252 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

Solutions to Problems

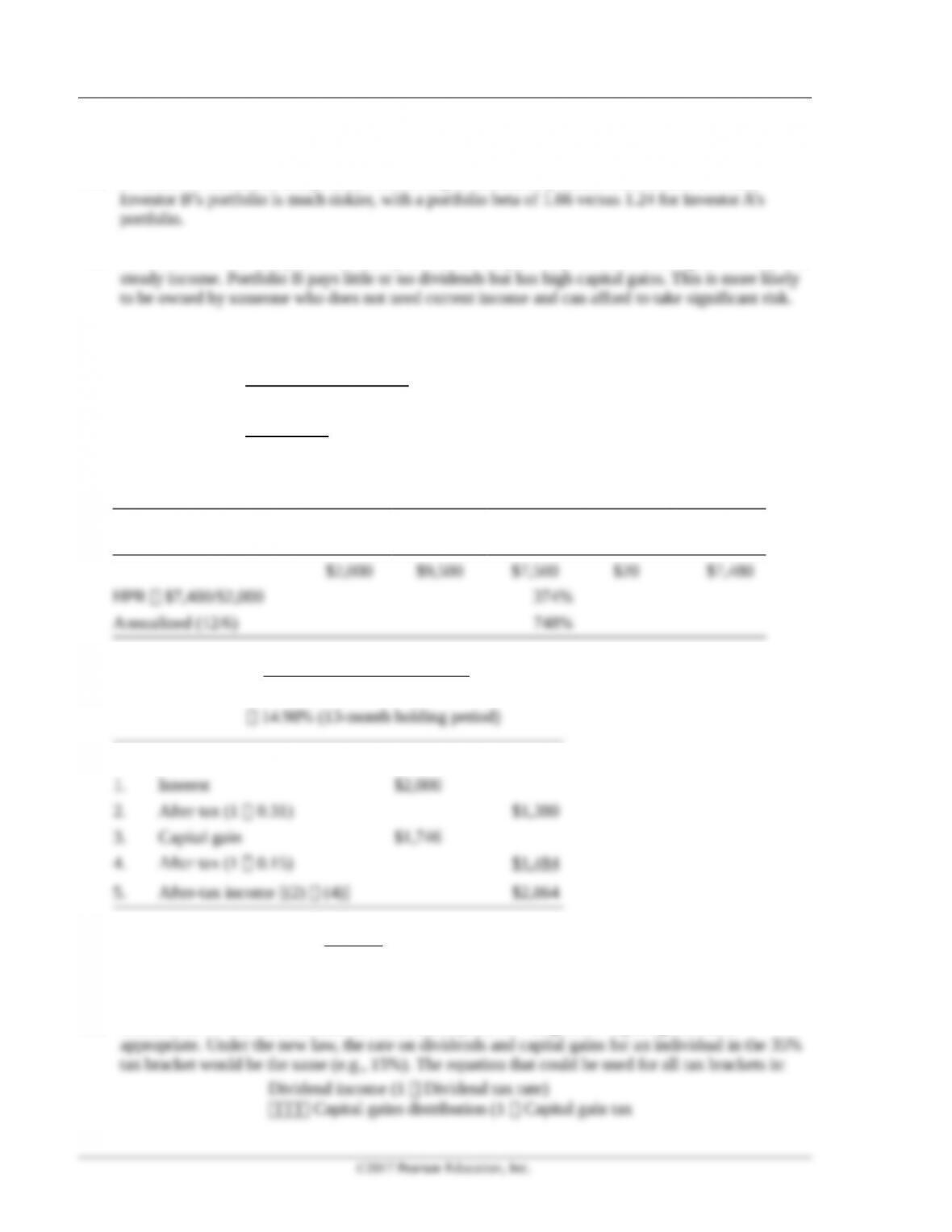

13.1 Investor A would more likely be the retired couple because they would want to have low risk.

13.2 Portfolio A is more likely to be owned by the retired couple. They would be looking for low risk and

13.3 Capital gain $2,500 – $1,762 $738

HPR =Dividend +Capital gain

Purchase price

=$300 +$738

$1,762 =58.9% (for a 15-month holding period)

13.4

A

Cost

B

Proceeds

B–A

Profit

Trading

Cost

Profit

after Costs

13.5 HPR (before tax)

$2,000 ($26,746 $25,000)

$25,000

+ –

14.98% (13-month holding period)

Tax Calculations

Therefore, HPR (after-tax)

$2,864 11.46%*

$25,000 =

For a 13-month holding period

13.6 Because the investment was held for more than a year, the “long-term” capital gains rate is

253 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

rate)

Incorporating the values from Charlotte Smidt’s situation we get:

Pretax HPR = (.32+.38+.15)/8.60 = 9.88%

Chapter 13 Managing Your Own Portfolio 254

c. SMmarket

9.0 6.2 0.298

9.4

–=

d. Based on the SMs, Niki’s portfolio performed better than the market (0.397 versus 0.298 for the

market).

13.12 Treynor’s measure for the portfolio (12.0 – 2.0)/1.3 7.69

13.13 a. Treynor’s measure = (Portfolio return-risk-free rate)/Portfolio beta

b. Anna’s portfolio outperformed Stacey’s, with a TM of 5.88 versus one of 1.25.

13.15 a. Jensen’s measure (JM) [(Total portfolio return Risk-free rate)

Portfolio beta (Market return Risk-free rate)]

b. Chee’s portfolio, with a JM of .14, slightly outperformed Carri’s portfolio, with a JM of

c. Based on its negative JM, Chee’s portfolio has performed worse than the market.

13.16 Measure Fio Family Market

a. SM

12.8 8.1 4.7 11.2 8.1 3.1

13.5 13.5 9.6 9.6

–– –

= =

p F

p

r R

s

The Fio family’s portfolio, with a slightly higher SM, marginally outperformed the market.

b. TM

12.8 8.1 4.7 11.2 8.1 3.1

1.1 1.1 1.0 1.0

–– –

= =

p F

p

r R

b

The Fio family’s portfolio, with a higher TM, outperformed the market.

d. Based on all the above measures, the Fio family’s portfolio performed better than the market.

©2017 Pearson Education, Inc.

255 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

b. To find the number of shares purchased each month, divide $300 by the share price:

Number of Shares

Month Year 1 Year 2

c. Average cost per share

$7,200 $12.17

591.4 =

per share

13.18 Without any action, the speculative portfolio is now worth $25,000, and the MM fund is worth

13.19 You should take no action because the trigger has not been hit.

13.20 The speculative portion now represents 61% of the total, which triggers the rebalance. The total

Time Period Stock Price Shares

MM Mutual

Fund NAV Shares Stock Value MM Value

The total value is now $48,992, and the speculative portfolio is 45% of the total.

Solutions to Case Problems

©2017 Pearson Education, Inc.

Chapter 13 Managing Your Own Portfolio 256

Case 13.1 Assessing the Stalchecks’s Portfolio Performance

This case gives the student an opportunity to compute the holding period return (HPR) for several

a. Before-tax HPRs:

HPR for common stock: HPRt

0

+C CG

V

HPR

($0.20 $0.20 $0.25 $0.25) ($18.75 $17.25)

17.25

+ + + + –

HPR for industrial bonds: HPR

0

+C CG

V

HPR

$92.50 ($963.75 $970) 8.89% for one-year holding period

$970

+ – =

HPR for mutual fund:

($.60 $.50) ($20.02 $19.45)

$19.45

+ + –

HPR for options:

($29,000 $26,000)

$26,000

–

b. For the calculations below, one must make an assumption about how to treat capital gains for tax

Stock (400 shares), reduced rate on dividends:

Industrial bonds (eight bonds):

The bonds generate $92.50 in interest income, which is taxable at 38%. The bonds decreased in value

by $6.25. The total before tax return is therefore (92.50-6.25)/970 = 8.89%. The tax treatment of the

©2017 Pearson Education, Inc.

257 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

Alternatively, we could treat the loss on the bond as a short-term loss, so the after–tax return becomes:

Mutual fund (500 shares), reduced rate on dividend and capital gain distributions:

Options:

HPR (portfolio)

$1,650 $3,835 10.89% for a 1-year holding period

$50,385

+=

d. JM (rp – RF) – [bp (rm – RF)]

(10.89 – 7.20) – [1.2 (10.10 – 7.20)]

3.69 – (1.20 2.90) 3.69 – 3.48 0.21

Using Jensen’s measure, the actual portfolio return is better than the required return because it is

positive. The use of Jensen’s measure is less than ideal because the Stalcheck’s portfolio cuts across

©2017 Pearson Education, Inc.

Chapter 13 Managing Your Own Portfolio 258

e. This question should lead to discussion—it has no pat answer. In general, the portfolio is balanced

between current income and growth. The ratio of current income to capital gain is 43 ($1,650/$3,835);

one might wish to discuss whether or not this is satisfactory. The returns on each of the investments

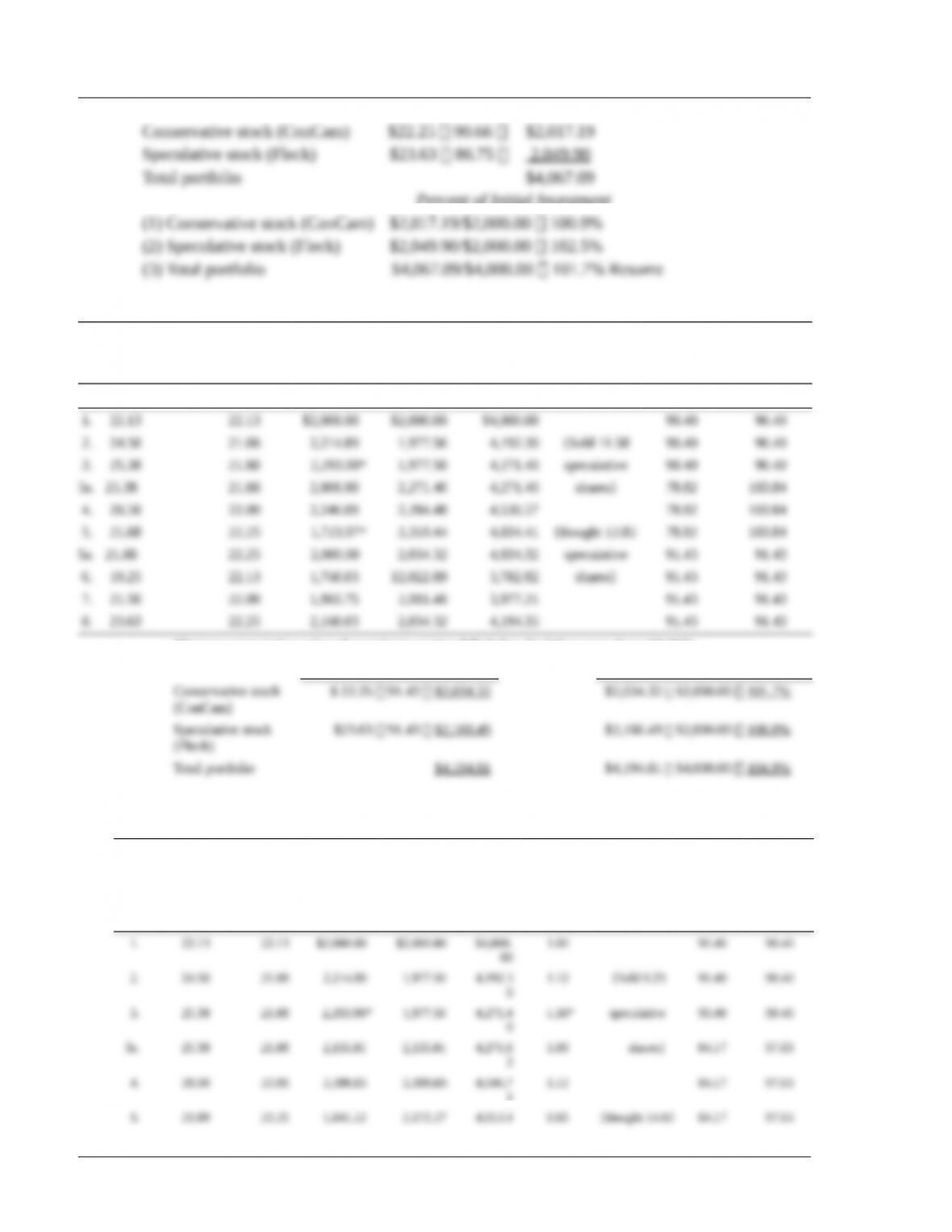

Case 13.2 Evaluating Formula Plans: Charles Spurge’s Approach

This case allows students to use a simplified portfolio to evaluate the four formula plans presented in the

text. For ease in computation and discussion, we have assumed that fractional shares can be purchased.

Instructors may wish to revise the numbers to eliminate fractional shares.

a. Price per share:

End of Period

Period ConCam Fleck

1.

Number of Shares Purchased

ConCam Fleck

Note: Remember, ConCam is the conservative stock, and Fleck is the speculative stock.

©2017 Pearson Education, Inc.

259 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

3. Year-End Value

Percent of Initial Investment

b. Constant-dollar plan: return speculative value (Fleck) to $2,000 when trigger points are reached.

Price of

Speculative

Stock

Price of

Conservative

Stock

Value of

Speculative

Stock

Value of

Conservative

Stock

Total

Value Transactions

Shares in

Speculative

Shares in

Conservative

Fleck ConCam Fleck ConCam

*Trigger points (when value of speculative portion falls below $1,740 or goes above $2,260)

Year-End Value Percent of Initial Investment

c. Constant ratio plan: rebalance to value of speculative portion equal to value of conservative portion

when ratio hits trigger point.

Period

Price of

Speculative

Stock

Price of

Conservative

Stock

Value of

Speculati

ve

Stock

Value of

Conservati

ve

Stock

Total

Value

Ratio of

Speculative

Stock to

Conservati

ve

Stock

Transactio

ns

Shares in

Speculati

ve

Shares in

Conservati

ve

©2017 Pearson Education, Inc.

Chapter 13 Managing Your Own Portfolio 260

9

0

*Trigger points (when ratio of the value of speculative portfolio to value of conservative portfolio falls below 0.84 or exceeds 1.15)

Note: Numbers may not add exactly due to rounding.

Year-End Value Percent of Initial Investment

d. Variable-ratio plan: rebalance speculative portion to 46% of the total portfolio value each time the

upper trigger point is reached; rebalance speculative portion to 50% each time the lower trigger

point is reached.

Period

Price of

Speculative

Stock

Price of

Conservative

Stock

Value of

Speculative

Stock

Value of

Conservativ

e

Stock

Total

Portfolio

Value Ratio Transactions

Shares in

Speculati

ve

Shares in

Conservativ

e

*Trigger points (when ratio of the value of speculative portfolio to the total portfolio value either exceeds 54%, the upper trigger point, or

falls below 38%, the lower trigger point).

Year-End Value Percent of Initial Investment

e. Formula plan:

Dollar Cost

Averaging

Constant

Dollar

Constant

Ratio

Variable

Ratio

Year-End Portfolio

Value as a Percentage

Number of Transactions

©2017 Pearson Education, Inc.

261 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

In this illustration, the formula plans have performed much the way one would expect. The most

The other three plans show increasing year–end values as one moves from the lowest activity and

risk—the constant-dollar plan—to highest activity and risk—the variable-ratio plan. While the

Answers to CFA Questions (Part V)

©2017 Pearson Education, Inc.