Assumptions 3-Month T-Bill 6-Month T-Bill

Treasury bill, face value $10,000.00 $10,000.00

Price at sale $9,993.93 $9,976.74

a. Discount on sale $6.07 $23.26

b. Simple yield 0.0607% 0.2331%

c. Annualized yield 0.2432% 0.4668%

The interest yields on U.S. Treasury securities in early 2009 fell to very low levels as a

result of the combined events surrounding the global financial crisis. Calculate the simple

and annualized yields for the 3-month and 6-month Treasury bills auctioned on March 9,

2009 listed here.

Discount on sale is the difference between the face value of the security and the price it is

sold at auction.

Simple yield is found by dividing the discount (the dollar return to the investor on maturity)

by the price paid on purchase.

Annualized yield is found by compounding the simple yield by the number of periods per

year. In this case a 3-month T-Bill is assumed to have a 90 day maturity within a 360 day

interest rate year (U.S. dollar practices).

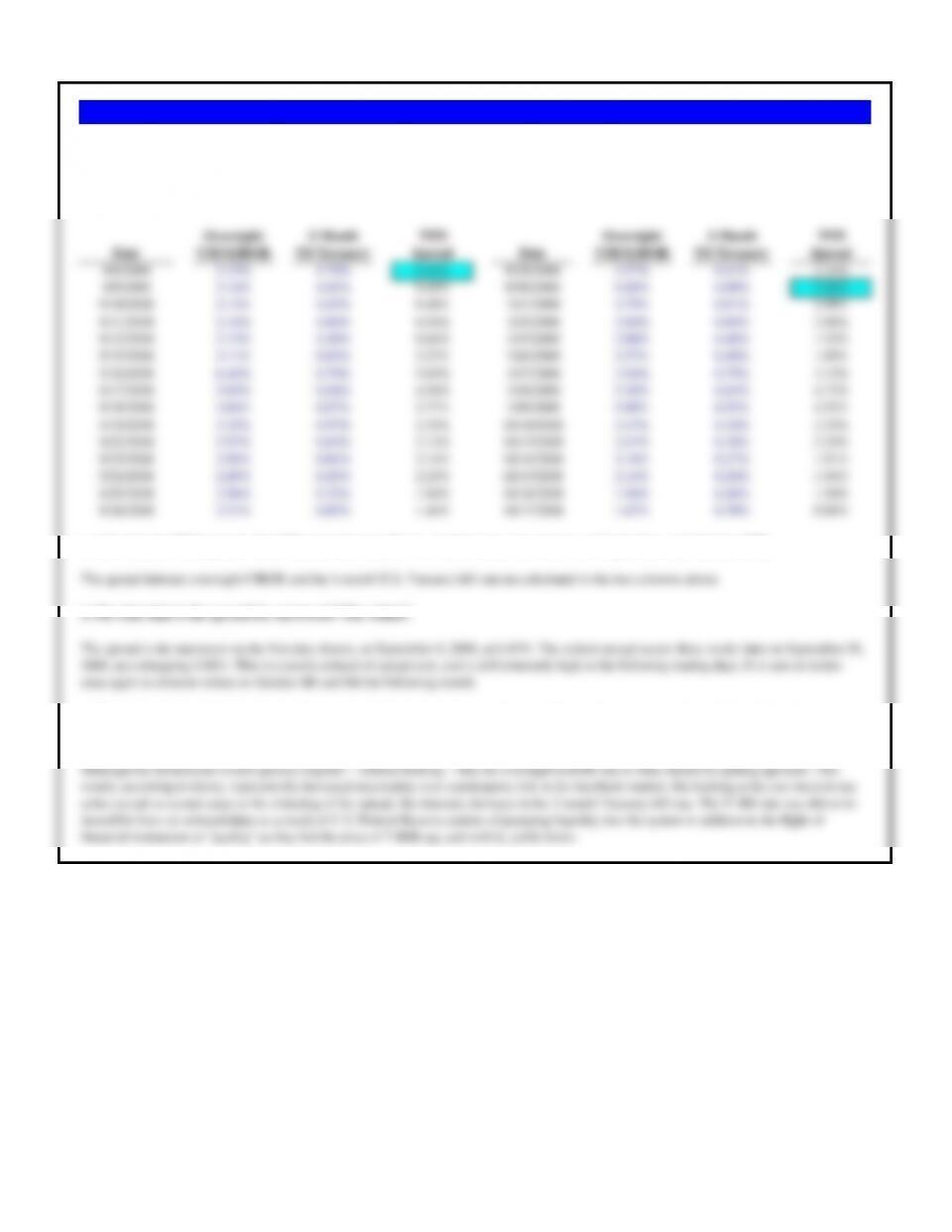

Problem 8.1 U.S. Treasury Bill Auction Rates – March 2009

Overnight 3-Month TED Overnight 3-Month TED

Date USD LIBOR US Treasury Spread Date USD LIBOR US Treasury Spread

9/8/2008 2.15% 1.70% 0.45% 9/29/2008 2.57% 0.41% 2.16%

9/9/2008 2.14% 1.65% 0.49% 9/30/2008 6.88% 0.89% 5.98%

9/10/2008 2.13% 1.65% 0.48% 10/1/2008 3.79% 0.81% 2.98%

9/11/2008 2.14% 1.60% 0.54% 10/2/2008 2.68% 0.60% 2.08%

9/12/2008 2.15% 1.49% 0.66% 10/3/2008 2.00% 0.48% 1.52%

9/15/2008 3.11% 0.83% 2.27% 10/6/2008 2.37% 0.48% 1.89%

9/16/2008 6.44% 0.79% 5.65% 10/7/2008 3.94% 0.79% 3.15%

9/17/2008 5.03% 0.04% 4.99% 10/8/2008 5.38% 0.65% 4.73%

9/18/2008 3.84% 0.07% 3.77% 10/9/2008 5.09% 0.55% 4.55%

9/19/2008 3.25% 0.97% 2.29% 10/10/2008 2.47% 0.18% 2.29%

9/22/2008 2.97% 0.85% 2.12% 10/13/2008 2.47% 0.18% 2.29%

9/23/2008 2.95% 0.81% 2.14% 10/14/2008 2.18% 0.27% 1.91%

9/24/2008 2.69% 0.45% 2.24% 10/15/2008 2.14% 0.20% 1.94%

9/25/2008 2.56% 0.72% 1.84% 10/16/2008 1.94% 0.44% 1.50%

9/26/2008 2.31% 0.85% 1.46% 10/17/2008 1.67% 0.79% 0.88%

a. Calculate the TED spread – the difference between the two market rates shown here – in September and October 2008.

The spread between overnight LIBOR and the 3-month U.S. Treasury bill rate are calculated in the two columns above.

b. On what date is the spread the narrowest? The widest?

Problem 8.2 Credit Crisis, 2008

During financial crises, short-term interest rates, particularly the extremely short-term interest rates, will often change quickly (typically up) as

indications that markets are under severe stress. The interest rates shown here are for selected dates in September and October 2008. Different

publications define the TED Spread different ways, but one measure is the differential between the overnight LIBOR interest rate and the 3-month

U.S. Treasury bill rate.

The spread is the narrowest on the first date shown, on September 8, 2008, at 0.45%. The widest spread occurs three weeks later on September 30,

2008, at a whopping 5.98%. This is a nearly unhead of spread size, and is still extremely high in the following trading days. It is seen to widen

once again to extreme values on October 8th and 9th the following month.

c. When the spread widens dramatically, presumably demonstrating some form of financial anxiety or crisis, which of the rates moves

the most and why?

Although the theoretician would quickly respond — without looking — that the overnight LIBOR rate is what should be spiking upwards. This

would, according to theory, represent the increased uncertainty over counterparty risk in the interbank market. But looking at the two interest rate

series reveals a second cause to the widening of the spread: the dramatic decrease in the 3-month Treasury bill rate. The T-Bill rate was driven to

incredible lows on selected dates as a result of U.S. Federal Reserve actions of pumping liquidity into the system in addition to the flight of

financial institutions to “quality” as they bid the price of T-Bills up, and with it, yields down.

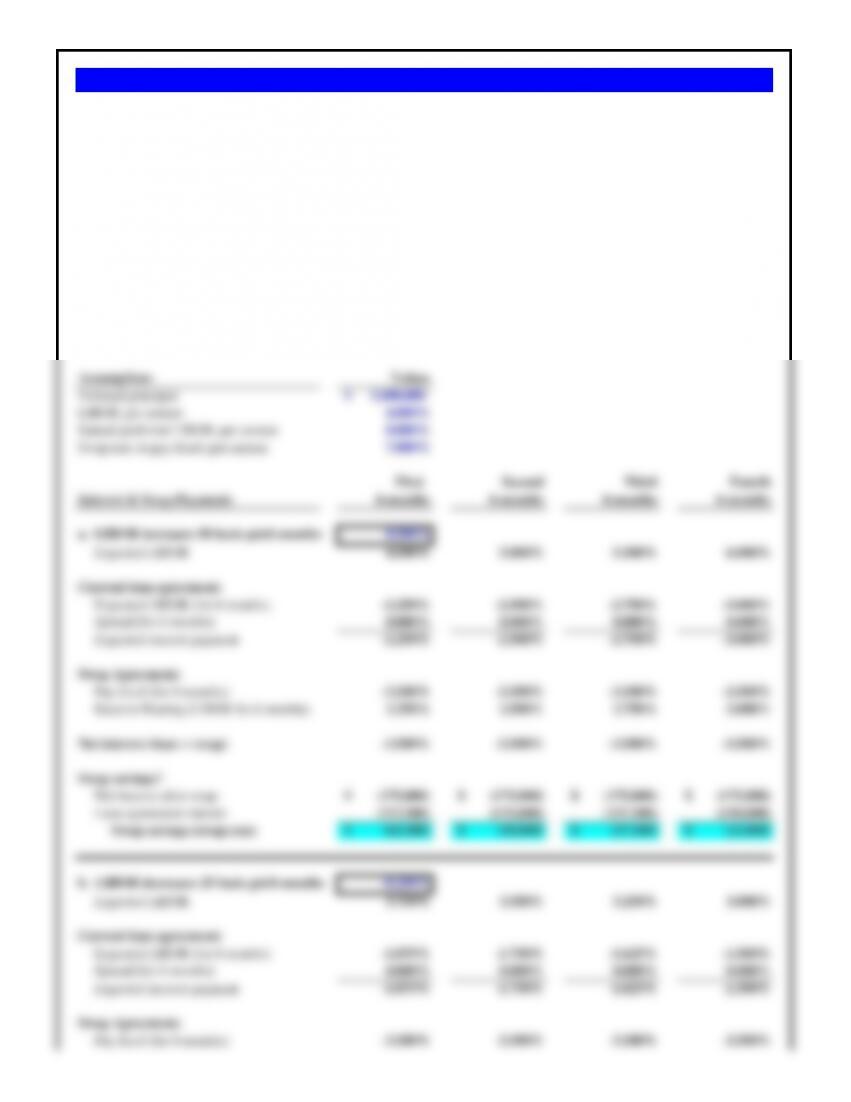

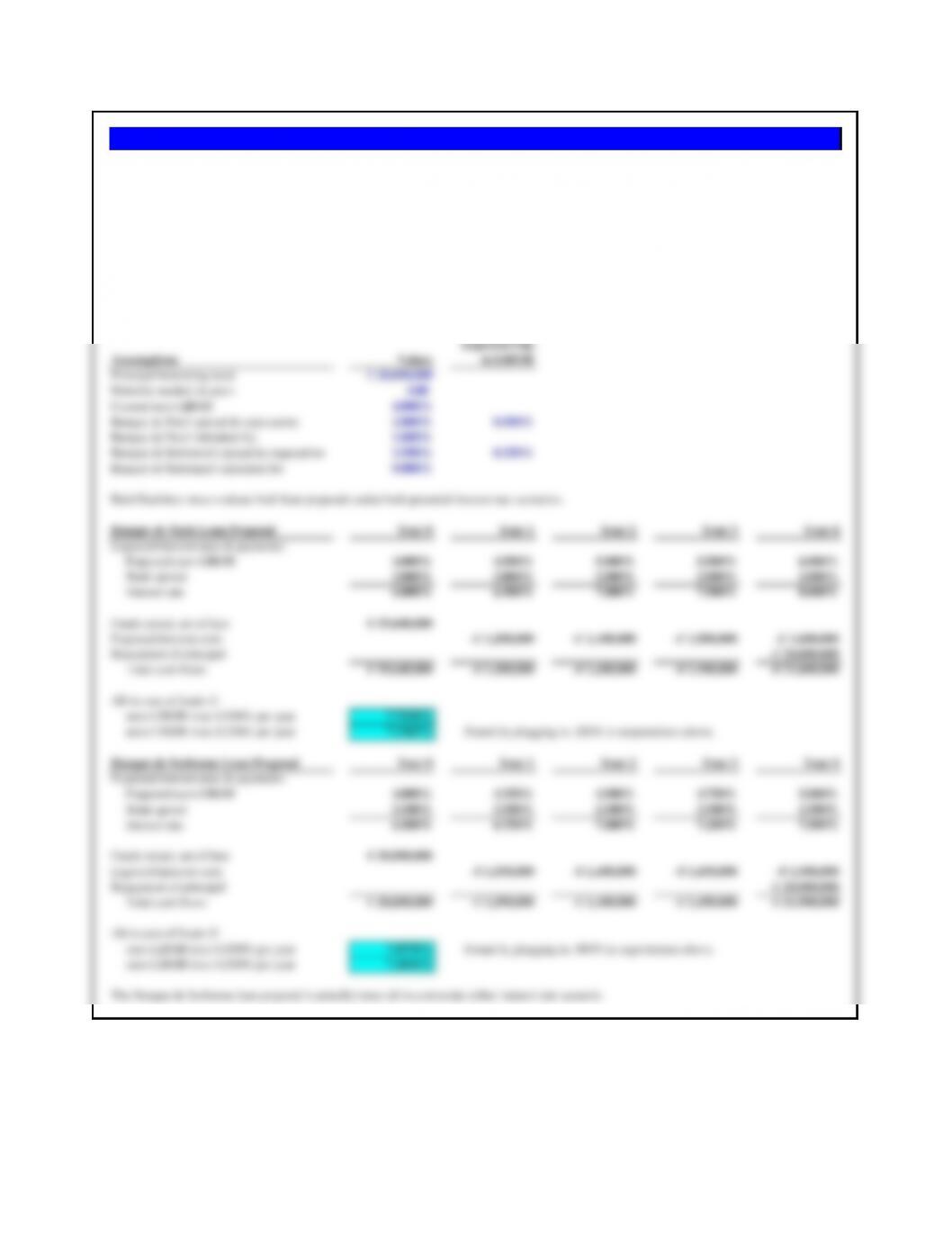

Assumptions 15-Year Mortgage 30-Year Mortgage

Price of house at purchase $240,000 $240,000

Less down-payment (20%) ($48,000) ($48,000)

Mortgage principal (US$) $192,000 $192,000

Mortgage length (years) 15 30

Mortgage length (months) 180 360

Fixed rate of interest 6.400% 6.875%

Monthly payment (amortizing loan, all equal payments) $1,662 $1,261

Assumptions 15-Year Mortgage

Price of house at purchase $240,000

Less down-payment (10%) 10% ($24,000)

Mortgage principal (US$) $216,000

Mortgage length (years) 15

Mortgage length (months) 180

Fixed rate of interest 7.125%

Monthly payment $1,957

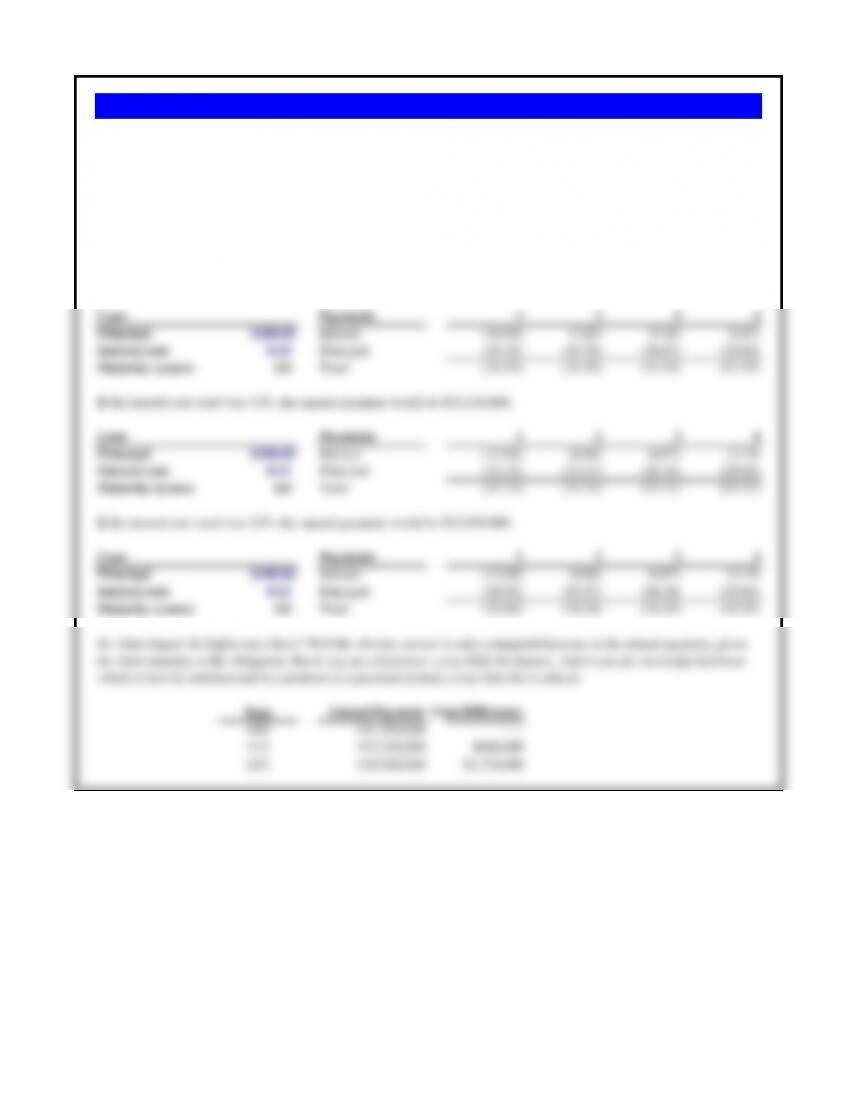

Home’s original value $240,000 $240,000

Fall in value -25.0% -25.0%

New home market value $180,000 $180,000

Mortgage outstanding $192,000 $192,000

Gain/loss on sale of house against mortgage alone ($12,000) ($12,000)

If the homeowner wanted to be assured of not selling the home at less than the mortgage outstanding, he would have to

price it at $192,000. At that price, given a market which now thinks it is only worth $180,000, the homeowner is going

to have a big problem selling it. Much longer to sell, if ever.

Problem 8.3 Underwater Mortgages

Bernie Madeoff pays $240,000 for a new four bedroom 2400 square foot home outside of Tonopah, Nevada. He plans

to make a 20% down payment, but is having trouble deciding whether he wants a 15-year fixed rate mortgage (6.400%)

or a 30-year fixed rate (6.875%).

a. What is the monthly payment, assuming a fully amortizing loan of equal payments for the life of the

mortgage?

This is calculated using Excel’s PMT formula. Note how much higher, roughly 32%, the payments are for a 15-year

mortgage over a 30-year mortgage.

b. Assume that instead of making a 20% down payment, he makes a 10% down payment, and finances the

remainder at 7.125% fixed interest for 15 years. What is his monthly payment?

c. Assume that the home’s total value falls by 25%. If Bernie sells the house at the new home value, what will be

his gain or loss on the home and mortgage assuming all of the mortgage principal remains? Use the same

assumptions as under part a.

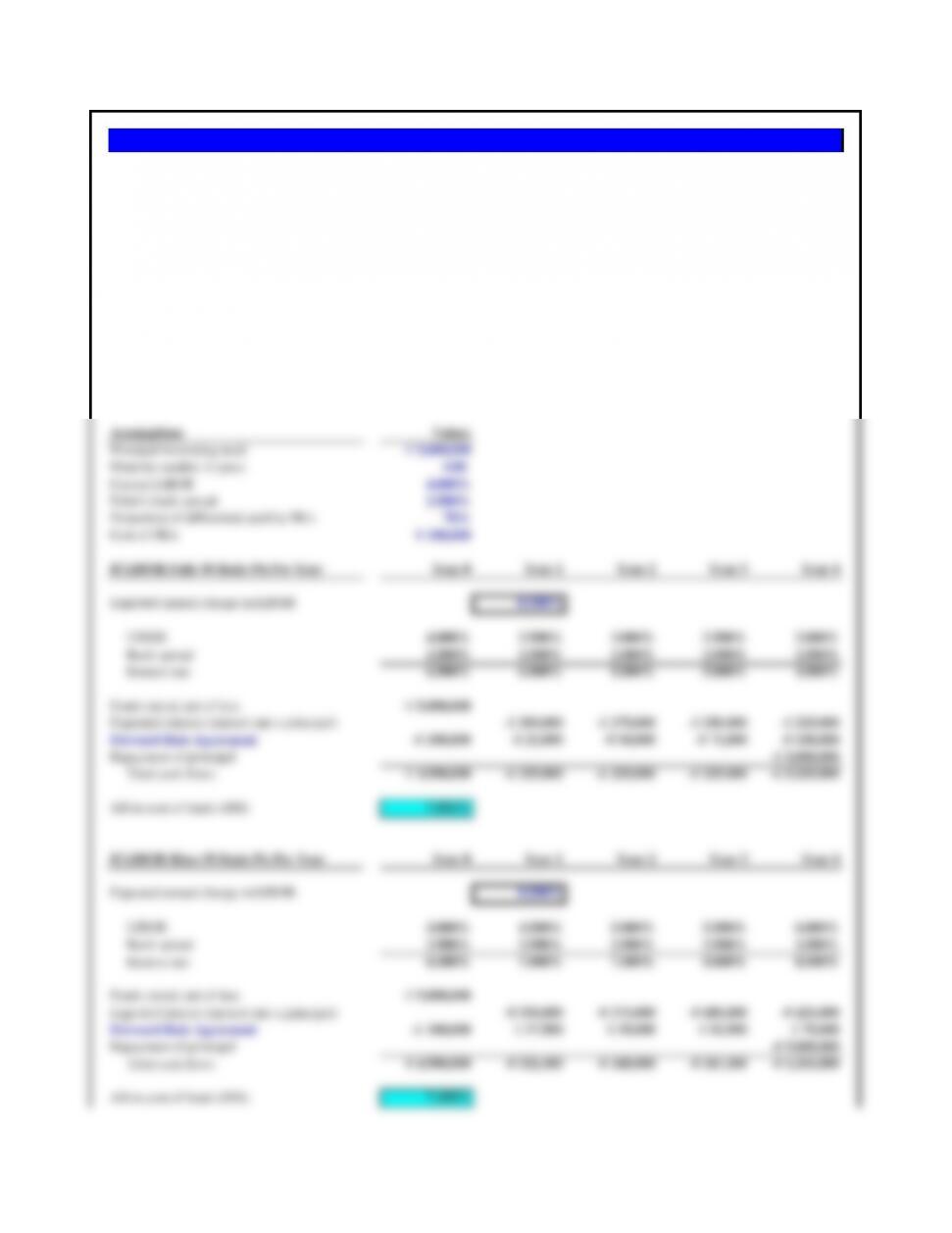

Assumptions Values

Principal borrowing need 30,000,000$

Maturity needed, in years 2.00

Fixed rate, 2 years 5.000%

Floating rate, six-month LIBOR + spread

Current six-month LIBOR 3.500%

Spread 0.000%

Fixed rate, 1 year, then re-fund 4.500%

First 6-months Second 6-months Third 6-months Fourth 6-months

#1: Fixed rate, 2 years

Interest cost per year 1,500,000$ 1,500,000$

Certainty over access to capital Certain Certain Certain Certain

Certainty over cost of capital Certain Certain Certain Certain

#2: Floating rate, six-month LIBOR

Interest cost per year 525,000$ 525,000$ 525,000$ 525,000$

Certainty over access to capital Certain Certain Certain Certain

Certainty over cost of capital Certain Uncertain Uncertain Uncertain

#3: Fixed rate, 1 year, then re-fund

Interest cost per year 1,350,000$ ??? ???

Certainty over access to capital Certain Certain Uncertain Uncertain

Certainty over cost of capital Certain Certain Uncertain Uncertain

Only alternative #1 has a certain access and cost of capital for the full 2 year period.

Alternative #2 has certain access to capital for both years, but the interest costs in the final 3 of 4 periods is uncertain.

Alternatvie #3, possessing a lower interest cost in year 1, has no guaranteed access to capital in the second year.

Depending on the company’s business needs and tolerance for interest rate risk, it could choose between #1 and #2.

#3. Botany Bay could borrow the US$30,000,000 for one year only at 4.5%. At the end of the first year Botany Bay would have to

negotiate for a new one-year loan.

Problem 8.4 Botany Bay Corporation

Botany Bay Corporation of Australia seeks to borrow US$30,000,000 in the Eurodollar market. Funding is needed for two years.

Investigation leads to three possibilities. Compare the alternatives and make a recommendation.

#1. Botany Bay could borrow the US$30,000,000 for two years at a fixed 5% rate of interest

#2. Botany Bay could borrow the US$30,000,000 at LIBOR which is currently 3.5%, and the rate would be reset every six months

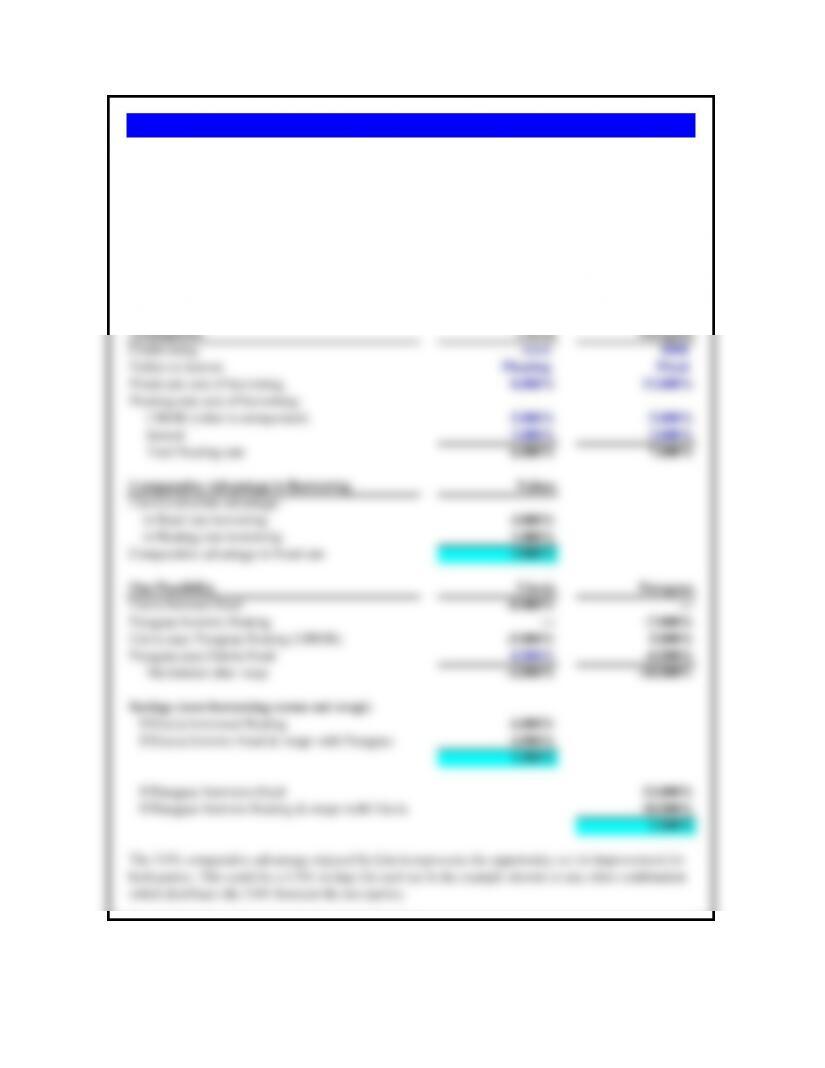

Assumptions Values

Interest rate futures, closing price 93.07

Effective yield on interest rate futures 6.930%

Floating Rate is Floating Rate is

Chrysler’s interest rate payments with futures 6.000% 8.000%

Interest payment due in three months 6.000% 8.000%

Sell a future (take a short position) -6.930% -6.930%

Gain or loss on position -0.930% 1.070%

Loss Gain

Three Months From Now

Problem 8.5 Chrysler LLC

Chrysler LLC, the now privately held company sold-off by DaimlerChrysler, must pay floating rate interest

three months from now. It wants to lock in these interest payments by buying an interest rate futures

contract. Interest rate futures for three months from now settled at 93.07, for a yield of 6.93% per annum.

a. If the floating interest rate three months from now is 6.00%, what did Chrysler gain or lose?

b. If the floating interest rate is 8.00% three months from now, what did Chrysler gain or lose?

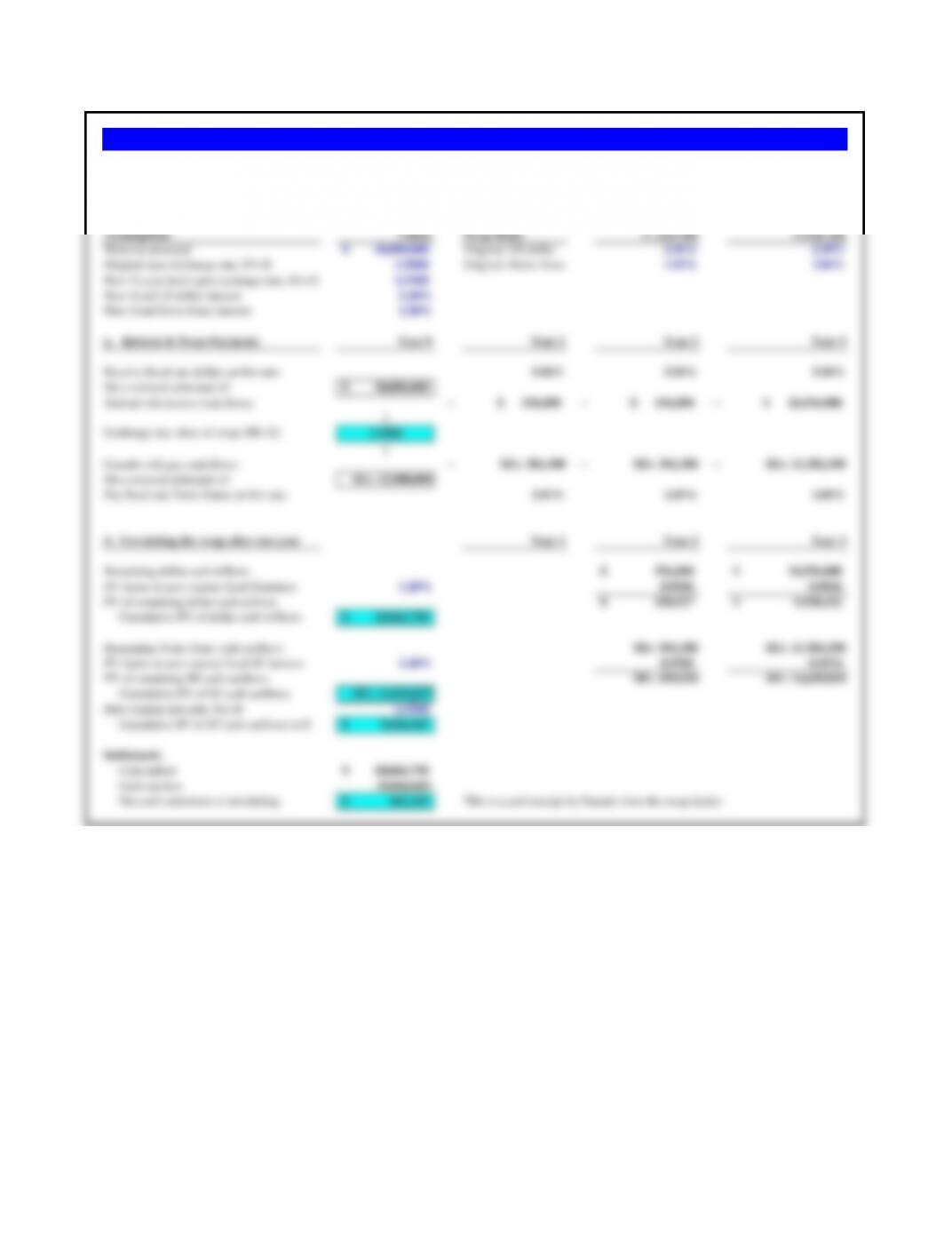

Assumptions Values

Notional principal 5,000,000$

LIBOR, per annum 4.000%

Spread paid over LIBOR, per annum 0.000%

Swap rate, to pay fixed, per annum 7.000%

First Second Third Fourth

Interest & Swap Payments 6-months 6-months 6-months 6-months

a. LIBOR increases 50 basis pts/6 months 0.500%

Expected LIBOR 4.500% 5.000% 5.500% 6.000%

Current loan agreement:

Expected LIBOR (for 6 months) -2.250% -2.500% -2.750% -3.000%

Spread (for 6 months) 0.000% 0.000% 0.000% 0.000%

Expected interest payment -2.250% -2.500% -2.750% -3.000%

Swap Agreement:

Pay fixed (for 6-months) -3.500% -3.500% -3.500% -3.500%

Receive floating (LIBOR for 6 months) 2.250% 2.500% 2.750% 3.000%

Net interest (loan + swap) -3.500% -3.500% -3.500% -3.500%

Swap savings?

Net interest after swap (175,000)$ (175,000)$ (175,000)$ (175,000)$

Loan agreement interest (112,500) (125,000) (137,500) (150,000)

Swap savings (swap cost) (62,500)$ (50,000)$ (37,500)$ (25,000)$

b. LIBOR decreases 25 basis pts/6 months -0.250%

Expected LIBOR 3.750% 3.500% 3.250% 3.000%

Current loan agreement:

Expected LIBOR (for 6 months) -1.875% -1.750% -1.625% -1.500%

Spread (for 6 months) 0.000% 0.000% 0.000% 0.000%

Expected interest payment -1.875% -1.750% -1.625% -1.500%

Swap Agreement:

Pay fixed (for 6-months) -3.500% -3.500% -3.500% -3.500%

a. If LIBOR rises at the rate of 50 basis points per six month period, starting tomorrow, how much does Heather save or cost

her company by making this swap?

b. If LIBOR falls at the rate of 25 basis points per six month period, starting tomorrow, how much does Heather save or cost

her company by making this swap?

Problem 8.6 CB Solutions

Heather O’Reilly, the treasurer of CB Solutions, believes interest rates are going to rise, so she wants to swap her future

floating rate interest payments for fixed rates. Presently, she is paying per annum on $5,000,000 of debt for the next two years,

with payments due semiannually. LIBOR is currently 4.00% per annum. Heather has just made an interest payment today, so

the next payment is due six months from today.

Heather finds that she can swap her current floating rate payments for fixed payments of 7.00% per annum. (CB Solution’s

weighted average cost of capital is 12%, which Heather calculates to be 6% per six month period, compounded semiannually).

Receive floating (LIBOR for 6 months) 1.875% 1.750% 1.625% 1.500%

Net interest (loan + swap) -3.500% -3.500% -3.500% -3.500%

Swap savings?

Net interest after swap (175,000)$ (175,000)$ (175,000)$ (175,000)$

Loan agreement interest (93,750) (87,500) (81,250) (75,000)

Swap savings (swap cost) (81,250)$ (87,500)$ (93,750)$ (100,000)$

In both cases CB Solutions is suffering higher total interest costs as a result of the swap.

Loan Payments 1 2 3 4

Principal $100.00 Interest (10.00) (7.85) (5.48) (2.87)

Interest rate 0.10 Principal (21.55) (23.70) (26.07) (28.68)

Maturity (years) 4.0 Total (31.55) (31.55) (31.55) (31.55)

If the interest rate used was 11%, the annual payment would be $32,230,000.

Loan Payments 1 2 3 4

Principal $100.00 Interest (11.00) (8.66) (6.07) (3.19)

Interest rate 0.11 Principal (21.23) (23.57) (26.16) (29.04)

Maturity (years) 4.0 Total (32.23) (32.23) (32.23) (32.23)

If the interest rate used was 12%, the annual payment would be $32,920,000.

Loan Payments 1 2 3 4

Principal $100.00 Interest (12.00) (8.66) (6.07) (3.19)

Interest rate 0.12 Principal (20.92) (23.57) (26.16) (29.04)

Maturity (years) 4.0 Total (32.92) (32.23) (32.23) (32.23)

Rate Annual Payment Cum Difference

10% $31,550,000 —–

11% $32,230,000 $680,000

12% $32,920,000 $1,370,000

Problem 8.7 Negotiating the Rate

A sovereign borrower is considering a $100 million loan for a four-year maturity. It will be an amortizing loan, meaning

that the interest and principal payments will total, annually, to a constant amount over the maturity of the loan. There is,

however, a debate over the appropriate interest rate. The borrower believes the appropriate rate for its creditstanding in the

market today is 10%, but a number of the international banks which it is negotiating with are arguing that it is most likely

12%, at the minimum 10%. What impact do these different interest rates have on the prospective annual payments?

The sovereign borrower believes the appropriate rate to be 10%, which would generate the following amortized (principal

and interest) payments, an annual payment of $31,550,000.

So ‘what impact’ do higher rates have? Well the obvious answer is only a marginal increase in the annual payment, given

the short maturity of the obligation. But if you are a borrower, every little bit matters. And if you are sovereign borrower

which is heavily indebted and in a position of a potential default, every little bit is critical.

Loan 0 Payments 1 2 3 4 5 6

Principal $220 Interest (26.950) (23.650) (19.946) (15.788) (11.120) (5.881)

Interest rate 12.250% Principal (26.939) (30.239) (33.943) (38.101) (42.769) (48.008)

Maturity (years) 6.0 Total (53.889) (53.889) (53.889) (53.889) (53.889) (53.889)

a. What would the annual amortizing loan payments be for the bank consortium’s proposal?

If the maturity in years is shortened to 4.0 years, the amortized payment rises to: 72.813

b. What would the annual amortizing loan payments be for Sahara’s loan preferences?

If the maturity is kept at 6.0 years, and the interest rate lowered to 11.75%, the amortized payment is: 53.131

Payments would fall from 72.813 to 53.889, a difference of: 18.924

The country of Sahara is negotiating a new loan agreement with a consortium of international banks. Both sides have a tentative agreement on the

principal — $220 million. But there are still wide differences of opinion on the final interest rate and maturity. The banks would like a shorter loan,

4 years in length, while Sahara would prefer a long maturity of 6 years. The banks also believe the interest rate will need to be 12.250% per annum,

but Sahara believes that is too high, arguing for 11.750%.

c. How much would annual payments drop on the bank consortium’s proposal if the same loan was stretched out from 4 to 6 years?

Problems 8.8 Saharan Debt Negotiations

Loan 0 Payments 1 2 3 4 5 6 7 8 9

Principal € 80.00 Interest (6.900) (5.974) (4.968) (3.876) (2.689) (1.400) – – –

Interest rate 8.6250% Principal (10.735) (11.661) (12.666) (13.759) (14.945) (16.234) – – –

Maturity (years) 6.0 Total (17.635) (17.635) (17.635) (17.635) (17.635) (17.635) – – –

a. What were Delos’s annual principal and interest payments under the original loan agreement?

The original interest and principal payments are shown above, with a constant annual payment for the six-year period of €17.635 million (€17,634,664 to be exact).

b. After two years debt-service, how much of the principal is still outstanding?

Original principal 80,000,000

Year 1 principal pmt (10,734,664)

Year 2 principal pmt (11,660,529)

Remaining balance € 57,604,808

c. If the loan was restructured to extend another two years, what would the annual payments — principal and interest — be?

Problems 8.9 Delos Debt Renegotiations (A)

Delos borrowed €80 million two years ago. The loan agreement, an amortizing loan, was for 6 years at 8.625% interest per annum. Delos has successfully completed two years of debt-

service, but now wishes to renegotiate the terms of the loan with the lender to reduce its annual payments.

After two years of regular debt service, the remaining principal would be the original €80,000,000 less the sum of the first year and second year principal payments of €10,734,664 and

€11,660,529.

Assuming that the remaining balance after two years is €57,604,808, as calculated from part b), then if the existing loan agreement was restructured from the remaining four years to

six years at the same interest rate, the annual payments would now be €12,698,018. This would represent a significant reduction from the original annual payments of €17,635,000.

Loan 0 Payments 1 2 3 4 5 6 7 8 9

Principal € 80.00 Interest (6.90) (5.97) (4.97) (3.88) (2.69) (1.40) – – –

Interest rate 8.6250% Principal (10.73) (11.66) (12.67) (13.76) (14.95) (16.23) – – –

Maturity (years) 6.0 Total (17.63) (17.63) (17.63) (17.63) (17.63) (17.63) – – –

Loan 0 Payments 1 2 3 4 5 6 7

Principal € 42.78 Interest (4.55) (3.97) (3.32) (2.61) (1.83) (0.96) –

Interest rate 10.6250% Principal (5.46) (6.04) (6.68) (7.39) (8.17) (9.04) –

Maturity (years) 6.0 Total (10.00) (10.00) (10.00) (10.00) (10.00) (10.00) –

Haircut 0.0%

This will reduce annual payments from the current €17.63 million per year to €13.47 million per year.

The easiest way to find this is by trial and error in the above loan calculator — continually reduce the remaining principal (first showing €57.60) until the total annual

payment, principal and interest, reaches €10.00. That value is a principal of €42.78 million, a sizeable haircut (a haircut of €14.82 million) from the remaining €57.60

Problem 8.10 Delos Debt Renegotiations (B)

Delos is continuing to renegotiate its prior loan agreement (€80 million for 6 years at 8.625% per annum), two years into the agreement. Delos is now facing serious tax

revenue shortfalls, and fears for its ability to service its debt obligations. So it has decided to get more aggressive, and has gone back to its lenders with a request for a

‘haircut’, a reduction in the the remaining loan amount. The banks have, so far, only agreed to restructure the loan agreement for another two years (a new loan of 6 years

on the remaining principal balance) but at an interest rate a full 200 basis points higher, 10.625%.

a. If Delos accepts the current bank proposal of the remaining principal for 6 years (extending the loan an additional 2 years since 2 of the original 6 years have

already passed), but at the new interest rate, what are its annual payments going to be? How much relief does this provide Delos on annual debt-service?

After the the first wo years of the original loan agreement, the principal of €80.00 has been reduced by –€10.73 (year 1) and – €11.66 (year 2), for a remaining principal

balance of €57.60.

b. Delos’s demands for a haircut are based on getting the new annual debt service payments down. If Delos does agree to the new loan terms, what size of

haircut should it try and get from its lenders to get its payments down to €10 million per year?

Expected Chg

Assumptions Values in LIBOR

Principal borrowing need € 20,000,000

Maturity needed, in years 4.00

Current euro-LIBOR 4.000%

Banque de Paris’ spread & expectation 2.000% 0.500%

Banque de Paris’ initiation fee 1.800%

Banque de Sorbonne’s spread & expectation 2.500% 0.250%

Banque de Sorbonne’s initiation fee 0.000%

Raid Gauloises must evaluate both loan proposals under both potential interest rate scenarios.

Banque de Paris Loan Proposal Year 0 Year 1 Year 2 Year 3 Year 4

Expected interest rates & payments:

Expected euro-LIBOR 4.000% 4.500% 5.000% 5.500% 6.000%

Bank spread 2.000% 2.000% 2.000% 2.000% 2.000%

Interest rate 6.000% 6.500% 7.000% 7.500% 8.000%

Funds raised, net of fees € 19,640,000

Expected interest costs -€ 1,300,000 -€ 1,400,000 -€ 1,500,000 -€ 1,600,000

Repayment of principal -€ 20,000,000

Total cash flows € 19,640,000 -€ 1,300,000 -€ 1,400,000 -€ 1,500,000 -€ 21,600,000

All-in-cost of funds if:

euro-LIBOR rises 0.500% per year 7.7438%

euro-LIBOR rises 0.250% per year 7.1365% Found by plugging in .250% in expectations above.

Banque de Sorbonne Loan Proposal Year 0 Year 1 Year 2 Year 3 Year 4

Expected interest rates & payments:

Expected euro-LIBOR 4.000% 4.250% 4.500% 4.750% 5.000%

Bank spread 2.500% 2.500% 2.500% 2.500% 2.500%

Interest rate 6.500% 6.750% 7.000% 7.250% 7.500%

Funds raised, net of fees € 20,000,000

Expected interest costs -€ 1,350,000 -€ 1,400,000 -€ 1,450,000 -€ 1,500,000

Repayment of principal -€ 20,000,000

Total cash flows € 20,000,000 -€ 1,350,000 -€ 1,400,000 -€ 1,450,000 -€ 21,500,000

All-in-cost of funds if:

euro-LIBOR rises 0.500% per year 7.0370% Found by plugging in .500% in expectations above.

euro-LIBOR rises 0.250% per year 7.1036%

The Banque de Sorbonne loan proposal is actually lower all-in-cost under either interest rate scenario.

Euro-LIBOR is currently 4.00%. Raid’s economist forecasts that LIBOR will rise by 0.5 percentage points each year. Banque de Sorbonne,

however, officially forecasts euro-LIBOR to begin trending upward at the rate of 0.25 percentage points per year. Raid Gauloises’s cost of capital is

11%. Which loan proposal do you recommend for Raid Gauloises?

Raid Gauloises is a rapidly growing French sporting goods and adventure racing outfitter. The company has decided to borrow €20,000,000 via a

euro-euro floating rate loan for four years. Raid must decide between two competing loan offerings from two of its banks.

Problem 8.11 Raid Gauloises

Banque de Paris has offered the four-year debt at euro-LIBOR + 2.00% with an up-front initiation fee of 1.8%. Banque de Sorbonne, however, has

offered euro-LIBOR + 2.5%, a higher spread, but with no loan initiation fees up-front, for the same term and principal. Both banks reset the interest

rate at the end of each year.

Assumptions Values

Principal borrowing need € 5,000,000

Maturity needed, in years 4.00

Current LIBOR 4.000%

Felini’s bank spread 2.500%

Proportion of differential paid by FRA 70%

Cost of FRA € 100,000

If LIBOR Falls 50 Basis Pts Per Year Year 0 Year 1 Year 2 Year 3 Year 4

Expected annual change in LIBOR -0.500%

LIBOR 4.000% 3.500% 3.000% 2.500% 2.000%

Bank spread 2.500% 2.500% 2.500% 2.500% 2.500%

Interest rate 6.500% 6.000% 5.500% 5.000% 4.500%

Funds raised, net of fees € 5,000,000

Expected interest (interest rate x principal) -€ 300,000 -€ 275,000 -€ 250,000 -€ 225,000

Forward Rate Agreement -€ 100,000 -€ 25,000 -€ 50,000 -€ 75,000 -€ 100,000

Repayment of principal -€ 5,000,000

Total cash flows € 4,900,000 -€ 325,000 -€ 325,000 -€ 325,000 -€ 5,325,000

All-in-cost of funds (IRR) 7.092%

If LIBOR Rises 50 Basis Pts Per Year Year 0 Year 1 Year 2 Year 3 Year 4

Expected annual change in LIBOR 0.500%

LIBOR 4.000% 4.500% 5.000% 5.500% 6.000%

Bank spread 2.500% 2.500% 2.500% 2.500% 2.500%

Interest rate 6.500% 7.000% 7.500% 8.000% 8.500%

Funds raised, net of fees € 5,000,000

Expected interest (interest rate x principal) -€ 350,000 -€ 375,000 -€ 400,000 -€ 425,000

Forward Rate Agreement -€ 100,000 € 17,500 € 35,000 € 52,500 € 70,000

Repayment of principal -€ 5,000,000

Total cash flows € 4,900,000 -€ 332,500 -€ 340,000 -€ 347,500 -€ 5,355,000

All-in-cost of funds (IRR) 7.458%

Purchase of the floating Rate Agreement will cost €100,000, paid at the time of the initial loan. What are Firenza’s annual financing

costs now if LIBOR rises and if LIBOR falls.? Firenza uses 12% as its weighted average cost of capital. Do you recommend that Firenza

purchase the FRA?

Problem 8.12 Firenza Motors

Firenza Motors of Italy recently took out a 4-year €5 million loan on a floating rate basis. It is now worried, however, about rising

interest costs. Although it had initially believed interest rates in the Euro-zone would be trending downward when taking out the loan,

recent economic indicators show growing inflationary pressures. Analysts are predicting that the European Central Bank will slow

monetary growth driving interest rates up.

Firenza is now considering whether to seek some protection against a rise in euro-LIBOR, and is considering a Forward Rate

Agreement (FRA) with an insurance company. According to the agreement, Firenza would pay to the insurance company at the end of

each year the difference between its initial interest cost at LIBOR + 2.50% (6.50%) and any fall in interest cost due to a fall in LIBOR.

Conversely, the insurance company would pay to Firenza 70% of the difference between Firenza’s initial interest cost and any increase in

interest costs caused by a rise in LIBOR.

This rather unusual forward rate agreement is somewhat one-sided in the favor of the insurance company. When Firenza is correct,

Firenza pays the full difference in rates to the insurance company. But when interest rates move against Firenza, the insurance company

pays Firenza only 70% of the difference in rates. And all of that is after Firenza paid €100,000 up-front for the agreement regardless of

outcome. Not a very good deal.

A final note of significance is that since Firenza receives only 70% of the difference in rates, its total cost of funds is not effectively

“capped”; they could in fact rise with no limit over the period as interest rates rose.

Assumptions Lluvia Paraguas

Credit rating AAA BBB

Prefers to borrow Floating Fixed

Fixed-rate cost of borrowing 8.000% 12.000%

Floating-rate cost of borrowing:

LIBOR (value is unimportant) 5.000% 5.000%

Spread 1.000% 2.000%

Total floating-rate 6.000% 7.000%

Comparative Advantage in Borrowing Values

Lluvia’s absolute advantage:

in fixed rate borrowing 4.000%

in floating-rate borrowing 1.000%

Comparative advantage in fixed rate 3.000%

One Possibility Lluvia Paraguas

Lluvia borrows fixed -8.000% —

Paraguas borrows floating — -7.000%

Lluvia pays Paraguas floating (LIBOR) -5.000% 5.000%

Paraguas pays Lluvia fixed 8.500% -8.500%

Net interest after swap -4.500% -10.500%

Savings (own borrowing versus net swap):

If Lluvia borrowed floating 6.000%

If Lluvia borrows fixed & swaps with Paraguas 4.500%

1.500%

If Paraguas borrowes fixed 12.000%

If Paraguas borrows floating & swaps with Lluvia 10.500%

1.500%

Problem 8.13 Lluvia and Paraguas

The 3.0% comparative advantage enjoyed by Lluvia represents the opportunity set for improvement for

both parties. This could be a 1.5% savings for each (as in the example shown) or any other combination

which distributes the 3.0% between the two parties.

Lluvia Manufacturing and Paraguas Products both seek funding at the lowest possible cost. Lluvia

would prefer the flexibility of floating rate borrowing, while Paraguas wants the security of fixed rate

borrowing. Lluvia is the more credit-worthy company. They face the following rate structure. Lluvia,

with the better credit rating, has lower borrowing costs in both types of borrowing.

Lluvia wants floating rate debt, so it could borrow at LIBOR+1%. However it could borrow fixed at

8% and swap for floating rate debt. Paraguas wants fixed rate, so it could borrow fixed at 12%. However

it could borrow floating at LIBOR+2% and swap for fixed rate debt. What should they do?

Assumptions Values Swap Rates 3- year bid 3-year ask

Notional principal 10,000,000$ Original: US dollar 5.56% 5.59%

Original spot exchange rate, SFr./$ 1.5000 Original: Swiss franc 1.93% 2.01%

New (1-year later) spot exchange rate, SFr./$ 1.5560

New fixed US dollar interest 5.20%

New fixed Swiss franc interest 2.20%

a. Interest & Swap Payments Year 0 Year 1 Year 2 Year 3

Receive fixed rate dollars at this rate: 5.56% 5.56% 5.56%

On a notional principal of: 10,000,000$

Trident will receive cash flows: →556,000$ →556,000$ →10,556,000$

↑

Exchange rate, time of swap (SFr./$)1.5000

↓

Ganado will pay cash flows: →SFr. 301,500 →SFr. 301,500 →SFr. 15,301,500

On a notional principal of: SFr. 15,000,000

Pay fixed rate Swiss francs at this rate: 2.01% 2.01% 2.01%

b. Unwinding the swap after one-year Year 1 Year 2 Year 3

Remaining dollar cash inflows 556,000$ 10,556,000$

PV factor at now current fixed $ interest 5.20% 0.9506 0.9036

PV of remaining dollar cash inflows 528,517$ 9,538,232$

Cumulative PV of dollar cash infllows 10,066,750$

Remaining Swiss franc cash outflows SFr. 301,500 SFr. 15,301,500

PV factor at now current fixed SF interest 2.20% 0.9785 0.9574

PV of remaining SF cash outflows SFr. 295,010 SFr. 14,649,818

Cumulative PV of SF cash outflows SFr. 14,944,827

New current spot rate, SFr./$ 1.5560

Cumulative PF of SF cash outflows in $ 9,604,645$

Settlement:

Cash inflow 10,066,750$

Cash outflow (9,604,645)

Net cash settlement of unwinding 462,105$ This is a cash receipt by Ganado from the swap dealer.

Problem 8.14 Ganado’s Cross Currency Swap: SFr for US$

Ganado Corporation entered into a three-year cross-currency interest rate swap to receive U.S. dollars and pay Swiss francs. Ganado, however, decided to

unwind the swap after one year – thereby having two years left on the settlement costs of unwinding the swap after one year. Repeat the calculations for

unwinding, but assume that the following rates now apply:

a. Calculate all principal and interest payments, in both euros and Swiss francs, for the life of the swap agreement.

Assumptions Values Swap Rates 3- year bid 3-year ask

Notional principal € 5,000,000 Euros — €0.20% 0.24%

Spot exchange rate, Yen/euro 104.00 Japanese yen 0.13% 0.19%

a) Interest & Swap Payments Year 0 Year 1 Year 2 Year 3

Receive fixed rate euros at this rate: 0.20% 0.20% 0.20%

On a notional principal of: € 5,000,000

Trident will receive cash flows: → € 10,000 → € 10,000 → € 5,010,000

↑

Exchange rate, time of swap (¥/€)104.00

↓

Ganado will pay cash flows: →988,000 →988,000 →520,988,000

On a notional principal of (yen): 520,000,000

Pay fixed rate Japanese yen at this rate: 0.19% 0.19% 0.19%

b) Unwinding the swap after one-year Year 1 Year 2 Year 3

Remaining euro cash inflows € 10,000 € 5,010,000

PV factor at now current fixed € interest 3.60% 0.9653 0.9317

PV of remaining € cash inflows € 9,653 € 4,667,864

Cumulative PV of € cash infllows € 4,677,517

Remaining ¥ cash outflows SFr. 988,000 SFr. 520,988,000

PV factor at now current fixed ¥ interest 0.80% 0.9921 0.9842

PV of remaining ¥ cash outflows SFr. 980,159 SFr. 512,751,165

Cumulative PV of ¥ cash outflows 513,731,324

New current spot rate, ¥/€114.00

Cumulative PV of ¥ cash outflows in €€ 4,506,415

Settlement:

Cash inflow € 4,677,517

Cash outflow (4,506,415)

Net cash settlement of unwinding € 171,102 This is a cash receipt by Ganado from the swap dealer.

Problem 8.15 Ganado’s Cross Currency Swap: Yen for Euros

Using the table of swap rates in the chapter (Exhibit 8.12), and assume Ganado enters into a swap agreement to receive euros and pay Japanese yen,

on a notional principal of €5,000,000. The spot exchange rate at the time of the swap is ¥104/€.

b. Assume that one year into the swap agreement Ganado decides it wishes to unwind the swap agreement and settle it in euros. Assuming that a two-

year fixed rate of interest on the Japanese yen is now 0.80%, and a two-year fixed rate of interest on the euro is now 3.60%, and the spot rate of

exchange is now ¥114/€, what is the net present value of the swap agreement? Who pays whom what?

Assumptions Values Swap Rates 7- year bid 7-year ask

Notional principal 50,000,000$ US dollar 2.02% 2.05%

Spot exchange rate, $/€1.16 Euros 0.51% 0.55%

a. Interest & Swap Payments Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

Receive fixed rate dollars at rate: 2.02%

Notional principal of: 50,000,000$

Receive cash inflows of: 1,010,000$ 1,010,000$ 1,010,000$ 1,010,000$ 1,010,000$ 1,010,000$ 51,010,000$

↑

Spot exchange rate, $/€1.16

↓

Pay cash outflows of: € 237,069 € 237,069 € 237,069 € 237,069 € 237,069 € 237,069 € 43,340,517

Notional principal of: € 43,103,448

Pay fixed rate euros at rate: 0.55%

b. Unwindingthe Swap Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

If the swap is unwound three years later, there are four years of cash flows remaining:

Remaining dollar cash inflows 1,010,000$ 1,010,000$ 1,010,000$ 51,010,000$

PV factor at now current fixed $ interest 4.40% 0.9579 0.9175 0.8788 0.8418

PV of remaining dollar cash inflows 967,433$ 926,660$ 887,605$ 42,939,139$

Problem 8.16 Falcor

Falcor is the U.S.-based automotive parts supplier which was spun-off from General Motors in 2000. With annual sales of over $26 billion, the company has expanded its markets

far beyond the traditional automobile manufacturers in the pursuit of a more diversified sales base. As part of the general diversification effort, the company wishes to diversify

the currency of denomination of its debt portfolio as well. Assume Falcor enters into a $50 million 7-year cross currency interest rate swap to do just that – pay euro and receive

dollars. Using the data in Exhibit 8.12, solve the following:

a. Calculate all principal and interest payments in both currencies for the life of the swap.

b. Assume that three years later Falcor decides to unwind the swap agreement. If 4-year fixed rates of interest in euros have now risen to 5.35% and 4-year fixed rate dollars have

fallen to 4.40%, and the current spot exchange rate of $1.02/€, what is the net present value of the swap agreement? Explain the payment obligations of the two parties precisely.

Cumulative PV of $ cash infllows 45,720,837$

Remaining euro cash outflows € 237,069 € 237,069 € 237,069 € 43,340,517

PV factor at now current fixed € interest 5.35% 0.9492 0.9010 0.8553 0.8118

PV of remaining euro cash outflows € 225,030 € 213,602 € 202,755 € 35,184,868

Cumulative PV of € cash outflows € 35,826,255

Spot exchange rate at unwinding ($/€)1.02

Cumulative PV of € cash outflows, $ 36,542,780$

Settlement:

Cash inflow 45,720,837$

Cash outflow (36,542,780)

Net cash settlement of unwinding 9,178,057$ This is a net cash payment to Falcor from the swap dealer.