Chapter 12 Mutual Funds and Exchange-Traded Funds 233

Solutions to Problems

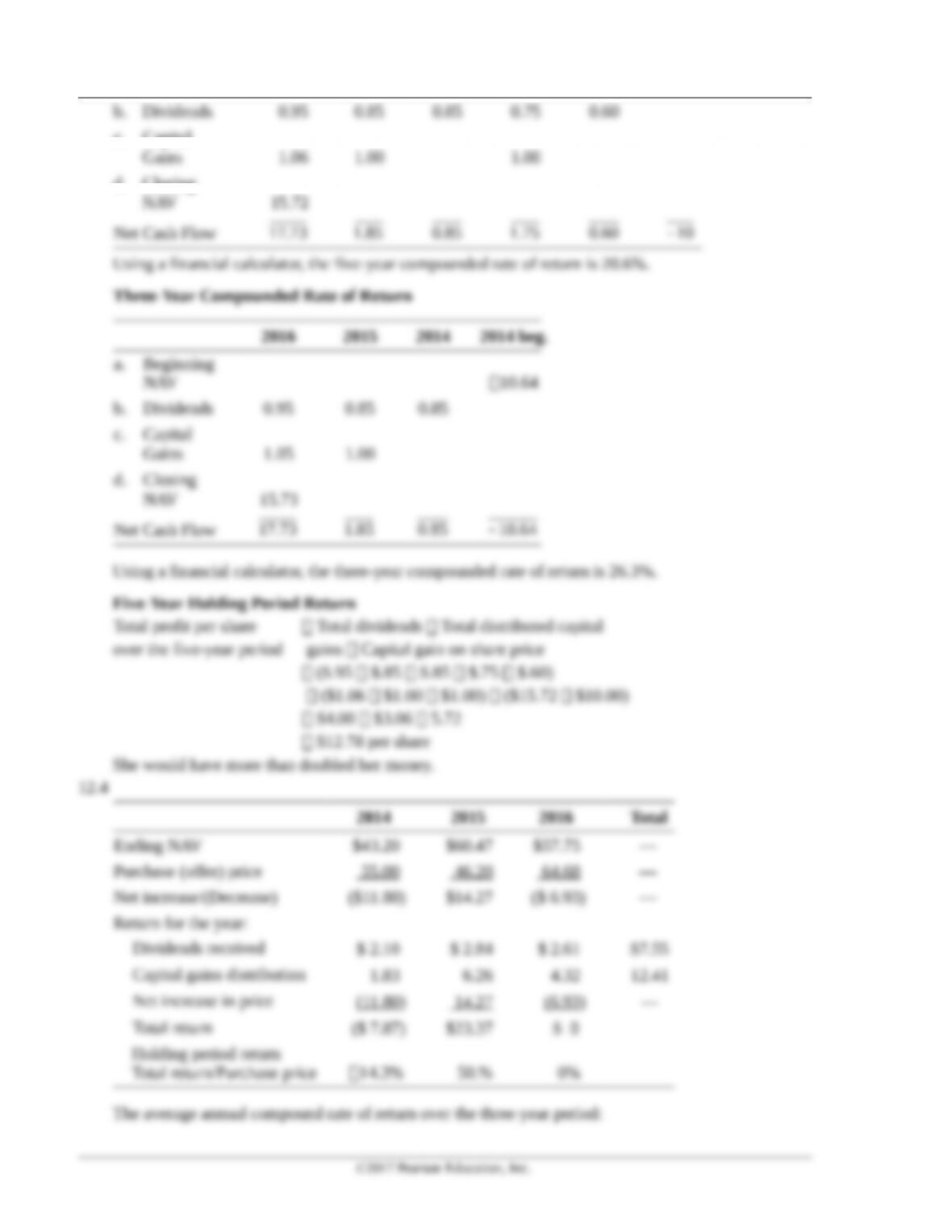

12.1 a. Return for the year (all changes on a per share basis):

b. When all dividends and capital gains distributions are reinvested into additional shares of the

fund ($8.75/share):

234 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

c. Capital

d. Closing

Chapter 12 Mutual Funds and Exchange-Traded Funds 235

Three-Year Compounded Rate of Return

2014 beg. 2014

end

2015 2016

236 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

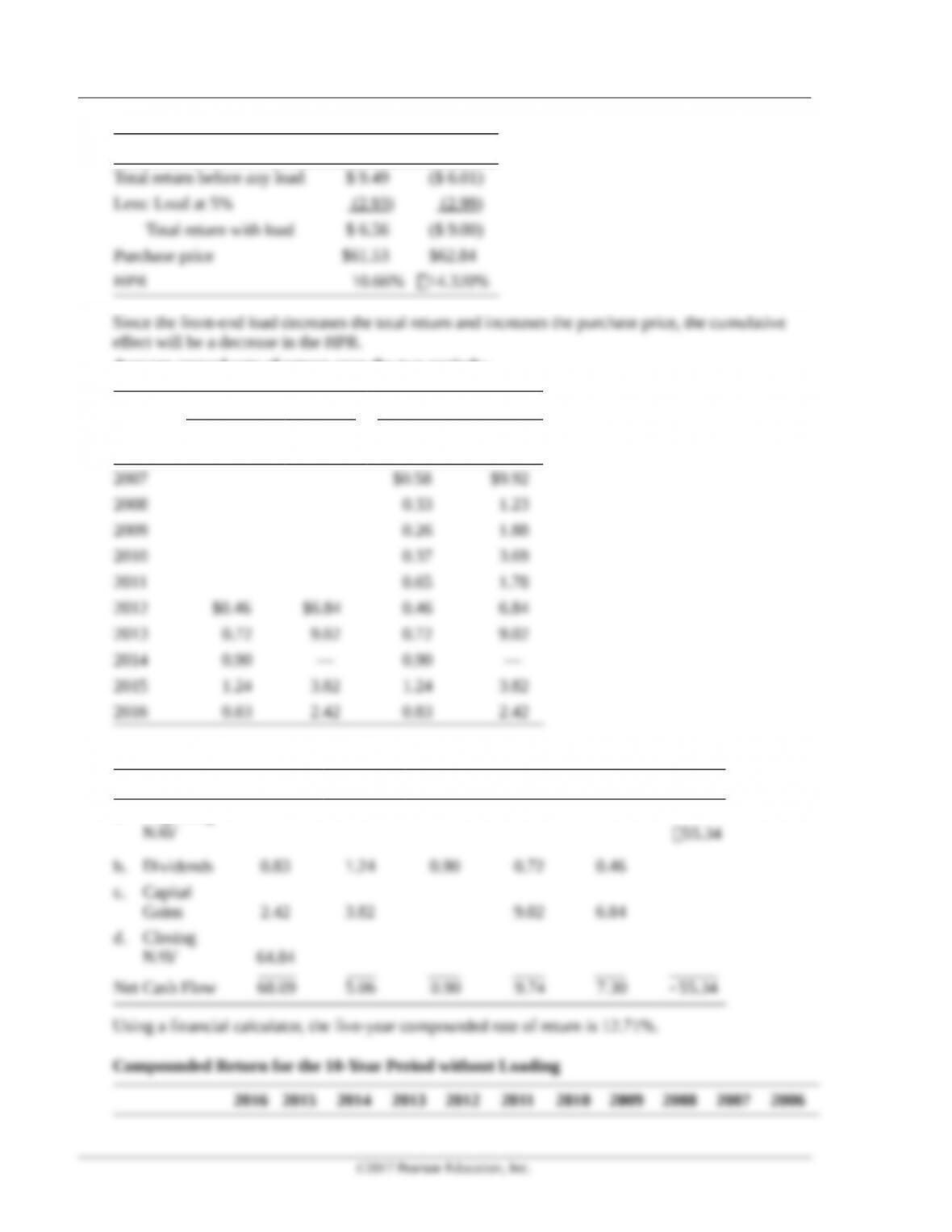

With a front-end load of 5% on NAV, the Purchase price Beginning NAV 1.05.

2016 2013

Average annual rate of return over the two periods:

2012–16 2007–16

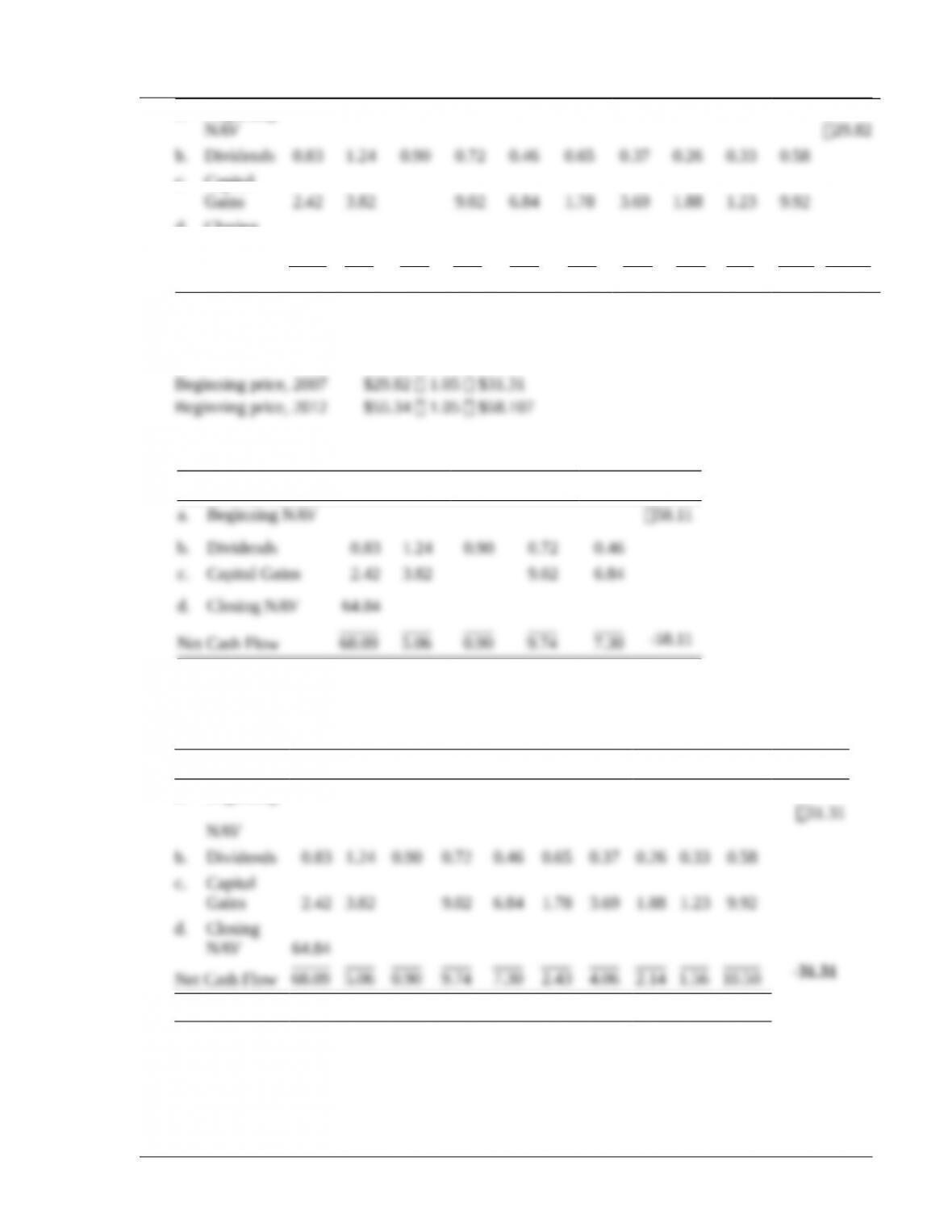

Dividends

Capital

Gains Dividends

Capital

Gains

2008 0.33 1.23

2009 0.26 1.88

2010 0.37 3.69

2011 0.65 1.78

2012 $0.46 $6.84 0.46 6.84

2013 0.72 9.02 0.72 9.02

Chapter 12 Mutual Funds and Exchange-Traded Funds 237

a. Beginning

c. Capital

d. Closing

NAV 64.84

Net Cash Flow

68.09

5.06

0.90

9.74

7.30

2.43

4.06

2.14

1.56

10.50

29.82–

Using a financial calculator, the 10-year compounded rate of return is 21%.

If the fund charges a 5% load on NAV, the beginning price would be different and that would change

the yield:

Compounded Return for the Five-Year Period with Loading

2016 2015 2014 2013 2012 2011

Net Cash Flow

68.09

5.06

0.90

9.74

7.30

Using a financial calculator, the five-year compounded rate of return is 11.36%.

Compounded Return for the 10-Year Period with Loading

2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006

a. Beginning

Net Cash Flow

68.09

5.06

0.90

9.74

7.30

2.43

4.06

2.14

1.56

10.50

Using a financial calculator, the 10-year compounded rate of return is 20.03%.

©2017 Pearson Education, Inc.

238 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

12.6 There is no set solution to this problem since the answers will vary with the funds selected by the

12.7 a. NAV-based HPR for the year:

$0.40 $0.95 ($11.69 $10.40)

$10.40

25.38%

+ + –

=

=

b. Market-based HPR for the year:

(i) Beginning period market price:

(Market price NAV)

Premium (or discount) NAV

(Market price $10.40)

0.18 $10.40

$8.53 Market price

–

=

–

– =

=

(ii) Ending period market price:

(Market price $11.69)

0.04 $11.69

$12.16 Market price

–

+ =

=

(iii)

($0.40 $0.95) ($12.16 $8.53)

HPR $8.53

HPR 58.38%

+ + –

=

=

The market discount applied to the purchase price, and the market premium applied to the

c. Market-based HPR for the year:

(i) Beginning period market price:

(Market price $10.40)

0.18 $10.40

$12.27 Market price

–

+ =

=

(ii) Ending period market price:

(Market price $11.69)

0.04 $11.69

$11.22 Market price

–

+ =

=

©2017 Pearson Education, Inc.

Chapter 12 Mutual Funds and Exchange-Traded Funds 239

(iii)

($0.40 $.95) ($11.22 $12.27)

HPR $12.27

HPR 2.44%

+ + –

=

=

Because the premium applied to the purchase price and the discount applied to the ending

12.8 a. NAV-based HPR for the year:

$1.20 $0.90 ($9.25 $7.50)

$7.50

51.33%

+ + –

=

=

b.

(Market price NAV)

Beginning period premium = NAV

($7.75 $7.50)

$7.50

3.33%

–

–

=

=

($9.00 $9.25)

End of the period premium $9.25

2.70%

–

=

=–

c. Market-based HPR for the period:

($1.20 $.90) ($9.00 $7.75)

HPR $7.75

43.20%

+ + –

=

=

The market premium increased the purchase price, and the market discount reduced the sale

12.9 This is a single cash flow IRR problem. Initial investment is $20,000. Three years later, the value is

$25,201 ($1,100$22.91).

Calculator solution:

12.10 Here, there is an additional 3% added to the cost of the initial purchase. The initial investment

becomes ($20,000 1.03) $20,600.

12.11 The problem assumes that Oh Yes Mutual Fund is a no-load fund.

Ending Beginning

HPR [Div Dist Gains Dist (NAV NAV )]/NAVBeginning

HPR [$1.50 $2.00 ($26.00 $25.00)]/$25.00

$4.50 / $25.00 0.18 or 18%

= + + –

= + + –

= =

12.12 The problem assumes that Oh Yes Mutual Fund carries a 2% load. If the initial NAV was $25.00, the

240 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

Ending

HPR [Div Dist Gains Dist (NAV Initial cost)]/Initial cost

HPR [$1.50 $2.00 ($26.00 $25.50)]/$25.50

$4.00 / $25.50 0.157 or 15.7%

= + + –

= + + –

= =

12.13 The fund is trading at a discount because the market price is below the NAV. (Share price NAV)/

NAV ($20.00 $22.5)/$22.50 $2.50/$22.50 0.1111 or 11.11%.

12.14 Taxes will be 15% on half of the distribution (dividends) and 25% on the other half (interest income).

Solutions to Case Problems

Case 12.1 Reverend Mark Thomas Ponders Mutual Funds

This case enables the student to deal with the issues included in putting together a long-term mutual fund

program that will meet some pretty specific investment objectives.

a. Mark needs to accumulate capital and needs an investment that will serve as a storehouse of value.

Given his lack of investment expertise and the small sum he has to invest, mutual funds would be an

b. As indicated earlier in the text, certain prerequisites must be satisfied prior to entering an investment

program. Mark can cover the necessities, but he should be sure that he also has adequate insurance

c. Mark’s specific investment needs are retirement and college education for his child. Both objectives

Case 12.2 Calvin Jacobs Seeks the Good Life

©2017 Pearson Education, Inc.

Chapter 12 Mutual Funds and Exchange-Traded Funds 241

a. Given Calvin’s existing financial condition, he can take on a certain amount of risk. Also, Calvin

wants to consume immediately. Although he seems financially capable of assuming increased risk to

generate a higher return, he has also stated that he “intends to be around for a long time.” However,

b. The factors that must be taken into consideration are (1) Calvin’s existing wealth level, (2) his ability

to take on risk, (3) his demand for current income, and (4) his desire for capital preservation. These

considerations will clearly dictate the kinds of mutual funds Calvin should select. His demand for

c. Calvin is clearly not in need of any savings plan. He already has a considerable amount of savings

and is able to manage things well on his own. What Calvin needs is a withdrawal plan because he

d. Fund earns 10%. Starting balance is $100,000. At the end of the first year, this would be

worth $100,000 1.10 $110,000. Let us assume (for ease of calculation) that Calvin withdraws

$15,000 per year at the end of each year and compute the value after he makes his fifth withdrawal:

Year

Initial

Sum

Ending

Sum

Less Annual

Withdrawal

Balance

End of Year

Thus, at a 10% earning rate, the value of his $100,000 investment will steadily decline to $69,474 by

the end of the fifth year. The reason for this is simple: he’s taking out more than he’s earning. This

will eventually (between 11 and 12 years), result in total capital consumption, something Calvin

©2017 Pearson Education, Inc.

242 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

Answer to Chapter-Opening Problem

©2017 Pearson Education, Inc.