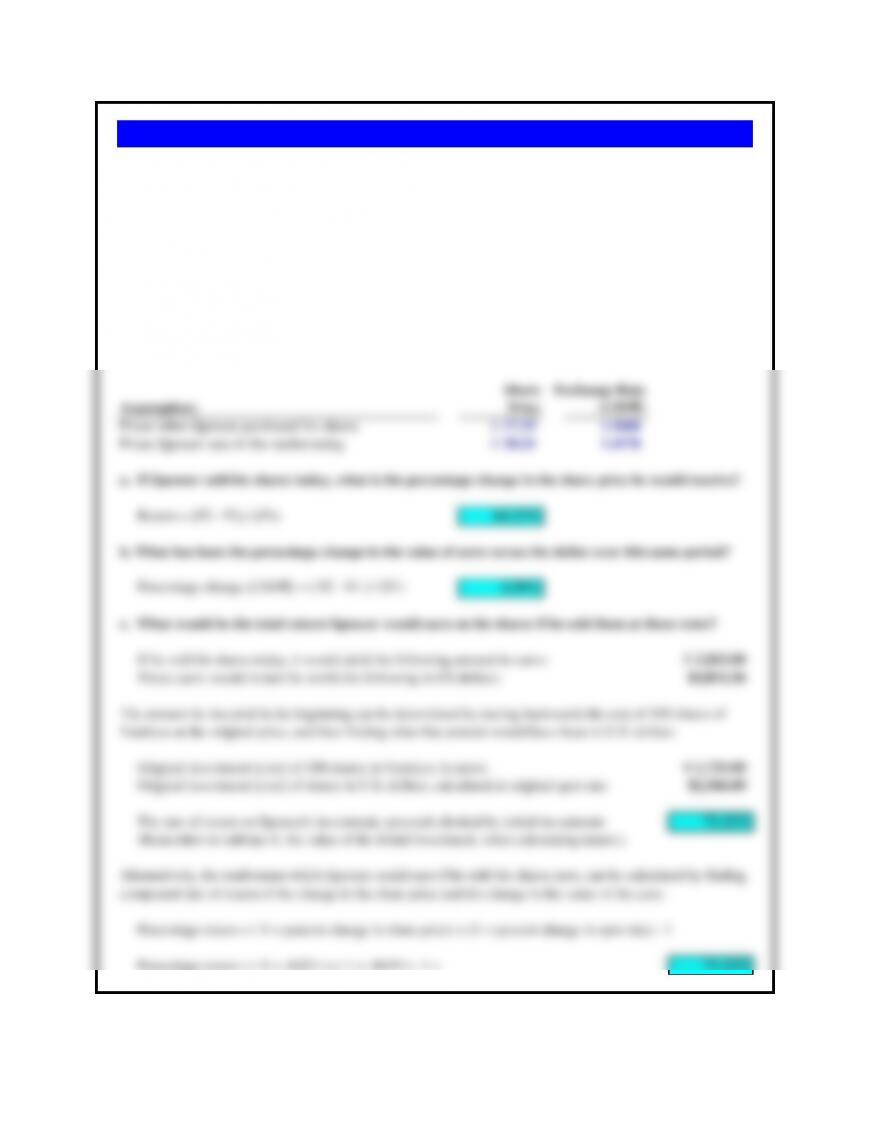

Assumptions Value

Share price, P1 12.00$

Share price, P2 15.00$

Dividend paid, D2 –$

a. If the company paid no dividend (plugging zero in for the dividend):

Return = ( D2 / P1 ) + ( P2 – P1 ) / P1 25.000%

b. And if the company paid a $1.00 dividend:

Assumptions Value

Share price, P1 12.00$

Share price, P2 15.00$

Dividend paid, D2 1.00$

Total shareholder return, including dividends, is: 33.333%

Return = ( D2 / P1 ) + ( P2 – P1 ) / P1

Dividend yield is D2 / P1 8.333%

Capital gain is (P2 – P1) / (P1) 25.000%

Total shareholder return is the sum of the two 33.333%

c. Assuming it did pay the dividend, separate the shareholder’s total return

into its two components — the dividend yield and the capital gain.

Problem 4.1 Emaline Returns

If the share price of Emaline, a New Orleans-based shipping firm, rises from

$12 to $15 over a one-year period, what is the rate of return to the

shareholder given each of the following:

a. The company paid no dividends

b. The company paid a dividend of $1 per share

c. The company paid the dividend and the total return to the shareholder is

separated into the dividend yield and the capital gain

Share Exchange Rate

Assumptions Price (US$/€)

Prices when Spencer purchased his shares € 17.25 1.3600

Prices Spencer sees in the market today € 28.33 1.4170

a. If Spencer sold his shares today, what is the percentage change in the share price he would receive?

Return = (P2 – P1) / (P1) 64.23%

b. What has been the percentage change in the value of euro versus the dollar over this same period?

Percentage change (US$/€) = ( S2 – S1 ) / (S1) 4.19%

c. What would be the total return Spencer would earn on his shares if he sold them at these rates?

If he sold his shares today, it would yield the following amount in euros: € 2,833.00

These euros would in turn be worth the following in US dollars: $4,014.36

Original investment (cost) of 100 shares in Vaniteux in euros: € 1,725.00

Original investment (cost) of shares in U.S. dollars, calculated at original spot rate: $2,346.00

The rate of return on Spencer’s investment, proceeds divided by initial investment: 71.12%

(Remember to subtract 1, the value of the initial investment, when calculating return.)

Percentage return = ( 1 + percent change in share price) x (1 + percent change in spot rate) – 1

Percentage return = ( 1 + .6423 ) x ( 1 + .0419 ) – 1 = 71.12%

The amount he invested in the beginning can be determined by tracing backwards the cost of 100 shares of

Vaniteux at the original price, and then finding what that amount would have been in U.S. dollars.

Alternatively, the total return which Spencer could earn if he sold his shares now, can be calculated by finding

compound rate of return of the change in the share price and the change in the value of the euro.

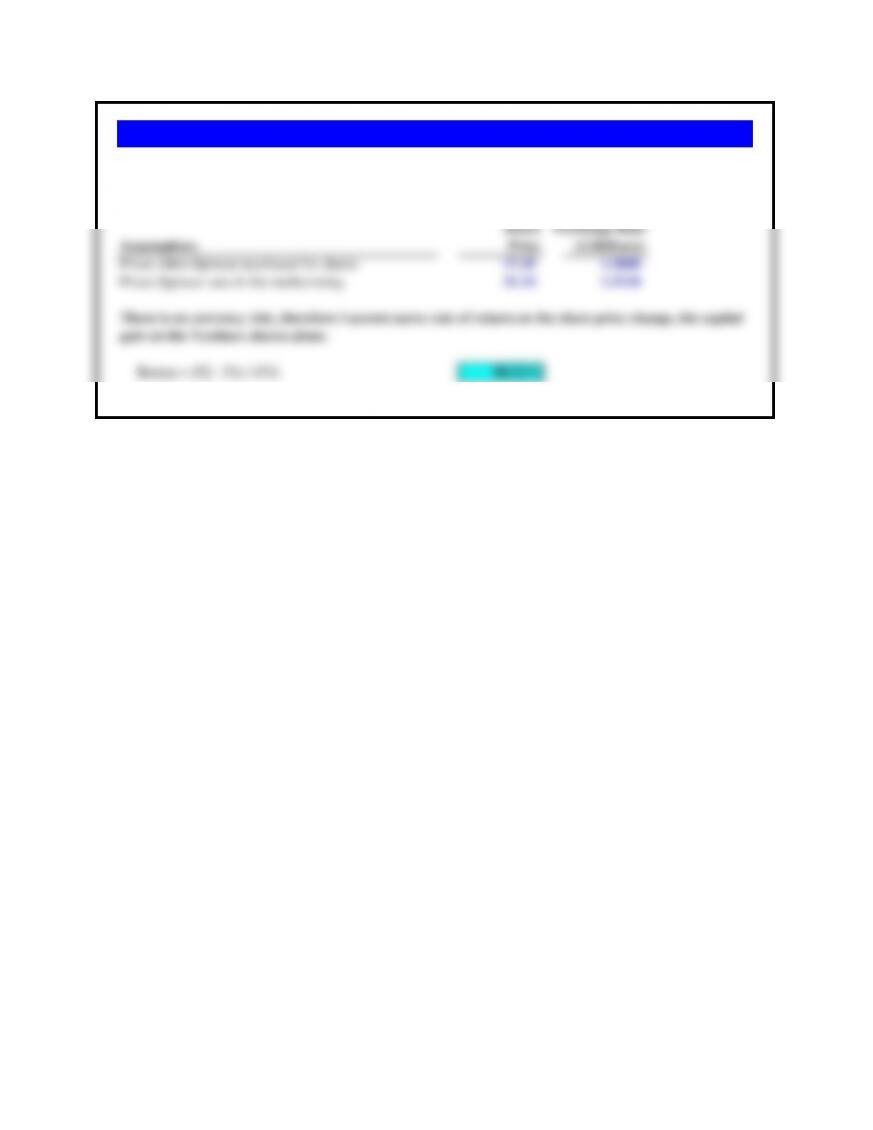

Problem 4.2 Vaniteux’s Returns (A)

Spencer Grant is a New York-based investor. He has been closely following his investment in 100 shares of

Vaniteux, a French firm that went public in February of 2010. When he purchased his 100 shares at €17.25 per

share, the euro was trading at $1.360/€. Currently, the share is trading at €28.33 per share, and the dollar has

fallen to $1.4170/€.

a. If Spencer sells his shares today, what percentage change in the share price would he receive?

b. What is the percentage change in the value of euro versus the dollar over this same period?

c. What would be the total return Spencer would earn on his shares if he sold them at these rates?

Share Exchange Rate

Assumptions Price (US$/Euro)

Prices when Spencer purchased his shares 17.25 1.3600

Prices Spencer sees in the market today 31.14 1.3110

a. If Spencer sold his shares today, what is the percentage change in the share price he would receive?

Return = (P2 – P1) / (P1) 80.52%

b. What has been the percentage change in the value of euro versus the dollar over this same period?

Percentage change (US$/euro) = ( S2 – S1 ) / (S1) -3.60%

c. What would be the total return Spencer would earn on his shares if he sold them at these rates?

If he sold his shares today, it would yield the following amount in euros: 3,114.00

These euros would in turn be worth the following in U.S. dollars: $4,082.45

Original investment (cost) of 100 shares in Vaniteux in euros: 1,725.00

Original investment (cost) of shares in U.S. dollars, calculated at original spot rate: $2,346.00

The rate of return on Spencer’s investment, proceeds divided by initial investment: 74.02%

(Remember to subtract 1, the value of the initial investment, when calculating return.)

Percentage return = ( 1 + percent change in share price) x (1 + percent change in spot rate) – 1

Percentage return = ( 1 + .8052 ) x ( 1 + -.0360 ) – 1 = 74.02%

Problem 4.3 Vaniteux’s Returns (B)

Ironically, although the share price has risen considerably more, the fall in the value of the euro has offset that

gain, resulting in nearly the identical same total return as in the previous problem.

The amount he invested in the beginning can be determined by tracing backwards the cost of 100 shares of

Vaniteux at the original price, and then finding what that amount would have been in U.S. dollars.

Alternatively, the total return which Spencer could earn if he sold his shares now, can be calculated by finding

compound rate of return of the change in the share price and the change in the value of the euro.

Spencer Grant chooses not to sell his shares at the time described in problem 4.2. He waits, expecting the

share price to rise further after the announcement of quarterly earnings. His expectations are correct and the

share price rises to €31.14 per share after the announcement. He now wishes to recalculate his returns. The

current spot exchange rate is $1.3110/€.

Note that the dollar has now actually appreciated versus the euro from Spencer’s initial purchase date. This

results in a negative percentage change in the value of the euro, and therefore a negative percentage change.

Share Exchange Rate

Assumptions Price (US$/Euro)

Prices when Spencer purchased his shares 17.25 1.3600

Prices Spencer sees in the market today 31.14 1.3110

Return = (P2 – P1) / (P1) 80.52%

Using the same prices and exchange rates as in problem 4.3, Vaniteux (B), what would be the total return on

the Vaniteux investment by Laurent Vuagnoux, a Paris-based investor?

There is no currency risk, therefore Laurent earns rate of return on the share price change, the capital

gain on the Vaniteux shares alone.

Problem 4.4 Vaniteux’s Returns ( C )

Closing If Shareholder Shareholder

Share Dividend Return Return

Date Price Paid (without Div) (with Div)

1998 (January 2) 131.13$

1999 (January 4) 141.00$ 0.16$ 7.53% 7.65%

2000 (January 3) 116.56$ 0.16$ -17.33% -17.22%

2001 (January 2) 43.38$ 0.16$ -62.78% -62.65%

2002 (January 2) 67.04$ 0.16$ 54.54% 54.91%

2003 (January 2) 53.72$ 0.16$ -19.87% -19.63%

a. Average annual shareholder return for the period is -7.58%

Return = (P2 – P1) / (P1)

b. Average annaul shareholder return if Microsoft had paid a constant dividend: -7.39%

Return = (P2 – P1 + D) / (P1)

In January 2003, Microsoft announced that it would begin paying a dividend of $0.16 per share. Given the following share prices

for Microsoft stock in the recent past, how would a constant dividend of $0.16 per share per year have changed the company’s

average annual return to its shareholders over this period?

Problem 4.5 Microsoft’s dividend

Problem 4.6 Carty’s Choices

Assumptions Value

Share price, P1 59.00$

Share price, P2 71.00$

Dividend paid, D2 1.75$

Total shareholder return for the period is 23.31%

Return = (P2 – P1 + D2) / (P1)

The share’s expected return of 23.31% far exceeds the required return

by Mr. Carty of 15%. He should therefore make the investment.

Brian Carty, a prominent investor, is evaluating investment alternatives.

If he believes an individual equity will rise in price from $59 to $71 in the

coming one-year period, and the share is expected to pay a dividend of

$1.75 per share, and he expects at least a 15% rate of return on an

investment of this type, should he invest in this particular equity?

Market Total

Number value Market

Company P/E ratio of shares per share Earnings EPS Value

ModoUnico 20 10,000,000 20.00$ 10,000,000$ 1.00$ 200,000,000$

Modern American 40 10,000,000 40.00$ 10,000,000$ 1.00$ 400,000,000$

Rate of exchange — Modern American shares offered:

5,500,000

a. How many shares would Modern American have outstanding after the acquisition of ModoUnico?

10,000,000 + 5,500,000 15,500,000

So, Modern American pays: 10 million divided by 2 x (1 + 10% premium)

b. What would be the consolidated earnings of the combined Modern American and ModoUnico?

ModoUnico earnings + Modern American earnings 20,000,000$

P/E x Consolidated earnings = 40 x $20,000,000 800,000,000$

d. What would be the new earnings per share of Modern American?

$20,000,000 / 15,500,000 shares 1.29$

e. What would be the new market value of a share of Modern American?

New market value / Total shares outstanding = $800,000,000 / 15,500,000 51.61$

f. How much would Modern American’s stock price increase?

Share price rose from $40.00 to $51.61. 11.61$

Percentage increase 29.03%

g. Assume that the market takes a negative view of the acquisition and lowers Modern American’s P/E ratio to 30.

What would be the new market price per share of stock? What would be its percentage loss?

c. Assuming the market continues to capitalize Modern American’s earnings at a P/E ratio of 40, what would be the new market

value of Modern American?

Modern American wants to acquire ModoUnico. It offers 5,500,000 shares of Modern American, with a current market value of

$220,000,000 and a 10% premium on ModoUnico’s shares, for all of ModoUnico’s shares.

During the 1960s, many conglomerates were created by a firm enjoying a high price/earnings ratio (P/E). These firms then used their highly–

valued stock to acquire other firms that had lower P/E ratios, usually in unrelated domestic industries. Conglomerates went out of fashion

during the 1980s when they lost their high P/E ratios, thus making it more difficult to find other firms with lower P/E ratios to acquire.

During the 1990s, the same acquisition strategy was possible for firms located in countries where high P/E ratios were common compared to

firms in other countries where low P/E ratios were common. Consider the hypothetical firms in the pharmaceutical industry shown in the

following table:

Problem 4.7 Fashion Acquisitions

Because ModoUnico shares are worth $20 per share, they are only worth one-half the value per share of Modern American’s $40 per share.

So, on a straight exchange, 1 Modern American share is worth 2 ModoUnico shares. But, Modern American also needs to pay a premium for

gaining control of ModoUnico, so it pays an additional 10% over market.

New market value = Total earnings x P/E = $20,000,000 x 30 600,000,000$

New market price per share = total market value / shares outstanding = 38.71$

Percentage loss to original Modern American shareholders = ($38.71 – $40.00)/ ($40.00) -3.23%

Problem 4.8 Corporate Governance: Overstating Earnings

Market Total

Number value Market

Company P/E ratio of shares per share Earnings EPS Value

Modo Unico 20 10,000,000 20.00$ 10,000,000$ 1.00$ 200,000,000$

Modern American 40 10,000,000 20.00$ 5,000,000$ 1.00$ 200,000,000$

If earnings were lowered to $5 million from the previously reported $10 million, could Modern American still do the deal?

To do the deal, Modo Unico’s shareholders need to be paid their market value plus a 10% premium, or 220,000,000$

At new market rates for Modern American, this would require the offer of ($220 million/$20 per share) 11,000,000

shares

This 11 million shares would exceed Modern American’s existing shares outstanding, effectively giving Modo Unico control.

Therefore the acquistion would probably not take place.

A number of firms, especially in the United States, have had to lower their previously reported earnings due to accounting errors or

fraud. Assume that Modern American (problem 4.7) had to lower its earnings to $5,000,000 from the previously reported $10,000,000.

What might be its new market value prior to the acquisition? Could it still do the acquisition?

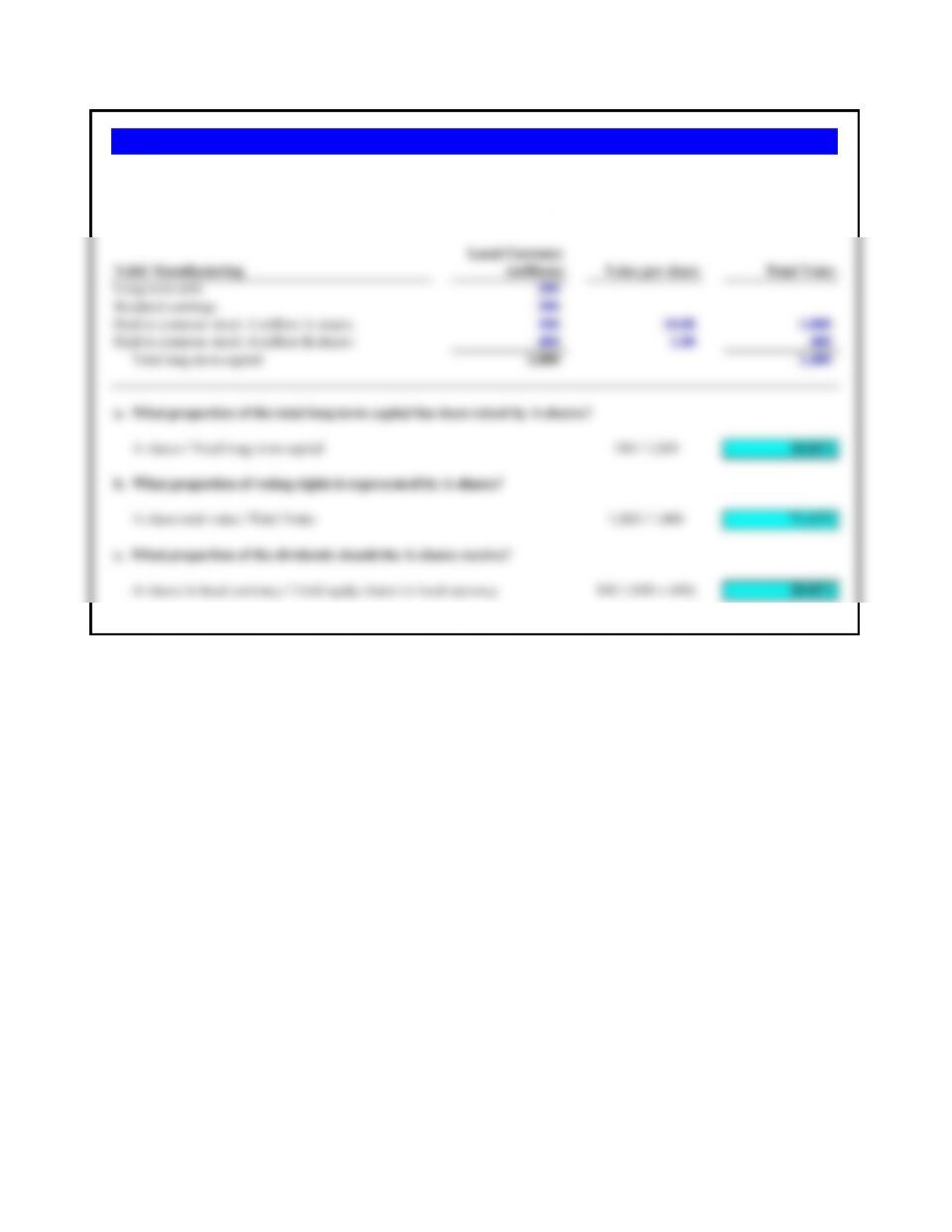

Local Currency

Yehti Manufacturing (millions) Votes per share Total Votes

Long-term debt 200

Retained earnings 300

Paid-in common stock: 1 million A-shares 100 10.00 1,000

Paid-in common stock: 4 million B-shares 400 1.00 400

Total long-term capital 1,000 1,400

a. What proportion of the total long-term capital has been raised by A-shares?

A-shares / Total long-term capital 100 / 1,000 10.00%

b. What proportion of voting rights is represented by A-shares?

A-share total votes / Total Votes 1,000 / 1,400 71.43%

c. What proportion of the dividends should the A-shares receive?

A-shares in local currency / Total equity shares in local currency 100 / (100 + 400) 20.00%

Dual classes of common stock are common in a number of countries. Assume that Yehti Manufacturing has the following

capital structure at book value. The A-shares each have ten votes and the B-shares each have one vote per share.

Problem 4.9 Yehti Manufacturing (A)

Local Currency

Yehti Manufacturing (millions) Votes per share Total Votes

Long-term debt 200

Retained earnings 300

Paid-in common stock: 1 million A-shares 100 1.00 100

Paid-in common stock: 4 million B-shares 400 1.00 400

Total long-term capital 1,000 500

a. What proportion of the total long-term capital has been raised by A-shares?

A-shares / Total long-term capital 100 / 1,000 10.00%

b. What proportion of voting rights is represented by A-shares?

A-share total votes / Total Votes 100 / 500 20.00%

c. What proportion of the dividends should the A-shares receive?

A-shares in local currency / Total equity shares in local currency 100 / (100 + 400) 20.00%

Assuming all of the same debt and equity values for Yehti Manufacturing in problem 4.9, with the sole exception that both A-

shares and B-shares have the same voting rights, one vote per share:

Problem 4.10 Yehti Manufacturing (B)

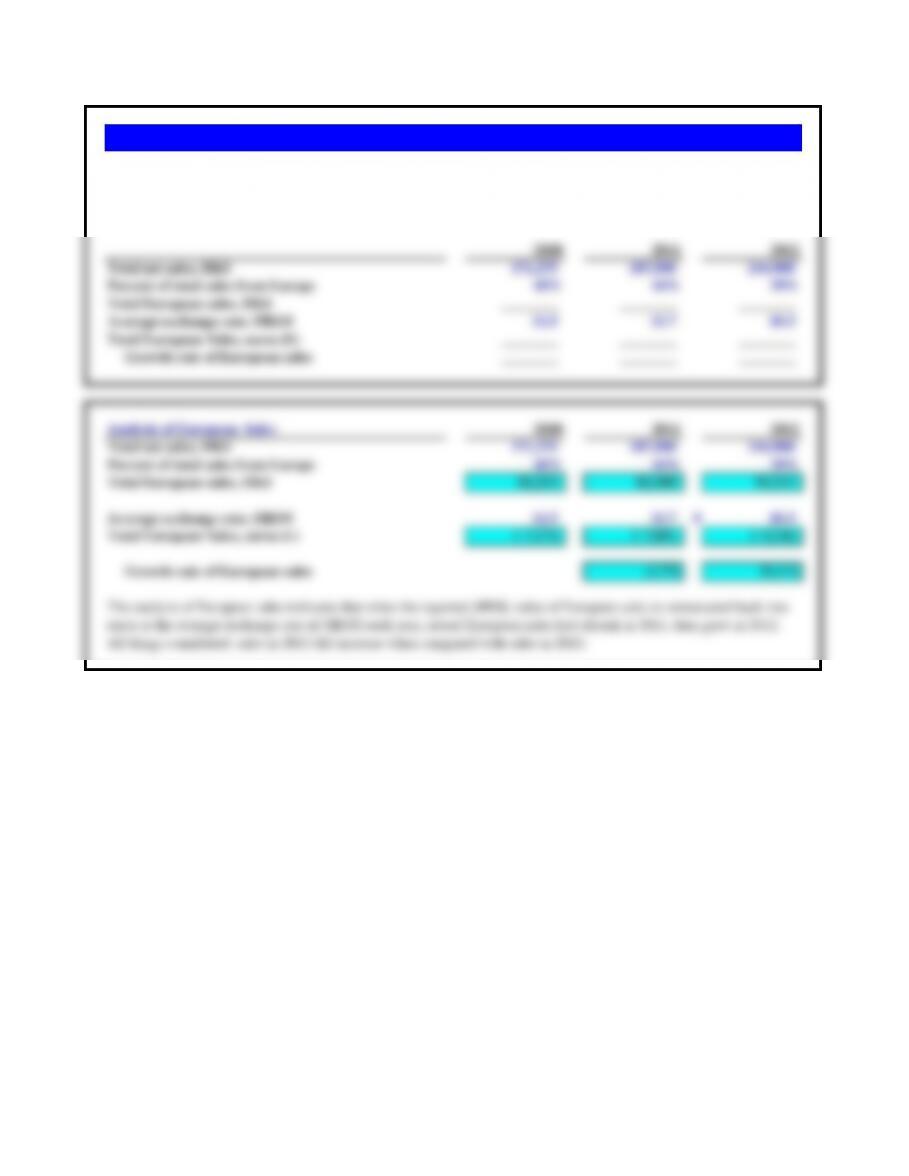

2010 2011 2012

Total net sales, HK$ 171,275 187,500 244,900

Percent of total sales from Europe 48% 44% 39%

Total European sales, HK$ ________ ________ ________

Average exchange rate, HK$/€ 11.5 11.7 10.3

Total European Sales, euros (€) ________ ________ ________

Growth rate of European sales ________ ________ ________

Analysis of European Sales 2010 2011 2012

Total net sales, HK$ 171,275 187,500 244,900

Percent of total sales from Europe 48% 44% 39%

Total European sales, HK$ 82,212 82,500 95,511

Average exchange rate, HK$/€ 11.5 11.7 # 10.3

Total European Sales, euros (€) € 7,174 € 7,051 € 9,246

Growth rate of European sales -1.7% 31.1%

Problem 4.11 Lantau Beer (A): European Sales

Lantau Beer is a Hong Kong-based brewery and files all of its financial statements in Hong Kong dollars (HK$). The

company‘s European sales director, Phillipp Bosse, has been criticized for his performance. He disagrees, arguing that

sales in Europe have grown steadily in recent years. Who is correct?

The analysis of European sales indicates that when the reported (HK$) value of European sales is remeasured back into

euros at the average exchange rate of HK$/E each year, actual European sales first shrunk in 2011, then grew in 2012.

All things considered, sales in 2012 did increase when compared with sales in 2010.

Analysis of Japanese yen-Denominated Debt 2008 2009 2010

Annual yen payments on debt agreement (¥) 12,000,000 12,000,000 12,000,000

Average exchange rate, ¥/HK$ 12.3 12.1 11.4

Annual yen debt service, HK$ 977,199 994,200 1,057,269

Problem 4.12 Lantau Beer (B): Japanese Yen Debt

Lantau Beer of Hong Kong borrowed Japanese yen under a long-term loan agreement several years ago. The company’s

new CFO believes, however, that what was originally thought to have been relatively “cheap debt” is no longer true.

What do you think?

The analysis of debt service payments on the Japanese yen-denominated long-term loan indicates that for the past two

years the effective cost of repaying the loan, in Hong Kong dollars, has been steadily rising as the Hong Kong dollar has

fallen in value against the Japanese yen. In fact, the Japanese yen debt has not proven to be as cheap as thought.

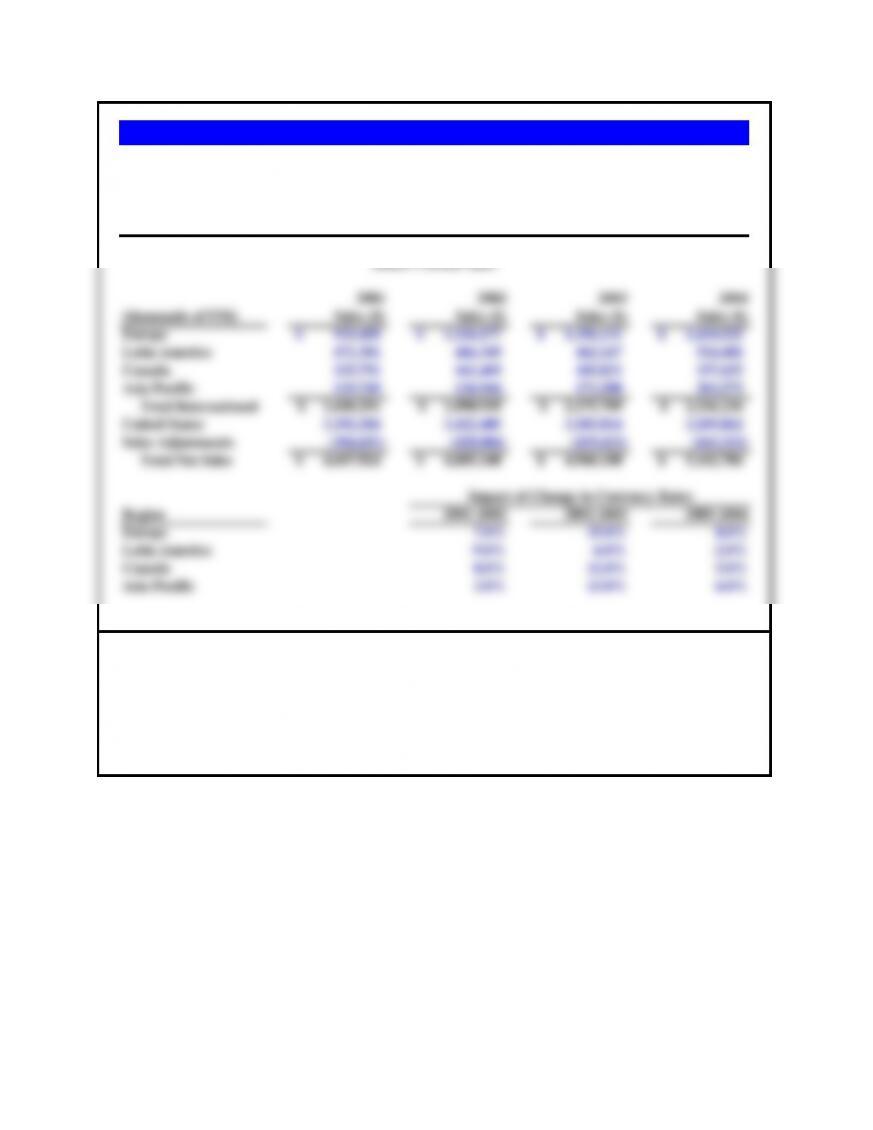

2001 2002 2003 2004

(thousands of US$) Sales ($) Sales ($) Sales ($) Sales ($)

Europe 933,450$ 1,126,177$ 1,356,131$ 1,410,525$

Latin America 471,301 466,349 462,167 524,481

Canada 155,791 161,469 185,831 197,655

Asia Pacific 119,749 136,944 171,580 203,575

Total International 1,680,291$ 1,890,939$ 2,175,709$ 2,336,236$

United States 3,392,284 3,422,405 3,203,814 3,209,862

Sales Adjustments (384,651) (428,004) (419,423) (443,312)

Total Net Sales 4,687,924$ 4,885,340$ 4,960,100$ 5,102,786$

Region 2001-2002 2002-2003 2003-2004

Europe 7.0% 15.0% 8.0%

Latin America -9.0% -6.0% -2.0%

Canada 0.0% 11.0% 5.0%

Asia Pacific 3.0% 13.0% 6.0%

Source: Mattel, Annual Report, 2002, 2003, 2004.

a. What was the percentage change in sales, in US dollars, by region?

b. What was the percentage change in sales by region net of currency change impacts?

c. What impact did currency changes have on the level and growth of consolidated sales between 2001 and 2004?

Mattel’s Global Performance

Mattel (US) achieved significant sales growth in its major international regions between 2001 and 2004. In its

filings with the United States Security and Exchange Commission (SEC), it reported both the amount of

regional sales and the percentage change in those sales occurred resulting from exchange rate changes.

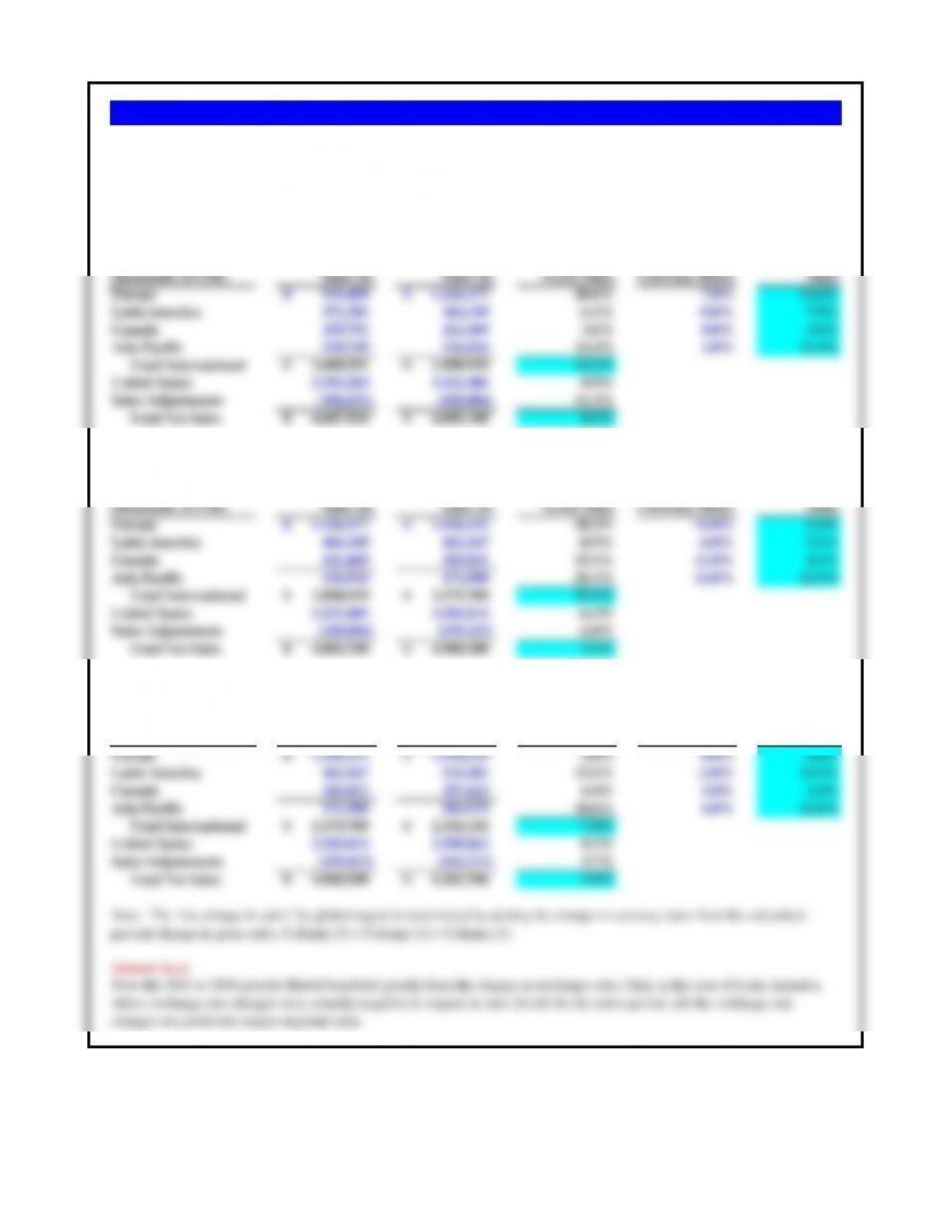

Impact of Change in Currency Rates

Mattel’s Global Sales

Answer to a) Answer to b)

(1) (2) (3)

Percent Impact of Net

2001 2002 Change in Change in Change in

(thousands of US$) Sales ($) Sales ($) Gross Sales Currency Rates Sales

Europe 933,450$ 1,126,177$ 20.6% 7.0% 13.6%

Latin America 471,301 466,349 -1.1% -9.0% 7.9%

Canada 155,791 161,469 3.6% 0.0% 3.6%

Asia Pacific 119,749 136,944 14.4% 3.0% 11.4%

Total International 1,680,291$ 1,890,939$ 12.5%

United States 3,392,284 3,422,405 0.9%

Sales Adjustments (384,651) (428,004) 11.3%

Total Net Sales 4,687,924$ 4,885,340$ 4.2%

(1) (2) (3)

Percent Impact of Net

2002 2003 Change in Change in Change in

(thousands of US$) Sales ($) Sales ($) Gross Sales Currency Rates Sales

Europe 1,126,177$ 1,356,131$ 20.4% 15.0% 5.4%

Latin America 466,349 462,167 -0.9% -6.0% 5.1%

Canada 161,469 185,831 15.1% 11.0% 4.1%

Asia Pacific 136,944 171,580 25.3% 13.0% 12.3%

Total International 1,890,939$ 2,175,709$ 15.1%

United States 3,422,405 3,203,814 -6.4%

Sales Adjustments (428,004) (419,423) -2.0%

Total Net Sales 4,885,340$ 4,960,100$ 1.5%

(1) (2) (3)

Percent Impact of Net

2003 2004 Change in Change in Change in

(thousands of US$) Sales ($) Sales ($) Gross Sales Currency Rates Sales

Europe 1,356,131$ 1,410,525$ 4.0% 8.0% -4.0%

Latin America 462,167 524,481 13.5% -2.0% 15.5%

Canada 185,831 197,655 6.4% 5.0% 1.4%

Asia Pacific 171,580 203,575 18.6% 6.0% 12.6%

Total International 2,175,709$ 2,336,236$ 7.4%

United States 3,203,814 3,209,862 0.2%

Sales Adjustments (419,423) (443,312) 5.7%

Total Net Sales 4,960,100$ 5,102,786$ 2.9%

Answer to c)

Mattel (U.S.) achieved significant sales growth in its major international regions between 2001 and 2004. In its filings with the

United States Security and Exchange Commission (SEC), it reported what percentage change in regional sales occurred as a

result of exchange rate changes.

Note: The “net change in sales” by global region is determined by netting the change in currency rates from the calcualted

percent change in gross sales. Column (3) = Column (1) + Column (2).

Over the 2001 to 2004 period, Mattel benefited greatly from the change in exchange rates. Only in the case of Latin America,

where exchange rate changes were actually negative in impact on sales levels for the entire period, did the exchange rate

changes not positively impact regional sales.

Problem 4.13 Mattel’s Global Sales Performance

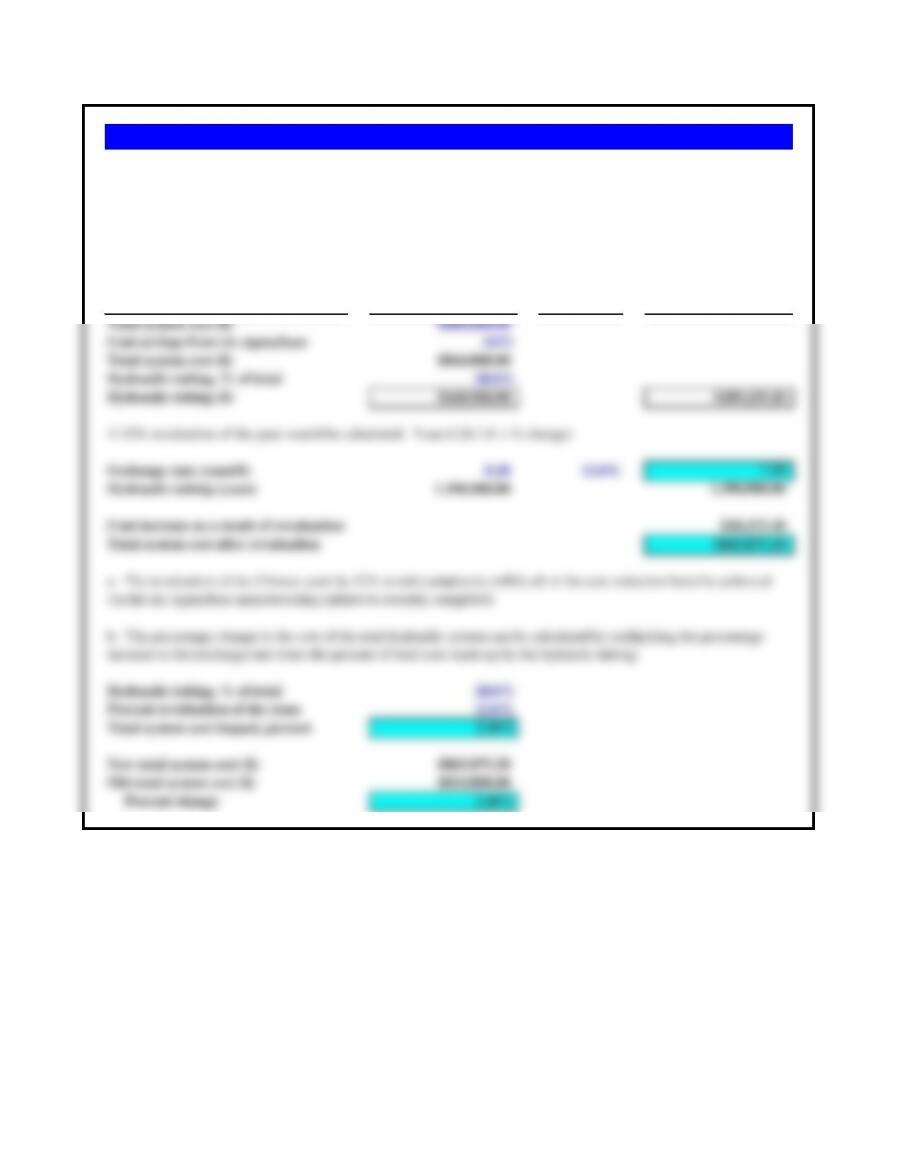

Assumptions Original/Current Revaluation? Future?

Total system cost ($) $880,000.00

Cost savings from six sigma/lean 4.0%

Total system cost ($) $844,800.00

Hydraulic tubing, % of total 20.0%

Hydraulic tubing ($) $168,960.00 $189,235.20

A 12% revaluation of the yuan would be calculated: Yuan 8.28 / (1 + % change)

Exchange rate (yuan/$) 8.28 12.0% 7.39

Hydraulic tubing (yuan) 1,398,988.80 1,398,988.80

Cost increase as a result of revaluation $20,275.20

Total system cost after revaluation $865,075.20

Hydraulic tubing, % of total 20.0%

Percent revaluation of the yuan 12.0%

Total system cost impact, percent 2.40%

New total system cost ($) $865,075.20

Old total system cost ($) $844,800.00

Percent change 2.40%

Harrison Equipment of Denver, Colorado purchases all of its hydraulic tubing from manufacturers in mainland China.

The company has recently completed a corporate-wide initiative in six sigma/lean manufacturing. Completed oil field

hydraulic system costs were reduced 4% over a one-year period, from $880,000 to $844,800. The company is now

worried that all of the hydraulic tubing that goes into the systems (making up 20% of their total costs) will be hit by

the potential revaluation of the Chinese yuan — if some in Washington get their way. How would a 12% revaluation of

the yuan against the dollar impact total system costs?

a. The revaluation of the Chinese yuan by 12% would completely nullify all of the cost reduction benefits achieved

via the six sigma/lean manufacturing initiatives recently completed.

b. The percentage change in the cost of the total hydraulic system can be calculated by multiplying the percentage

increase in the exchange rate times the percent of total cost made up by the hydraulic tubing:

Problem 4.14 Chinese Sourcing and the Yuan

a. Which period shown had the highest total returns? The lowest?

b. Which decade had the highest dividend returns? When were dividends clearly not a priority for publicly traded companies?

c. The 1990s was a boom period for U.S. equity returns. How did firm’s react in terms of their dividend distributions?

d. How has the 2000s period fared? How do you think publicly traded companies have started changing their dividend distribution habits as a result?

S&P 500 Equity Returns, 1926-2014 (average annual return, percent)

1926 to

Period 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s 2014

Capital appreciation -5.3% 3.0% 13.6% 4.4% 1.6% 12.6% 15.3% -2.7% 5.9%

Dividend yield 5.4% 6.0% 5.1% 3.3% 4.2% 4.4% 2.5% 1.8% 4.0%

Total return 0.1% 9.0% 18.7% 7.7% 5.8% 17.0% 17.8% -0.9% 9.9%

a. Which period shown had the highest total returns? The lowest?

The 1950s — somewhat surprisingly — had the highest total returns. The lowest were the 2000s.

b. Which decade had the highest dividend returns? When were dividends clearly not a priority for publicly traded companies?

Dividend returns were the highest in the 1940s. Since 2000 dividend yields have clearly been a lower priority.

c. The 1990s was a boom period for U.S. equity returns. How did firm‘s react in terms of their dividend distributions?

Dividend distributions/yields were clearly down during this era.

d. How has the 2000s period fared? How do you think publicly traded companies have started changing their dividend distribution habits as a result?

A negative return for 2000s shows pretty awful performance! Companies are increasing dividends –– now — finally — as a result.

S&P 500 Equity Returns, 1926-2014 (average annual return, percent)

1926 to

Period 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s 2014

Capital appreciation -5.3% 3.0% 13.6% 4.4% 1.6% 12.6% 15.3% -2.7% 5.9%

Dividend yield 5.4% 6.0% 5.1% 3.3% 4.2% 4.4% 2.5% 1.8% 4.0%

Total return 0.1% 9.0% 18.7% 7.7% 5.8% 17.0% 17.8% -0.9% 9.9%

Source: Data drawn from “JP Morgan Guide to the Markets, 2015,” JP Morgan Asset Management.

Problem 4.15 S&P Equity Returns History

The U.S. equity markets have delivered very different returns over the past 90 years. Use the following data arranged by decade to answer the following questions

about these U.S. equity investment returns.