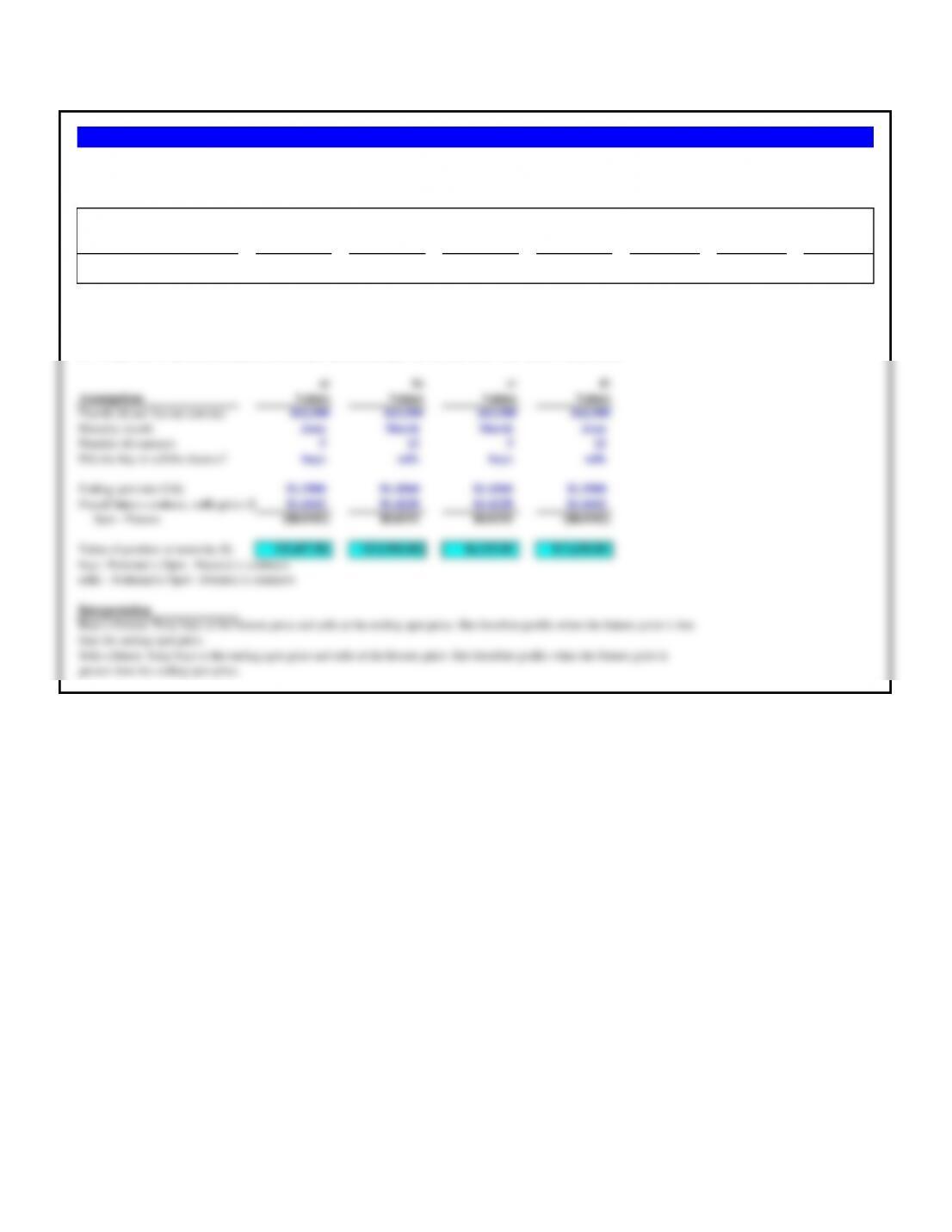

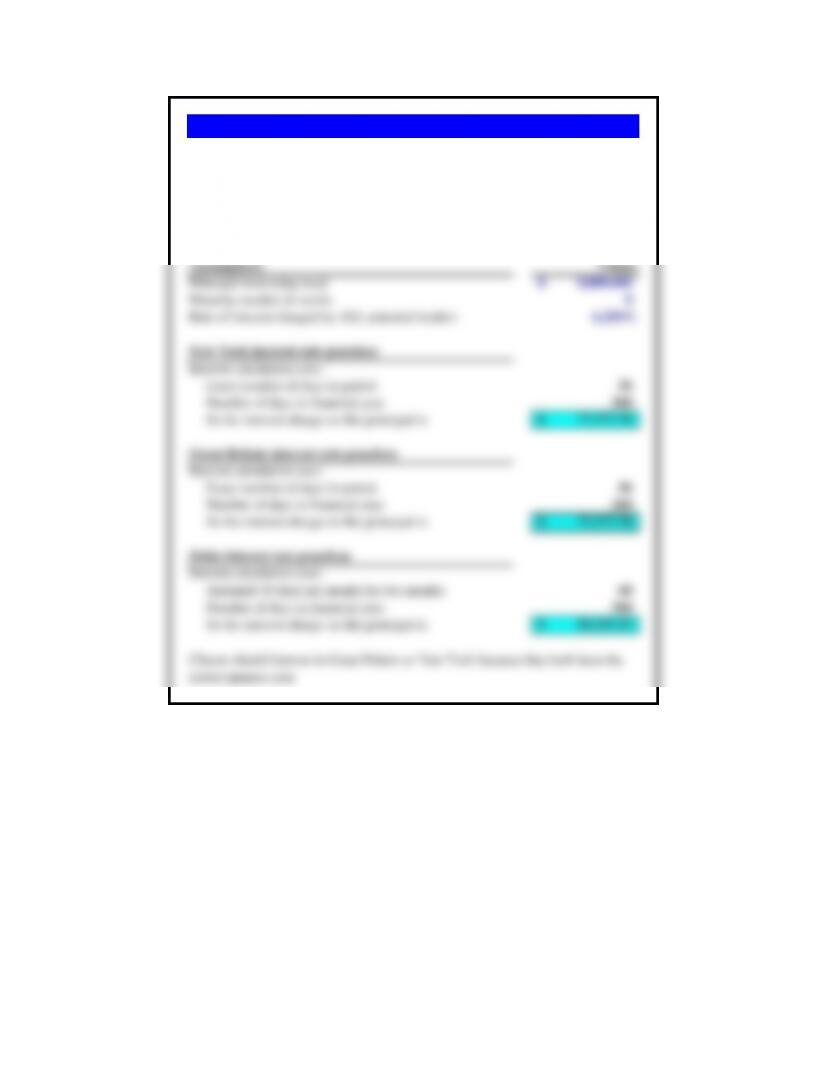

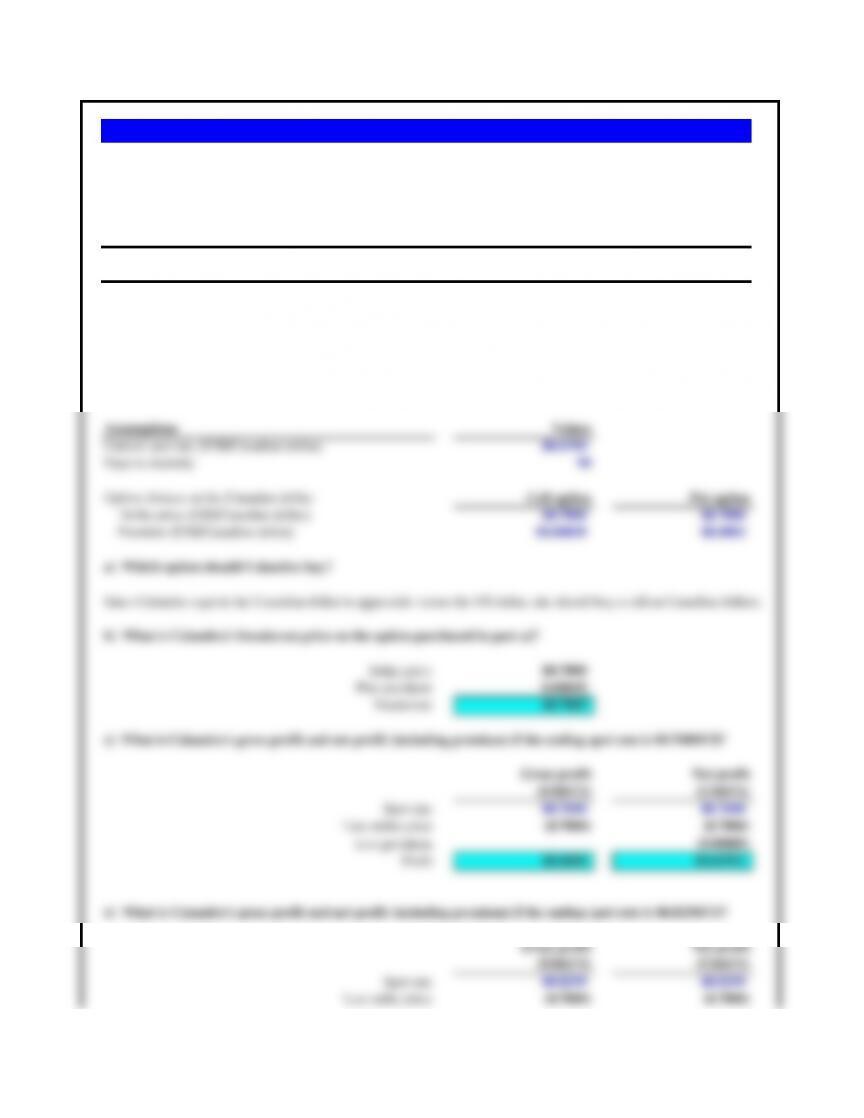

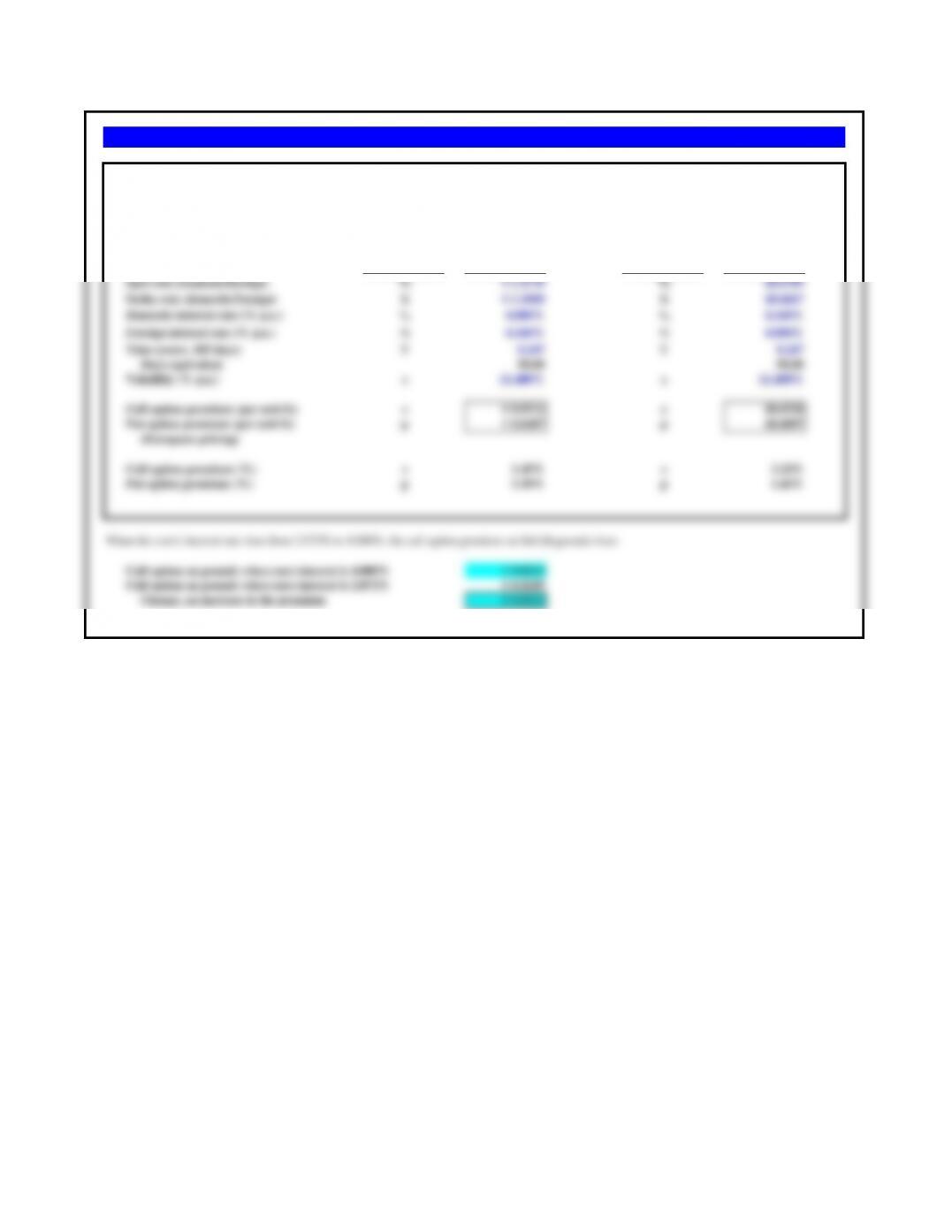

British Pound Futures, US$/pound (CME) Contract = 62,500 pounds

Open

Maturity Open High Low Settle Change High Interest

March 1.4246 1.4268 1.4214 1.4228 0.0032 1.4700 25,605

June 1.4164 1.4188 1.4146 1.4162 0.0030 1.4550 809

a. If Tony buys 5 June pound futures, and the spot rate at maturity is $1.3980/£, what is the value of her position?

b. If Tony sells 12 March pound futures, and the spot rate at maturity is $1.4560/£, what is the value of her position?

c. If Tony buys 3 March pound futures, and the spot rate at maturity is $1.4560/£, what is the value of her position?

d. If Tony sells 12 June pound futures, and the spot rate at maturity is $1.3980/£, what is the value of her position?

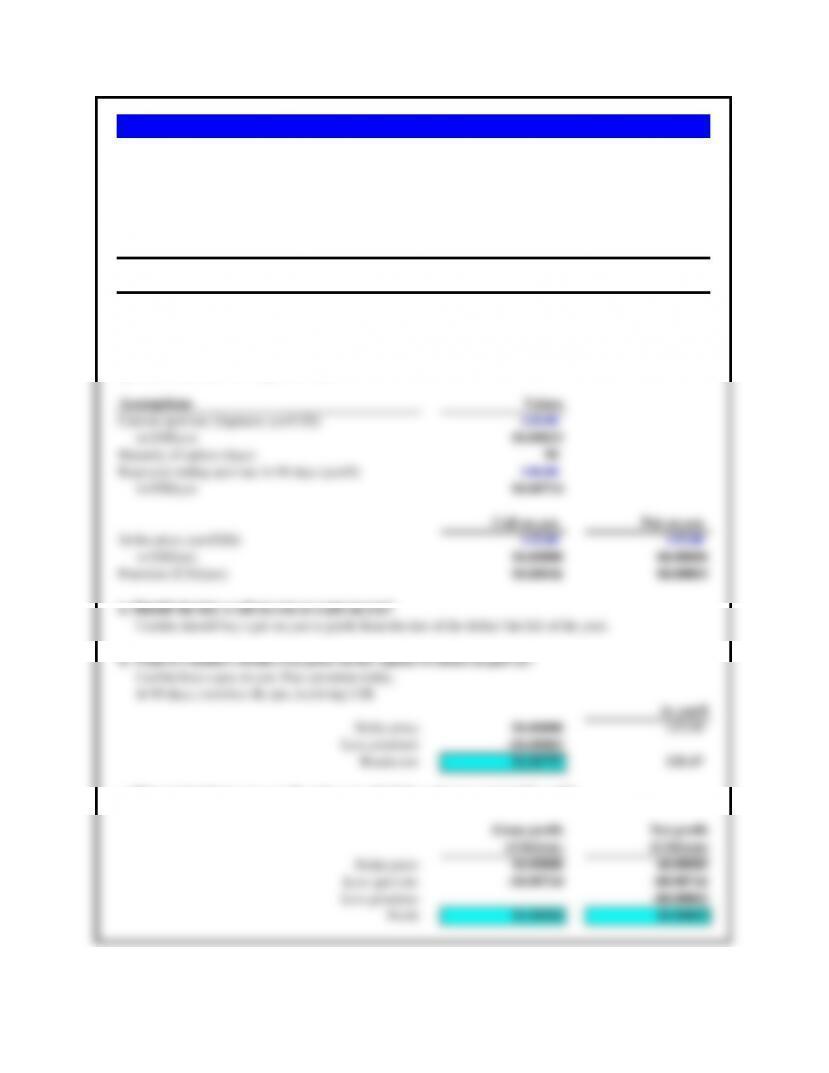

a) b) c) d)

Assumptions Values Values Values Values

Pounds (₤) per futures contract £62,500 £62,500 £62,500 £62,500

Maturity month June March March June

Number of contracts 5 12 3 12

Did she buy or sell the futures? buys sells buys sells

Ending spot rate ($/₤) $1.3980 $1.4560 $1.4560 $1.3980

Pound futures contract, settle price ($/₤)

$1.4162 $1.4228 $1.4228 $1.4162

Spot – Futures ($0.0182) $0.0332 $0.0332 ($0.0182)

Value of position at maturity ($) ($5,687.50) ($24,900.00) $6,225.00 $13,650.00

buys: Notional x (Spot – Futures) x contracts

sells: – Notional x (Spot – Futures) x contracts

Interpretation

Sells a future: Tony buys at the ending spot price and sells at the futures price. She therefore profits when the futures price is

greater than the ending spot price.

Problem 7.1 Saguaro Funds

Tony Begay, a currency trader for Chicago-based Saguaro Funds, uses the following futures quotes on the British pound (£) to speculate on the value of the pound.

Buys a futures: Tony buys at the futures price and sells at the ending spot price. She therefore profits when the futures price is less

than the ending spot price.

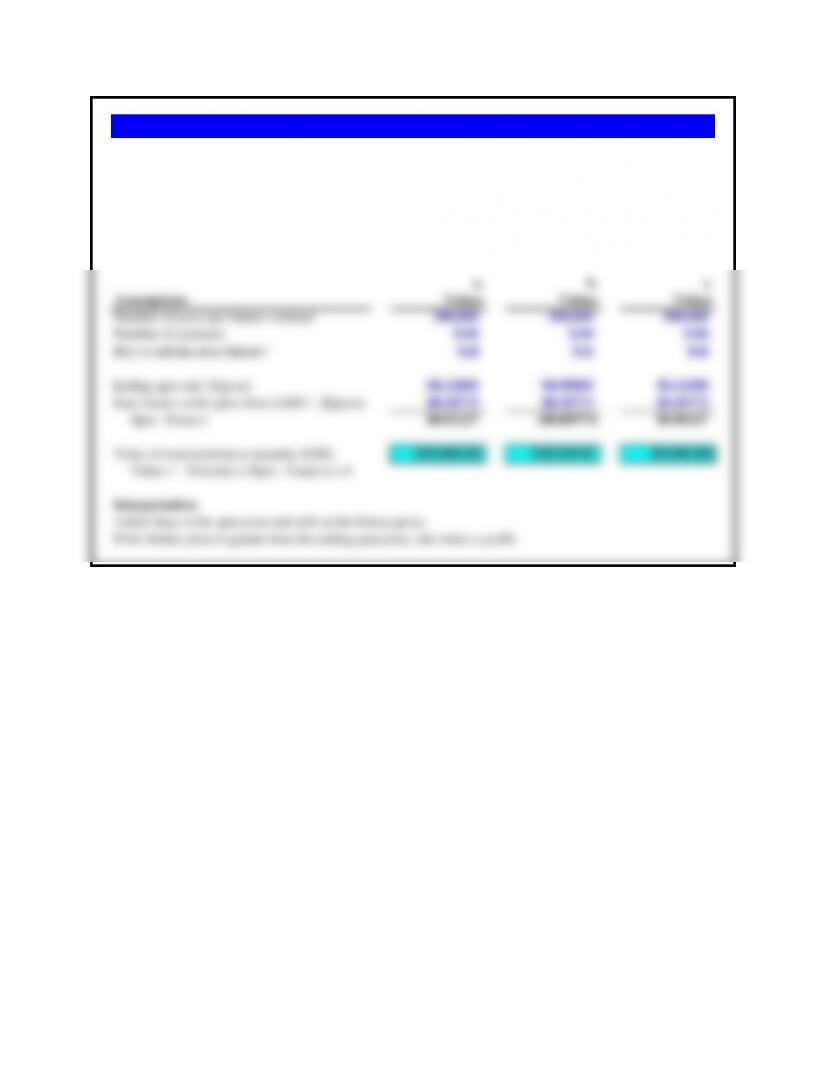

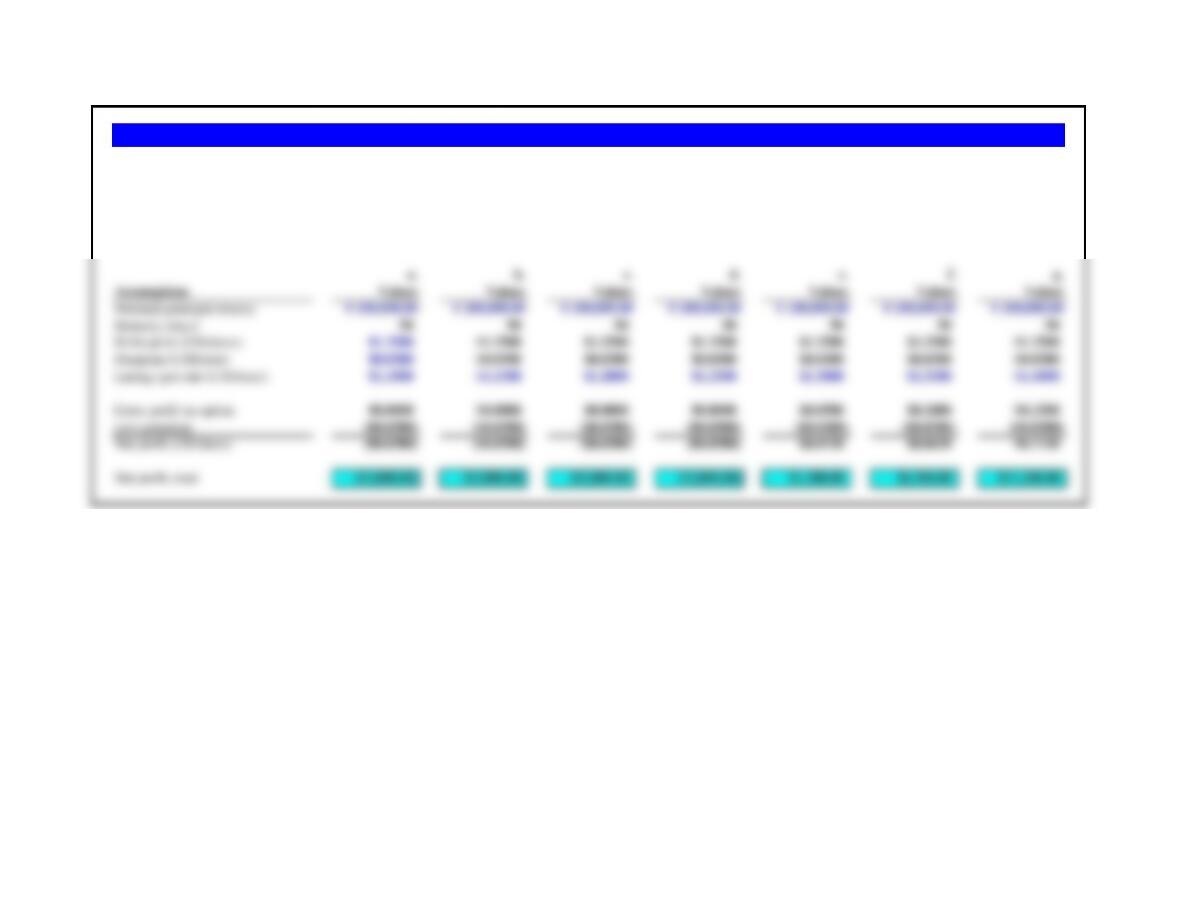

a. What is the value of her position at maturity if the ending spot rate is $0.12000/Ps?

b. What is the value of her position at maturity if the ending spot rate is $0.09800/Ps?

c. What is the value of her position at maturity if the ending spot rate is $0.11000/Ps?

a. b. c.

Assumptions Values Values Values

Number of pesos per futures contract 500,000 500,000 500,000

Number of contracts 8.00 8.00 8.00

Buy or sell the peso futures? Sell Sell Sell

Ending spot rate ($/peso) $0.12000 $0.09800 $0.11000

June futures settle price from Exh8.1 ($/peso) $0.10773 $0.10773 $0.10773

Spot – Futures $0.01227 ($0.00973) $0.00227

Value of total position at maturity (US$) ($49,080.00) $38,920.00 ($9,080.00)

Value = – Notional x (Spot – Futures) x 8

Interpretation

Amber buys at the spot price and sells at the futures price.

If the futures price is greater than the ending spot price, she makes a profit.

Problem 7.2 Amber McClain

Amber McClain, the currency speculator we met earlier in the chapter, sells eight June futures contracts for

500,000 pesos at the closing price quoted in Exhibit 7.1.

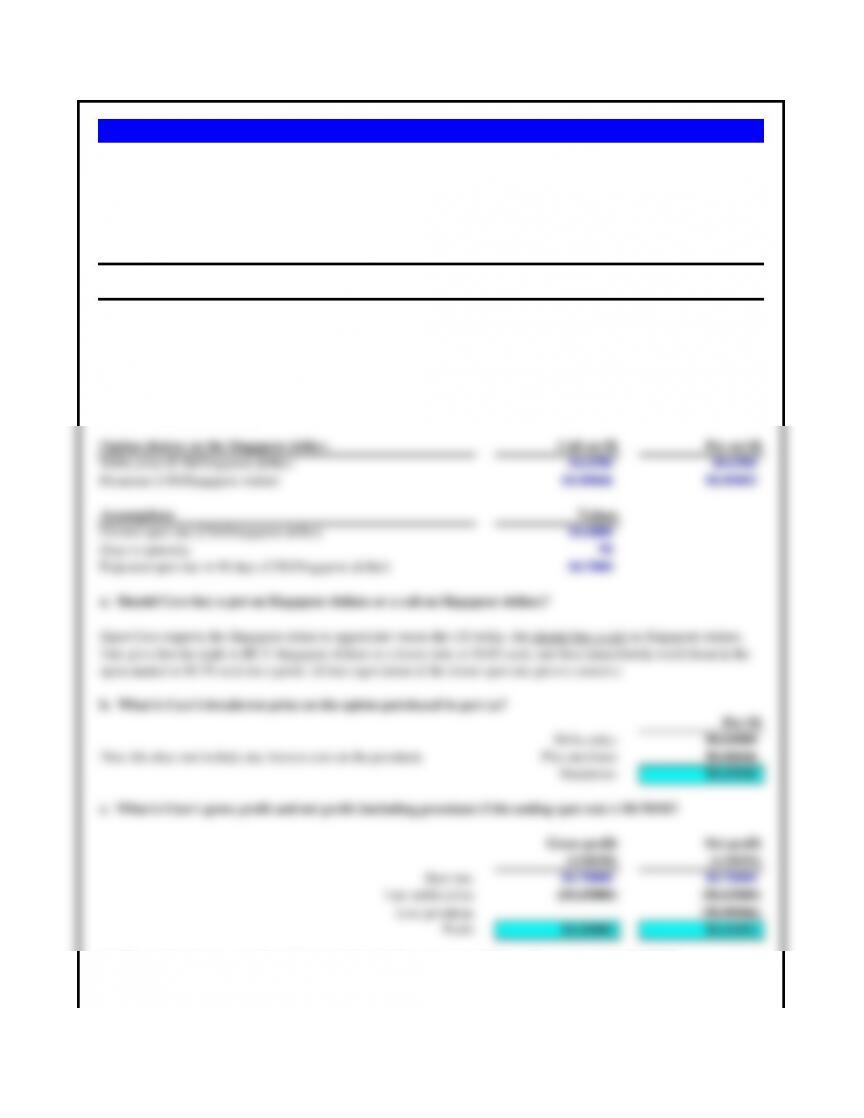

Option Strike Price Premium

Put on Sing $ $0.6500/S$ $0.00003/S$

Call on Sing $ $0.6500/S$ $0.00046/S$

a. Should Cece buy a put on Singapore dollars or a call on Singapore dollars?

b. What is Cece’s breakeven price on the option purchased in part (a)?

Option choices on the Singapore dollar: Call on S$ Put on S$

Strike price (US$/Singapore dollar) $0.6500 $0.6500

Premium (US$/Singapore dollar) $0.00046 $0.00003

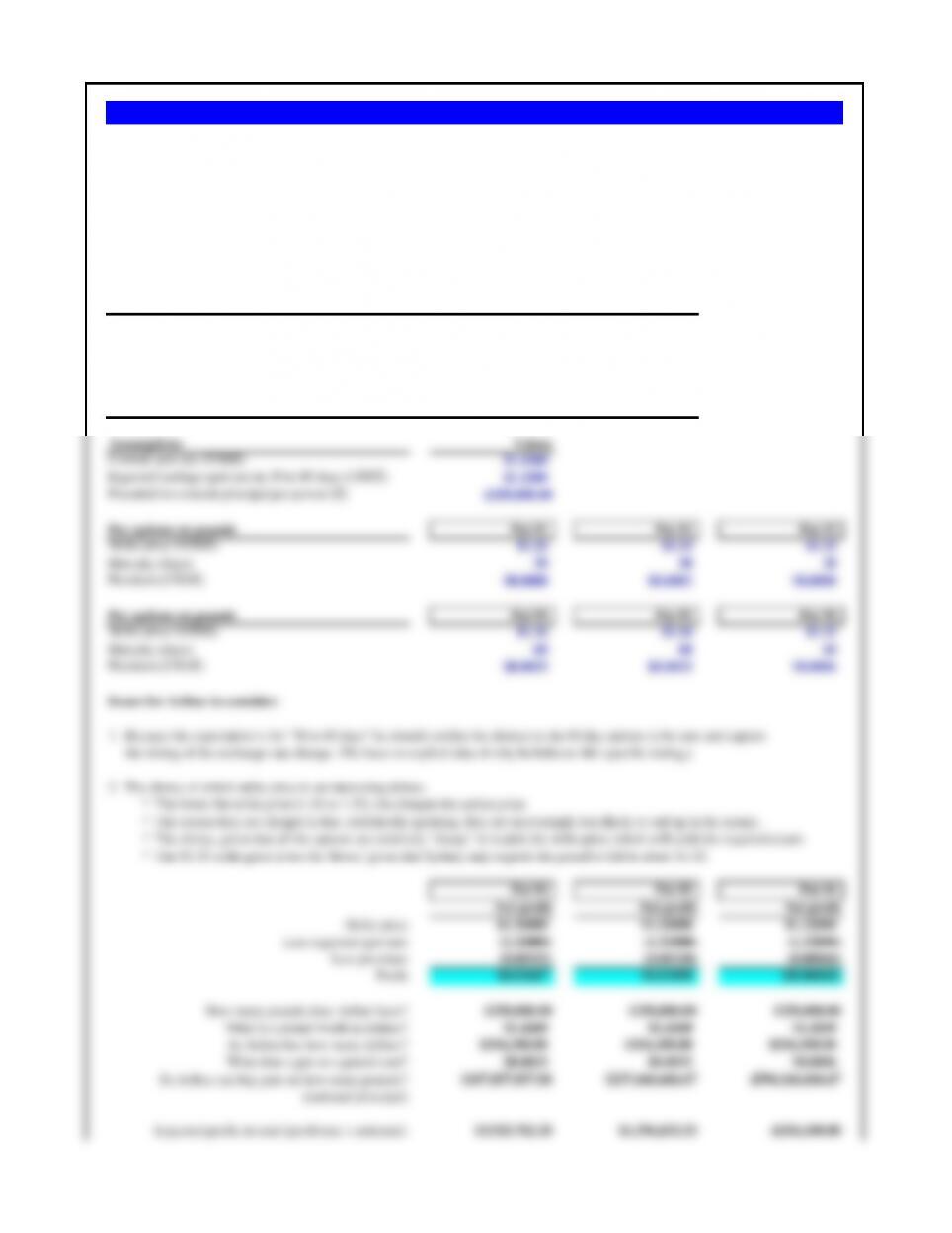

Assumptions Values

Current spot rate (US$/Singapore dollar) $0.6000

Days to maturity 90

Expected spot rate in 90 days (US$/Singapore dollar) $0.7000

a. Should Cece buy a put on Singapore dollars or a call on Singapore dollars?

b. What is Cece’s breakeven price on the option purchased in part a)?

Per S$

Strike price $0.65000

Note this does not include any interest cost on the premium. Plus premium $0.00046

Breakeven $0.65046

c. What is Cece’s gross profit and net profit (including premium) if the ending spot rate is $0.70/S$?

Gross profit Net profit

(US$/S$) (US$/S$)

Spot rate $0.70000 $0.70000

Less strike price ($0.65000) ($0.65000)

Less premium ($0.00046)

Profit $0.05000 $0.04954

d. What is Cece’s gross profit and net profit (including premium) if the ending spot rate is $0.80/S$?

Gross profit Net profit

Problem 7.3 Cece Cao in Jakarta

Cece Cao trades currencies for Sumatra Funds in Jakarta. She focuses nearly all of her time and attention on the U.S.

dollar/Singapore dollar ($/S$) cross-rate. The current spot rate is $0.6000/S$. After considerable study, she has concluded

that the Singapore dollar will appreciate versus the U.S. dollar in the coming 90 days, probably to about $0.7000/S$. She

has the following options on the Singapore dollar to choose from:

Since Cece expects the Singapore dollar to appreciate versus the US dollar, she should buy a call on Singapore dollars.

This gives her the right to BUY Singapore dollars at a future date at $0.65 each, and then immediately resell them in the

open market at $0.70 each for a profit. (If her expectation of the future spot rate proves correct.)

c. Using your answer from part (a), what is Cece’s gross profit and net profit (including premium) if the spot rate at the

end of 90 days is indeed $0.7000/S$?

d. Using your answer from part (a), what is Cece’s gross profit and net profit (including premium) if the spot rate at the

end of 90 days is $0.8000/S$?

(US$/S$) (US$/S$)

Spot rate $0.80000 $0.80000

Less strike price ($0.65000) ($0.65000)

Less premium ($0.00046)

Profit $0.15000 $0.14954

a. b.

Assumptions Values Values

Initial investment (funds available) $10,000,000 $10,000,000

Current spot rate (US$/€)$1.3358 $1.3358

30-day forward rate (US$/€)$1.3350 $1.3350

Expected spot rate in 30 days (US$/€)$1.3600 $1.2800

Strategy for Part a):

Initial investment principle $10,000,000.00

30 day forward rate (US$/€) $1.3350

Euros bought forward (Investment / forward rate) € 7,490,636.70

Spot rate in open market at end of 30 days (US$/€) $1.3600

US$ proceeds (euros bought forward exchanged to US$ spot) $10,187,265.92

Profit in US$ $187,265.92

Strategy for Part b):

Investment funds needed in 30 days $10,000,000.00

Spot rate in open market at end of 30 days $1.2800

Euros bought in open market in 30 days (Investment / spot rate) € 7,812,500.00

Christoph had sold these euros forward at the start of the 30 day period.

30 day forward rate (US$/€) $1.3350

US$ proceeds (euros sold forward into US$) $10,429,687.50

Profit in US$ $429,687.50

One of the more interesting dimensions of speculating in the forward market, is that if the speculator has access to the forward

market (bank lines or relationships when working on behalf of an established firm), many forward speculation strategies require

no actual cash flow position up-front. In this case, Christoph believes the dollar will be trading at $1.36/€ in the open market at

the end of 30 days, but he has the ability to buy or sell dollars at a forward rate of $1.3350/€. He should therefore buy euros

forward 30 days (requires no actual cash flow up-front), and at the end of 30 days take delivery of those euros and sell in the

spot market at the higher dollar rate for profit.

Again, a profitable strategy can be executed without any actual cash flow changing hands at the beginning of the period. Since

Christoph believes that the dollar will strengthen to $1.28 in 30 days, he should sell euros forward now at the higher dollar rate,

wait 30 days and buy the euros needed on the open market at $1.28, and immediately then use those euros to fulfill his forward

contract to sell euros for dollars at $1.3350. For a profit.

b. If Christoph believes the euro will depreciate in value against the U.S. dollar, so that he expects the spot rate to be $1.2800/€

at the end of 30 days, what should he do?

Problem 7.4 Kapinsky Capital (A)

Christoph Hoffeman trades currency for Kapinsky Capital of Geneva. Christoph has $10 million to begin with, and he must

state all profits at the end of any speculation in U.S. dollars. The spot rate on the euro is $1.3358/€, while the 30-day forward

rate is $1.3350/€.

a. If Christoph believes the euro will continue to rise in value against the U.S. dollar, so that he expects the spot rate to be

$1.3600/€ at the end of 30 days, what should he do?

a. Calculate Christoph’s expected profit assuming a pure spot market speculation strategy.

b. Calculate Christoph’s expected profit assuming he buys or sells SF three months forward.

a. b.

Assumptions Values Values

Initial investment (funds available) $100,000 $100,000

Current spot rate (US$/Swiss franc) $0.5820 $0.5820

Six-month forward rate (US$/Swiss franc) $0.5640 $0.5640

Expected spot rate in six months (US$/Swiss franc) $0.6250 $0.6250

Strategy for Part a:

1. Use the $100,000 today to buy SF at spot rate SFr. 171,821.31

2. Hold the SF indefinitely.

3. At the end of six months, convert SF at expected rate $0.6250

4. Yielding expected dollar revenues of $107,388.32

5. Realize profit (revenues less $100,000 initial invest) $7,388.32

Strategy for Part b:

1. Buy SF forward six months (no cash outlay required)

2. Fulfill the six months forward in six months SFr. 177,304.96

cost in US$ ($100,000.00)

3. Convert the SF into US$ at expected spot rate $110,815.60

4. Realize profit $10,815.60

Problem 7.5 Kapinsky Capital Geneva (B)

Christoph Hoffeman of Kapinsky Capital Geneva now believes the Swiss franc will appreciate versus the U.S.

dollar in the coming three-month period. He has $100,000 to invest. The current spot rate is $0.5820/SF, the three-

month forward rate is $0.5640/SF, and he expects the spot rates to reach $0.6250/SF in three months.

a) b) c) d) e) f) g)

Assumptions Values Values Values Values Values Values Values

Notional principal (¥)12,500,000 12,500,000 12,500,000 12,500,000 12,500,000 12,500,000 12,500,000

Maturity (days) 180 180 180 180 180 180 180

Strike price (US$/¥)$0.008000 $0.008000 $0.008000 $0.008000 $0.008000 $0.008000 $0.008000

Premium (US$/¥)$0.000080 $0.000080 $0.000080 $0.000080 $0.000080 $0.000080 $0.000080

Ending spot rate (¥/US$) 110.00 115.00 120.00 125.00 130.00 135.00 140.00

in US$/¥$0.009091 $0.008696 $0.008333 $0.008000 $0.007692 $0.007407 $0.007143

Gross profit on option $0.000000 $0.000000 $0.000000 $0.000000 $0.000308 $0.000593 $0.000857

Less premium ($0.000080) ($0.000080) ($0.000080) ($0.000080) ($0.000080) ($0.000080) ($0.000080)

Net profit (US$/¥)($0.000080) ($0.000080) ($0.000080) ($0.000080) $0.000228 $0.000513 $0.000777

Net profit, total ($1,000.00) ($1,000.00) ($1,000.00) ($1,000.00) $2,846.15 $6,407.41 $9,714.29

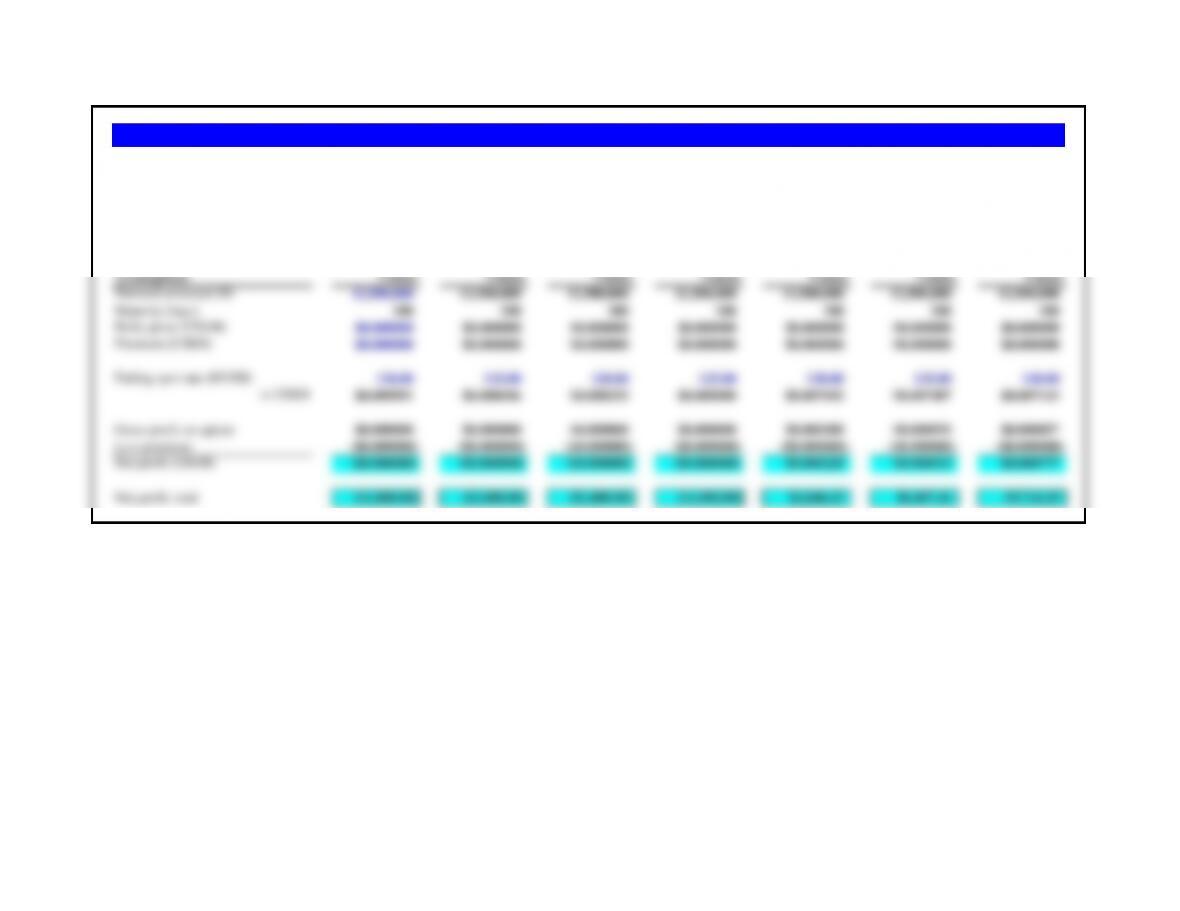

Problem 7.6 Peleh’s Puts

Peleh writes a put option on Japanese yen with a strike price of $0.008000/¥ (¥125.00/$) at a premium of 0.0080¢ per yen and with an expiration date six month from now.

The option is for ¥12,500,000. What is Peleh’s profit or loss at maturity if the ending spot rates are ¥110/$, ¥115/$, ¥120/$, ¥125/$, ¥130/$, ¥135/$, and ¥140/$.

Assumptions Values

Principal borrowing need 8,000,000$

Maturity needed, in weeks 8

Rate of interest charged by ALL potential lenders 6.250%

New York interest rate practices

Interest calculation uses:

Exact number of days in period 56

Number of days in financial year 360

So the interest charge on this principal is 77,777.78$

Great Britain interest rate practices

Interest calculation uses:

Exact number of days in period 56

Number of days in financial year 360

So the interest charge on this principal is 77,777.78$

Swiss interest rate practices

Interest calculation uses:

Assumed 30 days per month for two months 60

Number of days in financial year 360

So the interest charge on this principal is 83,333.33$

Problem 7.7 Chavez S.A.

Chavez S.A., a Venezuelan company, wishes to borrow $8,000,000 for eight

weeks. A rate of 6.250% per annum is quoted by potential lenders in New York,

Great Britain, and Switzerland using, respectively, international, British, and the

Swiss-Eurobond definitions of interest (day count conventions). From which

source should Chavez borrow?

Chavez should borrow in Great Britain or New York because they both have the

lowest interest cost.

Option Strike Price Premium

Put on yen ¥125/$ $0.00003/S$

Call on yen ¥125/$ $0.00046/S$

a. Should Cachita buy a put on yen or a call on yen?

b. What is Cachita’s breakeven price on the option purchased in part (a)?

Assumptions Values

Current spot rate (Japanese yen/US$) 120.00

in US$/yen $0.00833

Maturity of option (days) 90

Expected ending spot rate in 90 days (yen/$) 140.00

in US$/yen $0.00714

Call on yen Put on yen

Strike price (yen/US$) 125.00 125.00

in US$/yen $0.00800 $0.00800

Premium (US$/yen) $0.00046 $0.00003

a. Should she buy a call on yen or a put on yen?

Cachita should buy a put on yen to profit from the rise of the dollar (the fall of the yen).

b. What is Cachita’s break even price on her option of choice in part a)?

Cachita buys a put on yen. Pays premium today.

In 90 days, exercises the put, receiving US$.

in yen/$

Strike price $0.00800 125.00

Less premium -$0.00003

Breakeven $0.00797 125.47

c. What is Cachita’s gross profit and net profit if the end spot rate is 140 yen/$?

Gross profit Net profit

(US$/yen) (US$/yen)

Strike price $0.00800 $0.00800

Less spot rate -$0.00714 -$0.00714

Less premium -$0.00003

Profit $0.00086 $0.00083

Problem 7.8 Cachita Haynes at Vatic Capital

Cachita Haynes works as a currency speculator for Vatic Capital of Los Angeles. Her latest speculative

position is to profit from her expectation that the U.S. dollar will rise significantly against the Japanese yen.

The current spot rate is ¥120.00/$. She must choose between the following 90-day options on the Japanese

yen:

c. Using your answer from part (a), what is Cachita’s gross profit and net profit (including premium) if the

spot rate at the end of 90 days is ¥140/$?

Note: the option premium is 3.8 cents per euro, not 38 cents per euro.

a. b. c. d. e. f. g.

Assumptions Values Values Values Values Values Values Values

Notional principal (euros) € 100,000.00 € 100,000.00 € 100,000.00 € 100,000.00 € 100,000.00 € 100,000.00 € 100,000.00

Maturity (days) 90 90 90 90 90 90 90

Strike price (US$/euro) $1.2500 $1.2500 $1.2500 $1.2500 $1.2500 $1.2500 $1.2500

Premium (US$/euro) $0.0380 $0.0380 $0.0380 $0.0380 $0.0380 $0.0380 $0.0380

Ending spot rate (US$/euro) $1.1000 $1.1500 $1.2000 $1.2500 $1.3000 $1.3500 $1.4000

Gross profit on option $0.0000 $0.0000 $0.0000 $0.0000 $0.0500 $0.1000 $0.1500

Less premium ($0.0380) ($0.0380) ($0.0380) ($0.0380) ($0.0380) ($0.0380) ($0.0380)

Net profit (US$/euro) ($0.0380) ($0.0380) ($0.0380) ($0.0380) $0.0120 $0.0620 $0.1120

Net profit, total ($3,800.00) ($3,800.00) ($3,800.00) ($3,800.00) $1,200.00 $6,200.00 $11,200.00

Problem 7.9 Calling All Euros

Assume a call option on euros is written with a strike price of $1.2500/€ at a premium of 3.80¢ per euro ($0.0380/€) and with an expiration date three months from now. The

option is for €100,000. Calculate your profit or loss should you exercise before maturity at a time when the euro is traded spot at strike prices beginning at $1.10/€, rising to

$1.40/€ in increments of $0.05.

Strike Price Maturity Premium

$1.36/£ 30 days $0.00081/£

$1.34/£ 30 days $0.00021/£

$1.32/£ 30 days $0.00004/£

$1.36/£ 60 days $0.00333/£

$1.34/£ 60 days $0.00150/£

$1.32/£ 60 days $0.00060/£

Assumptions Values

Current spot rate (US$/£)$1.4260

Expected endings spot rate in 30 to 60 days (US$/£)$1.3200

Potential investment principal per person (£)£250,000.00

Put options on pounds Put #1 Put #2 Put #3

Strike price (US$/£)$1.36 $1.34 $1.32

Maturity (days) 30 30 30

Premium (US$/£)$0.0008 $0.0002 $0.0000

Put options on pounds Put #4 Put #5 Put #6

Strike price (US$/£)$1.36 $1.34 $1.32

Maturity (days) 60 60 60

Premium (US$/£)$0.0033 $0.0015 $0.0006

Issues for Arthur to consider:

1. Because his expectation is for “30 to 60 days” he should confine his choices to the 60 day options to be sure and capture

the timing of the exchange rate change. (We have no explicit idea of why he believes this specific timing.)

2. The choice of which strike price is an interesting debate.

* The lower the strike price (1.34 or 1.32), the cheaper the option price.

* The reason they are cheaper is that, statistically speaking, they are increasingly less likely to end up in the money.

* The choice, given that all the options are relatively “cheap,” is to pick the strike price which will yield the required return.

* The $1.32 strike price is too far ‘down,’ given that Sydney only expects the pound to fall to about $1.32.

Put #4 Put #5 Put #6

Net profit Net profit Net profit

Strike price $1.36000 $1.34000 $1.32000

Less expected spot rate (1.32000) (1.32000) (1.32000)

Less premium (0.00333) (0.00150) (0.00060)

Profit $0.03667 $0.01850 ($0.00060)

How many pounds does Arthur have? £250,000.00 £250,000.00 £250,000.00

What is a pound worth in dollars? $1.4260 $1.4260 $1.4260

So Arthur has how many dollars? $356,500.00 $356,500.00 $356,500.00

What does a put on a pound cost? $0.0033 $0.0015 $0.0006

So Arthur can buy puts on how many pounds? £107,057,057.06 £237,666,666.67 £594,166,666.67

(notional principal)

Expected profit, in total (profit rate x notional): $3,925,782.28 $4,396,833.33 -$356,500.00

Problem 7.10 Arthur Doyle at Baker Street

Arthur Doyle is a currency trader for Baker Street, a private investment house in London. Baker Street’s clients are a collection of

wealthy private investors who, with a minimum stake of £250,000 each, wish to speculate on the movement of currencies. The investors

expect annual returns in excess of 25%. Although officed in London, all accounts and expectations are based in U.S. dollars.

Arthur is convinced that the British pound will slide significantly — possibly to $1.3200/£ — in the coming 30 to 60 days. The current

spot rate is $1.4260/£. Arthur wishes to buy a put on pounds which will yield the 25% return expected by his investors. Which of the

following put options would you recommend he purchase. Prove your choice is the preferable combination of strike price, maturity, and

up-front premium expense.

Initial investment at current spot rate $356,500.00 $356,500.00 $356,500.00

Return on Investment (ROI) 1101% 1233% -100%

Risk: They could lose it all (full premium)

Note that the return on investment is driven by the difference between the curent spot rate and the expected spot rate (relative to strike

rate). It is not a function of the notional principal. The ROI is the same whether it is on one British pound or 250,000.

Option Strike Price Premium

Put on C$ $0.7000 $0.00003/S$

Call on C$ $0.7000 $0.00049/S$

a. Should Calandra buy a put on Canadian dollars or a call on Canadian dollars?

b. What is Calandra’s breakeven price on the option purchased in part (a)?

Assumptions Values

Current spot rate (US$/Canadian dollar) $0.6750

Days to maturity 90

Option choices on the Canadian dollar: Call option Put option

Strike price (US$/Canadian dollar) $0.7000 $0.7000

Premium (US$/Canadian dollar) $0.00049 $0.0003

a) Which option should Calandra buy?

Since Calandra expects the Canadian dollar to appreciate versus the US dollar, she should buy a call on Canadian dollars.

b) What is Calandra’s breakeven price on the option purchased in part a)?

Strike price $0.7000

Plus premium 0.00049

Breakeven $0.7005

c) What is Calandra’s gross profit and net profit (including premium) if the ending spot rate is $0.7600/C$?

Gross profit Net profit

(US$/C$) (US$/C$)

Spot rate $0.7600 $0.7600

Less strike price (0.7000) (0.7000)

Less premium (0.00049)

Profit $0.0600 $0.05951

d) What is Calandra’s gross profit and net profit (including premium) if the ending spot rate is $0.8250/C$?

Gross profit Net profit

(US$/C$) (US$/C$)

Spot rate $0.8250 $0.8250

Less strike price (0.7000) (0.7000)

Problem 7.11 Calandra Panagakos at CIBC

Calandra Panagakos works for CIBC Currency Funds in Toronto. Calandra is something of a contrarian — as opposed

to most of the forecasts, she believes the Canadian dollar (C$) will appreciate versus the U.S. dollar over the coming

90 days. The current spot rate is $0.6750/C$. Calandra may choose between the following options on the Canadian

c. Using your answer from part (a), what is Calandra’s gross profit and net profit (including premium) if the spot rate

at the end of 90 days is indeed $0.7600?

d. Using your answer from part (a), what is Calandra’s gross profit and net profit (including premium) if the spot rate

at the end of 90 days is $0.8250?

Less premium (0.00049)

Profit $0.1250 $0.12451

Pricing Currency Options on the Euro

Variable Value Variable Value

Spot rate (domestic/foreign)

S0$1.2480 S0€ 0.8013

Strike rate (domestic/foreign) X $1.2500 X€ 0.8000

Domestic interest rate (% p.a.)

rd1.453% rd2.187%

Foreign interest rate (% p.a.)

rf2.187% rf1.453%

Time (years, 365 days) T 1.000 T1.000

Days equivalent 365.00 365.00

Volatility (% p.a.) s 12.000% s 12.000%

Call option premium (per unit fc) c $0.0534 c € 0.0412

Put option premium (per unit fc) p $0.0643 p € 0.0342

(European pricing)

Call option premium (%) c 4.28% c 5.15%

Put option premium (%) p 5.15% p 4.27%

When the volatility is increased to 12.000% from 10.500%, the premium on the call option on euros rises to $0.0412/€, or 5.15%.

Problem 7.12 U.S. dollar/Euro

A U.S.-based firm wishing to buy

A European firm wishing to buy

or sell euros (the foreign currency)

or sell dollars (the foreign currency)

Pricing Currency Options on the Japanese yen

Variable Value Variable Value

Spot rate (domestic/foreign)

S0JPY 105.64 S0$0.0095

Strike rate (domestic/foreign) X JPY 100.00 X$0.0100

Domestic interest rate (% p.a.)

rd0.089% rd1.453%

Foreign interest rate (% p.a.)

rf1.453% rf0.089%

Time (years, 365 days) T 1.000 T1.000

Days equivalent 365.00 365.00

Volatility (% p.a.) s 12.000% s12.000%

Call option premium (per unit fc) c JPY 7.27 c $0.0003

Put option premium (per unit fc) p JPY 3.06 p $0.0007

(European pricing)

Call option premium (%) c 6.88% c 3.06%

Put option premium (%) p 2.90% p 7.27%

A Japanese firm wishing to sell U.S. dollars would need to purchase a put on dollars. The put option premium listed above is JPY3.06/$.

Put option premium (JPY/US$) JPY 3.06

Notional principal (US$) $750,000

Total cost (JPY) JPY 2,297,243

or sell dollars (the foreign currency)

or sell yen (the foreign currency)

Problem 7.13 U.S. Dollar/Japanese Yen

A Japanese firm wishing to buy

A U.S.-based firm wishing to buy

Pricing Currency Options on the Euro/Yen Crossrate

Variable Value Variable Value

Spot rate (domestic/foreign)

S0JPY 133.89 S0€ 0.0072

Strike rate (domestic/foreign) X JPY 136.00 X€ 0.0074

Domestic interest rate (% p.a.)

rd0.088% rd2.187%

Foreign interest rate (% p.a.)

rf2.187% rf0.088%

Time (years, 365 days) T 0.247 T0.247

Days equivalent 90.00 90.00

Volatility (% p.a.) s 10.000% s10.000%

Call option premium (per unit fc) c JPY 1.50 c € 0.0001

Put option premium (per unit fc) p JPY 4.30 p € 0.0002

(European pricing)

Call option premium (%) c 1.12% c 1.30%

Put option premium (%) p 3.21% p 2.90%

Put option premium (euro/JPY) € 0.0002

Notional principal (JPY) JPY 10,400,000

Total cost (euro) € 2,167.90

Problem 7.14 Euro/Japanese Yen

A European-based firm like Legrand (France) would need to purchase a put option on the Japanese yen. The company wishes a strike rate of 0.0072 euro

for each yen sold (the strike rate) and a 90-day maturity. Note that the “Time” must be entered as the fraction of a 365 day year, in this case, 90/365 =

0.247.

A Japanese firm wishing to buy

A European firm wishing to buy

or sell euros (the foreign currency)

or sell yen (the foreign currency)

Pricing Currency Options on the British pound

Variable Value Variable Value

Spot rate (domestic/foreign)

S0$1.8674 S0£0.5355

Strike rate (domestic/foreign) X $1.8000 X£0.5556

Domestic interest rate (% p.a.)

rd1.453% rd4.525%

Foreign interest rate (% p.a.)

rf4.525% rf1.453%

Time (years, 365 days) T 0.493 T0.493

Days equivalent 180.00 180.00

Volatility (% p.a.) s 9.400% s9.400%

Call option premium (per unit fc) c $0.0696 c £0.0091

Put option premium (per unit fc) p $0.0306 p £0.0207

(European pricing)

Call option premium (%) c 3.73% c 1.70%

Put option premium (%) p 1.64% p 3.87%

Call option premiums for a U.S.-based firm buying call options on the British pound:

180-day maturity ($/pound) $0.0696

90-day maturity ($/pound) $0.0669

Difference ($/pound) $0.0027

The maturity doubled while the option premium rose only about 4%.

Problem 7.15 U.S. Dollar/British Pound

A U.S.-based firm wishing to buy

A British firm wishing to buy

or sell pounds (the foreign currency)

or sell dollars (the foreign currency)

Pricing Currency Options on the British pound/Euro Crossrate

Variable Value Variable Value

Spot rate (domestic/foreign)

S0€ 1.4730 S0£0.6789

Strike rate (domestic/foreign) X € 1.5000 X£0.6667

Domestic interest rate (% p.a.)

rd4.000% rd4.160%

Foreign interest rate (% p.a.)

rf4.160% rf4.000%

Time (years, 365 days) T 0.247 T0.247

Days equivalent 90.00 90.00

Volatility (% p.a.) s 11.400% s11.400%

Call option premium (per unit fc) c € 0.0213 c £0.0220

Put option premium (per unit fc) p € 0.0487 p £0.0097

(European pricing)

Call option premium (%) c 1.45% c 3.24%

Put option premium (%) p 3.30% p 1.42%

When the euro’s interest rate rises from 2.072% to 4.000%, the call option premium on British pounds rises:

Call option on pounds when euro interest is 4.000% € 0.0213

Call option on pounds when euro interest is 2.072% € 0.0189

Change, an increase in the premium € 0.0213

Problem 7.16 Euro/British Pound

A European firm wishing to buy

A British firm wishing to buy

or sell pounds (the foreign currency)

or sell euros (the foreign currency)