CHAPTER 4 FO R E C A ST I N G 41

2 2 2

650 4(2.5)(55) 650 550

30 25

30 4(2.5)

100 20

5

55 (20)(2.5)

5

xy nx y

b

x nx

a y bx

− − −

= = = −

− −

==

=−

=−

=

The regression line is y = 5 + 20x. The forecast for May (x = 5) is

y = 5 + 20(5) = 105.

4.25

Season

Year1

Demand

Year2

Demand

Average

Year1–Year2

Demand

Average

Season

Demand

Seasonal

Index

Year3

Demand

Fall

200

250

225.0

250

0.90

270

Winter

350

300

325.0

250

1.30

390

Spring

150

165

157.5

250

0.63

189

Summer

300

285

292.5

250

1.17

351

12 12

12

12

3

Average to Demand Demand

2

Demand for season

Sum of Ave to Demand

Average seasonal demand 4

Average to Demand

Seasonal index = Average Seasonal Demand

New Annual Demand S

4

Yr Yr Yr Yr

Yr Yr

Yr Yr

Yr

+

=

=

=

easonal index

1200 Seasonal index

4

=

4.26

Year

Winter

Spring

Summer

Fall

1

1,400

1,500

1,000

600

2

1,200

1,400

2,100

750

3

1,000

1,600

2,000

650

4

900

1,500

1,900

500

4,500

6,000

7,000

2,500

Average over all seasons:

Average over spring:

Spring index:

5,600

Answer: sailboats

4

20,000 1,250

16

6,000 1,500

4

1,500 1.2

1,250

(1.2) 1,680

=

=

=

=

4.27

Quarter

Year

1

Year

2

Year

3

Average

Demand

Average

Quarterly

Demand

Seasonal

Index

Winter

73

65

89

75.67

106.67

0.709

Spring

104

82

146

110.67

106.67

1.037

Summer

168

124

205

165.67

106.67

1.553

Fall

74

52

98

74.67

106.67

0.700

4.28 The year 26 quarter numbers are 101 through 104.

(5)

(2)

(3)

(4)

Adjusted

(1)

Quarter

Forecast

Seasonal

Forecast

Quarter

Number

(77 + .43Q)

Factor

[(3) × (4)]

Winter

101

120.43

.8

96.344

Spring

102

120.86

1.1

132.946

Summer

103

121.29

1.4

169.806

Fall

104

121.72

.7

85.204

4.29 (a) See the table below.

2

2,880 5(3)(180) 2,880 2,700

55 45

55 5(3)

180 18

10

180 3(18) 180 54 126

126 18

−−

==

−

−

==

= − = − =

=+

b

a

yx

Year

1

140

1

2

320

4

3

570

9

5

1,050

Totals

= 180

42 CHAPTER 4 FO R E C A ST I N G

4.30

Year X

Patients Y

X2

Y2

XY

1

36

1

1,296

36

2

33

4

1,089

66

3

40

9

1,600

120

4

41

16

1,681

164

5

40

25

1,600

200

6

55

36

3,025

330

7

60

49

3,600

420

8

54

64

2,916

432

9

58

81

3,364

522

10

61

100

3,721

610

55

478

385

23,892

2,900

Given: Y = a + bX where:

22

XY nXY

b

X nX

a Y bX

−

=−

=−

and X = 55, Y = 478, XY = 2900, X2 = 385, Y2 = 23892,

5.5, 47.8,XY==

Then:

− −

= = = =

−

−

= − =

2

2,900 10 5.5 47.8 2,900 2,629 271 3.28

385 302.5 82.5

385 10 5.5

47.8 3.28 5.5 29.76

b

a

and Y = 29.76 + 3.28X. For:

11: 29.76 3.28 11 65.8

12: 29.76 3.28 12 69.1

XY

XY

= = + =

= = + =

Therefore:

Year 11 → 65.8 patients

7

20

+41.1

–21.1

+37.6

–17.6

8

30

+36.9

–6.9

+27.1

+2.9

9

35

+35.5

–0.5

+28.8

+6.2

20

+35.4

–15.4

+32.5

–12.5

15

+32.3

–17.3

+25.0

–10.0

40

+28.9

+11.1

+19.0

+21.0

55

+31.1

+23.9

+31.6

+23.4

35

+35.9

–0.9

+45.6

–10.6

25

+36.7

–10.7

+39.3

–14.3

55

+33.6

+21.4

+30.7

+24.3

55

+37.8

+17.2

+45.3

+9.7

40

+41.3

–1.3

+51.1

–11.1

35

+41.0

–6.0

+44.4

–9.4

60

+39.8

+38.8

+21.2

75

+43.9

+31.1

+51.5

+23.5

50

+50.1

–0.1

+65.6

–15.6

40

+50.1

–10.1

+56.2

–16.2

65

+48.1

+16.9

+46.5

+18.5

Year

Patients

Trend

Absolute

X

Y

Forecast

Deviation

Deviation

1

36

29.8 + 3.28 × 1 = 33.1

2.9

2.9

2

33

29.8 + 3.28 × 2 = 36.3

–3.3

3.3

3

40

29.8 + 3.28 × 3 = 39.6

0.4

0.4

4

41

29.8 + 3.28 × 4 = 42.9

–1.9

1.9

5

40

29.8 + 3.28 × 5 = 46.2

–6.2

6.2

6

55

29.8 + 3.28 × 6 = 49.4

5.6

5.6

7

60

29.8 + 3.28 × 7 = 52.7

7.3

7.3

8

54

29.8 + 3.28 × 8 = 56.1

–2.1

2.1

9

58

29.8 + 3.28 × 9 = 59.3

–1.3

1.3

10

61

29.8 + 3.28 × 10 = 62.6

–1.6

1.6

= 32.6

MAD = 3.26

The MAD is 3.26—this is approximately 7% of the average number

of patients and 10% of the minimum number of patients. We also see

absolute deviations, for years 5, 6, and 7 in the range 5.6–7.3. The

comparison of the MAD with the average and minimum number of

patients and the comparatively large deviations during the middle

years indicate that the forecast model is not exceptionally accurate. It

is more useful for predicting general trends than the actual number of

patients to be seen in a specific year.

4.31 (a) and (b) See the following table:

Actual

Smoothed

Smoothed

Week

Value

Value

Forecast

Value

Forecast

t

A(t)

Ft ( = 0.2)

Error

Ft ( = 0.6)

Error

1

50

+50.0

+0.0

+50.0

+0.0

2

35

+50.0

–15.0

+50.0

–15.0

3

25

+47.0

–22.0

+41.0

–16.0

4

40

+42.6

–2.6

+31.4

+8.6

5

45

+42.1

–2.9

+36.6

+8.4

6

35

+42.7

–7.7

+41.6

–6.6

CHAPTER 4 FO R E C A ST I N G 43

The MAD = 12.208. To evaluate the trend adjusted exponential

smoothing model, actual week 25 calls are compared to the forecast

value. The model appears to be producing a MAD approximately

mid–range between that given by simple exponential smoothing

using = 0.2 and = 0.6. Trend adjustment does not appear to give

any significant improvement.

4.33 (a) There is not a strong linear trend in sales over time.

(b, c) Bob wants to forecast by exponential smoothing (setting

February’s forecast equal to January’s sales) with alpha =

0.1. Sherry wants to use a 3-period moving average.

Sales

Bob

Sherry

Bob’s Error

Sherry’s Error

January

400

—

—

—

—

February

380

400

—

20.0

—

March

410

398

—

12.0

—

April

375

399.2

396.67

24.2

21.67

May

405

396.8

388.33

8.22

16.67

MAD =

16.11

19.17

(d) Note that Bob has more forecast observations, while Sherry’s

moving average does not start until month 4. Also note that

the MAD for Bob is an average of 4 numbers, while Sherry’s

is only 2.

Bob’s MAD for exponential smoothing (16.11) is lower than

that of Sherry’s moving average (19.17). So his forecast

seems to be better.

8

30.000

30.571

–2.361

28.210

1.790

9

35.000

28.747

–2.253

26.494

8.506

10

20.000

29.046

–1.743

27.303

–7.303

11

15.000

25.112

–2.181

22.931

–7.931

12

40.000

20.552

–2.657

17.895

22.105

13

55.000

24.526

–1.331

23.196

31.804

14

35.000

32.737

0.578

33.315

1.685

15

25.000

33.820

0.679

34.499

–9.499

16

55.000

31.649

0.109

31.758

23.242

17

55.000

38.731

1.503

40.234

14.766

18

40.000

44.664

2.389

47.053

–7.053

19

35.000

44.937

1.966

46.903

–11.903

20

60.000

43.332

1.252

44.584

15.416

21

75.000

49.209

2.177

51.386

23.614

22

50.000

58.470

3.594

62.064

–12.064

23

40.000

58.445

2.870

61.315

–21.315

24

65.000

54.920

1.591

56.511

8.489

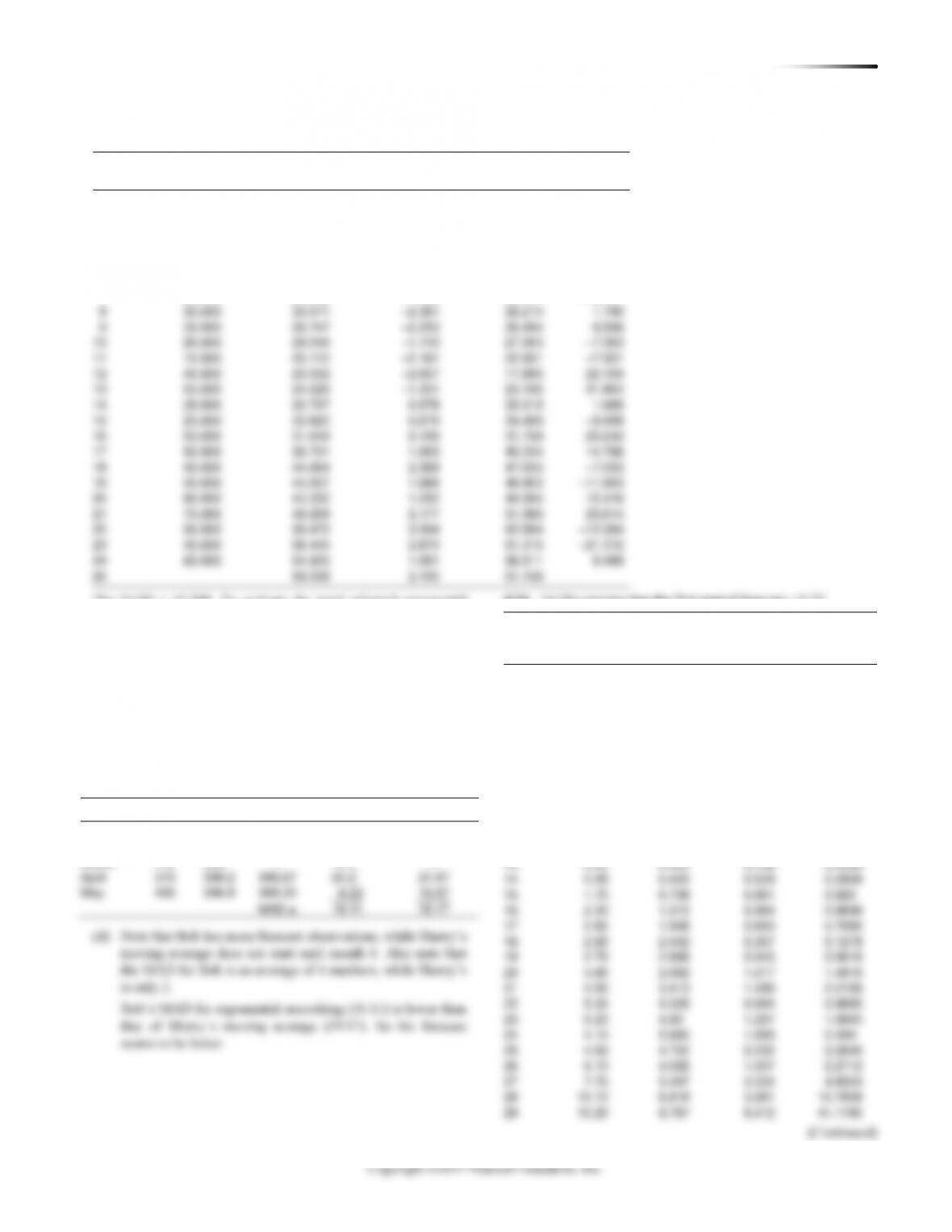

4.34 (a) We assume that the first-period forecast = 0.25.

Method → Exponential Smoothing

0.6 =

Year

Deposits (Y)

Forecast

|Error|

Error2

1

0.25

0.25

0.00

0.00

2

0.24

0.25

0.01

0.0001

3

0.24

0.244

0.004

0.0000

4

0.26

0.241

0.018

0.0003

5

0.25

0.252

0.002

0.00

6

0.30

0.251

0.048

0.0023

7

0.31

0.280

0.029

0.0008

8

0.32

0.298

0.021

0.0004

9

0.24

0.311

0.071

0.0051

10

0.26

0.268

0.008

0.0000

11

0.25

0.263

0.013

0.0002

12

0.33

0.255

0.074

0.0055

13

0.50

0.300

0.199

0.0399

14

0.95

0.420

0.529

0.2808

15

1.70

0.738

0.961

0.925

16

2.30

1.315

0.984

0.9698

17

2.80

1.906

0.893

0.7990

18

2.80

2.442

0.357

0.1278

19

2.70

2.656

0.043

0.0018

20

3.90

2.682

1.217

1.4816

21

4.90

3.413

1.486

2.2108

22

5.30

4.305

0.994

0.9895

23

6.20

4.90

1.297

1.6845

24

4.10

5.680

1.580

2.499

25

4.50

4.732

0.232

0.0540

26

6.10

4.592

1.507

2.2712

27

7.70

5.497

2.202

4.8524

28

10.10

6.818

3.281

10.7658

29

15.20

8.787

6.412

41.1195

(Continued)

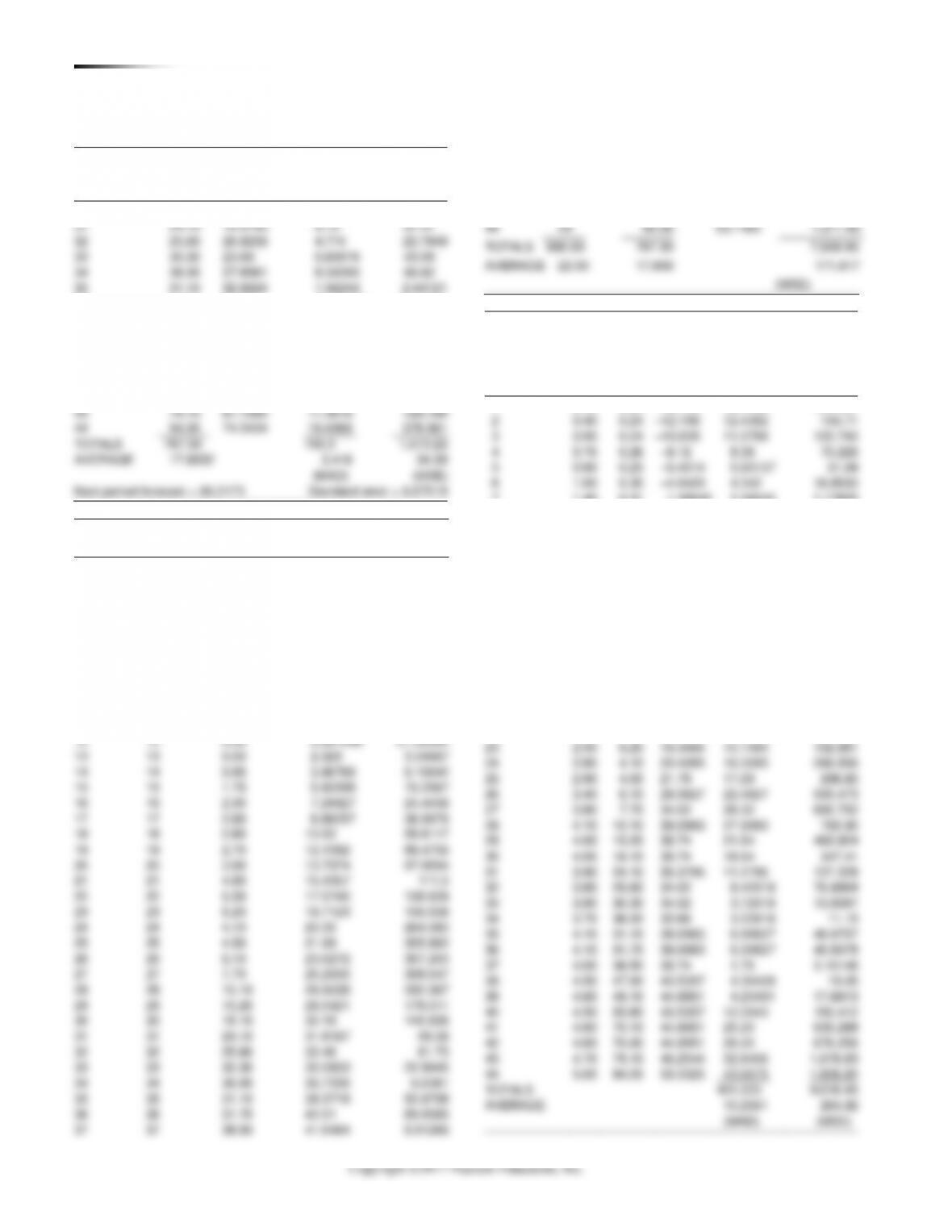

4.32

Week

Actual Value

Smoothed Value

Trend Estimate

Forecast

Forecast

t

At

Ft (

= 0.3)

Tt (

= 0.2)

FITt

Error

1

50.000

50.000

0.000

50.000

0.000

2

35.000

50.000

0.000

50.000

–15.000

3

25.000

45.500

–0.900

44.600

–19.600

4

40.000

38.720

–2.076

36.644

3.356

5

45.000

37.651

–1.875

35.776

9.224

6

35.000

38.543

–1.321

37.222

–2.222

7

20.000

36.555

–1.455

35.101

–15.101

44 CHAPTER 4 FO R E C A ST I N G

4.34 (a) (Continued)

Method → Exponential Smoothing

0.6 =

Year

Deposits (Y)

Forecast

|Error|

Error2

30

18.10

12.6350

5.46498

29.8660

31

24.10

15.9140

8.19

67.01

32

25.60

20.8256

4.774

22.7949

33

30.30

23.69

6.60976

43.69

34

36.00

27.6561

8.34390

69.62

35

31.10

32.6624

1.56244

2.44121

36

31.70

31.72

0.024975

0.000624

37

38.50

31.71

6.79

46.1042

38

47.90

35.784

12.116

146.798

39

49.10

43.0536

6.046

36.56

40

55.80

46.6814

9.11856

83.1481

41

70.10

52.1526

17.9474

322.11

42

70.90

62.9210

7.97897

63.66

43

79.10

67.7084

11.3916

129.768

44

94.00

74.5434

19.4566

378.561

TOTALS

787.30

150.3

1,513.22

AVERAGE

17.8932

3.416

34.39

(MAD)

(MSE)

Next period forecast = 86.2173

Standard error = 6.07519

Method → Linear Regression (Trend Analysis)

Year

Period (X)

Deposits (Y)

Forecast

Error2

1

1

0.25

–17.330

309.061

2

2

0.24

–15.692

253.823

3

3

0.24

–14.054

204.31

4

4

0.26

–12.415

160.662

5

5

0.25

–10.777

121.594

6

6

0.30

–9.1387

89.0883

7

7

0.31

–7.50

61.0019

8

8

0.32

–5.8621

38.2181

9

9

0.24

–4.2238

19.9254

10

10

0.26

–2.5855

8.09681

11

11

0.25

–0.947

1.43328

12

12

0.33

0.691098

0.130392

13

13

0.50

2.329

3.34667

14

14

0.95

3.96769

9.10642

15

15

1.70

5.60598

15.2567

16

16

2.30

7.24427

24.4458

17

17

2.80

8.88257

36.9976

18

18

2.80

10.52

59.6117

19

19

2.70

12.1592

89.4756

20

20

3.90

13.7974

97.9594

21

21

4.90

15.4357

111.0

22

22

5.30

17.0740

138.628

23

23

6.20

18.7123

156.558

24

24

4.10

20.35

264.083

25

25

4.50

21.99

305.862

26

26

6.10

23.6272

307.203

27

27

7.70

25.2655

308.547

28

28

10.10

26.9038

282.367

29

29

15.20

28.5421

178.011

30

30

18.10

30.18

145.936

31

31

24.10

31.8187

59.58

32

32

25.60

33.46

61.73

33

33

30.30

35.0953

22.9945

34

34

36.00

36.7336

0.5381

35

35

31.10

38.3718

52.8798

36

36

31.70

40.01

69.0585

37

37

38.50

41.6484

9.91266

38

38

47.90

43.2867

21.2823

39

39

49.10

44.9250

17.43

40

40

55.80

46.5633

85.3163

41

41

70.10

48.2016

479.54

42

42

70.90

49.84

443.528

43

43

79.10

51.4782

762.964

44

44

94.00

53.1165

1,671.46

TOTALS

990.00

787.30

7,559.95

AVERAGE

22.50

17.893

171.817

(MSE)

Method → Least squares–Simple Regression on GSP

(a)

(b)

–17.636

13.5936

Coefficients:

GSP

Deposits

Year

(X)

(Y)

Forecast

|Error|

Error2

1

0.40

0.25

–12.198

12.4482

154.957

2

0.40

0.24

–12.198

12.4382

154.71

3

0.50

0.24

–10.839

11.0788

122.740

4

0.70

0.26

–8.12

8.38

70.226

5

0.90

0.25

–5.4014

5.65137

31.94

6

1.00

0.30

–4.0420

4.342

18.8530

7

1.40

0.31

1.39545

1.08545

1.17820

8

1.70

0.32

5.47354

5.15354

26.56

9

1.30

0.24

0.036086

0.203914

0.041581

10

1.20

0.26

–1.3233

1.58328

2.50676

11

1.10

0.25

–2.6826

2.93264

8.60038

12

0.90

0.33

–5.4014

5.73137

32.8486

13

1.20

0.50

–1.3233

1.82328

3.32434

14

1.20

0.95

–1.3233

2.27328

5.16779

15

1.20

1.70

–1.3233

3.02328

9.14020

16

1.60

2.30

4.11418

1.81418

3.29124

17

1.50

2.80

2.75481

0.045186

0.002042

18

1.60

2.80

4.11418

1.31418

1.727

19

1.70

2.70

5.47354

2.77354

7.69253

20

1.90

3.90

8.19227

4.29227

18.4236

21

1.90

4.90

8.19227

3.29227

10.8390

22

2.30

5.30

13.6297

8.32972

69.3843

23

2.50

6.20

16.3484

10.1484

102.991

24

2.80

4.10

20.4265

16.3265

266.556

25

2.90

4.50

21.79

17.29

298.80

26

3.40

6.10

28.5827

22.4827

505.473

27

3.80

7.70

34.02

26.32

692.752

28

4.10

10.10

38.0983

27.9983

783.90

29

4.00

15.20

36.74

21.54

463.924

30

4.00

18.10

36.74

18.64

347.41

31

3.90

24.10

35.3795

11.2795

127.228

32

3.80

25.60

34.02

8.42018

70.8994

33

3.80

30.30

34.02

3.72018

13.8397

34

3.70

36.00

32.66

3.33918

11.15

35

4.10

31.10

38.0983

6.99827

48.9757

36

4.10

31.70

38.0983

6.39827

40.9378

37

4.00

38.50

36.74

1.76

3.10146

38

4.50

47.90

43.5357

4.36428

19.05

39

4.60

49.10

44.8951

4.20491

17.6813

40

4.50

55.80

43.5357

12.2643

150.412

41

4.60

70.10

44.8951

25.20

635.288

42

4.60

70.90

44.8951

26.00

676.256

43

4.70

79.10

46.2544

32.8456

1,078.83

44

5.00

94.00

50.3325

43.6675

1,906.85

TOTALS

451.223

9,016.45

AVERAGE

10.2551

204.92

(MAD)

(MSE)

CHAPTER 4 FO R E C A ST I N G 45

Copyright ©2017 Pearson Education, Inc.

Given that one wishes to develop a 5-year forecast,

trend analysis is the appropriate choice. Measures of

error and goodness-of-fit are really irrelevant. Exponen-

tial smoothing provides a forecast only of deposits for

the next year—and thus does not address the 5-year

forecast problem. In order to use the regression model

based on GSP, one must first develop a model to fore-

cast GSP, and then use the forecast of GSP in the model

to forecast deposits. This requires the development of

two models—one of which (the model for GSP) must be

based solely on time as the independent variable (time is

the only other variable we are given).

(b) One could make a case for exclusion of the older data.

Were we to exclude data from roughly the first 25 years,

the forecasts for the later years would likely be consider-

ably more accurate. Our argument would be that a

change that caused an increase in the rate of growth ap-

pears to have taken place at the end of that period. Ex-

clusion of this data, however, would not change our

choice of forecasting model because we still need to

forecast deposits for a future 5-year period.

4.35*

smallest MSE of 20.6.

Problem 4.34 (Continued)

Forecasting Summary Table

Exponential

Linear Regression

Method Used

Smoothing

(Trend Analysis)

Linear Regression

Y = –18.968 +

Y = –17.636 +

1.638 × Year

13.59364 × GSP

MAD

3.416

10.587

10.255

MSE

34.39

171.817

204.919

Standard error using

6.075

13.416

14.651

n – 2 in denominator

Correlation coefficient

0.846

0.813

Week

1

2

3

4

5

6

7

8

9

10

Forecast

Registration

22

21

25

27

35

29

33

37

41

37

(a)

Naïve

22

21

25

27

35

29

33

37

41

37

(b)

2-week moving

21.5

23

26

31

32

31

35

39

39

(c)

4-week moving

23.75

27

29

31

33.5

35

37

46 CHAPTER 4 FO R E C A ST I N G

4.36*

Period

Demand

Exponentially Smoothed Forecast

1

7

5

2

9

5 + 0.2 × (7 – 5) = 5.4

3

5

5.4 + 0.2 × (9 – 5.4) = 6.12

4

9

6.12 + 0.2 × (5 – 6.12) = 5.90

5

13

5.90 + 0.2 × (9 – 5.90) = 6.52

6

8

6.52 + 0.2 × (13 – 6.52) = 7.82

7

Forecast

7.82 + 0.2 × (8 – 7.82) = 7.86

4.37*

Actual

Forecast

|Error|

Error2

95

100

5

25

108

110

2

4

123

120

3

9

130

130

0

0

10

38

4.38* (a) 3-month moving average:

3-Month

Absolute

Month

Sales

Moving Average

Deviation

January

11

February

14

March

16

April

10

(11 + 14 + 16)/3 = 13.67

3.67

May

15

(14 + 16 + 10)/3 = 13.33

1.67

June

17

(16 + 10 + 15)/3 = 13.67

3.33

July

11

(10 + 15 + 17)/3 = 14.00

3.00

August

14

(15 + 17 + 11)/3 = 14.33

0.33

September

17

(17 + 11 + 14)/3 = 14.00

3.00

October

12

(11 + 14 + 17)/3 = 14.00

2.00

November

14

(14 + 17 + 12)/3 = 14.33

0.33

December

16

(17 + 12 + 14)/3 = 14.33

1.67

January

11

(12 + 14 + 16)/3 = 14.00

3.00

February

(14 + 16 + 11)/3 = 13.67

= 22.00

MAD = 2.20

(b) 3-month weighted moving average

June

17

(1 × 16 + 2 × 10 + 3 × 15)/6 = 13.50

3.50

July

11

(1 × 10 + 2 × 15 + 3 × 17)/6 = 15.17

4.17

August

14

(1 × 15 + 2 × 17 + 3 × 11)/6 = 13.67

0.33

September

17

(1 × 17 + 2 × 11 + 3 × 14)/6 = 13.50

3.50

October

12

(1 × 11 + 2 × 14 + 3 × 17)/6 = 15.00

3.00

November

14

(1 × 14 + 2 × 17 + 3 × 12)/6 = 14.00

0.00

December

16

(1 × 17 + 2 × 12 + 3 × 14)/6 = 13.83

2.17

(c) Based on a mean absolute deviation criterion, the

3-month moving average with MAD = 2.2 is to be pre-

ferred over the 3-month weighted moving average with

MAD = 2.72.

4.39*

y

x

x2

xy

7

1

1

7

9

2

4

18

5

3

9

15

11

4

16

44

10

5

25

50

13

6

36

78

55

21

91

212

9.17

3.5

5.27 1.11

y

x

yx

=

=

=+

Period 7 forecast = 13.07

Period 12 forecast = 18.64, but this is far outside the range

of valid data.

4.40* To compute seasonalized or adjusted sales forecast, we just

multiply each seasonalized index by the appropriate trend forecast.

Seasonal Trend forecast

ˆˆ

Y Index Y=

Hence, for

ˆ

Quarter I: 1.25 120, 000 150,000

ˆ

Quarter II: 0.90 140,000 126,000

ˆ

Quarter III: 0.75 160,000 120,000

ˆ

Quarter IV: 1.10 180, 000 198,000

I

II

III

IV

Y

Y

Y

Y

= =

= =

= =

= =

Month

Sales

3-Month Weighted Moving Average

Absolute Deviation

January

11

February

14

March

16

April

10

(1 × 11 + 2 × 14 + 3 × 16)/6 = 14.50

4.50

May

15

(1 × 14 + 2 × 16 + 3 × 10)/6 = 12.67

2.33

CHAPTER 4 FO R E C A ST I N G 47

4.41*

Forecast 220 (Mon) 180 (Tue) 258 (Wed)

221 (Thu) 171 (Fri) 189 (Sat)

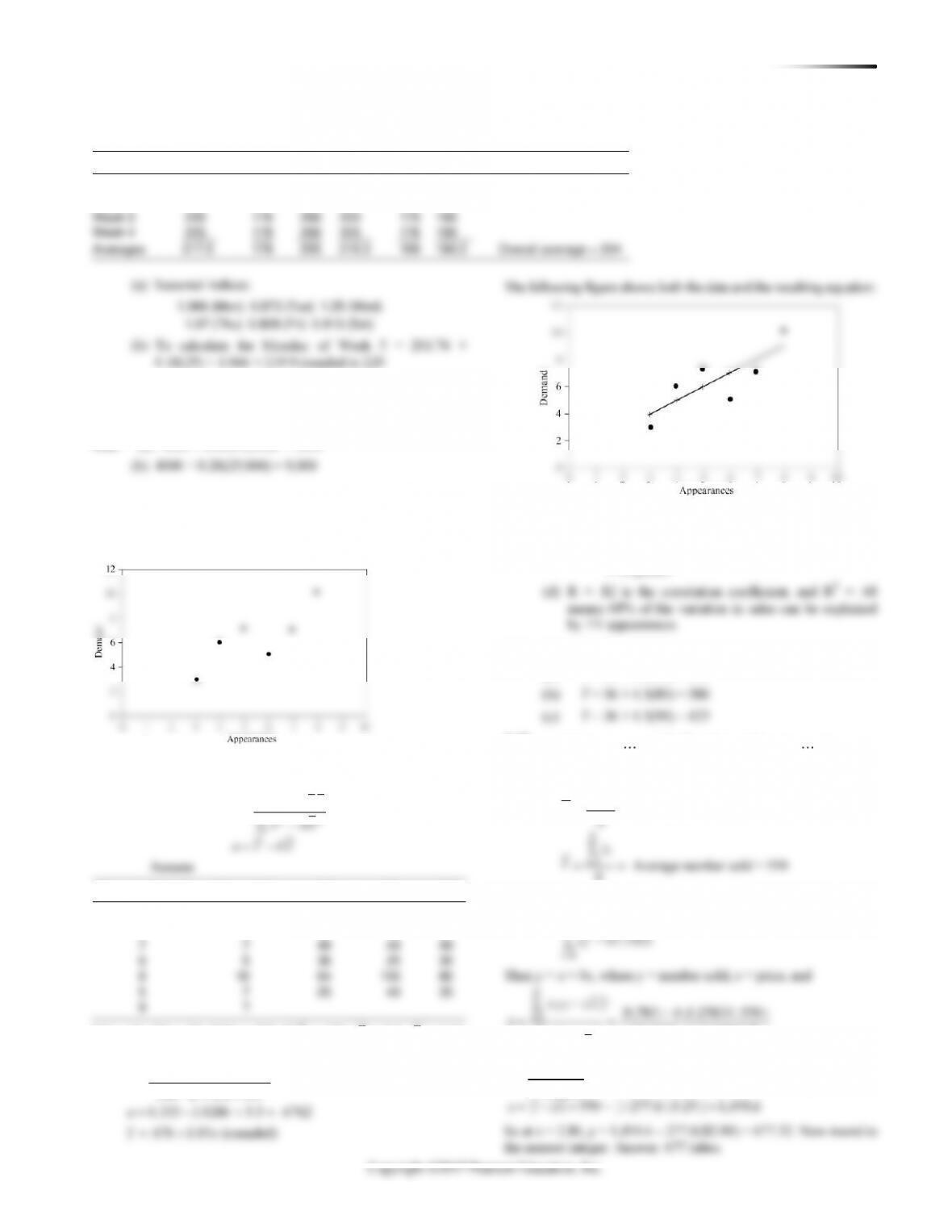

4.43 (a) Graph of demand

The observations obviously do not form a straight line but do tend

to cluster about a straight line over the range shown.

(b) Least-squares regression:

22

Y a bX

XY nXY

b

X nX

a Y bX

=+

−

=−

=−

Appearances X

Demand Y

X2

Y2

XY

3

3

9

9

9

4

6

16

36

24

7

7

49

49

49

6

5

36

25

30

8

10

64

100

80

5

7

25

49

35

9

?

X = 33, Y = 38, XY = 227, X2 = 199,

X

= 5.5,

Y

= 6.33.

Therefore:

b

==

227 – 6 5.5 6.333 1.0286

Week 4

225

178

260

225

176

190

(c) If there are nine performances by Maroon 5, the

estimated sales are:

9.676 1.03 9 .676 9.27 9.93 guitars

10 guitars

= + = + =

Y

4.44 Given Y = 36 + 4.3X

(a) Y = 36 + 4.3(70) = 337

4.45

=

=

=

=

==

=

1 2 6 1 2 6

6

1

6

1

6

1

62

1

Let , , , be the prices and , , ,

be the number sold.

Average price = 3.2583

6

6

9,783

= 67.1925

i

i

i

i

ii

i

i

i

x x x y y y

x

X

y

xy

x

Then y = a + bx, where y = number sold, x = price, and

6

1

62

22

1

9 783 6 3 25833 550

67 1925 6 3 25833

969 489 277 6

( , ) ( . )( )

. ( . )

..

ii

i

i

i

x y nxy

b

x nx

=

=

−

−

==

−

−

−

= = −

Mon.

Tue.

Wed.

Thu.

Fri.

Sat.

Week 1

210

178

250

215

160

180

Week 2

215

180

250

213

165

185

Week 3

220

176

260

220

175

190