Chapter 5 Modern Portfolio Concepts 75

5.19 a. If the market return increases by 13.2%, the table below shows the extent to which each

security’s return will change in response:

Security Beta Change in

rm

Change in

ri

b.

Security Beta Change in

rm

Change in

ri

c. Security C is the most risky security in the sense that it has the highest

beta.Security C’s negative beta means that its returns are negatively correlated with the market,

making it the least risky security. Because Security C performs best when most other securities

5.20 Because each investment has an equal weight, the portfolio beta is simply 1/3(1.4) + 1/3(0.8) +

1/3(–.9) = 0.43.

5.21 If the market rallied 20%, the portfolio would be expected to rise by 0.43(20%) = 8.6%. The

$60,000 portfolio would then have a value of $60,000(1.086) = $65,160.

5.22

Security

Risk-Free

Rate

Market

Return Beta Ri = rrf + β(rm – rf)

A 5 8 1.3 8.9

B 8 13 0.9 12.5

5.23 Using the CAPM, Jay’s required rate of return on the stock should be:

Required rate of return Risk-free rate [Beta (Market rate Risk-free rate)]

©2017 Pearson Education, Inc.

76 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

24. If the risk-free rate is 3% and the market return is 10%:

b. Capital asset pricing model: ri RF [bi (rm RF)]

Investment riRF [bi (rm RF)]

A 13.5% 3% [1.50 (10% 3%)]

c. The figure showing the security market line (SML) can be found on the book’s website at

d. Based on the above graph and the calculations, there is a linear relationship between risk and

return.

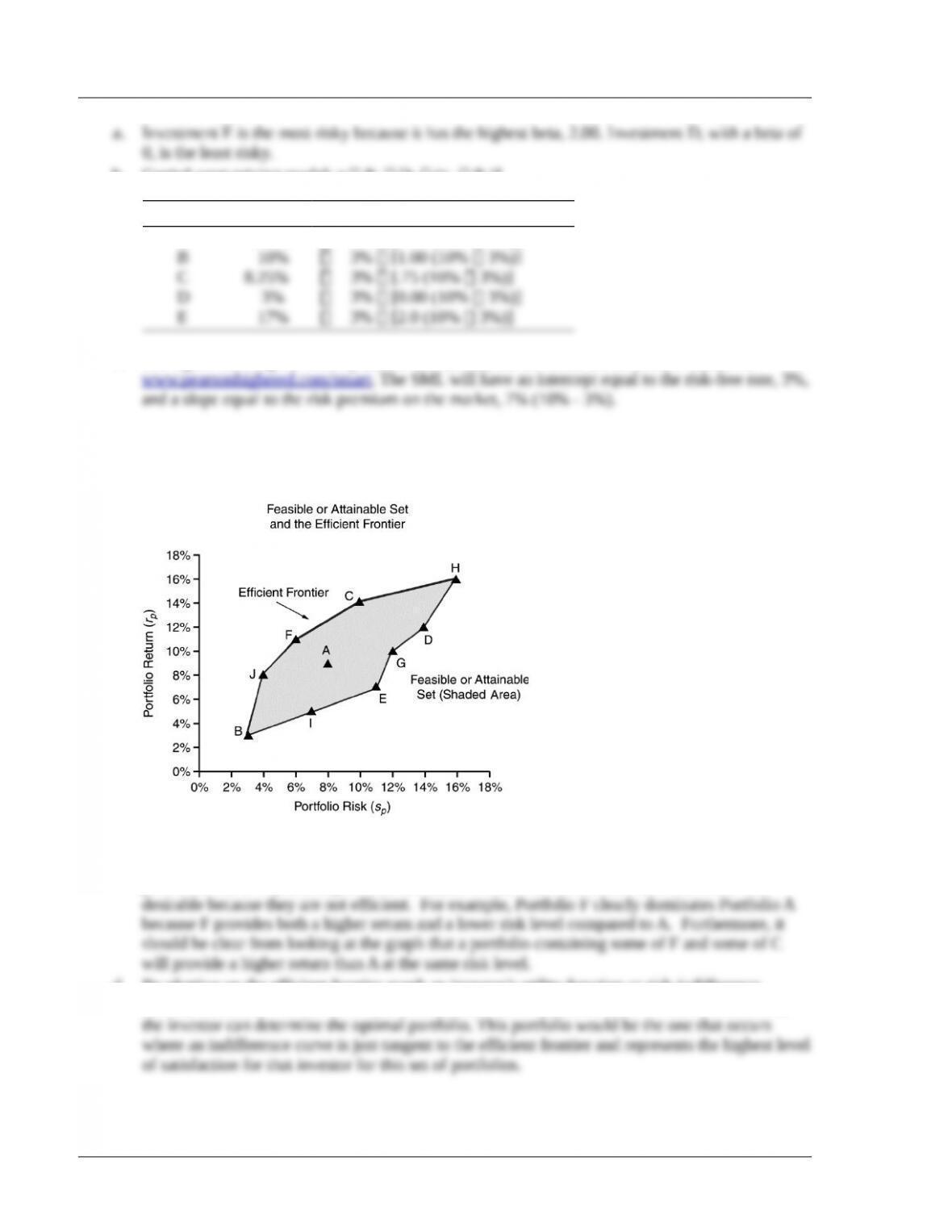

5.25 a. and b.

c. Portfolios B, J, F, C, and H lie on the efficient frontier. These portfolios are the efficient

portfolios, those that provide the best tradeoff between risk and return (the highest return for a

particular risk level). These portfolios dominate because all those below the frontier are not

d. By plotting on the efficient frontier graph an investor’s utility function or risk-indifference

curves, which show those risk-return combinations for which an investor would be indifferent,

©2017 Pearson Education, Inc.

Chapter 5 Modern Portfolio Concepts 77

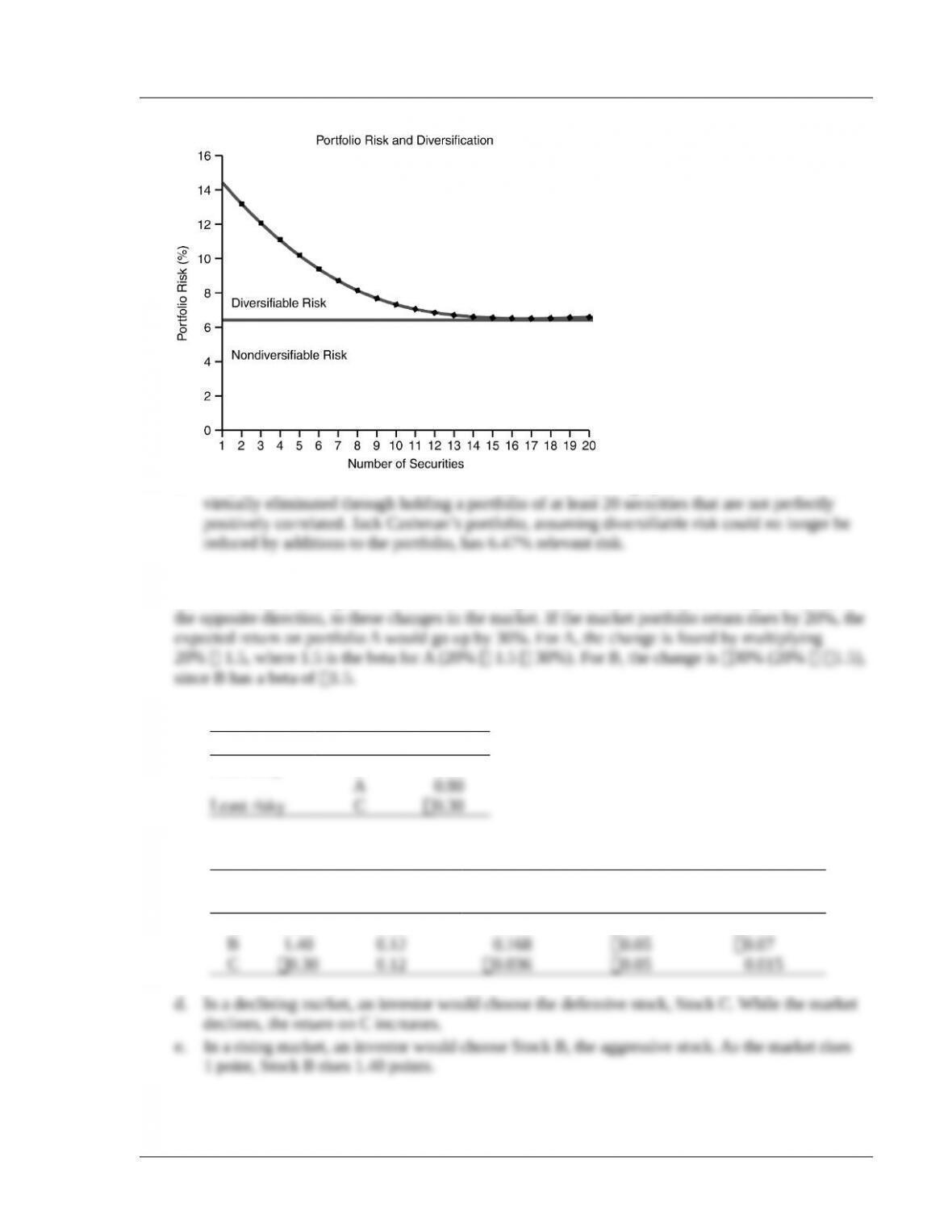

5.26 a. and b.

c. Only undiversifiable risk is relevant because, as shown by the graph, diversifiable risk can be

5.27 With a beta value of 1.5, portfolio A would be 1.5 times as responsive to changes in the market as

the market itself, while portfolio Z with a beta of 1.5 would also be 1.5 times as responsive, but in

5.28 a.

Stock Beta

Most risky B 1.40

b. and c.

Stock Beta

Increase in

Market Return

Impact on

Asset Return

Decrease in

Market Return

Impact on

Asset Return

A 0.80 0.12 0.096 0.05 0.04

©2017 Pearson Education, Inc.

78 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

5.29

1

Portfolio betas:

n

p j j

i

b w b

=

= ´

å

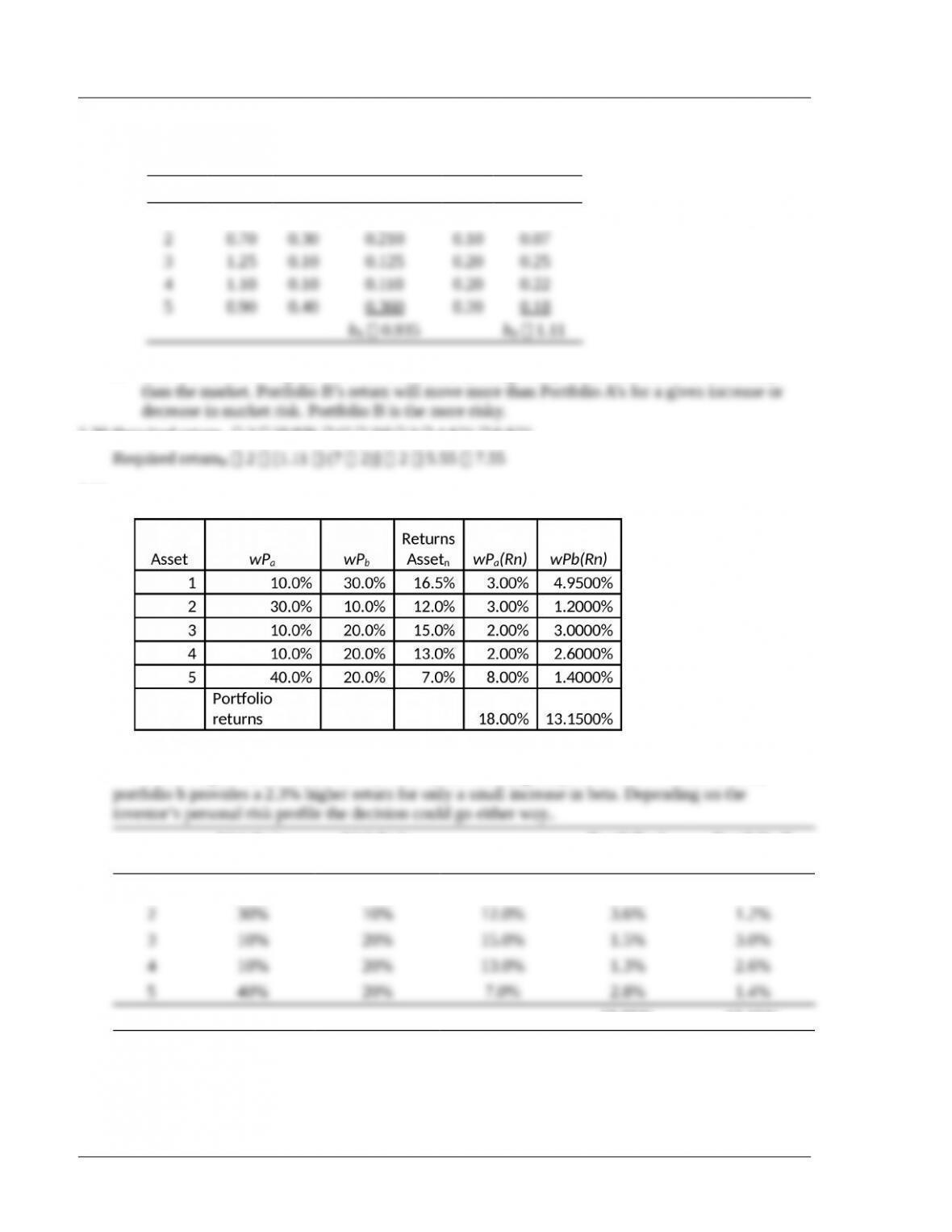

a.

Asset Beta wAwA bAwBwB bB

1 1.30 0.10 0.130 0.30 0.39

b. Portfolio A risk is slightly less than the market (average risk), while Portfolio B is more risky

5.30 Required returnA 2 [0.935 (7 2)] 2 4.675 6.675

5.31

Portfolio a provides a lower return (10.85%) but has marginally lower risk with beta at .935;

Asset

Weight in

Portfolio A

Weight in

Portfolio B Asset Return

Portfolio A

Return

Portfolio B

Return

1 10% 30% 16.5% 1.65% 4.95%

10.85% 13.15%

Solutions to Case Problems

©2017 Pearson Education, Inc.

Chapter 5 Modern Portfolio Concepts 79

Case 5.1 Traditional Versus Modern Portfolio Theory: Who’s Right?

This case provides a basis for discussion of traditional and modern portfolio theory with emphasis on the

reconciliation of the two.

a. Walt’s arguments rely on the traditional approach to portfolio management. He believes that by

building a large portfolio, the maximum benefits of diversification can be achieved. For this reason,

b. Shane is incorrect in assuming that the stock with a beta of 1.2 is equivalent to a mutual fund with a

beta of 1.2. The error in logic occurs because a stock with a beta of 1.2 also has a certain amount of

diversifiable (unsystematic) risk. On the other hand, a mutual fund with a beta of 1.2 has no diversifiable

risk. Therefore, the only risk in a mutual fund is its nondiversifiable risk. Simply stated, a stock

c. The traditional approach to portfolio management simply involves forming a portfolio with a large

variety of stocks from different industries to obtain the benefits of diversification. These are usually

d. Modern portfolio theory relies on statistical concepts. The use of the correlation coefficient and the

beta value are the most popular. Two securities that are negatively correlated tend to provide a greater

degree of diversification than two securities that are positively correlated, and two securities that are

perfectly positively correlated provide no risk diversification at all. Negative correlation is not an

e. To reconcile the traditional portfolio approach and modern portfolio theory:

(1) Determine how much risk the investor is willing to bear.

©2017 Pearson Education, Inc.

80 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

In using this four-step procedure, we are in effect reconciling the approaches suggested by Walt

and Shane. We are forming a portfolio (though not as large as a mutual fund) to get the benefits of

Case 5.2 Susan Lussier’s Inherited Portfolio: Does It Meet Her Needs?

This case demonstrates that a portfolio designed for one person is not likely to be appropriate for another.

In particular, it emphasizes some of the considerations in designing a portfolio.

a. Susan’s financial position is quite strong: She has a regular $135,000 per year job and also has

inherited a portfolio worth nearly $350,000 and $10,000 in cash. Susan has a good job and does not

have to rely on earnings from her portfolio to fulfill current income needs, at least for the present.

b. Reviewing Susan’s inherited portfolio indicates that current income was her father’s chief objective;

the portfolio’s current yield is nearly 10%. The asset allocation based on the total cost data is heavily

weighted toward bonds: 46% bonds ($158,100/$338,000), 29% common stock ($96,900/$338,000),

c. Since current yield is not an important consideration for Susan, she should revise the portfolio to

include securities with low current yields and high capital appreciation potential. This will enable her

to lower her annual tax liability. Her asset allocation should be shifted to more stocks and fewer bonds

Within each asset category, she should hold higher-risk, capital-appreciation-oriented securities

rather than the income-oriented securities currently held. Since Susan is single and has adequate

current income, she appears to be in a position to justify a higher–risk portfolio. For example, the

©2017 Pearson Education, Inc.

Chapter 5 Modern Portfolio Concepts 81

d. As discussed earlier, the inherited portfolio focuses on current income and capital preservation, rather

than Susan’s objectives of capital gains and tax shelter. She will want to adjust the portfolio to include

more capital appreciation securities, and she may also want to restructure the portfolio to meet

e. The inherited portfolio is a very low-risk portfolio. As mentioned in the response to question c., this is

not a good portfolio for Susan. What Susan really needs is a portfolio offering greater capital

appreciation and, consequently, lower taxable income. Susan should reallocate the assets in the

©2017 Pearson Education, Inc.

82 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

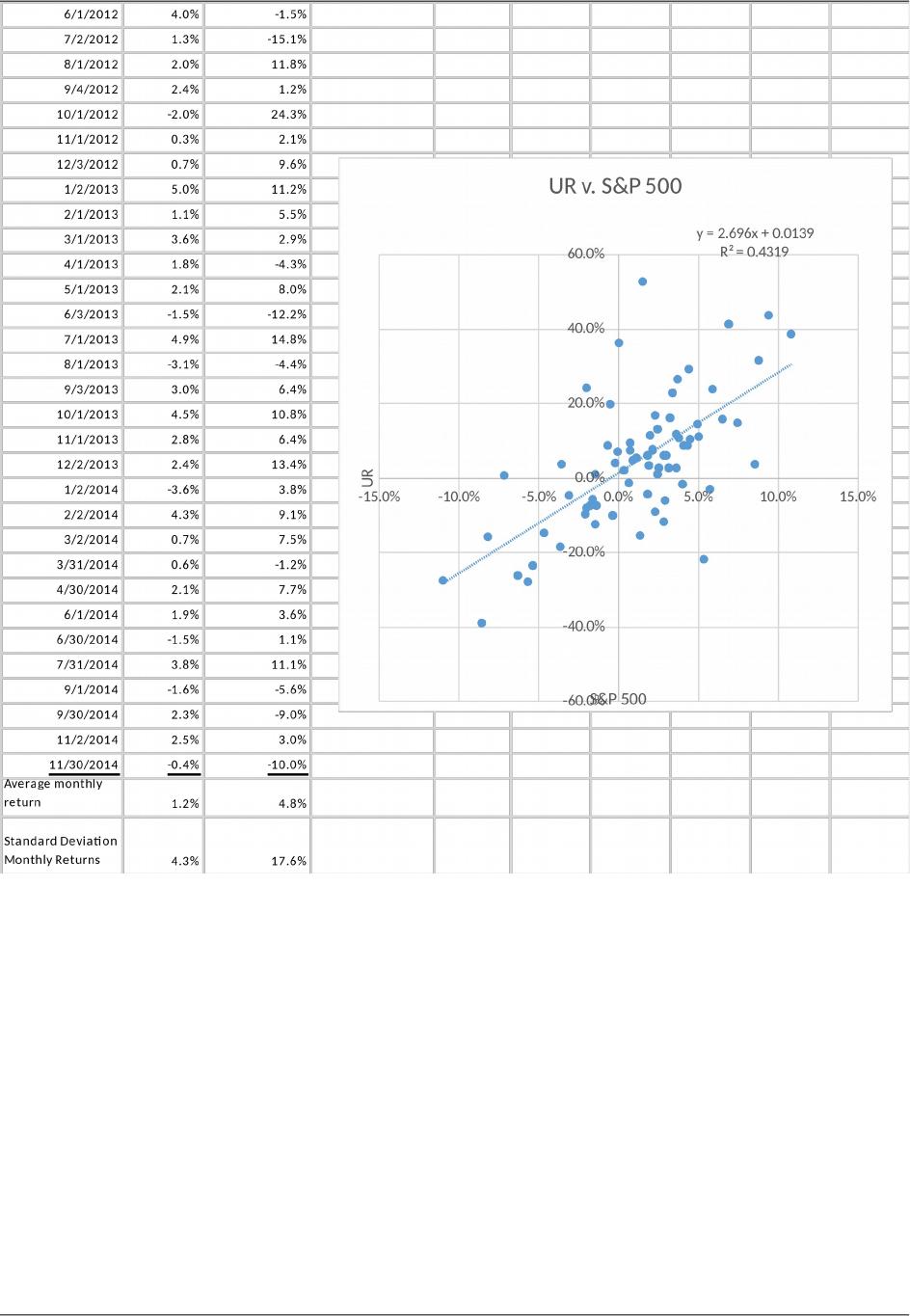

Answer to Chapter-Opening Problem

©2017 Pearson Education, Inc.

Chapter 5 Modern Portfolio Concepts 83

©2017 Pearson Education, Inc.

84 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

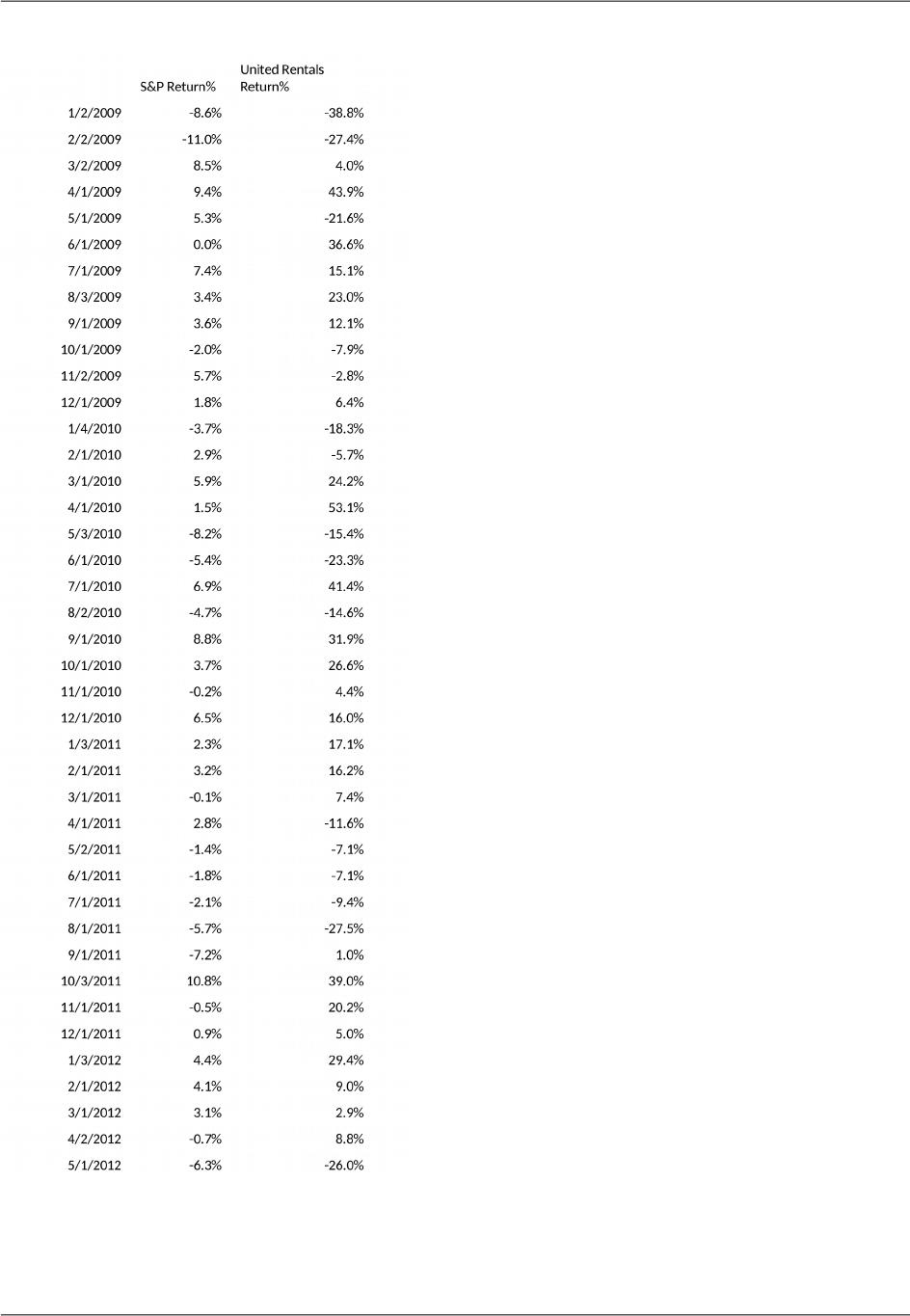

b. Note that the standard deviation for URI is roughly four times larger than the standard deviation

for the index. URI in some months gained more than 30%, and there were other periods in which

the stock lost more than one third of its value. Changes in the Index were not insignificant, +10%

c. Like most stocks, United Rentals is positively correlated with the larger market as represented

here by the S&P 500 Index.

d. Note that the trend line has a rather steep upward slope which is somewhat understated because

Answers to CFA Questions (Part II)

5.1 b

5.4 Portfolio B is not on the efficient frontier. It is inferior to Portfolio A because it has both higher risk

and lower expected return. Portfolio C has higher risk but also higher return than A.

5.7 c

©2017 Pearson Education, Inc.