Chapter 2 Securities Markets and Transactions 15

Suggested Answers to Discussion Questions

8.2 a. 1.The value of a growth stock that pays little or nothing in dividends could be found using a

2. The S&P 500 would best be valued with a constant growth model, since abnormally good

3. A relatively new company that has a brief history of earnings would best be valued using a

4. A large, mature company is probably paying a dividend; however, that dividend might vary

6. A firm with a large amount of depreciation and amortization should use the free cash flow to

b. Answers will vary by student and this is a good topic to stimulate discussion, but the instructor

should emphasize that valuation models are not a one-size-fits-all choice. For established

c. Again, answers will vary by student and this is a good topic for discussion.. The choice of a

8.3 All decisions are made in light of future consequences. Shareholder investment decisions are based

upon the future cash inflows arising from their investment. New firm-specific events (i.e., anticipated

The intrinsic value of a stock is an inverse function of the required rate of return. The higher the

8.4 a. Increase. The answer depends upon the impact of the dividend payout ratio going up on

growth.

If sales and earnings, and consequently cash paid out over time, do not change, as assumed in the

b. Decrease. As a stock’s systematic risk rises, the required rate of return will also rise. If dividends

©2017 Pearson Education, Inc.

16 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

c. Increase. A decrease in the equity multiplier results from less financial leverage being used by the

d. Increase. A decrease in the T-bill rate decreases the required rate of return. As the required rate of

e. Increase. An increasing net profit margin will result in both a higher current dividend and a

f. Decrease. As total asset turnover declines, fewer dollars are earned per dollar invested and the

g. Decrease. If the market return increases, investors will demand a higher return on each individual

Solutions to Problems

b. Total dividends next year are $5 million (half of earnings), and dividing that by the number of

8.3 With total equity of $600 million and an ROE of 18%, Granger earned net income of $108 million.

8.4 Dividend per share EPS Payout ratio

8.5 Growth rate ROE Retention rate

8.6 Total debt $75M/0.10 $750,000,000

©2017 Pearson Education, Inc.

Chapter 2 Securities Markets and Transactions 17

Interest expense 0.075 $862,500,000 $64,687,500

8.7

8.8 a. The intrinsic worth (or justified price) is equal to the present value of expected dividends

b. N=3, i=?, PV=–48, PMT=4, FV=60, i=expected return=15.5%

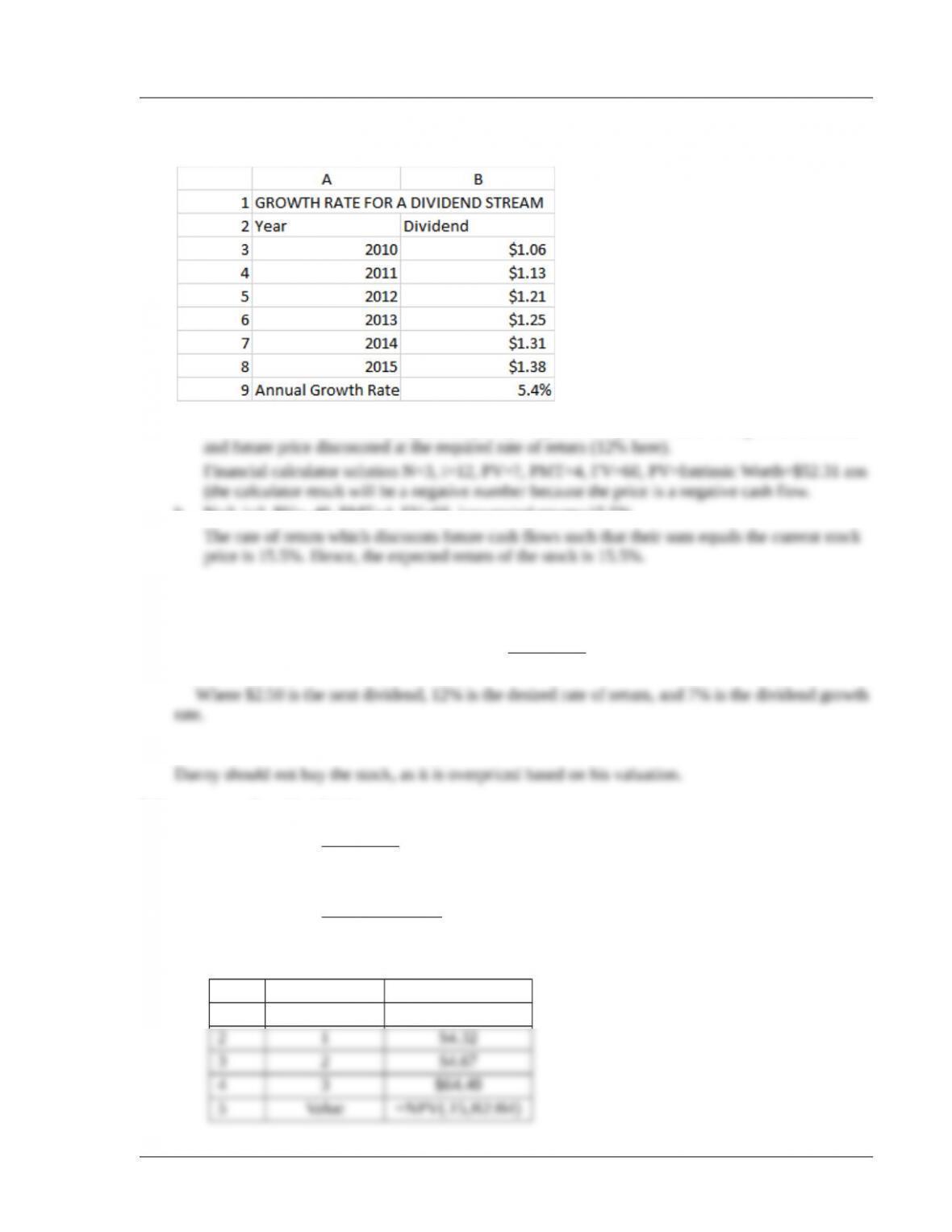

8.9 The intrinsic value of Amalgamated Aircraft Parts, Inc., can be calculated using the dividend

valuation model:

$2.50

Value per share $50

0.12 0.07

= =

–

8.10 Intrinsic value Annual dividend/ Required rate of return $2/.12 $16.67

8.11 a. Larry’s valuation

$2.50

Value per share $37.50

0.12 0.05

= =

–

Curley’s valuation:

$1,000,000(1.05)

Value per share / 400,000 $37.50

0.12 0.05

= =

–

8.12 a.

A B

1 Year Cash flow

©2017 Pearson Education, Inc.

18 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

The value of the stock at the end of year 3 is the present value of all future dividends. Using the

above.

c.

A B

1 Year Cash flow

e.

A B

1 Year Cash flow

8.13 First, use the CAPM to find the stock’s required return:

To find the expected return on this security, we need to find the expected future price of the stock:

Future price of the stock Future EPS Expected P/E multiple

If we assume that the P/E ratio will still be 10 at the end of 3 years, the value of WCE’s stock will

10 x $7 = $70. Therefore, if we buy the stock today, we experience a cash outflow of $62. In years 1,

A B

©2017 Pearson Education, Inc.

Chapter 2 Securities Markets and Transactions 19

1 Year Cash flow

Using the dividend valuation model with constant dividends the intrinsic value of the stock would

Why are these two approaches giving us conflicting answers, indicating that the stock is a good

Under these assumptions, the value of the stock is slightly higher than its market price, so it is a

(moderately) good buy.

Returning to the original assumptions in this problem, if we believed that dividends would remain

On the other hand, what rate of return would justify a stock price of $70, again assuming that

dividends stay at $5 forever:

So if we expected the required return on this stock to fall, that would bring about an increase in the

©2017 Pearson Education, Inc.

20 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

8.14 Calculator solution: N=3, i=?, PV=–80, PMT=0, FV=110. I=11.2% ans. Because 11.2% is ABOVE

8.15 a.

Projected Annual Dividends

Year Dividends

Estimated annual growth rate for year 6 and beyond: 6%

Step 1: Present value of dividends using a required rate of return of 12%:

Year Dividends

Present

Value

Note that the $14.22 sum above might appear to be off by one penny, but that is simply a

rounding issue. Throughout this solution, we perform calculations in Excel and do not round any

numbers until the final answer is obtained, so apparent errors of a penny or two arise simply

because of this approach to rounding.

Step 2: Price of stock at the end of year 5:

P5

D6

r–g=$5.12

0.12 –0.06 =$5.12

0.06 =$85.33

Step 3: Take the price of the stock price at the end of year 5 and calculate its present value as of

today:

Step 4:

Therefore, $62.65 is the maximum price you should be willing to pay for this stock.

©2017 Pearson Education, Inc.

Chapter 2 Securities Markets and Transactions 21

b. Since g 0 for year 6 and beyond, dividends for year 6 will be the same as the dividend for

P5

D6

r–g=$4.83

0.12 –0=$4.83

0.12 =$40.25

Step 3: Present value of the stock price = $40.26 / (1.12) 5 = $22.85

Since the present value of the first 5 years of dividends is the same as in a. above, the intrinsic

value of the stock is:

c. The intrinsic value of the stock in a. is much higher than that computed in b. In a., dividends are

©2017 Pearson Education, Inc.