7

S U P P L E M E N T

Capacity and Constraint Management

DISCUSSION QUESTIONS

1. Design capacity is the theoretical maximum output of a

system in a given period under ideal conditions. Effective capacity

2. Effective capacity is the capacity a firm can expect to achieve

zation

4. Effective capacity takes into account planned resource

unavailability (e.g., scheduled breaks). Actual output starts with

5. Doubling capacity of a bottleneck only moves the bottleneck

somewhere else; every system has at least one bottleneck. There

LO S7.3: Perform bottleneck analysis

7. Theory of constraints is the body of knowledge that deals

8. The fundamental assumptions of break-even analysis are:

LO S7.4: Compute break-even

AACSB: Reflective thinking

9. Revenue data, when plotted, do not fall on a straight line

Leading is preferred when a firm cannot afford to lose customers

11. NPV determines the discounted or time value of money,

comparing cost and income streams over periods of time. Process

AACSB: Reflective thinking

expanding capability.

5. When one set of constraints is overcome, go back to Step 1 and

13. Techniques for dealing with bottlenecks include offloading

tracting may expand the volume of units processed but not speed

SUPPLEMENT 7 CA P A CI T Y A N D CO N S TR A I N T MANA G E M E N T 111

ACTIVE MODEL EXERCISES

1. Due to an anticipated decrease in demand the firm is considering

work on weekdays. What will be the capacity if they select this

S7.6 Design: 93,600 0.95 = 88,920

S7.7 Where:

Actual output = 1,450 students

112 SUPPLEMENT 7 CA P A C I T Y A N D CO N S T R A I N T MA N A G E M E N T

(c) Weekly capacity = (60 min/hr)(8 hr/day)(6 days/wk) /

S7.14 (a) Workstation C is the bottleneck, at 20 min/unit

(Two different Part 1’s can be worked on by Workstation A and

S7.15 (a) Converting each capacity to a process time,

Sawing = Sanding = 60 min/hr ÷ 6 units/hr = 10 min/unit;

(c) Throughput time (time for a unit to go through the system) =

Maximum of (10 + 10 + 30 + 85.71, or 25 + 30 + 85.71) = Maxi-

S7.16 Break-even:

500 2,000 units

F

S7.17 (a) Proposal A break-even in units is:

===

Fixed cost $70,000 $70,000 7,000 units

– 20 – 10 10PV

S7.18 (a) Proposal A break-even in dollars is:

12

20

0.40

1–1–

V

P

0.50

S7.19 Set Proposal A = Proposal B

(8) – 50,000 (10) – 70,000

(8) 20,000 (10)

20,000 10 – 8

XX

XX

XX

=

+=

=

SUPPLEMENT 7 CA P A CI T Y A N D CO N S TR A I N T MANA G E M E N T 113

Break-even is given by:

S7.23 Option A: Stay as is

Option B: Add new equipment

( )

( )

( )

Units Price – – = Profit

Profit = 30,000 1.00 – 0.50 – 14,000

= $1,000

Profit = 50,000 1.00 – 0.60 – 20,000

= $0

A

B

VF

S7.24 Option A: Stay as is

Option B: Add new equipment, raise selling price

( )

( )

( )

Units Price – – = Profit

Profit = 30,000 1.00 – 0.50 – 14,000

= $1,000

Profit = 45,000 1.10 – 0.60 – 20,000

= $2,500

A

B

VF

S7.25 Where:

– 2.50 – 1.75

PV

(b) Revenue at the break-even quantity for the manual

process:

=

=

==

$

50,000 2.50 $125,000 and

37,500

1–

37,500 $125,000

1.75

1– 2.50

BEP V

P

(c) Break-even quantity for the mechanized process:

where: F = 75,000 P = 2.50 V = 1.25

==

−

75,000 60,000 bags

2.50 1.25

X

BEP

(d) Revenue at the break-even quantity for the mechanized

process:

(e) Monthly profit or loss of the manual process if they

(g) They should be indifferent to the process selected at

75,000 bags.

− = −

=

.75 37,500 1.25 75,000

75,000

XX

X

(h) The manual process should be preferred over the mech-

anized process below 75,000 bags. The mechanized

process should be preferred over the manual process

S7.26 (a) Break-even volume:

= $3,800

Selling

Price

Volume

Revenue

Percent of

Total Revenue

Drinks

1.50

30,000

45,000

0.153

Meals

10.00

10,000

100,000

0.339

Desserts, etc.

2.50

10,000

25,000

0.085

Sandwiches

6.25

20,000

125,000

0.423

295,000

1.000

P

V

V/P

1–V/P

Wi

1–(V/P)Wi

Drinks

1.50

0.75

0.50

0.50

0.153

0.077

Meals

10.00

5.00

0.50

0.50

0.339

0.170

Desserts

2.50

1.00

0.40

0.60

0.085

0.051

Lunch

6.25

3.25

0.52

0.48

0.423

0.203

1.000

0.501

$

3,800 $7,584.83

0.501

1ii

i

F

BEP

VW

P

= = =

−

$

60,000 × 2.50 = $150,000

75,000

or = $150,000

1.25

1– 2.50

BEP =

114 SUPPLEMENT 7 CA P A C I T Y A N D CO N S T R A I N T MA N A G E M E N T

(b) Number of meals per day at break even = 9

Selling

Price

Fraction

of Total

Revenue

Dollar

Volume

BE Units

per

Month

BE Units

per

Day

Drinks

1.50

0.153

1,160.48

774→

26

Meals

10.00

0.339

2,571.26

258→

9

Desserts, etc.

2.50

0.085

644.71

258→

8

Sandwiches

6.25

0.424

3,208.28

514→

18

S7.27 (a) Break-even volume, where total fixed cost = labor

(at $250) + booth rental (at 5 $50) = $500.

986.19 × 0.25

= = 140.9 servings

$1.75

20 12 8SP VC = = =

−−

(b) Proposal B break even in units is:

Fixed cost 70,000 70,000 7,000 units

20 10 10SP VC = = =

−−

S7.29* (a) Proposal A break even in dollars is:

Fixed cost 50,000 50,000 $125,000

S7.31* (a) Proposal A: Profit at 8,500 units

Profit = ( ) SP VC X F−−

@ 8,500 for Proposal A:

(20 12)8,500 50,000 = 18,000

@ 8,500 for Proposal B:

(20 10)8,500 70,000 = 15,000

−−

−−

Proposal A is best.

S7.31* (b) Proposal B: Profit at 15,000 units

@ 15,000 units for Proposal A:

(20 12)15,000 50,000 = $70,000

(20 10)15,000 70,000 = $80,000

−−

−−

Proposal B is best.

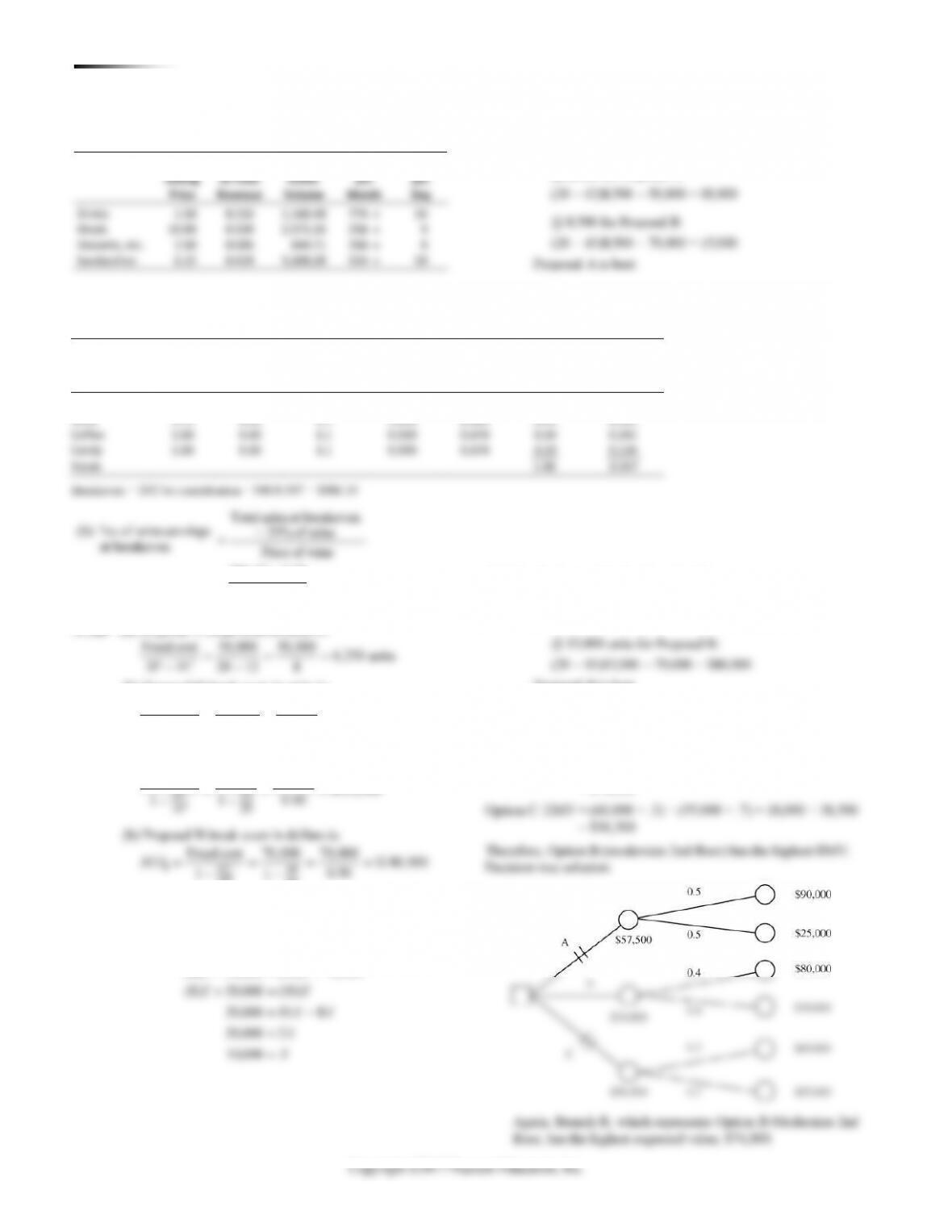

S7.32

Option A: EMV = (90,000 × .5) + (25,000 × .5) = 45,000 + 12,500

= $57,500

Option B: EMV = (80,000 × .4) + (70,000 × .6) = 32,000 + 42,000

Item

(P)

Selling

Price

(V)

Variable

Cost

Var. Cost

Factor (%)

Total

Var. Cost

1– (V/P)

Estimated

Percent

Revenue

Contribution

Weighted

Revenue

Soft drinks

1.00

0.65

1.1

0.715

0.285

0.25

0.071

Wine

1.75

0.95

1.1

1.045

0.403

0.25

0.101

Coffee

1.00

0.30

1.1

0.330

0.670

0.30

0.201

Candy

1.00

0.30

1.1

0.330

0.670

0.20

0.134

Totals

1.00

0.507

Breakeven = TFC/wt contribution = 500/0.507 = $986.19

SUPPLEMENT 7 CA P A CI T Y A N D CO N S TR A I N T MANA G E M E N T 115

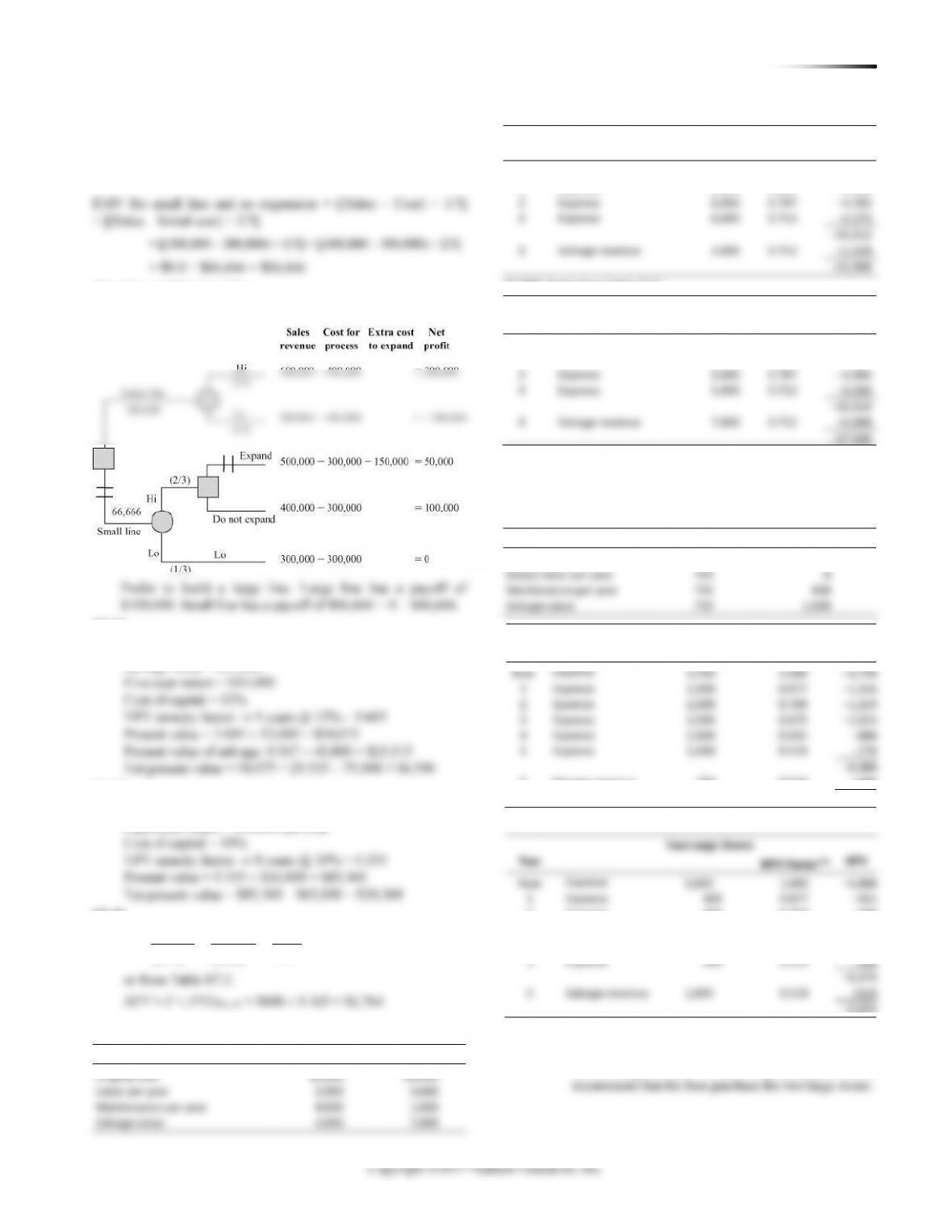

S7.33

EMV for large line = [(Sales – Cost) × 2/3] + [(Sales – Cost) × 1/3]

= (200,000 × 2/3) + (–100,000 × 1/3) = $100,000

2

Expense

6,000

0.797

–4,782

3

Expense

6,000

0.712

–4,272

–24,412

3

Salvage revenue

2,000

0.712

+1,424

Therefore, build a large line.

Decision tree solution:

Excess labor per year

Maintenance per year

S7.34

Initial investment = $75,000

Now

1.000

1

Expense

0.877

2

Expense

0.769

3

Expense

0.675

4

Expense

0.592

5

Expense

0.519

S7.35

Initial investment = $65,000

Two Large Ovens

NPV

Now

5,000

Expense

Expense

Expense

Expense

Expense

Salvage revenue

1,000

+519

Year

Machine A

NPV Factor**

NPV

Now

Expense

10,000

1.000

–10,000

1

Expense

6,000

0.893

–5,358

** NPV factor from Table S7.2.

Year

Machine B

NPV Factor**

NPV

Now

Expense

20,000

1.000

–20,000

1

Expense

5,000

0.893

–4,465

2

Expense

5,000

0.797

–3,985

3

Expense

5,000

0.712

–3,560

–32,010

3

Salvage revenue

7,000

0.712

+4,984

–27,026

** NPV factor from Table S7.2.

NPV for Machine A is –$22,988; NPV for Machine B is –$27,026.

Therefore, Machine A should be recommended.

S7.38

Expense

Three Small Ovens

Two Large Ovens

Original cost

3,750

5,000

Year

Three Small Ovens

NPV Factor**

NPV

5

Salvage revenue

750

0.519

+389

–8,511

** NPV factor from Table S7.2.