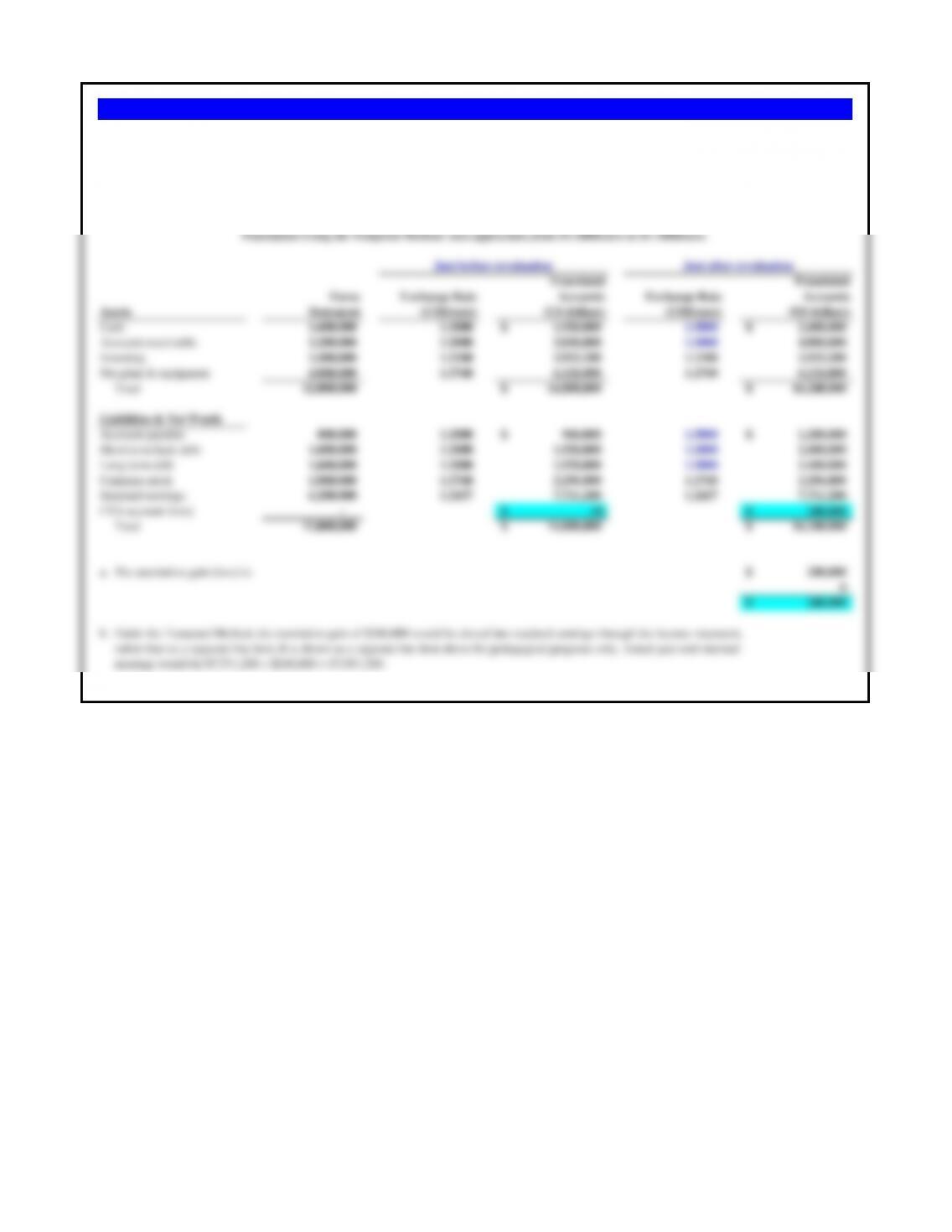

Cash 1,600,000 1.2000 1,920,000$ 1.5000 2,400,000$

Accounts receivable 3,200,000 1.2000 3,840,000 1.5000 4,800,000

Inventory 2,400,000 1.2180 2,923,200 1.2180 2,923,200

Net plant & equipment 4,800,000 1.2760 6,124,800 1.2760 6,124,800

Total 12,000,000 14,808,000$ 16,248,000$

Liabilities & Net Worth

Accounts payable 800,000 1.2000 960,000$ 1.5000 1,200,000$

Short-term bank debt 1,600,000 1.2000 1,920,000 1.5000 2,400,000

Long-term debt 1,600,000 1.2000 1,920,000 1.5000 2,400,000

Common stock 1,800,000 1.2760 2,296,800 1.2760 2,296,800

Retained earnings 6,200,000 1.2437 7,711,200 1.2437 7,711,200

CTA account (loss) - (0)$ 240,000$

Total 12,000,000 14,808,000$ 16,248,000$

a. The translation gain (loss) is: 240,000$

0

240,000$

b. Under the Temporal Method, the translation gain of $240,000 would be closed into retained earnings through the income statement,

rather than as a separate line item. It is shown as a separate line item above for pedagogical purposes only. Actual year-end retained

earnings would be $7,711,200 + $240,000 = $7,951,200.

Problem 11.4 Ganado Europe (D)

Using facts in the chapter for Ganado Europe, assume as in Ganado Europe (C) that the exchange rate on January 2, 2006, in Exhibit 11.4 appreciated from

$1.2000/€ to $1.5000/€. Calculate Ganado Europe’s translated balance sheet for January 2, 2006 with the new exchange rate using the temporal method.

Translation Using the Temporal Method: euro appreciates from $1.2000/euro to $1.5000/euro.

Just before revaluation

Just after revaluation

Balance Sheet (thousands of pesos Uruguayo, $U)

Exchange Rate

Assets January 1st ($U/US$)

Cash 60,000 20.00

Accounts receivable 120,000 20.00

Inventory 120,000 20.00

Net plant & equipment 240,000 20.00

540,000

Liabilities & Net Worth

Current liabilities 30,000 20.00

Long-term debt 90,000 20.00

Capital stock 300,000 15.00

Retained earnings 120,000 15.00

540,000

b) Translation

January 1st

$U/US$

Calculation of Accounting Exposures: $U (000s) 20.00

Exposed assets (all assets) 540,000 27,000$

Less exposed liabilities (curr liabs + lt debt) (120,000) (6,000)

a) Net exposure 420,000 21,000$

b. Calculate Tristan Narvaja, S.A.'s contribution to its parent's translation loss if the exchange rate on

December 31st is $U20/US$. Assume all peso Uruguayo accounts remain as they were at the beginning of

Problem 11.5 Tristan Narvaja, S.A. (A)

Tristan Narvaja, S.A., is the Uruguayan subsidiary of a U.S. manufacturing company. Its balance sheet for

January 1 follows. The January 1st exchange rate between the U.S. dollar and the peso Uruguayo ($U) is

$U20/$.

a. Determine Tristan Narvaja’s contribution to the translation exposure of its parent on January 1, using the

current rate method.

Balance Sheet (thousands of pesos Uruguayo, $U)

Exchange Rate

Assets January 1st ($U/US$)

Cash 60,000 22.00

Accounts receivable 120,000 22.00

Inventory 120,000 22.00

Net plant & equipment 240,000 22.00

540,000

Liabilities & Net Worth

Current liabilities 30,000 22.00

Long-term debt 90,000 22.00

Capital stock 300,000 15.00

Retained earnings 120,000 15.00

540,000

January 1st

$U/US$

Calculation of Accounting Exposures: $U (000s) 22.00

Exposed assets (all assets) 540,000 24,545$

Less exposed liabilities (curr liabs + lt debt) (120,000) (5,455)

Net exposure 420,000 19,091$

Problem 11.6 Tristan Narvaja, S.A. (B)

Calculate Tristan Narvaja’s contribution to its parent’s translation loss if the exchange rate on December

31st is $U22/$. Assume all peso accounts remain as they were at the beginning of the year.

Balance Sheet (thousands of pesos Uruguayo, $U)

Exchange Rate

Assets January 1st ($U/US$)

Cash 60,000 12.00

Accounts receivable 120,000 12.00

Inventory 120,000 12.00

Net plant & equipment 240,000 12.00

540,000

Liabilities & Net Worth

Current liabilities 30,000 12.00

Long-term debt 90,000 12.00

Capital stock 300,000 15.00

Retained earnings 120,000 15.00

540,000

January 1st

$U/US$

Calculation of Accounting Exposures: $U (000s) 12.00

Exposed assets (all assets) 540,000 45,000$

Less exposed liabilities (curr liabs + lt debt) (120,000) (10,000)

Net exposure 420,000 35,000$

Problem 11.7 Tristan Narvaja, S.A. (C)

Calculate Tristan Narvaja’s contribution to its parent’s translation gain or loss using the current rate

method if the exchange rate on December 31 is $U12/$. Assume all peso accounts remain as they were at

the beginning of the year.

Exchange rates for translating Bangkok Instruments' balance sheet into U.S. dollars are:

B40.00/$ April 1st exchange rate after 25% devaluation

B30.00/$ March 31st exchange rate, before 25% devaluation. All inventory was acquired at this rate.

B20.00/$ Historic exchange rate at which plant and equipment were acquired

Balance Sheet (thousands)

Translated Translated

Thai baht Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (Baht/US$) US dollars (Baht/US$) US dollars

Cash ฿24,000 30 800$ 40 600$

Accounts receivable 36,000 30 1,200 40 900

Inventory 48,000 30 1,600 40 1,200

Net plant & equipment 60,000 30 2,000 40 1,500

Total ฿168,000 5,600$ 4,200$

Liabilities & Net Worth

Accounts payable ฿18,000 30 600$ 40 450$

Bank loans 60,000 30 2,000 40 1,500

Common stock 18,000 20 900 20 900

Retained earnings 72,000 34 2,100 34 2,100

CTA account (loss) 0 - (750)$

Total ฿168,000 5,600$ 4,200$

Note: Dollar retained earnings before devaluation are the cumulative sum of additions to retained earnings of all prior years, translated at exchange

rates in effect in each of those years.

This cumulative translation account (CTA) loss of $750,000 would be entered into the company's consolidated balance sheet under equity.

Balance Sheet (thousands)

Translated Translated

Thai baht Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (Baht/US$) US dollars (Baht/US$) US dollars

Cash ฿24,000 30 800$ 40 600$

Accounts receivable 36,000 30 1,200 40 900

Inventory 48,000 30 1,600 30 1,600

Net plant & equipment 60,000 20 3,000 20 3,000

Total ฿168,000 6,600$ 6,100$

Liabilities & Net Worth

Accounts payable ฿18,000 30 600$ 40 450$

Bank loans 60,000 30 2,000 40 1,500

Common stock 18,000 20 900 20 900

Retained earnings 72,000 23 3,100 23 3,100

CTA account (loss) 0 - 150$

Total ฿168,000 6,600$ 6,100$

Note a: Dollar retained earnings before devaluation are the cumulative sum of additions to retained earnings of all prior years, translated at exchange

rates in effect in each of those years.

Note b: Retained earnings after devaluation are translated at the same effective rate (see Note a) as before devaluation.

The translation gain of $150,000 would be passed-through to the consolidated income statement.

TRANSLATION BY THE TEMPORAL METHOD

Before Devaluation

After Devaluation

Problem 11.8 Bangkok Instruments, Ltd (A)

Bangkok Instruments, Ltd., the Thai subsidary of a U.S. corporation, is a seismic instrument manufacturer. Bangkok Instruments manufactures the instruments

primarily for the oil and gas industry globally, though with recent commodity price increases of all kinds -- including copper -- its business has begun to grow

rapidly. Sales are primarily to multinational companies based in the United States and Europe. Bankok Instruments' balance sheet in thousands of Thai bahts (B)

as of March 31st is as follows.

The Thai baht dropped in value from B30/$ to B40/$ between March 31st and April 1st. Assuming no change in balance sheet accounts between these two days,

calculate the gain or loss from translation by both the current rate method and the temporal method. Explain the translation gain or loss in terms of changes in the

value of exposed accounts.

TRANSLATION BY THE CURRENT RATE METHOD

Before Devaluation

After Devaluation

The Temporal Method results in a translation gain, as opposed to the CTA loss found under the Current Rate Method, because of the different

exchange rates used against Net plant & equipment and the inventory line items. This gain would be impossible under the Current Rate

Method because ALL assets are exposed under that method, whereas the Temporal Method carries Net plant & equipment and inventory

at relevant historical exchange rates.

EXPLANATION OF DIFFERENT OUTCOME BY TRANSLATION METHODOLOGY

Balance Sheet (thousands)

Translated Translated

Thai baht Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (Baht/US$) US dollars (Baht/US$) US dollars

Cash ฿24,000 30 800$ 25 960$

Accounts receivable 36,000 30 1,200 25 1,440

Inventory 48,000 30 1,600 25 1,920

Net plant & equipment 60,000 30 2,000 25 2,400

Total ฿168,000 5,600$ 6,720$

Liabilities & Net Worth

Accounts payable ฿18,000 30 600$ 25 720$

Bank loans 60,000 30 2,000 25 2,400

Common stock 18,000 20 900 20 900

Retained earnings 72,000 34 2,100 34 2,100

CTA account (loss) 0 - 600$

Total ฿168,000 5,600$ 6,720$

Note: Dollar retained earnings before devaluation are the cumulative sum of additions to retained earnings of all prior years, translated at exchange

rates in effect in each of those years.

This cumulative translation account (CTA) gain of $600,000 would be entered into the company's consolidated balance sheet under equity.

Balance Sheet (thousands)

Translated Translated

Thai baht Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (Baht/US$) US dollars (Baht/US$) US dollars

Cash ฿24,000 30 800$ 25 960$

Accounts receivable 36,000 30 1,200 25 1,440

Inventory 48,000 30 1,600 30 1,600

Net plant & equipment 60,000 20 3,000 20 3,000

Total ฿168,000 6,600$ 7,000$

Liabilities & Net Worth

Accounts payable ฿18,000 30 600$ 25 720$

Bank loans 60,000 30 2,000 25 2,400

Common stock 18,000 20 900 20 900

Retained earnings 72,000 23 3,100 23 3,100

CTA account (loss) 0 - (120)$

Total ฿168,000 6,600$ 7,000$

Note a: Dollar retained earnings before devaluation are the cumulative sum of additions to retained earnings of all prior years, translated at exchange

rates in effect in each of those years.

Note b: Retained earnings after devaluation are translated at the same effective rate (see Note a) as before devaluation.

The translation loss of $120,000 would be passed-through to the consolidated income statement.

The Temporal Method results in a translation gain, as opposed to the CTA loss found under the Current Rate Method, because of the different

exchange rates used against Net plant & equipment and the inventory line items. This gain would be impossible under the Current Rate

Method because ALL assets are exposed under that method, whereas the Temporal Method carries Net plant & equipment and inventory

at relevant historical exchange rates.

Before Devaluation

After Devaluation

EXPLANATION OF DIFFERENT OUTCOME BY TRANSLATION METHODOLOGY

Problem 11.9 Bangkok Instruments, Ltd (B)

Using the original data provided for Bangkok Instruments, assume that the Thai baht appreciated in value from B30/$ to B25/$ between March 31 and April 1.

Assuming no change in balance sheet accounts between those two days, calculate the gain or loss from translation by both the current rate method and the

temporal method. Explain the translation gain or loss in terms of changes in the value of exposed accounts.

TRANSLATION BY THE CURRENT RATE METHOD

Before Devaluation

After Devaluation

TRANSLATION BY THE TEMPORAL METHOD

Balance Sheet of Cairo Ingot, Ltd. Translated Translated

Egyptian pounds Exchange Rate Accounts Exchange Rate Accounts

Assets Statement (Egyptian £/UK£)British pounds (Egyptian £/UK£)British pounds

Cash 16,500,000 5.50 £3,000,000.00 6.00 £2,750,000.00

Accounts receivable 33,000,000 5.50 6,000,000 6.00 5,500,000

Inventory 49,500,000 5.50 9,000,000 6.00 8,250,000

Net plant & equipment 66,000,000 5.50 12,000,000 6.00 11,000,000

Total 165,000,000 £30,000,000.00 £27,500,000.00

Liabilities & Net Worth

Accounts payable 24,750,000 5.50 £4,500,000.00 6.00 £4,125,000.00

Long-term debt 49,500,000 5.50 9,000,000 6.00 8,250,000

Invested capital 90,750,000 5.50 16,500,000 5.50 16,500,000

CTA account (loss) - - -£1,375,000.00

Total 165,000,000 £30,000,000.00 £27,500,000.00

December 31st End of Quarter

a. Calculation of Actg Exposures: Egyptian pounds 5.50 6.00

Exposed assets (all assets) 165,000,000 £30,000,000.00 £27,500,000.00

Less exposed liabilities (c.liabs + lt debt)

(74,250,000) (13,500,000) (12,375,000)

Net exposure 90,750,000 £16,500,000.00 £15,125,000.00

b. Change in translation exposure: Gain (Loss) -£1,375,000.00

Problem 11.10 Cairo Ingot, Ltd.

Before Exchange Rate Change

After Exchange Rate Change

Cairo Ingot, Ltd., is the Egyptian subsidiary of Trans-Mediterranean Aluminum, a British multinational that fashions automobile engine blocks from aluminum. Trans-

Mediterranean’s home reporting currency is the British pound. Cairo Ingot’s December 31st balance sheet is shown below. At the date of this balance sheet the exchange

rate between Egyptian pounds and British pounds sterling was £E5.50/UK£.

a. What is Cairo Ingot’s contribution to the translation exposure of Trans-Mediterranean on December 31st, using the current rate method?

b. Calculate the translation exposure loss to Trans-Mediterranean if the exchange rate at the end of the following quarter is £E6.00/£. Assume all balance sheet accounts

are the same at the end of the quarter as they were at the beginning.

Alternatively, the translation loss arising from the fall in the value of the Egyptian pound can be found as follows:

Net exposed assets (£)£16,500,000.00

Percentage change in the value of the British pound -8.3%

Translation gain (loss) -£1,375,000.00