6

S U P P L E M E N T

Statistical Process Control

DISCUSSION QUESTIONS

1. Shewhart’s two types of variation, common and special

causes, are also called natural and assignable variation.

LO S6.1: Explain the purpose of a control chart

LO S6.1: Explain the purpose of a control chart

AACSB: Application of knowledge

5. The 5 steps are:

1. Collect 20 to 25 samples, often of n = 4 or 5 each;

compute the mean and range of each sample.

2. Compute the overall means (

x

and

R

), set appropriate

control limits using the new data.

LO S6.4: List the five steps involved in building control charts

6. Text list includes machine wear, misadjusted equipment,

LO S6.1: Explain the purpose of a control chart

AACSB: Application of knowledge

7. Two sigma covers only 95.5% of all natural variation; even in

the absence of assignable cause, points will fall outside the control

size. The control charts presented here should not be used if the

sample size varies.

LO S6.1: Explain the purpose of a control chart

11. Cpk, the process capability index, is one way to express

process capability. It measures the proportion of natural variation

(3) between the center of the process and the nearest specifica-

tion limit.

AACSB: Application of knowledge

14. A run test is used to help spot abnormalities in a control

chart process. It is used if points are not individually out of con-

88 SUPPLEMENT 6 ST AT I ST I CA L PR OC ES S CO N TR O L

15. Managerial issues include:

◼ Selecting places in a process that need SPC

◼ Deciding which type of control charts best fit

◼ Setting rules for workers to follow if certain points or pat-

terns emerge

LO S6.3: Build x-bar charts and R-charts

estimate the quality of a lot.

LO S6.7: Explain acceptance sampling

18. The two risks when acceptance sampling is used are type I

error: rejecting a good lot; type II error: accepting a bad lot.

LO S6.7: Explain acceptance sampling

19. A process that has a capability index of one or greater—a

“capable” process—produces small percentages of unacceptable

items. The capability formula is built around an assumption of

2. If we use a two-sigma control chart, what are the UCL and

LCL? Is the process more out of control?

The control limits are tighter. UCL = 16.667 and LCL =

15.333. Now five points are out of control.

3. What happens if the Z-value increases?

Now the control limits are wider at Z = 4, only one point is

out of control.

3. Suppose that the sample size used was actually 120 instead of

the 100 that it was supposed to be. How does this affect the chart?

The overall percentage of defects drops and, in addition,

the UCL and LCL get closer to the center line and each other.

4. What happens to the chart as we reduce the Z-value?

The chart gets “tighter.” The UCL and LCL get closer to

the center line and each other.

2. Increase the standard deviation. At what value will the curve

cross the upper specification?

About .9

END–OF-SUPPLEMENT PROBLEMS (PROBLEMS WITH ASTER-

ISKS APPEAR IN MYOMLAB ONLY)

S6.1

0.1 0.1 0.0167

6

36

xn

= = = =

( )

( )

= + = + =

= = =

1.72

UCL 50 2 50 2 .77 51.54

5

1.72

LCL 50 50 .77 48.46

5

x

x

– 2 – 2

The control limits are tighter, but the confidence level has dropped.

S6.3 The relevant constants are:

2 4 3

= 0.419 = 1.924 = 0.076A D D

25

SUPPLEMENT 6 ST AT ISTIC AL PROC ES S CO N T R O L 89

( )

( )

(b) LCL 3 420 3 5 405

UCL 3 420 3 5 435

X

X

xn

xn

= − = − =

= + = + =

S6.5 From Table S6.1, A2 = 0.308, D4 = 1.777, D3 = 0.223

= +

2

UCL

xx A R

2

LCL

xx A R= −

S6.6

2

2

4

3

UCL 2.982 0.729 1.024 3.728

LCL 2.982 0.729 1.024 2.236

UCL 2.282 1.024 2.336

LCL 0 1.024 0

X

X

R

R

X A R

X A R

DR

DR

= + = + =

= − = − =

= = =

= = =

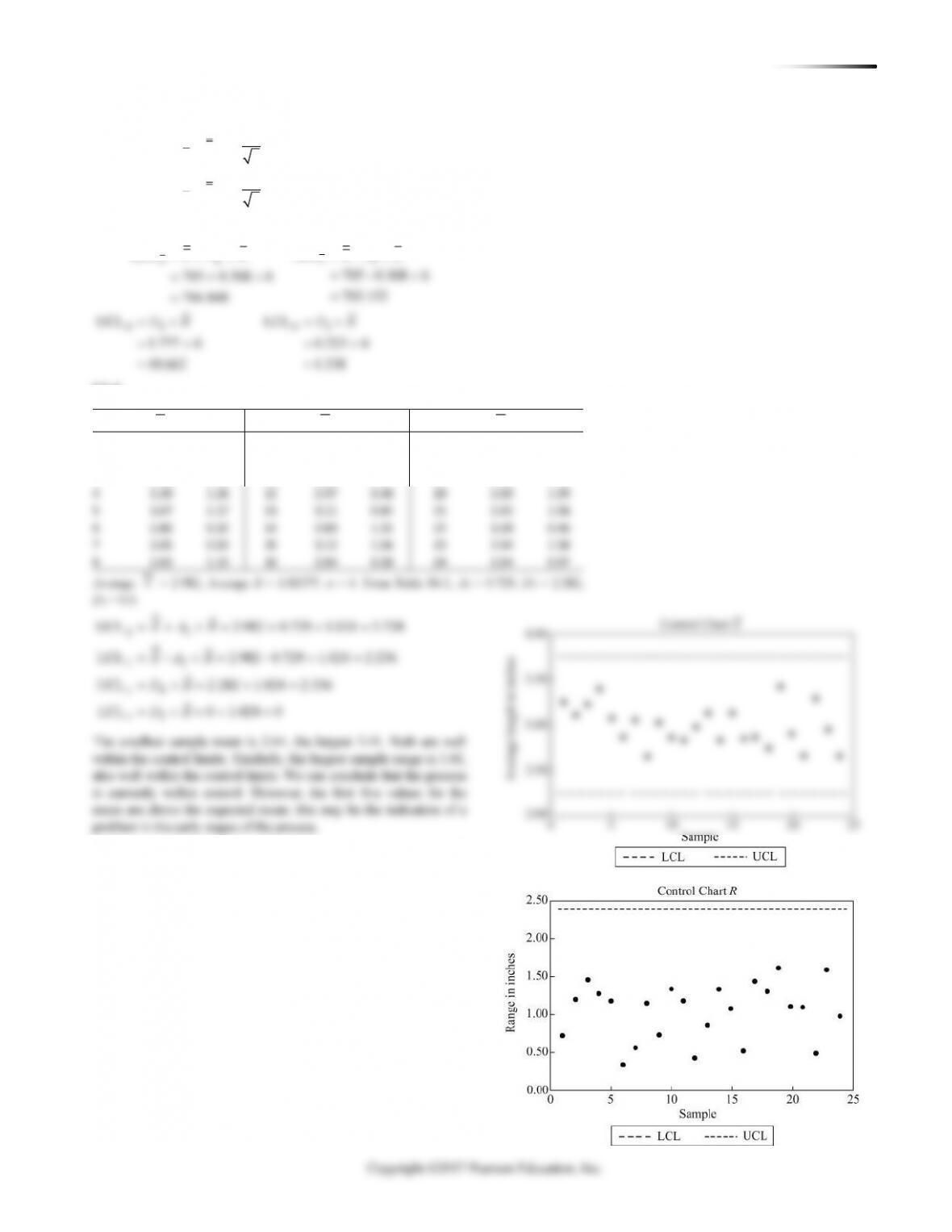

The smallest sample mean is 2.64, the largest 3.41. Both are well

within the control limits. Similarly, the largest sample range is 1.61,

also well within the control limits. We can conclude that the process

is currently within control. However, the first five values for the

mean are above the expected mean; this may be the indication of a

problem in the early stages of the process.

4

3.39

1.26

12

2.97

0.40

20

2.89

1.09

5

3.07

1.17

13

3.11

0.85

21

2.65

1.08

6

2.86

0.32

14

2.83

1.31

22

3.28

0.46

7

3.05

0.53

15

3.12

1.06

23

2.94

1.58

8

2.65

1.13

16

0.50

24

2.64

0.97

Hour

X

R

Hour

X

R

Hour

X

R

1

3.25

0.71

9

3.02

0.71

17

2.86

1.43

2

3.10

1.18

10

2.85

1.33

18

2.74

1.29

3

3.22

1.43

11

2.83

1.17

19

3.41

1.61

90 SUPPLEMENT 6 ST AT I ST I CA L PR OC ES S CO N TR O L

S6.7

Sample 1

6.025

0.4

(d) -chart:R

R4

R3

4.48 mm

UCL 1.777(4.48) 7.96 mm

LCL .223(4.48) 1.00 mm

R

DR

DR

=

= = =

= = =

(e) If the desired nominal line is 155 mm, then:

UCL 155 (.308 4.48) 155 1.38 156.38

LCL 155 (.308 4.48) 155 1.38 153.62

X

X

= + = + =

= − = − =

S6.8 (a)

(b) With z = 3,

0.12

U CL 16 3 16 .12 16.12

3

0.12

LCL 16 3 16 .12 15.88

3

X

X

= + = + =

= − = − =

UCL 1.141

LCL 0

R

R

=

=

S6.10

10, 3.3XR==

(a) Process (population) standard deviation () = 1.36,

(b) Using

x

( )

x

= + =

UCL 10 3 0.61 11.83

(d) Yes, both mean and range charts indicate process is

in control.

S6.11

= = =

==

==

==

2 4 3

(a) .577, 2.115, 0

10.0005 0.0115

UCL 10.0071 LCL 9.9939

UCL 0.0243 LCL 0

xx

RR

A D D

XR

Sample 2

6.05

0.4

Sample 3

5.475

1.5

Sample 4

6.075

0.3

Sample 5

6.625

0.4

156.9 153.2 153.6 155.5 156.6

(a) 155.16 mm

5

4.2 4.6 4.1 5.0 4.5

(b) 4.48 mm

5

X

R

+ + + +

==

+ + + +

==

Standard deviation of the sampling means

1.36 5

0.61

x

=

=

=

=

=

UCL and LCL

384

xZ xx

n

x

SUPPLEMENT 6 ST AT ISTIC AL PROC ES S CO N T R O L 91

(b)

Original Data

Are Both the Mean

Sample

and Range

Sample

Mean (in.)

Range (in.)

in Control?

1

10.002

0.011

Y

2

10.002

0.014

Y

3

9.991

0.007

N

4

10.006

0.022

Y

5

9.997

0.013

Y

6

9.999

0.012

Y

7

10.001

0.008

Y

8

10.005

0.013

Y

9

9.995

0.004

Y

10

10.001

0.011

Y

11

10.001

0.014

Y

12

10.006

0.009

Y

Revised Control Limits

Are both the Mean

Sample

and Range

Sample

Mean (in.)

Range (in.)

in Control?

1

10.002

0.011

Y

2

10.002

0.014

Y

3

4

10.006

0.022

Y

5

9.997

0.013

Y

6

9.999

0.012

Y

7

10.001

0.008

Y

8

10.005

0.013

Y

9

9.995

0.004

Y

10

10.001

0.011

Y

11

10.001

0.014

Y

12

10.006

0.009

Y

These limits reflect a process that is now in control.

S6.12

R= 3.25

mph, Z = 3,with n = 8, from Table S6.1, D4 =

1.864, D3 = .136

4

UCL = D R = (1.864)(3.25) = 6.058

LCL = D R = (.136) (3.25) = 0.442

R

92 SUPPLEMENT 6 ST AT I ST I CA L PR OC ES S CO N TR O L

(e) When the sample size increases,

( )

1

ˆ

p

pp

n

−

=

is smaller.

UCL 0.057 3(0.023) 0.057 0.069 0.126

LCL 0.057 3(0.023) 0.057 0.069 0.012 0

= + = + =

= − = − = − =

p

p

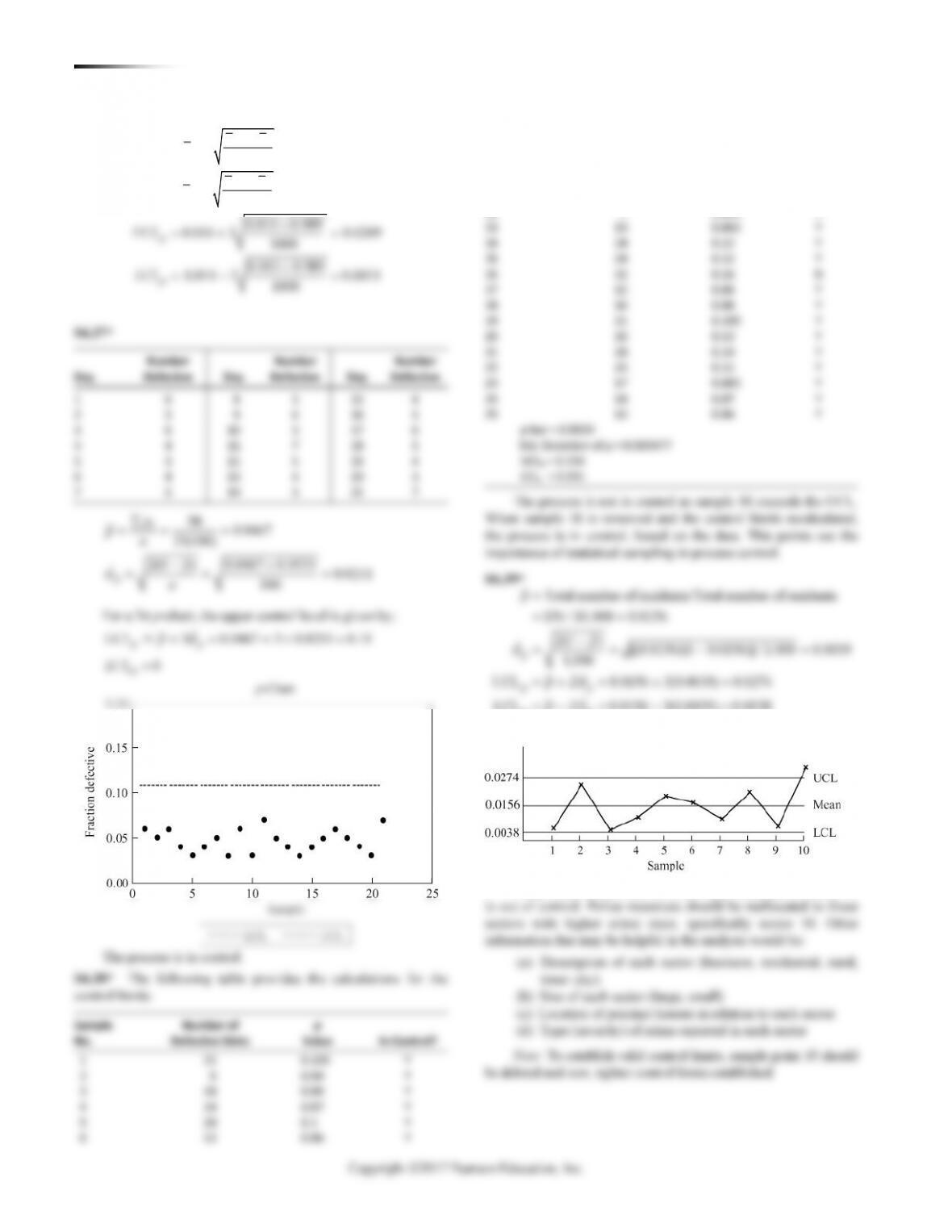

(b) The process is out of control on the third day (of the

next 3 days). For example, .13 exceeds the upper

control limit of 0.126.

()

()

1

UCL 3

1

LCL 3

0.015 0.985

UCL 0.015 3 0.0313

500

0.015 0.985

LCL 0.015 3 0.0013, or zero

p

p

p

pp

pn

pp

pn

S6.16 −

=+

−

=−

= + =

= − = −

(b) The LCL cannot be negative because the percent defective can

never be less than zero.

(c) The industry standards are not as strict as those at Birmingham

S6.20 (a) n = 200,

p

= 50/10(200) = 0.025

(1 )

UCL 3

(1 )

LCL 3

0.025 0.975

UCL 0.025 3 0.0581

200

0.025 0.975

LCL 0.025 3 0.0081, or zero

200

p

p

p

p

pp

pn

pp

pn

−

=+

−

=−

= + =

= − = −

SUPPLEMENT 6 ST AT ISTIC AL PROC ES S CO N T R O L 93

(b) Use mean of 6 weeks of observations

36 =6

6

for

,c

as true

c

is unknown.

(c) It is in control because all weeks’ calls fall within

interval of [0, 13].

(d) Instead of using we now use

LCL = 4 – 3(2) = –2, or 0

Week 4 (11 calls) exceeds UCL. Not in control.

S6.23

213/5 42.6 test errors per school

UCL 3 42.6 3 42.6 42.6 19.5806 62.1806

LCL 3 42.6 – 3 42.6 42.6 19.5806 23.0194

c

c

c

cc

cc

==

= + = + = + =

= − = = − =

The chart indicates that there are no schools out of control. It

also shows that 3 of 5 schools fall close to or below the process

average, which is a good indication that the new math program has

been taught as effectively at one school in the county as another.

Whether or not the new math program is effective would require

comparisons of this year’s test results with results from previous

years (under the old program) or comparisons with national

per-formance data.

S6.24

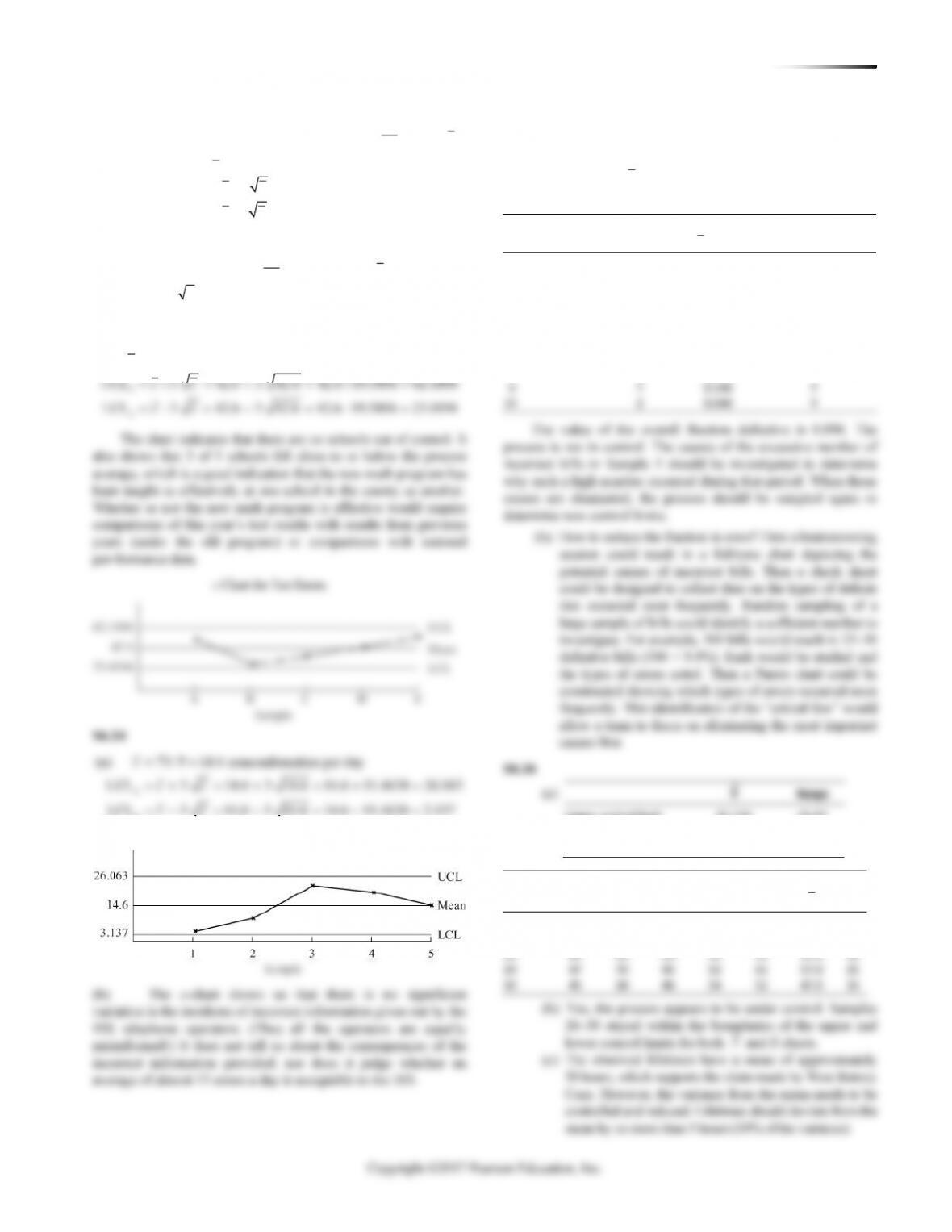

(a) 73/ 5 14.6 nonconformities per day

UCL 3 14.6 3 14.6 14.6 11.4630 26.063

LCL 3 14.6 3 14.6 14.6 11.4630 3.137

c

c

c

cc

cc

==

= + = + = + =

= − = − = − =

(b) The c-chart shows us that there is no significant

variation in the incidents of incorrect information given out by the

IRS telephone operators. (Thus all the operators are equally

misinformed!) It does not tell us about the consequences of the

incorrect information provided, nor does it judge whether an

average of almost 15 errors a day is acceptable to the IRS.

S6.25

(a)

ˆ

0.094, 0.041

UCL 0.218 LCL 0

==

==

p

pp

p

No. of

Is the Billing

Sample No.

Incorrect Bills

p

Value

Process in Control?

1

6

0.120

Y

2

5

0.100

Y

3

11

0.220

N

4

4

0.080

Y

5

0

0.000

Y

6

5

0.100

Y

7

3

0.060

Y

8

4

0.080

Y

9

7

0.140

Y

10

2

0.040

Y

The value of the overall fraction defective is 0.094. The

process is not in control. The causes of the excessive number of

incorrect bills in Sample 3 should be investigated to determine

why such a high number occurred during that period. When those

causes are eliminated, the process should be sampled again to

determine new control limits.

(b) How to reduce the fraction in error? First a brainstorming

session could result in a fishbone chart depicting the

potential causes of incorrect bills. Then a check sheet

could be designed to collect data on the types of defects

that occurred most frequently. Random sampling of a

large sample of bills could identify a sufficient number to

investigate. For example, 300 bills would result in 25–30

defective bills (300 × 9.4%). Each would be studied and

the types of errors noted. Then a Pareto chart could be

constructed showing which types of errors occurred most

frequently. This identification of the “critical few” would

allow a team to focus on eliminating the most important

causes first.

S6.26

(a)

X

Range

Upper control limit

61.131

41.62

Center line (avg)

49.776

19.68

Lower control limit

38.421

0.00

Recent Data Sample

Hour

1

2

3

4

5

X

R

26

48

52

39

57

61

51.4

22

27

45

53

48

46

66

51.6

21

28

63

49

50

45

53

52.0

18

29

47

70

45

52

61

57.0

25

30

45

38

46

54

52

47.0

16

(b) Yes, the process appears to be under control. Samples

26–30 stayed within the boundaries of the upper and

lower control limits for both

X

and R charts.

(c) The observed lifetimes have a mean of approximately

50 hours, which supports the claim made by West Battery

Corp. However, the variance from the mean needs to be

controlled and reduced. Lifetimes should deviate from the

mean by no more than 5 hours (10% of the variance).

= + = + =

= − = − = −

UCL 6 3(2.45) 13.35

LCL 6 3(2.45) 1.35, or 0

c

c

c z c

c z c

36 6,

6=

3 4 = 4 + 3(2) = 10.

4. UCL 4c= = +

c-Chart for Test Errors

c-Chart for Number of Nonconformities

94 SUPPLEMENT 6 ST AT I ST I CA L PR OC ES S CO N TR O L

Sample

Late Flights

Percentage of

Late Flights

Percentage

(n/100)

in Sample

Late Flights (n/100)*

Sample

in Sample

of Late Flights

1

2

0.02

16

2

0.02

2

4

0.04

17

3

0.03

3

10

0.10

18

7

0.07

4

4

0.04

19

3

0.03

5

1

0.01

20

2

0.02

6

21

3

0.03

7

22

7

0.07

8

9

23

4

0.04

9

11

24

3

0.03

0

0.00

25

2

0.02

3

0.03

26

2

0.02

27

0

0.00

2

0.02

28

1

0.01

2

0.02

29

3

0.03

S6.27

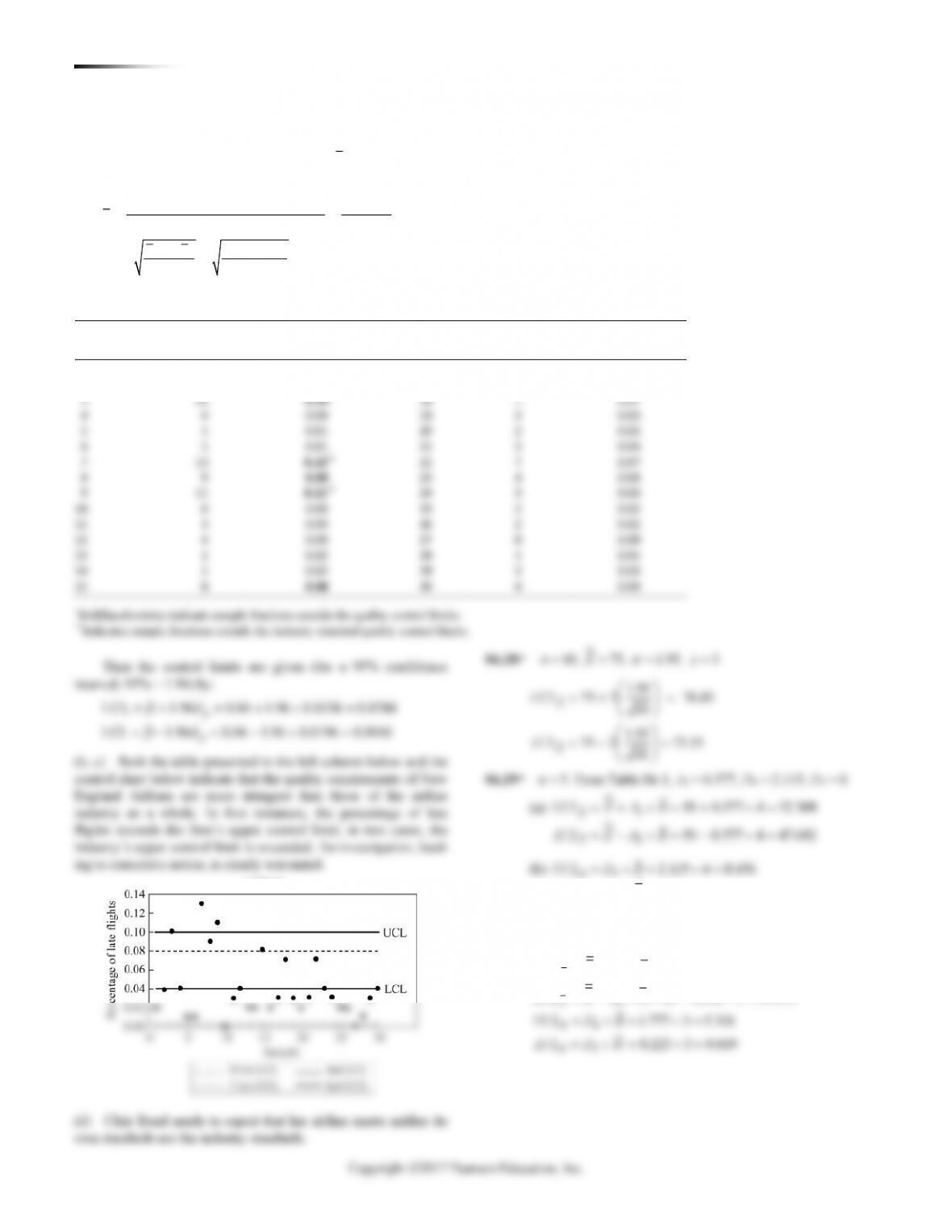

(a) The overall percentage of late flights

()p

and the control

limits are developed as follows:

Total number of late flights 120 0.04

Number of samples Sample size 30 100

(1 ) 0.04 0.96

ˆ0.0196

100

= = =

−

= = =

p

p

pp

n

Table for Problem S6.27

SUPPLEMENT 6 ST AT ISTIC AL PROC ES S CO N T R O L 95

S6.31*

Sample

X

R

Sample

X

R

Sample

X

R

1

63.5

2.0

10

63.5

1.3

19

63.8

1.3

2

63.6

1.0

11

63.3

1.8

20

63.5

1.6

3

63.7

1.7

12

63.2

1.0

21

63.9

1.0

4

63.9

0.9

13

63.6

1.8

22

63.2

1.8

5

63.4

1.2

14

63.3

1.5

23

63.3

1.7

6

63.0

1.6

15

63.4

1.7

24

64.0

2.0

7

63.2

1.8

16

63.4

1.4

25

63.4

1.5

8

63.3

1.3

17

63.5

1.1

9

63.7

1.6

18

63.6

1.8

= = =

= = =

2 4 3

63.49, 1.5, 4. From Table S6.1,

0.729, 2.282, 0.0.

X R n

A D D

2

2

4

3

63.49 0.729 1.5 64.58

63.49 0.729 1.5 62.40

2.282 1.5 3.423

0 1.5 0

X

X

R

R

UCL X A R

LCL X A R

UCL D R

LCR D R

= + = + =

= − = − =

= = =

= = =

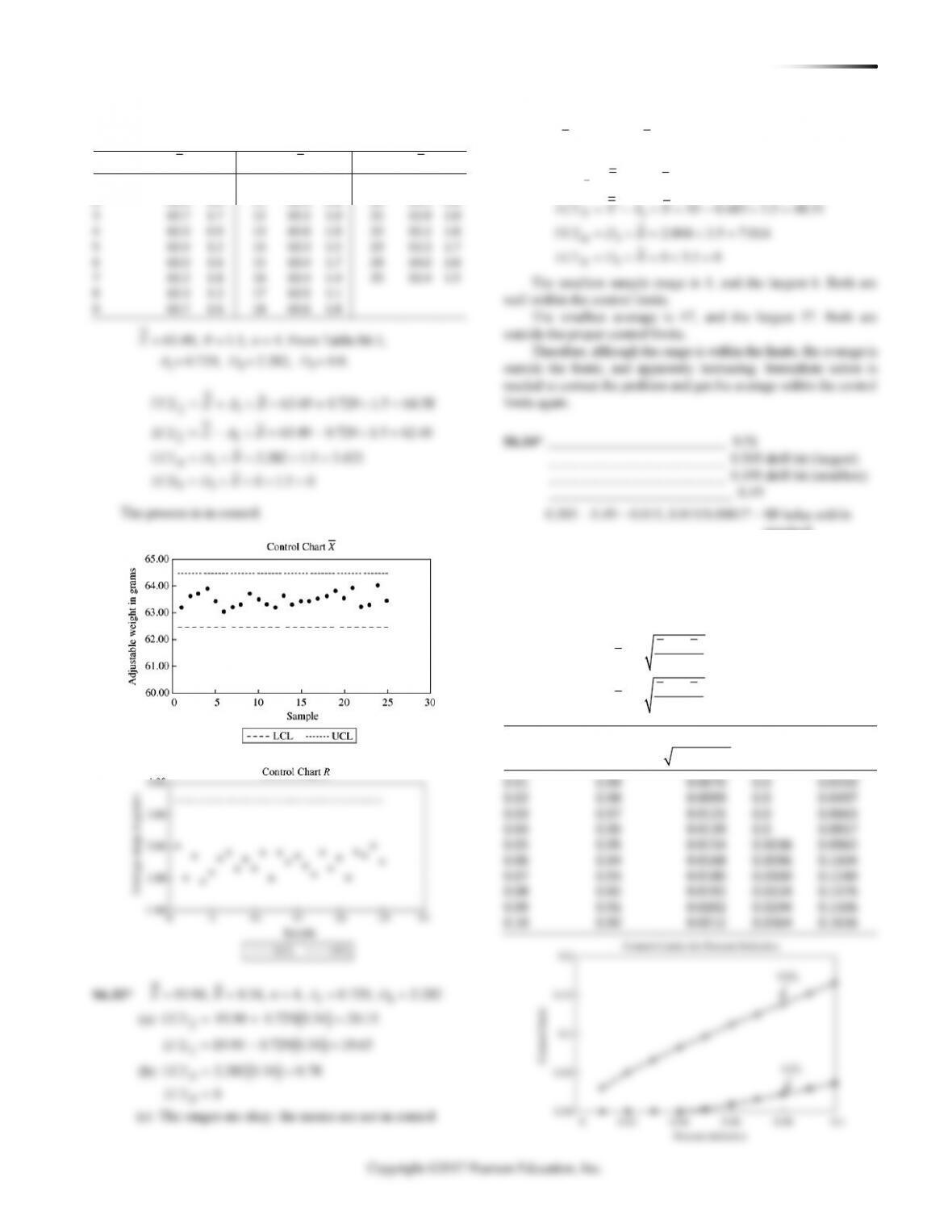

The process is in control.

S6.33*

Desired Desired

3.5, 50, 6R X n= = =

= + = + =

= − = − =

= = =

= = =

2

2

3

4

50 0.483 3.5 51.69

50 0.483 3.5 48.31

2.004 3.5 7.014

0 3.5 0

X

X

R

R

UCL X A R

LCL X A R

UCL D R

LCL D R

The smallest sample range is 1, and the largest 6. Both are

well within the control limits.

The smallest average is 47, and the largest 57. Both are

outside the proper control limits.

Therefore, although the range is within the limits, the average is

outside the limits, and apparently increasing. Immediate action is

needed to correct the problem and get the average within the control

limits again.

S6.34* 0.51

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 0.505 drill bit (largest)

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ 0.495 drill bit (smallest)

0.49

0.505 – 0.49 = 0.015, 0.015/0.00017 = 88 holes within

standard

0.495 – 0.49 = 0.005, 0.005/0.00017 = 29 holes within

standard

Any one drill bit should produce at least 29 holes that meet

tolerance but no more than 88 holes before being replaced.

(1 )

3

(1 )

3

−

=+

−

=−

pp

UCL p

pn

pp

LCL p

pn

S6.35 *

Percent

n = 200

Defective (p)

1 – p

_

(1 )/p p n

p

LCL

p

U CL

0.01

0.99

0.0070

0.0

0.0310

0.02

0.98

0.0099

0.0

0.0497

0.03

0.97

0.0121

0.0

0.0663

0.04

0.96

0.0139

0.0

0.0817

0.05

0.95

0.0154

0.0038

0.0962

0.06

0.94

0.0168

0.0096

0.1104

0.07

0.93

0.0180

0.0160

0.1240

0.08

0.92

0.0192

0.0224

0.1376

0.09

0.91

0.0202

0.0294

0.1506

0.10

0.90

0.0212

0.0364

0.1636

96 SUPPLEMENT 6 ST AT I ST I CA L PR OC ES S CO N TR O L

(1 )

3

(1 )

3

0.011 0.989

0.011 3 0.0209

1000

0.011 0.989

0.011 3 0.0011

1000

−

=+

−

=−

= + =

= − =

p

p

p

p

pp

UCL p n

pp

LCL p n

UCL

LCL

S6.36 *

1

21

0.105

Y

2

8

0.04

Y

3

18

0.09

Y

4

14

0.07

Y

5

20

0.1

Y

6

12

0.06

Y

19

21

0.105

Y

20

26

0.13

Y

21

28

0.14

Y

22

22

0.11

Y

23

17

0.085

Y

24

14

0.07

Y

25

12

0.06

Y

Std. Deviation of p = 0.020477

7

29

0.145

Y

8

24

0.12

Y

9

16

0.08

Y

10

20

0.1

Y

11

12

0.06

Y

12

7

0.035

Y

13

13

0.065

Y

14

24

0.12

Y

15

24

0.12

Y

16

32

0.16

N

17

12

0.06

Y

18

16

0.08

Y

SUPPLEMENT 6 ST AT ISTIC AL PROC ES S CO N T R O L 97

=

= = =

p

Difference between upper and lower specifications

C6

.6 .6 1.0

6(.1) .6

S6.40

This process is barely capable.

−

=

−

= = =

p

Upper specification Lower specification

C6

2,400 1,600 800 1.33

6(100) 600

S6.41

pk

C min ,

33

2,400 1,800 1,800 1,600

min ,

3(100) 3(100)

min [2.00, 0.67] = 0.67

USL x x LSL

−−

=

−−

=

=

The Cp tells us the machine’s variability is acceptable

relative to the range of tolerance limits. But the Cpk tells us the

distribution of output is too close to the lower specification and

will produce chips whose lives are too short.

−−

=

==

=

pk

pk

8.135 8.00 8.00 7.865

C min of , or

(3)(0.04) (3)(0.04)

0.135 0.135

1.125, 1.125

0.12 0.12

Therefore, C 1.125.

S6.42

The process is centered and will produce within the specified

Upper tolerance limit

Lower tolerance limit

Standard deviation

S6.47*

Time

Box 1

Box 2

Box 3

Box 4

Average

9 AM

9.8

10.4

9.9

10.3

10.1

10 AM

10.1

10.2

9.9

9.8

10.0

11 AM

9.9

10.5

10.3

10.1

10.2

12 PM

9.7

9.8

10.3

10.2

10.0

1 PM

9.7

10.1

9.9

9.9

9.9

Average=

10.04

Std. Dev. =

0.11

10.1 10 10 9.9

0.3 and 0.3

(3)(0.11) (3)(0.11)

−−

==

As 0.3 is less than 1, the process will not produce within the

specified tolerance.

S6.48* Machine 1 produces “off–center” with a smaller standard

deviation than Machine 2. Machine 1 has index of 0.83, and

Machine 2 has an index of 1.0. Thus, Machine 1 is not capable.

Machine 2 is capable.

Machine 1

Parameter

Value

Results

Value

Upper tolerance

0.403

Process capability

0.8333

limit

index

Lower tolerance

0.4

Upper one

1.6667

limit

sided index

Mean

0.401

Lower one

0.8333

sided index

Standard deviation

0.0004

98 SUPPLEMENT 6 ST AT I ST I CA L PR OC ES S CO N TR O L

S6.52

( )( )( – ) (.04)(.57)(500 – 60) 10.0

AOQ = .02

500 500

AOQ 2.0%

da

P P N n

N= = =

=

Time

Ave

Low

High

Ave

Low

High

Ave

Low

High

4:00

50.3

49.2

52.7

47.2

45.3

50.9

50.0

49.1

50.6

5:00

51.4

50.0

55.3

46.8

44.1

49.0

45.2

51.2

6:00

51.6

49.2

54.7

46.8

41.0

51.2

44.0

49.7

7:00

51.8

50.0

55.6

50.0

46.2

51.7

44.4

50.0

8:00

51.0

48.6

53.2

47.4

44.0

48.7

46.6

48.9

Time

Ave

Low

High

Ave

Low

High

Ave

Low

High

10:00

49.2

46.1

50.7

46.6

50.2

49.2

48.1

50.7

11:00

49.0

46.3

50.8

48.6

47.0

50.0

47.0

50.8

12:00

45.4

50.2

49.8

48.2

50.4

46.4

49.2

44.3

49.7

49.6

48.4

51.7

46.8

49.0

44.1

49.6

50.0

49.0

52.2

48.8

47.2

51.4

45.2

49.0

50.0

49.2

50.0

49.6

49.0

50.6

49.1

46.3

50.5

51.0

50.5

51.5

5:00

47.1

49.6

44.1

49.7

50.5

50.0

51.9

1:00

49.0

46.4

50.0

50.1

49.4

53.6

48.9

47.6

51.2

Evening Shift

Time

Ave

Low

High

Ave

Low

High

Ave

Low

High

2:00

49.0

46.0

50.6

49.7

48.6

51.0

49.8

48.4

51.0

3:00

49.8

48.2

50.8

48.4

47.2

51.7

49.8

48.8

50.8

SUPPLEMENT 6 ST AT ISTIC AL PROC ES S CO N T R O L 99

1

2

The immediate problem, however, must be corrected by additional

training, bag weight monitoring, and weight-feeder adjustments.

Short-run declines in bag output may be necessary to achieve

acceptable bag weights.

AACSB: Application of knowledge

VIDEO CASE STUDIES

These videos have been created specifically for this text to

supplement the cases below.

FRITO-LAY’S QUALITY-CONTROLLED

POTATO CHIPS

Note to instructors: Here is a real-world case of a company whose

products are known to every student. We suggest you show this

AACSB: Application of knowledge

3. Quality drives this consumer product. The taste of each chip

or other snack must be the same every bite. The bags must be

identical in weight and appearance. The product must be fresh.

Every step in production—from farm to factory—needs to meet

AACSB: Application of knowledge

2. Many options in any restaurant exist for fishbone analysis.

These include customer satisfaction, employee performance, meal

quality, and delivery quality. In the solutions of Chapter 6, we

presented several fishbone charts that can provide a starting point

for quality analysis in a restaurant:

◼ For the dissatisfied restaurant customer, see Solution 6.8,

“A Dissatisfied Airline Customer”

100 SUPPLEMENT 6 STAT IS TIC AL PROC ES S CO N T R O L

Sample 11 warrants some evaluation, but the report should sug-

gest an excellent process, and you tell the vendor to keep up the

good work.

LO S6.3: Build x-bar charts and R-charts

AACSB: Application of knowledge

ADDITIONAL CASE STUDY

(AVAILABLE IN MYOMLAB)

GREEN RIVER CHEMICAL CO.

This is a very straightforward case. Running software to analyze

the data will generate the

-chart asX