Chapter 2 Securities Markets and Transactions 15

11.21 Expected Yield

N = 3

11.22

a. Yield to Maturity b. Yield to Maturity c. Yield to Maturity

a. Yield to Call b. Yield to Call c. Yield to Call

©2017 Pearson Education, Inc.

16 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

Of course it is worth noting here that because bonds A and C are trading well below their

11.23 Modified duration Macaulay duration/(1 Yield) 9.5/1.075 8.84

11.24 Percent change in bond price 1 Modified duration

Change in interest rates

Modified duration Macaulay duration/(1 Yield)

11.25 The prices of the bond at yields of 6.5%, 7.0% and 7.5% compounded semiannually are:

©2017 Pearson Education, Inc.

Chapter 2 Securities Markets and Transactions 17

938.62 831.74 12.11 years

2 882.72 0.005

ED –

= =

´ ´

The effective duration is 12.11 years.

11.26 To calculate the duration of the bond, first calculate the bond’s current market price:

Bond terms: 10% coupon, 20 years, 8% YTM

Price

N = 20

I = 8

PMT = 100

FV = 1000

CPT

PV= –1,196.36

In the table below, start by listing the times when cash flow is paid. IN the next column, write down

the cash flow paid at each time. Next, calculate the present value of each cash payment by

PV of CF as Column 1

Time Cash Flow PV of CF % of bond price × Column 4

©2017 Pearson Education, Inc.

18 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

PV of CF as Column 1

Time Cash Flow PV of CF % of bond price × Column 4

Modified duration

Duration in years

1 Yield-to-maturity+

% change in bond price 1 Modified duration Change in interest rates

1 9.42 1% 9.42%

If market yields rise 1%, the modified duration calculation predicts that the price of the bond will

Assuming that the bond’s yield does rise to 9%,we can use a calculator or Excel to calculate the

bond’s price. In Excel we would use =pv(.09,20,100,1000) to find the price of $1,091.29. This

©2017 Pearson Education, Inc.

Chapter 2 Securities Markets and Transactions 19

11.27 This question is about bond price volatility. We need to measure the responsiveness of a bond’s

Modified duration

Duration in years

1 Yield-to-maturity+

a. Bond with duration of 8.46 years with YTM of 7.5%:

Modified duration

8.46 7.87%

1 .075 =

+

b. Bond with duration of 9.30 years with YTM of 10%:

Modified duration

9.30 8.45%

1 .10 =

+

c. Bond with duration of 8.75 years with YTM of 5.75%:

Modified duration

8.75 8.27%

1 .0575 =

+

Bond (b) offers the potential for maximum capital appreciation. To maximize gains, this bond

should be selected over the others.

Note: This question can be answered directly by looking at the modified duration. For a given

11.28 Current price of the bonds at 9% market interest:

Zero-coupon bond:

Bond 1 Bond 2

Capital gains:

©2017 Pearson Education, Inc.

20 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

To maximize the dollar value of capital gains per bond, buy the 7.5%, 20-year bond, but this doesn’t

HPR

Interest Capital gains

Purchase price

+

Based on holding period return, Stacy should purchase the zero-coupon bond.

We know from Chapter 10 that prices of bonds with lower coupons and/or longer maturities will

The duration of a zero-coupon bond is equal to its actual maturity, while the duration of a

11.29 There is an error in this problem in one printing of the textbook. The prices and yields given for

each bond are not consistent with each other. A solution may be developed by taking the yield as

given and recalculating the price (this is the approach taken below) or by taking the price as given

and recalculating the yield. The bonds we are comparing have these characteristics:

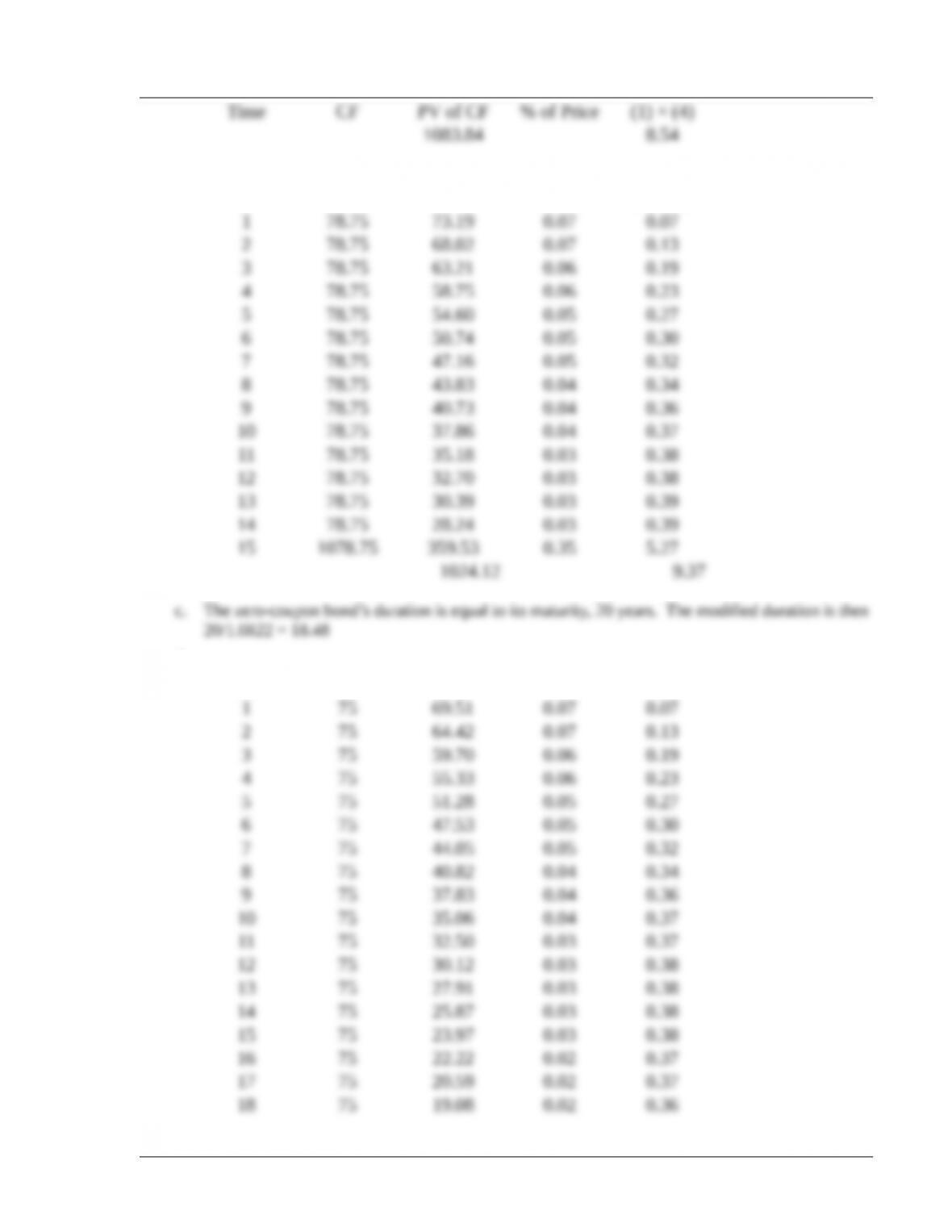

a. 8.5%, 13-year, ytm = 7.47%, price = $1,083.84, duration = 8.54, modified duration = 7.94

b. 7.875%, 15-year, ytm = 7.6%, price = $1,024.12, duration = 9.37, mod. duration = 8.71

c. 0%, 20-year, ytm = 8.22%, price = $205.99, duration = 20, modified duration = 18.48

d. 7.5%, 24-year, ytm = 7.9%, price = $957.53, duration = 11.56, modified duration = 10.72

The tables below show the calculations for the price and duration for each bond. To find modified

duration, simply divide the duration by 1+ytm.

a.

Time CF PV of CF % of Price (1) × (4)

©2017 Pearson Education, Inc.

Chapter 2 Securities Markets and Transactions 21

b.

Time CF PV of CF % of Price (1) × (4)

d.

Time CF PV of CF % of Price (1) (4)

©2017 Pearson Education, Inc.

22 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

Time CF PV of CF % of Price (1) (4)

b. When Elliot invests $250,000 in each of the four bonds, the weighted average duration of the

portfolio is:

(1) (2)

Bond

Particulars

(3)

Amount

Invested

(4)

Weight

(5)

Bond

Duration

(6)

Weighted

Duration

(4) (5)

c. When Elliot invests $360,000 each into Bonds 1 and 3, and $140,000 each into Bonds 2 and 4,

the weighted average duration of the bond portfolio is:

(1) (2)

Bond

Particulars

(3)

Amount

Invested

(4)

Weight

(5)

Bond

Duration

(6)

Weighted

Duration

(4) (5)

d. Portfolio (c) has a higher duration than portfolio (b). If rates are about to rise, then it is safer to

©2017 Pearson Education, Inc.