Chapter 2 Securities Markets and Transactions 15

Solutions to Problems

5.1

Beginning Value Ending Value Return %

2013 $50,000 $55,000 10.0%

2014 $55,000 $58,000 5.5%

5.2

Beginning Value Ending Value Return % Difference Squared

2013 $50,000 $55,000 10.0% 1.20 1.44

2014 $55,000 $58,000 5.5% 3.30 10.89

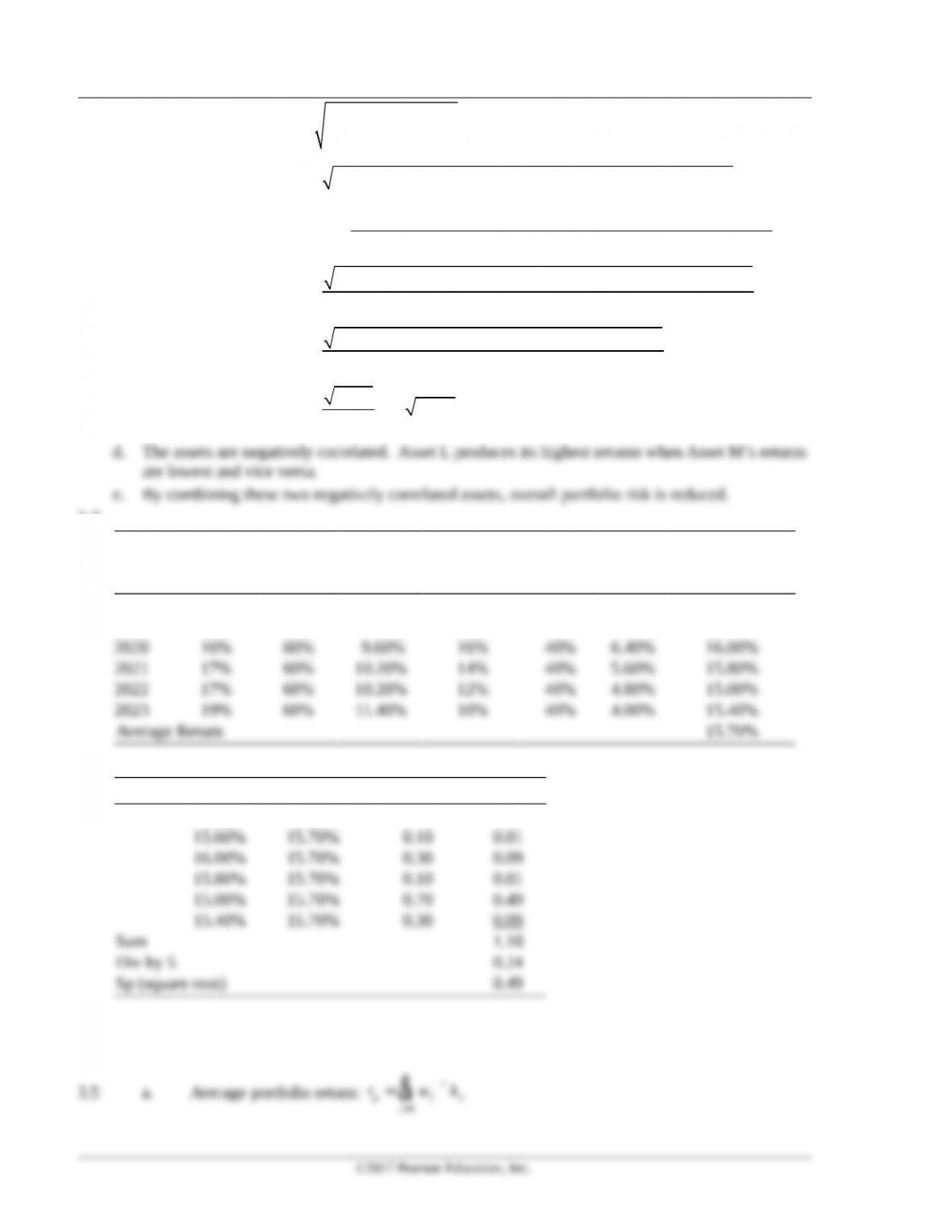

5.3 a. Average portfolio return for each year: rp (wL rL) (wM rM )

Year

Asset L

(wL rL)

Asset M

(wM rM)

Expected

Portfolio Return

rp

2018 (14% 0.40 5.6%) (20% 0.60 12.0%) 17.6%

2019 (14% 0.40 5.6%) (18% 0.60 10.8%) 16.4%

b. Portfolio return:

=

æ ö

= ´ ¸

ç ÷

è ø

+++++

= =

å

1

17.6 16.4 16.0 15.2 14.0 13.6 15.467

6

n

j

j

j

p

r w r n

r

p

©2017 Pearson Education, Inc.

16 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

c. Standard deviation:

p p

i=1

s (r= – ¸ –

å2

) ( 1)

n

r n

2 2 2

222

2 2 2 2 2 2

[(17.6% 15.5%) (16.4% 15.5%) (16.0% 15.5%)

[(15.2% 15.5%) (14.0% 15.5%) (13.6% 15.5%) ]

6 1

[(2.1%) (.9%) (.5%) ( .3%) ( 1.5%) ( 1.9%) ]

5

(4.41% .81% .25% .09% 2.25% 3.61%)

5

11.42

5

p

p

p

p

s

s

s

s

= – + – + –

+ – + – + –

–

+ + + – + – + –

=

+ + + + +

=

= = 2.284 1.511=

d. The assets are negatively correlated. Asset L produces its highest returns when Asset M’s returns

are lowest and vice versa.

e. By combining these two negatively correlated assets, overall portfolio risk is reduced.

5.4

Asset LWeight W rAsset MWeight W r

Expected

Portfolio Return

rp

2018 14% 60% 8.40% 20% 40% 8.00% 16.40%

2019 14% 60% 8.40% 18% 40% 7.20% 15.60%

Return Avg. Return Difference Squared

16.40% 15.70% 0.70 0.49

The average return is almost the same in each case (15.47 versus 15.7), but the standard deviation is

much lower in this portfolio because less weight is given to the more variable asset.

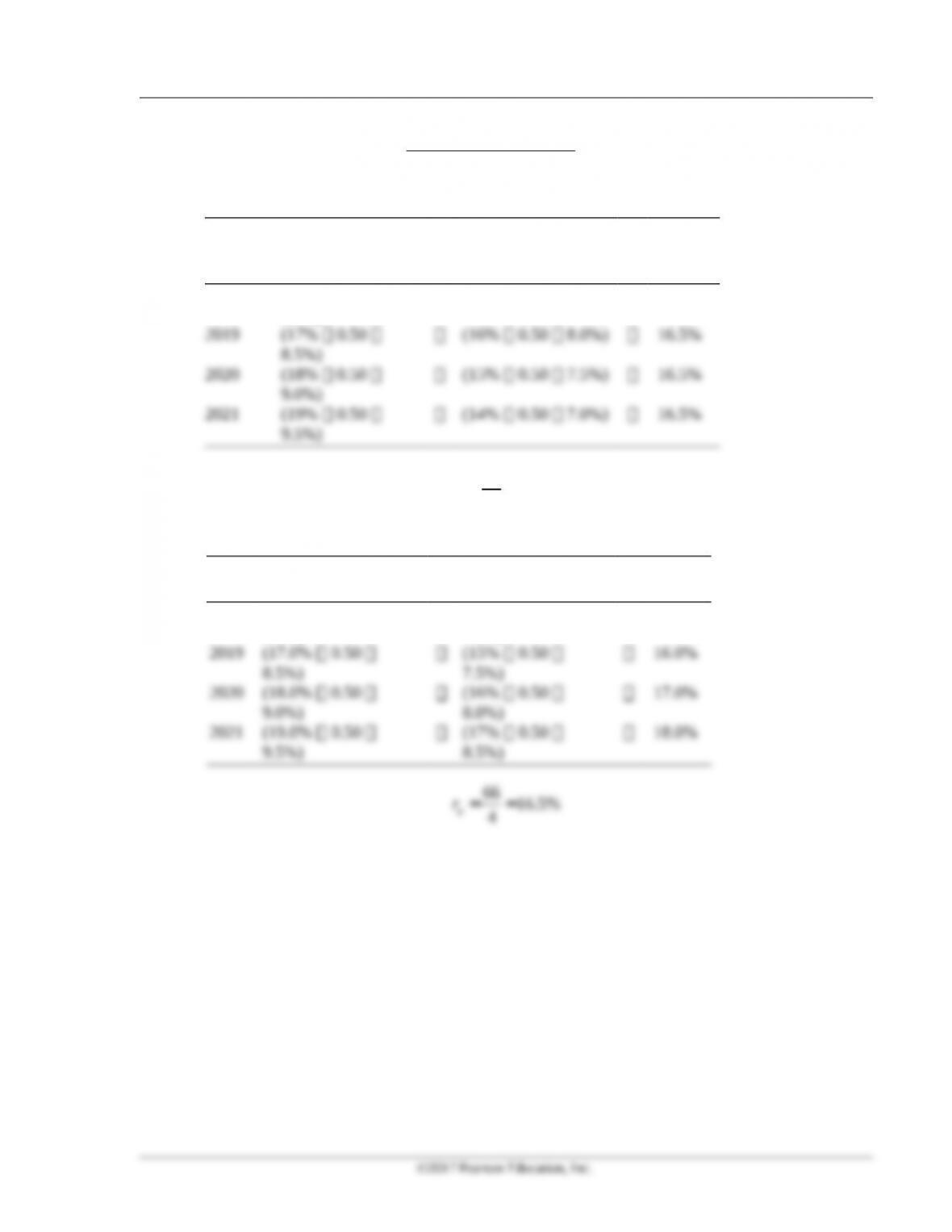

5.5 a. Average portfolio return:

n

p j j

j 1

r w k

=

= ´

å

©2017 Pearson Education, Inc.

Chapter 2 Securities Markets and Transactions 17

Alternative 1: 100% Asset F

+++

= =

16% 17% 18% 19% 17.5%

4

p

r

Alternative 2: 50% Asset F 50% Asset G

Year

Asset F

(wF rF)

Asset G

(wG rG)

Portfolio

Return

rp

2018 (16% 0.50

8.0%)

(17% 0.50 8.5%) 16.5%

= =

66 16.5%

4

p

r

Alternative 3: 50% Asset F 50% Asset H

Year

Asset F

(wF rF)

Asset H

(wH rH)

Portfolio

Return rp

2018 (16.0% 0.50

8.0%)

(14% 0.50

7.0%)

15.0%

9.5%)

8.5%)

= =

66 16.5%

4

p

r

©2017 Pearson Education, Inc.

18 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

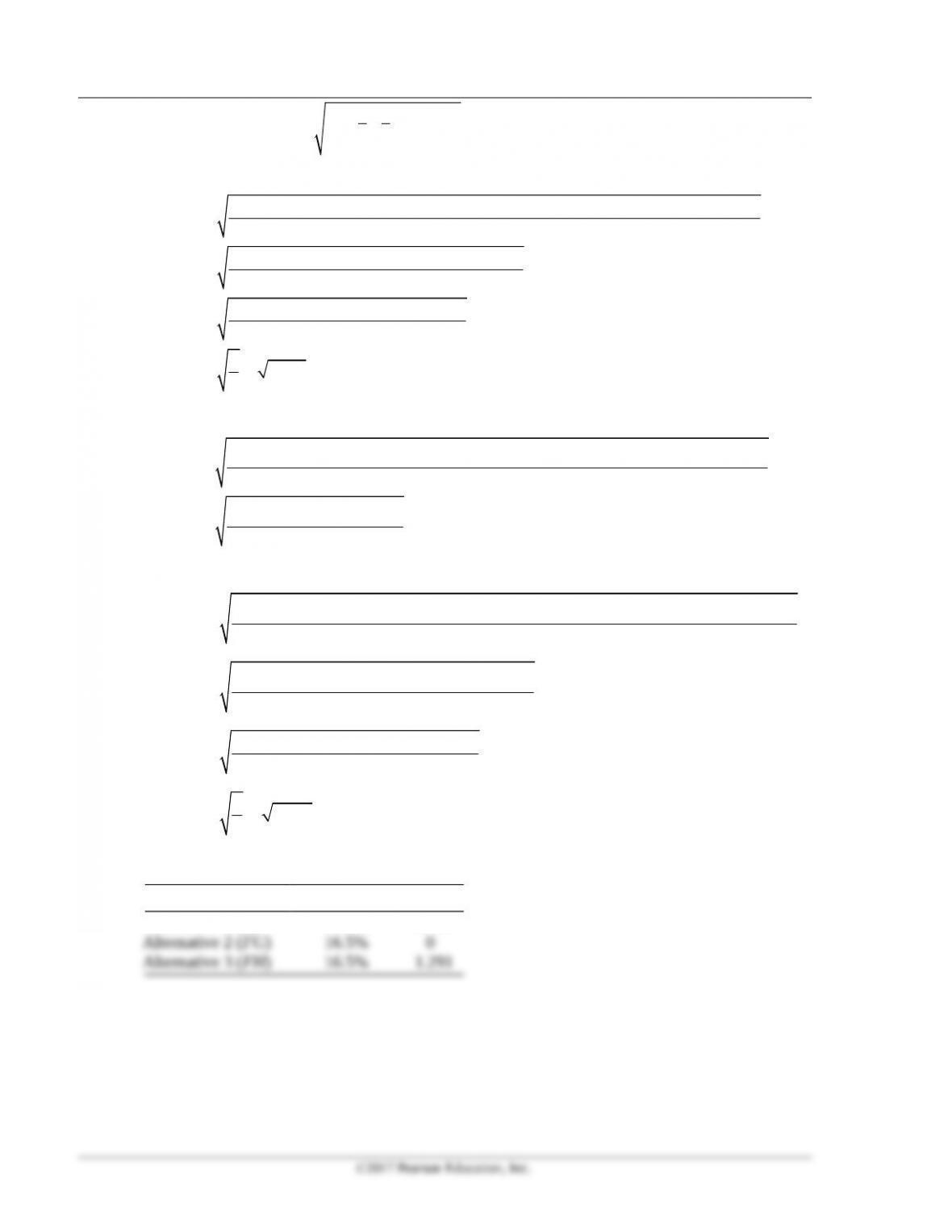

b. Standard deviation:

s

P=(r

i–r)2

i=1

n

å

æ

è

çö

ø

÷

¸(n–1)

(1)

2 2 2

2 2 2 2

[(16.0% 17.5%) + (17.0% 17.5%) (18.0% 17.5%) (19.0% 17.5%)]

4 1

[( 1.5%) + ( 0.5%) (0.5%) (1.5%) ]

3

(2.25% 0.25% 0.25% 2.25%)

3

51.667 1.291

F

F

F

F

s

s

s

s

– – + – + –

=–

– – + +

=

+ + +

=

= = =

3

(2)

2 2 2

2 2 2 2

(16.5% 16.5%) (16.5% 16.5%) (16.5% 16.5%) (16.5% 16.5%)

4 1

(0) (0) (0) (0) 0

3

FG

FG

s

s

é ù

– + – + – + –

ë û

=–

é ù

+++

ë û

= =

(3)

2 2 2 2

2 2 2 2

(15.0% 16.5%) (16.0% 16.5%) (17.0% 16.5%) (18.0% 16.5%)

4 1

( 1.5%) (0.5%) (0.5%) (1.5%)

3

(2.25% 0.25% 0.25% 2.25%)

3

51.667 1.291

3

FH

FH

SH

SH

s

s

s

s

é ù

– + – + – + –

ë û

=–

é ù

– + + +

ë û

=

+++

=

= = =

c. Summary: rp: Average

Portfolio Return rpsp

Alternative 1 (F) 17.5% 1.291

Alternative 2 (FG) 16.5% 0

Alternative 3 (FH) 16.5% 1.291

Chapter 2 Securities Markets and Transactions 19

Since the assets have different average returns, the standard deviation and the correlation patterns

should be used to determine the best portfolio. Alternative 3, the same risk as Alternative 1 and a

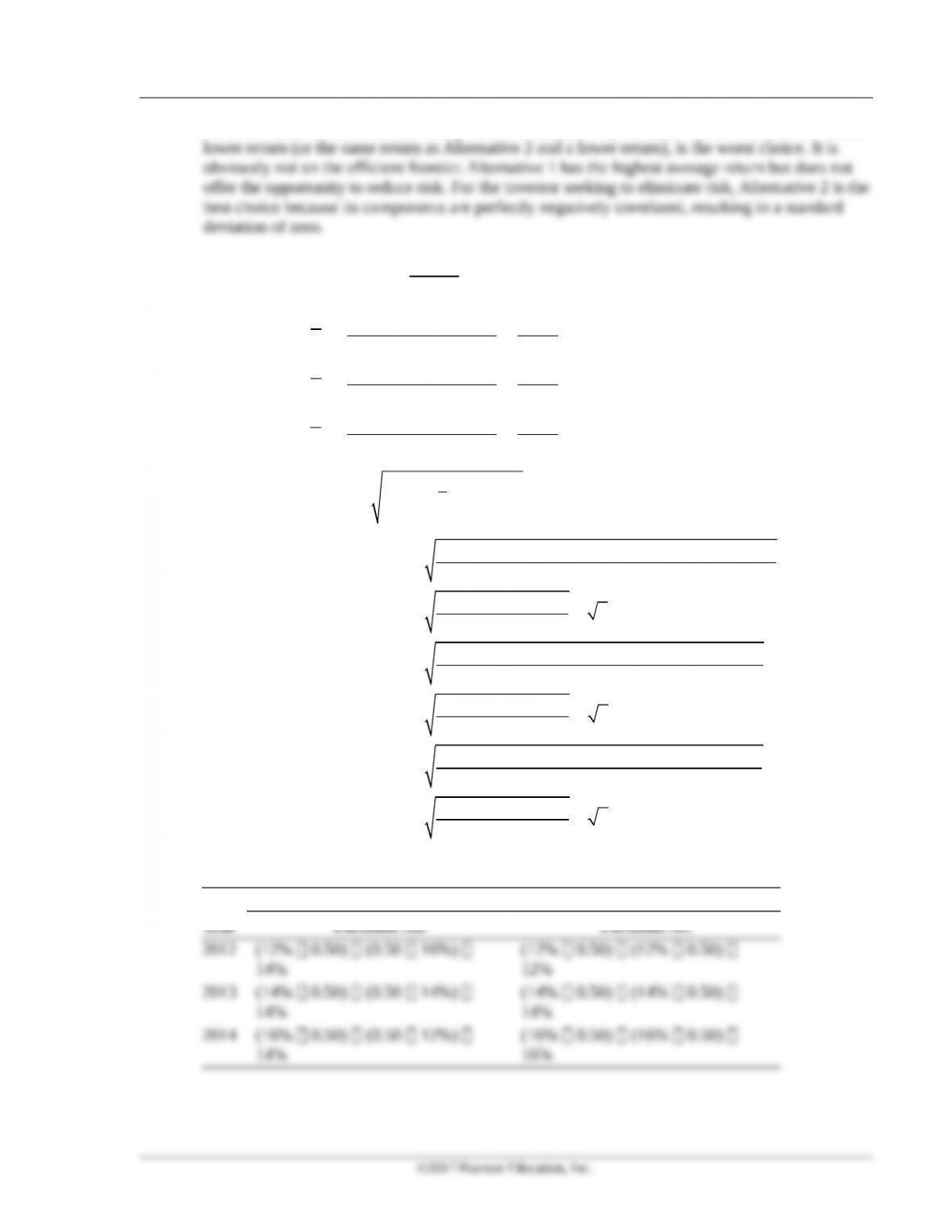

5.6 a. Average return:

returns

3

r=å

12% 14% 16% 42% 14%

3 3

16% 14% 12% 42% 14%

3 3

12% 14% 16% 42% 14%

3 3

A

B

C

r

r

r

+ +

= = =

+ +

= = =

+ +

= = =

b. Standard deviation:

s

i=(r

i–r)

i=1

n

å2

æ

è

çö

ø

÷

¸ (n– 1)

2 2 2

2 2 2

222

[(12.0% 14%) (14% 14%) (16% 14%) ]

3 1

[(4%) (0) (4%)] 4 = 2%

2

[(16% 14%) (14% 14%) (12% 14%) ]

3 1

[(4%) (0) (4%)] 4 2%

2

[(12% 14%) (14% 14%) (16% 14%) ]

3 1

[(4%) (0) (4%)] 4 2%

2

A

A

B

B

C

C

s

s

s

s

s

s

– + – + –

=–

+ +

= =

– + – + –

=–

+ +

= = =

– + – + –

=–

+ +

= = =

c.

Portfolio Return

Year Portfolio AB Portfolio AC

20 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

14% 14% 14% 42% 12% 14% 16% 42%

14% 14%

3 3 3 3

AB AC

r r

+ + + +

= = = = = =

d. Portfolio AB is perfectly negatively correlated.

Portfolio AC is perfectly positively correlated.

e. Standard deviation of portfolios:

2 2 2

222

[(14% 14%) (14% 14%) (14% 14%) ]

3 1

[(0%) (0) (0%)] 0% 0%

2 2

[(12% 14%) (14% 14%) (16% 14%) ]

3 1

[(4%) (0) (4%)] 4 2%

2

AB

AB

AC

AC

s

s

s

s

– + – + –

=–

+ +

= = =

– + – + –

=–

+ +

= = =

5.7

2018 2019 2020

Asset A 12 14 16

Asset B 16 14 12

Asset C 12 14 16

Portfolio Return 13.33 14 14.67

2 2 2

Mean return 1/3 (13.33) 1/3(14) 1/3(14.67) 14%

Standard deviation [(13.33 14) (14 14) (14.67 14) ] / 2

[0.4489 0 0.4489] / 2

0.4489 0.67

= + + =

= – + – + –

= + +

= =

The return would be the same with slightly higher risk. This is because the assets are no longer

perfectly negatively correlated.

5.8 a.5.1 Range of expected return: between 8% and 13%.

Chapter 2 Securities Markets and Transactions 21

5.9

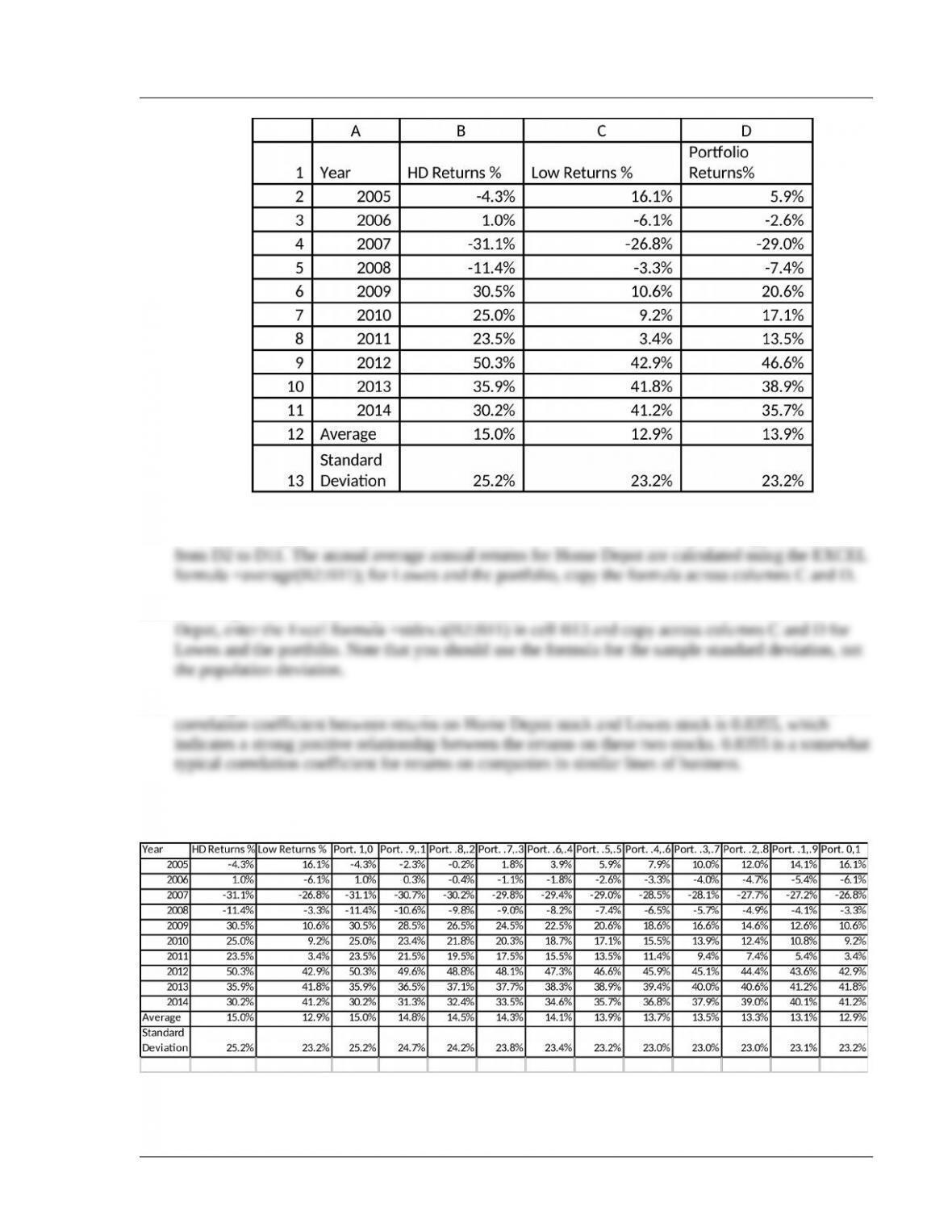

To calculate portfolio returns enter the formula =.5*B2+.5*C2 in cell D2, then copy the formula

5.10 Referring to the solution for problem 9, to calculate the standard deviation of returns for Home

5.11 Using the table in the solution to problem 9, enter the Excel formula =correl(B2:B11,C2:C11). The

5.12 Efficient portfolios start at approximately 0.6 HD and 0.4 L and proceed rightward through an all

Lowes portfolio

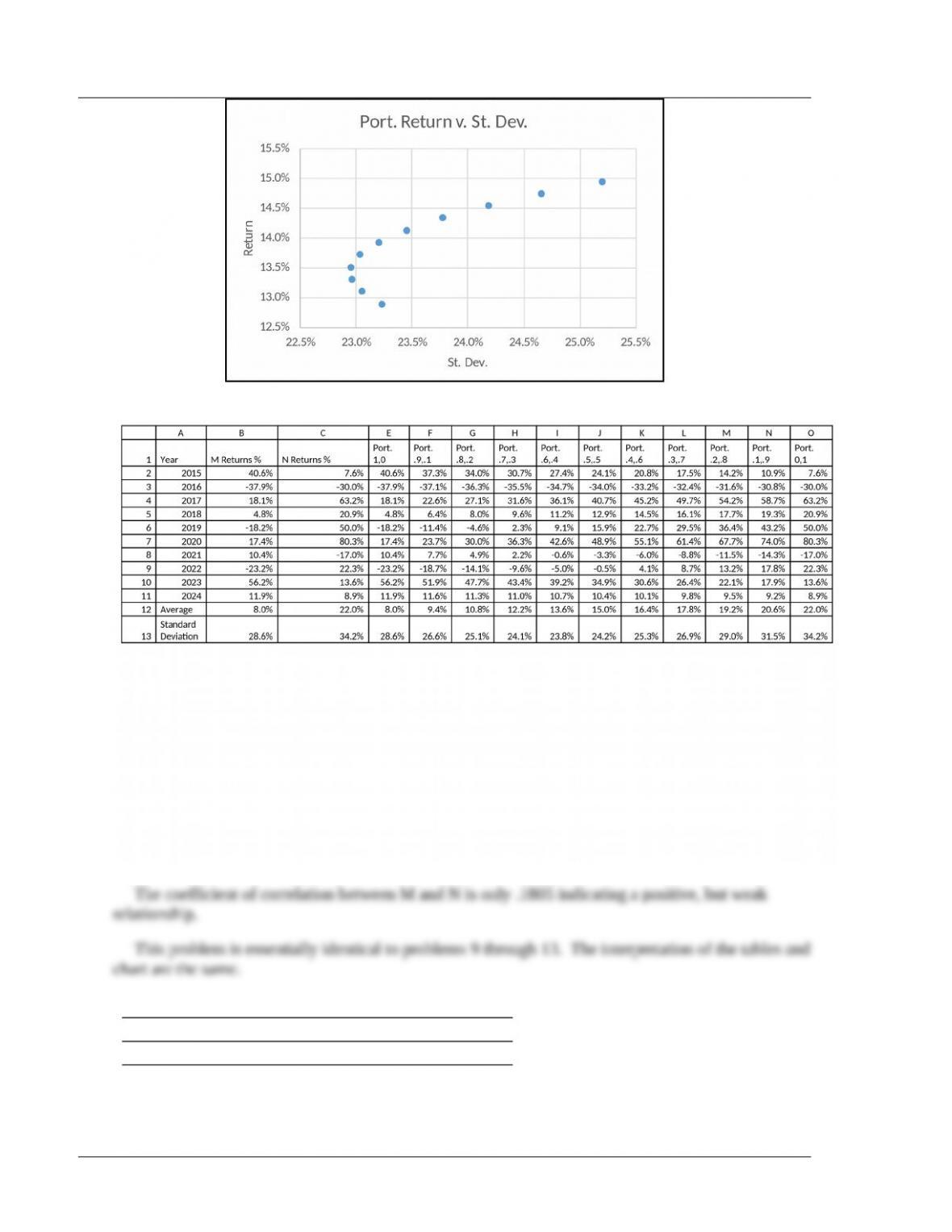

5.13

©2017 Pearson Education, Inc.

22 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

14.

5.15

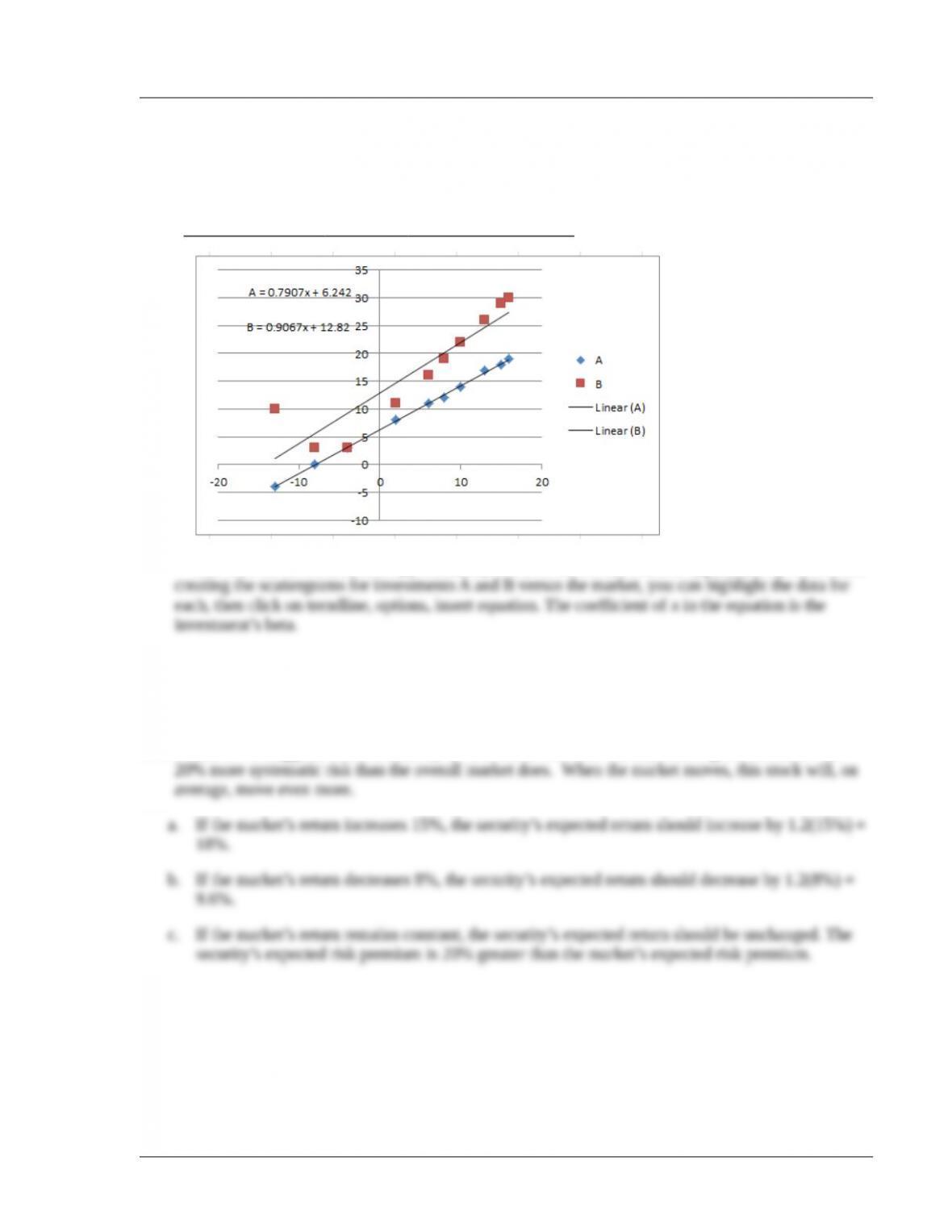

Investment %

Year Market A B

2008 6 11 16

2009 2 8 11

2010 –13 –4 10

©2017 Pearson Education, Inc.

Chapter 2 Securities Markets and Transactions 23

2011 –4 3 3

2012 –8 0 3

2013 16 19 30

2014 10 14 22

2015 15 18 29

2016 8 12 19

2017 13 17 26

The beta for investment A is approximately 0.79; for investment B, it is approximately 0.91. After

5.16 You should buy Buyme because it provides the same return at lower risk (beta).

5.17 If you are very confident that there will be a market rally, you might buy Getit because that stock’s

higher beta would in a higher expected response to the rise in the market.

5.18 A beta of 1.2 suggests that this security is 20% riskier than the market, meaning that the stock has

©2017 Pearson Education, Inc.